A Staggering 2.3 Billion Yuan Loss: What's Ailing Li Auto?

06/02 2026

06/02 2026

327

327

"However lofty one's aspirations may be, it is essential to confront reality."

How dire is Li Auto's financial situation?

To put it simply, Li Auto, once a dominant force in the extended-range vehicle market with a 'blockbuster product' and consistent monthly profits, now appears to have 'lost its knack for making money.'

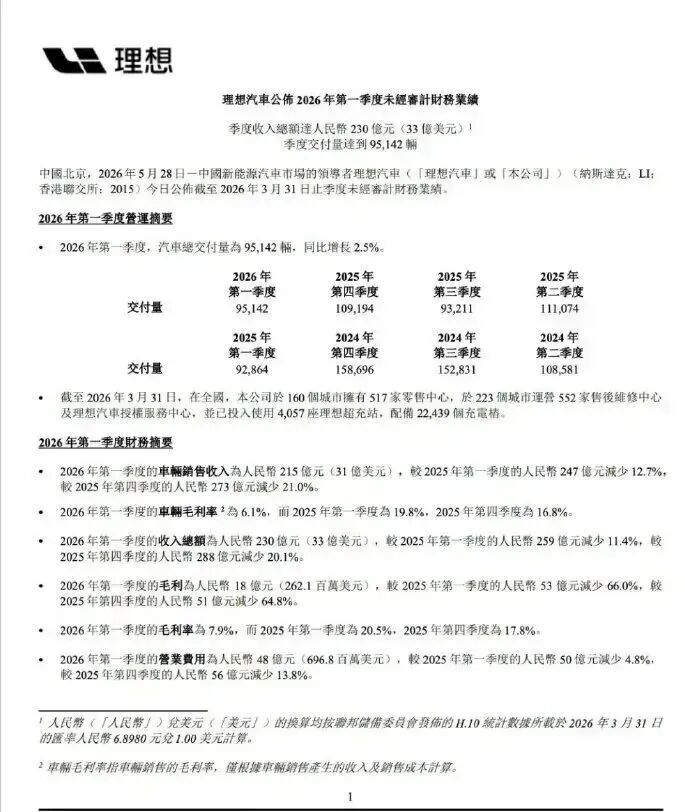

In the first quarter of 2026, revenue stood at 23 billion yuan, marking an 11.4% year-on-year decline. However, this is merely the tip of the iceberg. What truly alarmed investors was the collapse in profits: a net loss of 2.276 billion yuan, compared to a net profit of 647 million yuan in the same period last year—a true 'free fall.'

Even more concerning is the gross profit margin, once Li Auto's strong suit. In the first quarter, the vehicle gross profit margin plummeted to just 6.1%, down from 19.8% in the same period last year and 16.8% in the fourth quarter of the previous year.

Now, only a fraction remains. The reason is straightforward: the best-selling models are no longer the high-priced extended-range L-series but the lower-priced, lower-margin pure electric i6 and the low-spec L6.

Additionally, to prepare for the L-series facelift, Li Auto opted not to clear inventory by selling old and new models concurrently but voluntarily discontinued the older models, naturally putting pressure on sales during this period.

What about sales? In fact, Li Auto delivered 95,142 vehicles in the first quarter, a 2.5% year-on-year increase—far from a collapse. So why did profits plummet? Because previous 'prosperity' was buoyed by high prices; now that prices have dropped, profits have vanished.

In essence, sales haven't plummeted, but individual vehicles can no longer command a premium.

Just before the financial report's release, Li Xiang himself demonstrated confidence by increasing his stake—he purchased 3.4 million shares of the company's Hong Kong-listed stock over two trading days in late March, totaling nearly 200 million Hong Kong dollars. The message from the executive team is clear: we're looking ahead, and the current pain is intentional.

Of course, capital markets are unforgiving. Upon the report's release, Hong Kong-listed shares tumbled, hitting a low of 55.7 Hong Kong dollars during intraday trading,刷新 (refreshing) the lowest point since the end of 2022.

What's the real story behind the losses?

Since we've mentioned the collapse in gross profit margin, let's delve deeper. Is Li Auto failing, or is it undergoing 'short-term pain for long-term gain'?

Let's examine the three main culprits behind the losses.

The first, and most damaging, is the complete shift in product mix. Vehicle sales revenue fell 12.7% year-on-year in the first quarter, to just 21.5 billion yuan. However, note that sales volume slightly increased, meaning 'what's being sold isn't as expensive.'

Previously, Li Auto relied on high-end extended-range models like the L9 and L8, priced starting at 400,000 yuan, with naturally high margins.

But now, to compete in the fiercely contested 200,000–300,000 yuan market, the pure electric i6's share has surged. The i6 has consistently sold over 20,000 units monthly in the past two months—a hit, to be sure—but this 'high volume, low margin' strategy has financially dragged down the overall gross profit margin floor. This is a classic phase of 'trading scale for price.'

The second factor is significant spending to maintain user reputation. In 2026, the new energy vehicle purchase tax shifted from 'fully exempt' to 'half exempt,' meaning customers taking delivery across years would face higher taxes.

But Li Auto made a decision that peers might deem 'unnecessary': it covered this difference out of pocket, spending over 500 million yuan in total. Why would an automaker do this? Because those who haven't experienced owners protesting with banners might not understand. Li Xiang clearly wants to avoid that, so he's spending money to prevent disasters.

The third, and most intriguing, point is that R&D spending didn't decrease—it increased by 8.3%, reaching 2.7 billion yuan. This stands out in an industry where cost-cutting to beautify financial statements is common.

Today, when slashing R&D to polish reports is an industry norm, Li Auto is 'sharpening its blade faster.' Their investments in AI and next-generation pure electric platforms are accelerating, with a 2026 R&D budget of roughly 12 billion yuan, half of which will go to AI-related fields.

So you'll notice that Li Auto's losses aren't the 'death knell' type, where 'no one's buying cars'—but rather 'growth pains' from structural transition.

One issue is selling products at lower prices, another is voluntarily covering user costs, and the third is investing heavily in technological moats. None of these stem from mistakes.

Can Li Auto withstand peer pressure?

When discussing automotive companies, we must examine the current state of its 'NIO, XPeng, Li Auto' peers to gauge Li Auto's standing.

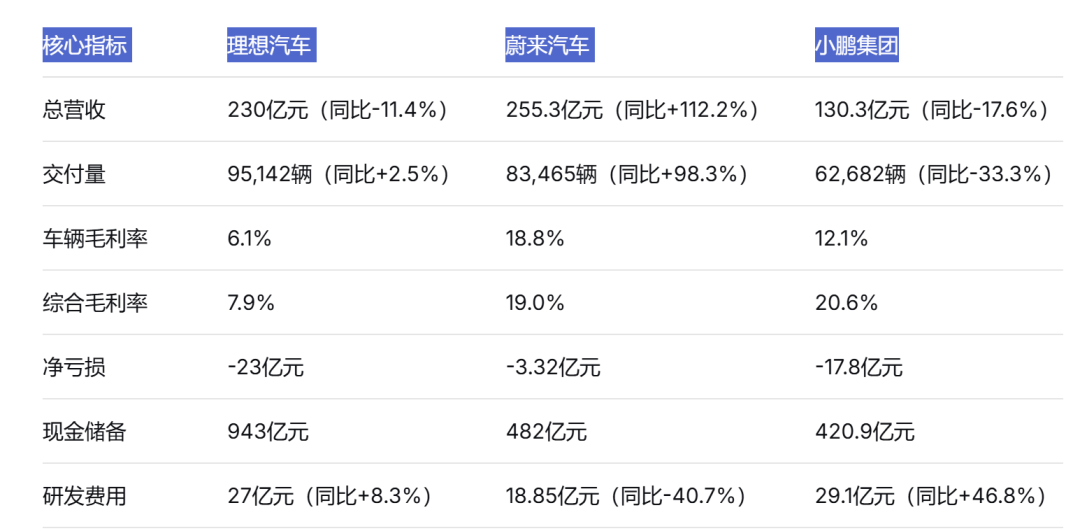

In the first quarter, NIO's total revenue reached 25.53 billion yuan, up 112.2% year-on-year, with a comprehensive gross profit margin of 19.0% and a vehicle gross profit margin of 18.8%, achieving profitability for two consecutive quarters.

NIO's performance surge owes much to strong sales of high-margin models like the ES8 and LeDao L90, along with full-matrix efforts across its three brands. NIO's current strategy is clever—while the Li Auto L9 sells well in the premium market, NIO counters with even pricier models like the ES8 and LeDao across multiple lines, covering a broader market. From a profitability standpoint, NIO has once again left Li Auto behind.

Now, let's look at XPeng. In the first quarter, XPeng Group's total revenue was 13.03 billion yuan, down 17.6% year-on-year, with a net loss of 1.78 billion yuan and deliveries of 63,000 vehicles, a 33.3% decline. While the numbers don't look great, there are some unexpected bright spots: the overall gross profit margin held strong at 20.6%, notably higher than Li Auto's 7.9%.

So upon closer inspection, in this quarter's 'NIO, XPeng, Li Auto' lineup, Li Auto neither sold the most (NIO grew faster) nor had the healthiest margins (XPeng stabilized margins through technology exports)—but it did suffer the worst losses, with a net loss of 2.3 billion yuan, far exceeding XPeng's 1.78 billion and NIO's 332 million.

Li Auto's 'profit benchmark' reputation has now completely shattered.

But remember, 'NIO, XPeng, Li Auto' are now on different trajectories: NIO sticks to the premium segment, XPeng pursues cross-border diversification, and Li Auto firmly adopts an extended-range + pure electric dual-drive strategy, heavily investing in AI and self-developed chips. This battle isn't over—Li Auto has simply been forced into 'tough times' earlier than expected.

From this table, you can see that Li Auto still holds the thickest cash reserves at 42.8 billion yuan, meaning it can afford to lose money and wait. While NIO surpasses Li Auto in revenue and margins, its cash volume is only half of Li Auto's. XPeng, despite having the highest comprehensive gross profit margin, is burning through cash the fastest.

Not profitable, but accomplishing the most crucial thing

Many financial media outlets interpret Li Auto's 'shift from profit to loss' as a risk signal, with some even joking that 'Li Auto is burning money to death.' I disagree. If you focus solely on reported profits, you might miss its true strategic intent.

This requires examining a strange phenomenon: many traditional automakers, before model transitions, often heavily discount older models to clear inventory, even offering 'deep discounts' to attract attention. This might look good on financial statements (since inventory is cleared and cash flows in).

But what does this mean for existing owners? It means their newly purchased vehicle might depreciate by 100,000 yuan within six months, with used car residual value plummeting.

What choice did Li Auto make during the L-series transition? It chose 'not to profit at the expense of old users.' Before the L-series facelift, the company voluntarily discontinued older models, avoiding price wars to clear inventory or blurring lines between old and new models to compete in the same market.

This strategy benefits users: vehicle residual values remain stable, and owners aren't 'scammed' by the manufacturer. But for Li Auto, this means willingly accepting delivery downtime and sales declines.

Today, when most automakers prioritize short-term gains, Li Auto's willingness to make this trade-off shows it has moved beyond 'survival anxiety' and is considering long-term brand value and user trust. This is what sets Li Auto apart from 'NIO, XPeng, Li Auto.'

NIO uses battery swapping services to retain users, XPeng earns from intelligent technology exports, while Li Auto's core moat isn't just its 'dad car SUV' positioning but the 'considerable conscience' it shows during product iterations. This restraint may seem foolish now, sacrificing profits, but it will yield increasingly valuable user reputation over time.

Looking back at the reasons for these losses, which weren't passively accepted but actively chosen:

Voluntarily discontinuing older L-series models was for the facelift; covering purchase taxes for i6 users was for reputation; and investing 2.7 billion yuan in R&D against the trend was to secure full-stack self-developed core competitiveness in the next three years.

Together, these three reasons explain a core logic: Li Auto isn't incompetent—it's daring to abandon short-term pretty numbers on profit statements at this juncture to secure long-term confidence in leading both AI and pure electric tracks.

This is the most valuable interpretation of this financial report. Money has been lost, but brand value and technological barriers remain.

The baton of product strength is already being passed. In mid-May, the all-new Li Auto L9, equipped with the self-developed 'Mach M100' chip and Mach VLA large model, began deliveries, priced between 459,800 and 509,800 yuan.

By late June, the new Li Auto L8 will launch, followed by the pure electric flagship SUV i9 in the second half, forming a complete high-end product matrix from extended-range to pure electric. Whether these new models can push gross profit margins back above 10% will be the critical focus in the second half.

Consider a simple question: how could a company with 94.3 billion yuan in cash reserves and a debt-to-asset ratio of just 51.2% be dragged down by a first-quarter loss? The truth is that Li Auto is undergoing a systemic transition from 'selling hardware' to 'competing on AI ecosystem.' Such transitions inevitably involve pain.

And frankly, the years when Li Auto was hailed as the 'profit king' also had an element of luck—no strong competitors existed in the extended-range track, and Li Auto profited handsomely from its first-mover advantage. Now that rivals have arrived and policies have changed, those easy profit-making days are over.

But this doesn't mean Li Auto will collapse. On the contrary, its willingness to endure these hardships now shows it's more sober-minded than the market assumes.

This bitter pill is worth swallowing bravely

Facing such a 'profit collapse' financial report, investors voting with their feet is normal. In capital markets, when profitability fades, valuations should fall.

But my view on Li Auto's future hasn't turned negative for three reasons.

First, its foundation remains solid. First-quarter sales outperformed the overall new energy vehicle market, which saw a 21.1% year-on-year decline in retail volume, while Li Auto managed a 2.5% increase—a sign of a robust foundation.

Second, its transition path is clear. The roadmap from 'selling extended-range vehicles' to 'AI large models + self-developed chips + pure electric SUVs' is already drawn. With the i9 launching in the second half, brand momentum can rise again.

Third, its ammunition is relatively abundant. With 94.3 billion yuan in cash, some might see this as 'losing money with no one to blame.' But conversely, cash reserves mean 'margin for error.' Many automakers fail without making mistakes; Li Auto can make several mistakes and keep fighting. This confidence is rare in the new energy industry.

Of course, stock price movements are another matter. Bank of America lowered its U.S. stock target from $22 to $18, while CL

The first-quarter loss of 2.3 billion yuan may actually pave the way for Li Auto to gain a dominant position in the realms of AI and intelligent driving in the latter half of the year. Such a strategic move is far more advantageous than simply maintaining profitability throughout the year without amassing any core technological capabilities.

Disclaimer: This article is intended solely for financial hotspot analysis. All data and references have been sourced from public inquiries, company announcements, and Tonghuashun IFinD. The viewpoints presented are for reference purposes only and do not constitute any form of investment or consumption advice.

#InvestmentBankHotspots #DeepThinking #BusinessFinance #CaseStudy #InvestmentBankCircle #FinancialTrends #ListedCompanies #AI #FinancialBuzz #IPO #PrimaryMarket #GoingPublic #AutomotiveListedCompanies #LiAuto #LiAutoFinancialPerformance

What are your thoughts on this matter?

We eagerly await your civil and rational insights in the comments section. The comment that garners the most likes...

Thank you for your patience in reading this article. If you found it enjoyable, please feel free to give us a 'Like'.

Statement: This platform has been deeply engaged in the financial self-media sector for 12 years, with a focus on providing in-depth interpretations of the capital market, listed companies, and the latest trends in business and technology. Boasting a network of over 3 million fans, we welcome contributions from writers. If your submission is accepted, we will compensate you accordingly. For any copyright issues related to quoted articles or images, please contact the administrator, who will promptly correct the source, acknowledge the author, pay a certain fee, or remove the content upon verification.

-

![]()

A Staggering 2.3 Billion Yuan Loss: What's Ailing Li Auto?

-

![]()

May’s Emerging Auto Sales Rankings: Leapmotor Tops 80,000 Units! Hongmeng Zhixing and Zeekr Surge, Xiaomi Maintains 30,000+ | Mirror Pro

-

![]()

What Signal Does Alibaba's QianWen Embarking on Embodied AI Send?

-

![]()

Chinese Vocabulary Flashcard Market Soars Yearly; Baicizhan, New Oriental, and Science Canister Top Q1 Sales

-

![]()

Kuaishou Considers Spinning Off Kling AI to Forge New Frontiers in the AI Era

-

![]()

The SpaceX IPO is Here: Why is Global Capital Scrambling for This 'Ticket to the Future World'?

-

MiHoYo Makes a Bold Move in AI Amid Revenue Slowdown and Lack of New Game Releases", "MiHoYo, AI, Gaming, Revenue, New Game Releases", "Facing sluggish revenue growth and diminishing core competitive

-

12.25 Billion Yuan! Seven State-Owned Giants, Including Baotou Steel, Communications, and Transportation Investment, Unite to Launch Inner Mongolia’s New Energy Powerhouse: ‘Guojin New Energy’