Kuaishou's Q1 Revenue Increases But Profits Decline: 26% Profit Drop, Kling AI Revenue Surges 300% to Become Second Growth Engine

05/28 2026

05/28 2026

617

617

A Transformation-Phase Report Card of 'Revenue Growth Under Pressure'

Author|Jin Yingshi

On May 27, Kuaishou-W (01024.HK) released its Q1 2026 financial results, showing a 3.4% YoY increase in revenue but a 26.3% YoY decline in adjusted net profit, indicating significant pressure on profitability. Additionally, the explosive growth of Kling AI's commercialization, the acceleration of the advertising business against the trend as a core pillar, and the YoY decline in live streaming revenue with continued ecosystem optimization, these three signals outline Kuaishou's true situation in the deepening phase of its AI strategy, actively exchanging short-term profits for long-term competitiveness.

Against a backdrop of a complex and volatile macroeconomic environment, this financial report exhibits distinct characteristics of a 'transformation phase.'

Core Financial Data: Steady Revenue, Profit Under Pressure

Overall, Kuaishou's Q1 2026 performance shows revenue growth without profit increase. Specifically, total revenue for the quarter was RMB 33.716 billion, up 3.4% YoY; adjusted net profit was RMB 3.374 billion, down 26.3% YoY, with an adjusted net profit margin of 10.0%, a 4 percentage point decrease from 14.0% in the same period in 2025.

In terms of gross profit, Q1 gross profit was RMB 17.249 billion, down 3.1% YoY, with a gross margin of 51.2%, a 3.4 percentage point decrease from 54.6% in the same period in 2025, mainly affected by rising AI computing costs and increased sales costs.

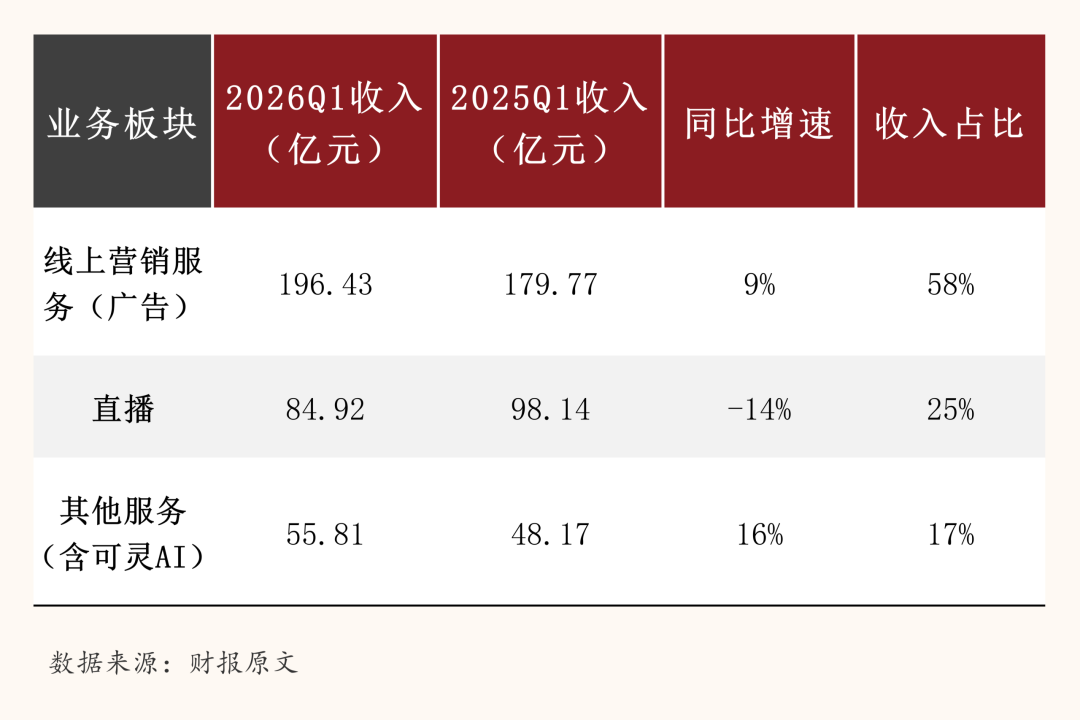

Breakdown of Revenue by Business Segment:

The advertising business, with a 9.3% growth rate, became the only core business to achieve relatively rapid growth, while live streaming revenue declined by 13.5% YoY, being the main factor dragging down overall revenue growth.

From the expense side, Kuaishou's Q1 sales and marketing expenses were RMB 10.333 billion, up 4.4% YoY, accounting for 30.6% of total revenue, a slight increase from 30.4% in the same period in 2025. R&D expenses were RMB 3.621 billion, up 9.8% YoY, accounting for 10.7% of total revenue, an increase from 10.1% in the same period in 2025, reflecting continued increases in AI-related R&D investment. Income tax expenses surged from RMB 258 million in Q1 2025 to RMB 504 million, also being one of the important reasons for the pressure on net profit.

The reasons for the 'revenue growth without profit increase' this quarter lie in the increase in AI computing investment pushing up sales costs (up 11.1% YoY), with a 3.4 percentage point decline in gross margin; meanwhile, the growth rate of R&D expenses (9.8%) was higher than the revenue growth rate (3.4%), and income tax expenses nearly doubled. This is the Periodic cost (phased cost) of Kuaishou's proactive increase in AI strategic investment, and whether it can be compensate (offset) by accelerated AI monetization in subsequent quarters is the core issue of market concern.

Kling AI Revenue Surges, Second Growth Curve Takes Shape

This is the biggest highlight of this quarter's financial report and the core focus supporting market confidence.

In Q1 2026, Kling AI's single-quarter revenue exceeded RMB 650 million, up over 300% YoY. As of March 2026, Kling AI's annualized revenue run rate (ARR) has approached $500 million, a figure far exceeding previous market expectations, fully validating the feasibility of Kling AI's commercialization path.

From a product perspective, Kling AI continues to maintain its technological leadership. The recently launched 'Baseball Live' special effects feature swept global social platforms, propelling Kling AI to the top of the App Store overall charts in 42 countries and regions, including Brazil and Germany, with its global influence continuing to expand.

From a commercialization path perspective, Kling AI's monetization has formed a diversified layout: C-end paid subscriptions continue to expand, with strong willingness to pay among creator groups; B-end enterprise services cover multiple scenarios such as advertising marketing and content creation; in-platform circulation empowerment effects are significant. AIGC short video marketing material consumption now accounts for 10% of the platform's total online short video marketing consumption, with AI-empowered live streaming incremental GMV exceeding RMB 10 million daily, and comic series daily marketing consumption peaking at over RMB 20 million.

The strategic value of Kling AI lies not only in its direct revenue contribution but also in its 'efficiency multiplication' effect on Kuaishou's entire commercial ecosystem. With ARR approaching $500 million, Kling AI is becoming the core driver of Kuaishou's valuation logic shift.

Advertising Business Accelerates Against the Trend, Becoming Core Revenue Pillar

Against a backdrop of overall revenue growth slowing to 3.4%, the online marketing services (advertising) business accelerated against the trend with a 9.3% YoY growth rate, reaching RMB 19.643 billion in revenue, with its proportion of total revenue increasing from 55.1% in the same period in 2025 to 58.3%, further consolidating its core pillar status.

The growth in the advertising business stems from three points:

The effectiveness of AI advertising tools is increasingly evident. Kuaishou has upgraded advertising delivery efficiency through AI technology, with the widespread application of AIGC marketing materials significantly improving advertisers' ROI, attracting more budgets to tilt towards the Kuaishou platform. The number of merchants using dynamic sales launch increased by 38.0% YoY, and brand merchant marketing consumption increased by 42.0% YoY, both reflecting the healthy expansion of the advertising ecosystem.

The sustained growth of e-commerce in-platform circulation advertising, with a 47.0% YoY increase in the number of merchant- expert (influencer) matches in the distribution library, and a 23.5% YoY increase in the number of active influencers participating in distribution, directly driving the increase in in-platform circulation advertising consumption.

Technological breakthroughs in search advertising, with the new-generation generative search framework OneSearch V2 fully launched in e-commerce search scenarios, bringing about a approximately 3.0% incremental improvement in e-commerce search business GMV, and continuous improvement in search advertising monetization efficiency.

The average online marketing revenue per DAU reached RMB 47.6, up 7.9% from RMB 44.1 in the same period in 2025, showing continuous improvement in advertising monetization efficiency.

User Base Reaches New High, MAU Surpasses 770 Million

The continuous expansion of the user base is the foundation of all of Kuaishou's commercialization efforts.

In Q1 2026, the average DAU of the Kuaishou app reached 412.7 million, a steady increase from 408 million in the same period in 2025; the average MAU reached 771.7 million, an 8.4% increase from 711.7 million in the same period in 2025, both reaching new all-time highs. The MAU growth rate (8.4%) was significantly higher than the DAU growth rate, showing the platform's continuous efforts in acquiring new users.

The average daily usage time per DAU remained relatively stable, and maintaining user stickiness amidst significant MAU expansion was no easy feat.

During the Spring Festival period, the platform's content consumption data was impressive: live streaming views exceeded 15 billion, short video views exceeded 250 billion, cumulative likes exceeded 6.5 billion, the number of interacting user pairs for 'Huozaizai' increased by 25%, and the number of users sending private messages increased by 15%, fully demonstrating Kuaishou's content operation capabilities during important events.

Live Streaming Business Revenue Declines, Ecosystem Optimization is a Proactive Choice

The live streaming business is the segment in this quarter's financial report that requires the most objective interpretation.

In Q1 2026, live streaming business revenue declined by 13.5% YoY to RMB 8.492 billion, being the only segment among the three major businesses to experience negative growth and the main factor dragging down overall revenue growth.

However, management attributed this decline to the result of 'continuous efforts to establish a rich and healthy live streaming ecosystem and diversified high-quality content,' i.e., the phased cost of proactively optimizing the ecosystem and removing low-quality live streams. From operational data, the number of effective daily broadcasters with over 10,000 fans increased by 10.1% YoY, with continuous expansion in high-quality content supply, and the healthiness of the platform's live streaming ecosystem improving.

The assistance of AI to the live streaming business is also accelerating: AI-empowered live streaming incremental GMV exceeds RMB 10 million daily, with 1.1 million AI Vientiane series customizable exclusive special effect gifts sent out in a single quarter, and new forms such as digital human live streaming are expanding the boundaries of live streaming.

Overseas Business Shifts from Profit to Loss, but Losses Continue to Narrow

In terms of overseas business, it is necessary to correct an important perception. In Q1 2026, Kuaishou's overseas business recorded an operating loss of RMB 31 million, compared to an operating profit of RMB 28 million in the same period in 2025, i.e., shifting from profit to loss. However, the loss amount has significantly narrowed from RMB 59 million in Q4 2025, with continuous improvement in operational efficiency.

Overseas revenue was RMB 1.162 billion, down 11.6% YoY from RMB 1.315 billion in the same period in 2025, mainly affected by exchange rate fluctuations and market strategy adjustments.

In the core market of Brazil, DAU and average daily usage time remained stable MoM, with robust YoY growth in e-commerce business GMV and order volume, maintaining a healthy foundation. Kling AI's strong performance in overseas markets such as Brazil (topping the App Store in 42 countries) also provides new assistance in enhancing Kuaishou's overseas brand influence.

Conclusion

Overall, Kuaishou's Q1 2026 financial report exhibits clear characteristics of a 'strategic investment phase':

Revenue growth slows to 3.4%, profits decline by 26.3% YoY, with both live streaming and overseas businesses under pressure. The financial data overall falls short of market expectations, with short-term sentiment leaning negative.

The Exceed expectations (better-than-expected) performance of Kling AI revenue exceeding RMB 650 million and ARR nearing $500 million is the most important positive signal this quarter. The 9.3% growth rate in the advertising business and the user base surpassing 770 million in MAU provide support for the mid-term fundamentals.

The global expansion of Kling AI (topping the App Store in 42 countries) and the rapid growth in ARR are opening up Kuaishou's second growth curve. The continuous deepening of AI's empowerment effect on the three core businesses of advertising, live streaming, and e-commerce is expected to gradually reflect on the profit side in future quarters.

Risk Warning and Disclaimer: Data is sourced from the original Q1 2026 financial results announcement of Kuaishou. This article does not constitute investment advice.

THE END

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle