12.25 Billion Yuan! Seven State-Owned Giants, Including Baotou Steel, Communications, and Transportation Investment, Unite to Launch Inner Mongolia’s New Energy Powerhouse: ‘Guojin New Energy’

06/02 2026

06/02 2026

349

349

Inner Mongolia’s State-Owned Enterprises Forge a New Path: Innovative Resource Integration for Next-Gen Energy Investment

Foresee Energy reports that seven state-owned enterprises under Inner Mongolia’s administration have pooled 1.225 billion yuan to establish a pioneering investment platform, ‘Guojin New Energy.’ Spearheaded by the Inner Mongolia SASAC, Mengyi Asset—a subsidiary asset management firm—serves as the executing partner. Other key backers include Baotou Steel Group, Communications Group, Transportation Investment Group, and Xinhua Distribution Group.

This marks Inner Mongolia’s latest foray into state-led new energy investment, but with a twist. Historically, state firms either directly funded projects or formed joint ventures for independent operations. This time, a limited partnership model separates capital provision from operational control: professional entities handle project sourcing and fund management, while state-owned backers contribute capital without micromanaging daily activities. Foresee Energy interprets this shift as a strategic move to optimize local state assets’ participation in new energy, moving beyond reliance on internal capabilities.

Single Operator, Seven Backers: A Streamlined Approach

Guojin New Energy’s operational framework is straightforward. Mengyi Asset, the executing partner, oversees daily operations and investment choices, while other state-owned enterprises, acting as limited partners, fulfill their capital commitments. This setup ensures investment experts drive decisions, while capital providers shoulder financial risks without needing specialized knowledge.

Foresee Energy highlights how this addresses traditional state-owned enterprises’ pitfalls: sluggish decision-making, risk aversion, and lack of expertise. Many local state firms, mandated to invest in new energy in recent years, either delayed action or saw subpar returns. The new structure empowers professionals to act swiftly, with state backers focusing solely on risk assessment for their capital stakes.

This model mirrors nationwide trends. In 2025, Qingdao’s state asset platforms launched the 1 billion yuan Zhilian Green Energy Fund, managed by a pro team. Similarly, Ningbo’s Yongtou Energy Partnership, with 1.5 billion yuan, combines sub-fund participation and direct project investments. These cases signal a broader retreat from direct operations, with state assets evolving into strategic investors.

Baotou Steel’s Land and Transportation Investment’s Roads: A Synergistic Value Creation

The investors span diverse sectors. Baotou Steel Group boasts vast idle factory roofs and industrial land ideal for solar panels or wind turbines. Communications and Transportation Investment Groups control Inner Mongolia’s road networks, crucial for desert and Gobi energy bases requiring logistical support. Xinhua Distribution Group offers stable cash flow but lacks industrial investment experience.

Previously, these assets operated in silos: Baotou Steel managed its land, Communications Group its roads, with no cross-sector collaboration. Guojin New Energy now bridges these gaps. For instance, the platform could deploy solar projects on Baotou Steel’s land, coordinate road access with Communications Group, and secure financing via other investors.

A similar model emerged in Dalian, Liaoning, in 2025. Liaoning Province, Dalian City, and China Merchants Group jointly invested 1 billion yuan in a Taiping Bay energy fund, merging land, port, and policy resources under professional oversight. This ‘resource-for-capital’ swap proves more sustainable than fiscal dependence, boosting stakeholder engagement.

Investment Allocation: Tougher Than Fundraising

With 1.225 billion yuan secured, Guojin New Energy’s next hurdle is identifying viable projects.

Inner Mongolia aims to add 30 million kilowatts of new energy capacity this year, launch six desert/Gobi bases, and advance three green hydrogen pipelines. These ventures demand massive funding, with individual bases costing billions. The 1.225 billion yuan, while modest in scale, aims to catalyze—not replace—private investment.

The real challenge lies in utilizing generated electricity. Inner Mongolia’s wind and solar resources are abundant, but local demand is limited, and transmission infrastructure lags. By 2025, some regions saw a resurgence in wind/solar curtailment rates. Investing in traditional plants would oversaturate the market. Instead, capital should target high-risk, high-reward areas: off-grid hydrogen production, grid-load-storage integration, and long-distance hydrogen transport.

Hunan’s Xiangtou Puxin Fund offers a blueprint. Despite its 500 million yuan scale, it focuses on industrial chain bottlenecks and key technologies, avoiding mature projects. Ningbo’s Yongtou Energy Fund similarly prioritizes hydrogen energy and new materials. These cases underscore that industrial platforms’ value hinges on backing long-term breakthroughs, not short-term gains.

Guojin New Energy’s success by late 2026—and its project choices—will determine if this model is replicable. Financial stakes in mature solar/wind projects would reduce it to mere asset allocation. However, if it mobilizes private capital for one or two groundbreaking demos, it could inspire resource-rich provinces nationwide.

-

![]()

A Staggering 2.3 Billion Yuan Loss: What's Ailing Li Auto?

-

![]()

May’s Emerging Auto Sales Rankings: Leapmotor Tops 80,000 Units! Hongmeng Zhixing and Zeekr Surge, Xiaomi Maintains 30,000+ | Mirror Pro

-

![]()

What Signal Does Alibaba's QianWen Embarking on Embodied AI Send?

-

![]()

Chinese Vocabulary Flashcard Market Soars Yearly; Baicizhan, New Oriental, and Science Canister Top Q1 Sales

-

![]()

Kuaishou Considers Spinning Off Kling AI to Forge New Frontiers in the AI Era

-

![]()

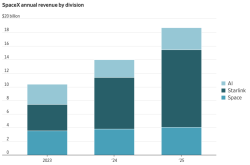

The SpaceX IPO is Here: Why is Global Capital Scrambling for This 'Ticket to the Future World'?

-

MiHoYo Makes a Bold Move in AI Amid Revenue Slowdown and Lack of New Game Releases", "MiHoYo, AI, Gaming, Revenue, New Game Releases", "Facing sluggish revenue growth and diminishing core competitive

-

12.25 Billion Yuan! Seven State-Owned Giants, Including Baotou Steel, Communications, and Transportation Investment, Unite to Launch Inner Mongolia’s New Energy Powerhouse: ‘Guojin New Energy’