Surprisingly, Cheap Electric Cars Are Facing Sluggish Sales

06/16 2026

06/16 2026

331

331

Introduction

The fact that cheap electric cars are not selling as well as they once did signifies the end of an era dominated by a low-cost dividend model.

For quite some time, there has been a widespread 'misconception' regarding the Chinese auto market—many believe that in China, affordability alone guarantees sales success.

This mindset is quite understandable. Previously, the Chinese auto market witnessed a boom in low-end SUVs, with many automakers reaping substantial profits by simply producing these vehicles. However, times have changed, and the sales logic of that era is now obsolete.

Today, in the new energy era, especially as we approach 2026 and the auto market enters its final competitive phase, a counterintuitive trend has emerged: cheap electric cars are struggling to sell.

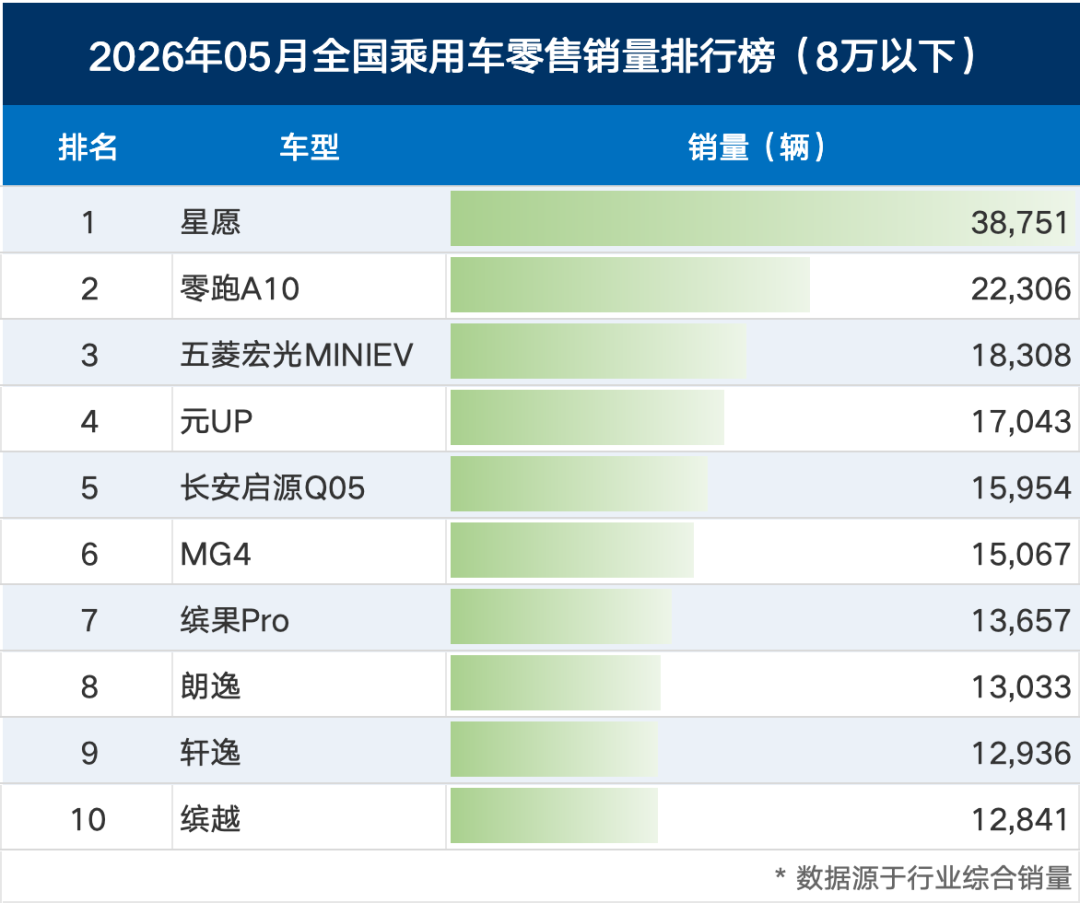

The data speaks volumes. From January to April 2026, domestic sales of new energy vehicles priced below RMB 80,000 plummeted by nearly 50%, with retail sales of pure electric microcars experiencing a staggering year-on-year decline of nearly 70%. Even the once-dominant Hongguang MINIEV in the micro electric car segment is now facing difficulties. Models like the Chery QQ Ice Cream have seen their monthly sales dwindle to the 500-unit range, a sharp contrast to their previous monthly sales in the tens of thousands.

As these low-priced electric cars, which once accounted for a significant portion of sales, lose their appeal, the domestic auto market has entered a downturn. From January to April 2026, cumulative retail sales of new energy passenger vehicles in China reached 2.758 million units, marking a double-digit year-on-year decline.

While the industry often discusses a cooling auto market, my visits to frontline dealerships reveal a different story. It's not that people have stopped buying new energy vehicles; rather, it's the low-priced electric commuter cars, which previously relied on policy dividends and lacked core product competitiveness, that are now failing in the market.

01 The Changing Cost Landscape for Low-Priced Electric Cars

From a macro perspective, the decline in low-priced electric cars can be attributed to the implementation of the new purchase tax policy on January 1, 2026.

Previously, new energy vehicles enjoyed full exemption from purchase tax. However, the new policy adjusted this exemption to a 50% reduction, with the purchase tax relief cap lowered from RMB 30,000 to RMB 15,000. Coupled with the restructuring of annual national subsidy rules, vehicle scrapping subsidies and trade-in subsidies were significantly reduced. For new energy vehicles priced below RMB 166,700, subsidy amounts decreased by RMB 3,000 to RMB 10,000 compared to 2025, directly increasing user costs.

After these adjustments, terminal users purchasing a RMB 50,000-class micro electric car faced an additional tax cost of over RMB 2,000. For a RMB 100,000-class family new energy vehicle, the additional tax exceeded RMB 4,000. For a RMB 200,000 mainstream family new energy vehicle, taxes increased by nearly RMB 10,000.

Of course, for mid- to high-end car buyers, a few thousand yuan in tax fluctuations would hardly sway their purchasing decisions. However, for users in the RMB 80,000 and below price range who need a commuter car, sensitivity to purchasing costs is extremely high. These users are primarily from lower-tier markets and have strict budget constraints for car purchases, as the funds are mainly allocated from fixed household expenses with little room for flexibility.

As the cost burden increases, it undoubtedly influences their final decision on whether to buy a car. After visiting car dealerships in some third- and fourth-tier cities in Shandong and Henan, I learned that many potential buyers abandoned their purchase plans due to the additional RMB 2,000 in taxes.

In other words, the past sales success of low-priced electric cars was not driven by product competitiveness but rather by the dual dividends of purchase tax exemptions and national subsidies, which lowered the final price and drove passive sales volume. Once these policy dividends were withdrawn, the price advantage vanished instantly, and a sales decline became inevitable.

Of course, a single policy rollback is not sufficient to trigger a halving of sales. Year-end demand overdrafts and price wars emerged as another major factor contributing to the collapse of low-priced new energy vehicles.

At the end of 2025, the auto industry hyped up the end of subsidy rollbacks, prompting county and township users with rigid demand to purchase cars in advance, overdrafting the demand for commuter cars in the first quarter of 2026. Multiple auto salespeople informed me that at the end of last year, stores were inundated with customers interested in micro electric cars, with order backlogs exceeding two weeks. This year, however, store foot traffic has plummeted, and the market has directly fallen into a demand gap.

At the same time, fuel vehicle companies cleared their inventories, indirectly attacking the low-cost stronghold of new energy vehicles. Media reports indicate that the transaction price of a certain Japanese A-class sedan even fell below RMB 52,000, while mainstream B-class fuel vehicles like the Magotan and Accord offered comprehensive discounts of RMB 30,000 to RMB 50,000, significantly lowering the entry barrier for traditional family fuel vehicles.

At the same budget level, users could now opt for an entry-level fuel sedan, avoiding the shortcomings of charging and range limitations, while also enjoying more mature vehicle quality control and a longer vehicle lifecycle. Many consumers quickly shifted their purchasing preferences toward fuel vehicles.

02 Price Disparities Split the Auto Market

As mentioned earlier, users of micro electric cars priced below RMB 80,000 are highly price-sensitive. Their final purchasing decisions are based solely on indicators like the final price and purchase subsidies, rather than factors such as body structure, battery stability, chassis tuning, or intelligent configurations.

In the past, automakers relied on low-cost lithium iron phosphate batteries with small capacities, simplified body construction processes, and reduced after-sales support to cut manufacturing costs. Combined with policy subsidies, they created price advantages and achieved mass-market sales volume.

However, with the increase in policy-related costs, automakers found themselves in a dilemma. Raising prices to cover taxes would result in direct customer loss. Maintaining original prices would lead to selling cars at a loss. Given that the net profit per unit for micro electric cars is less than RMB 1,000, there is little room for concessions. Under this vicious cycle, model discontinuations, store closures, and channel contractions occurred one after another.

In contrast, the consumption logic for mid- to high-end new energy vehicle buyers priced at RMB 150,000 and above is entirely different. They prioritize core product competitiveness such as vehicle range, intelligent driving experience, overall vehicle quality, brand services, and used car resale value. Compared to these factors, fluctuations in taxes of a few thousand yuan are secondary or even irrelevant to their decision-making.

Let's crunch the numbers. After the new energy vehicle purchase tax shifted from 'full exemption' to '50% reduction' in 2026, the maximum tax relief is capped at RMB 15,000. For a RMB 300,000 model, the original tax exemption saved about RMB 26,500, but now it only saves RMB 15,000, a difference of about RMB 11,500. Even when compared to fuel vehicles (which also have a maximum tax relief of RMB 15,000), the advantage is not significant.

For buyers with such high purchasing power, for models priced above RMB 250,000, tax subsidies represent a smaller proportion of the vehicle price and are unlikely to become a core decision-making factor. Survey data shows that only 10% of new energy vehicle buyers in the RMB 250,000 and above price range pay attention to purchase tax subsidies.

This explains the current market pattern of 'cooling at the low end and heating up at the high end': sales in the low-price market below RMB 80,000 have nearly halved; mid-range models priced between RMB 150,000 and RMB 200,000 have seen a slight decline; while high-end models priced above RMB 250,000 have grown against the trend, breaking free from price competition and relying on technology and branding to establish a competitive edge.

Behind this phenomenon lies the fact that, with the industry's knockout phase underway, the low-cost dividend business model is quickly becoming unsustainable.

For a long time, the industry has viewed micro electric cars like the Hongguang MINIEV as essential vehicles for lower-tier markets, overlooking the fact that these models are, to some extent, phase-specific products driven by policies.

Automakers relied on subsidy dividends to scale up, boost sales, and earn new energy credits, neglecting core product development such as chassis R&D, intelligent cockpit upgrades, and battery safety optimizations. Instead, they used low prices to capture the market. This volume-driven business model failed in 2026. Going forward, the new energy sector will witness the end of the low-cost competition era, and a competition era based on strength will officially commence.

Editor: Shi Jie Editor: He Zengrong

THE END

-

![]()

The Hidden Update of visionOS 27 is Incredible: Uncovering the Major Upgrades Apple Didn't Mention

-

![]()

Volunteer Application Agent: Tencent is Restrained, Alibaba is Aggressive

-

![]()

A Glimmer of Innovation Dances on the Tightrope

-

![]()

The AI Glasses Track is Fully Taking Off: How Far Are We from Them Being 'Must-Haves'?

-

![]()

US Media Criticizes China’s Auto Exports: ‘No Domestic Buyers, High Oil Prices Force Consumers into Chinese EVs’

-

![]()

In May, Battery Installations Soar to 71.9 GWh, with CATL and BYD Dominating Over 60% of the Market

-

![]()

Three Times a Week, Avatr Passionately Advocates Originality: A World-Class Brand Cannot Exist Without Innovation

-

Best-Selling Car Model to Be Phased Out: Is Porsche Heading Toward a Tough Patch?