In May, Battery Installations Soar to 71.9 GWh, with CATL and BYD Dominating Over 60% of the Market

06/16 2026

06/16 2026

470

470

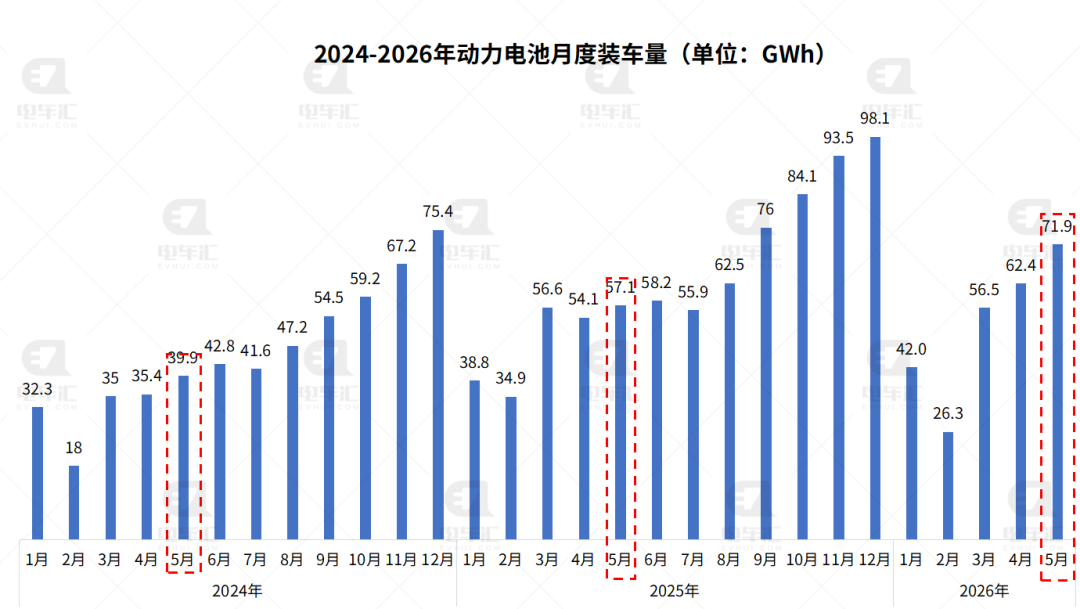

The palpable heat of the new energy vehicle market is strongly reflected in the power battery sector. According to the latest data from the China Automotive Power Battery Industry Innovation Alliance, in May 2026, the domestic power battery installation volume surged to 71.9 GWh, marking a 25.9% year-on-year increase and a 15.2% month-on-month rise. This indicates a robust recovery momentum across the industry.

Analyzing the monthly power battery installation volumes from 2024 to 2026, the cumulative installation for the first five months of this year has reached 259.1 GWh. Notably, the installation volume in May set a new annual high, with the month-on-month growth rate continuing to expand. This trend underscores that downstream automakers are indeed ramping up production, and terminal demand is on the rise. If this momentum persists, the full-year data promises to be highly encouraging.

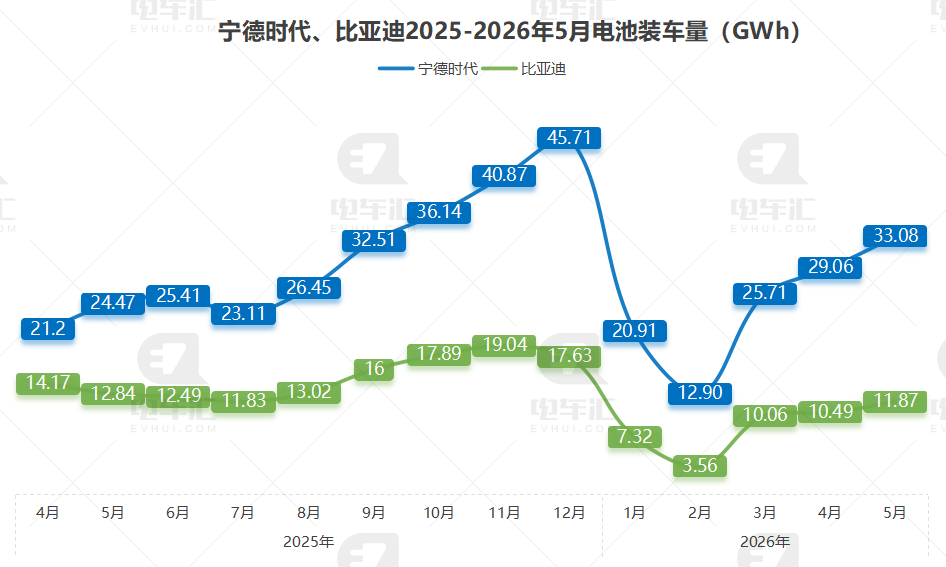

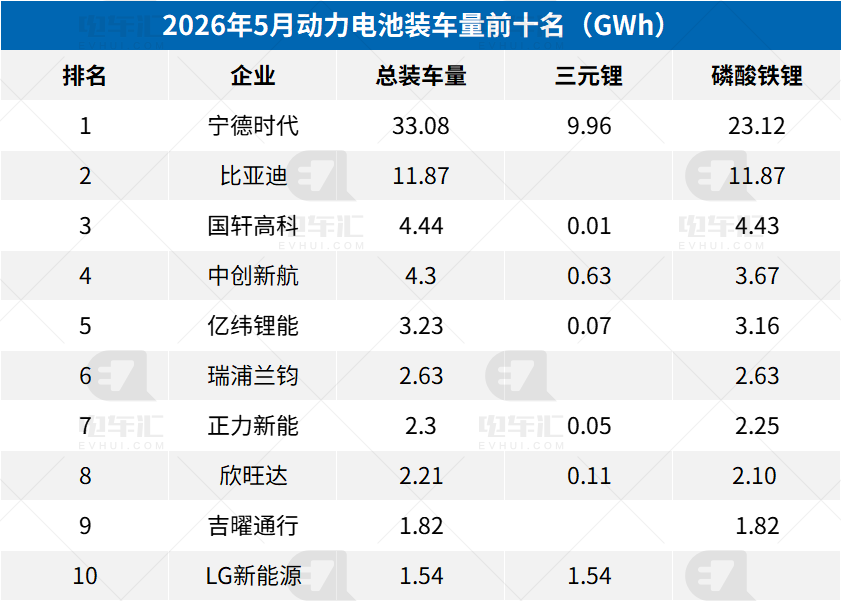

In May 2026, the competitive landscape among the top 15 power battery companies, in terms of installation volume, remained largely stable, with the top two maintaining their strong positions. CATL installed 33.08 GWh in May, capturing 46.14% of the market. This represents a slight decrease of 0.51 percentage points from the previous month, but its leading position remains unchallenged. BYD installed 11.87 GWh, accounting for 16.56% of the market, also experiencing a slight decrease of 0.27 percentage points. However, its self-supply system advantage ensures it remains firmly in second place. Together, CATL and BYD captured 62.7% of the market share. The subsequent positions were largely occupied by familiar names: Guoxuan High-Tech with 4.44 GWh, CALB with 4.3 GWh, and EVE Energy with 3.23 GWh, collectively accounting for approximately 16.7% of the market, with minimal changes in their rankings. However, several second-tier manufacturers made significant strides this month. LG Energy Solution saw a 1.58 percentage point increase to 2.14%, breaking into the top 10, while Sunwoda rose by 0.68 percentage points to 3.08%, climbing to eighth place. The competition among second-tier manufacturers is indeed intensifying.

Top 15 Power Battery Companies by Installation Volume from January to May 2026

Battery Installation Volumes of CATL and BYD from May 2025 to May 2026

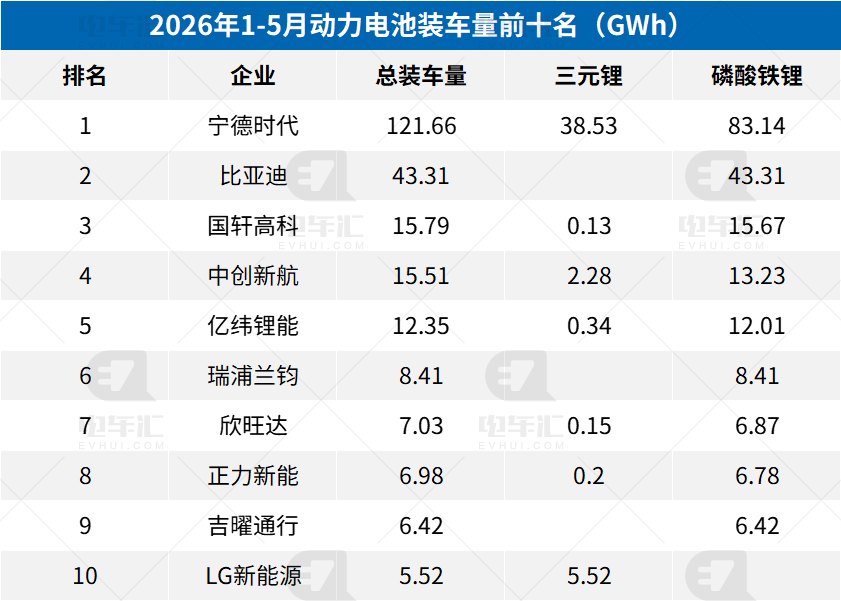

Examining the cumulative data for battery installation volumes from May 2025 to May 2026, the leading effect becomes even more pronounced. From January to May, CATL's cumulative installation volume reached 121.66 GWh, accounting for a staggering 47.02% of the market. This represents a significant increase of 4.12 percentage points from the beginning of the year, indicating an expanding lead. BYD's cumulative installation volume was 43.31 GWh, accounting for 16.74%. Although its monthly performance in May remained stable, its cumulative market share slipped by 7.32 percentage points from the beginning of the year. Together, CATL and BYD captured over 63% of the market share, further increasing industry concentration.

Top 10 Power Battery Companies by Installation Volume in May 2026

In terms of technology routes, lithium iron phosphate (LFP) continues to expand its advantage. In May, LFP battery installations reached 59.5 GWh, accounting for 82.8%, setting a new record. Ternary batteries, on the other hand, only accounted for 12.4 GWh, or 17.2%. The cumulative trend is similar, with LFP accounting for over 80% from January to May. Companies like BYD, Guoxuan High-Tech, and REEPower are almost entirely focused on LFP. Simply put, LFP, with its high cost-effectiveness and long cycle life, has become the preferred choice for mainstream models and commercial vehicles. In contrast, ternary lithium batteries are primarily demanded by high-end vehicles for their long range and fast-charging capabilities. Overall, the May data is quite impressive, with both monthly and cumulative sales growing, leading companies making steady progress, second-tier manufacturers showcasing their strengths, and the divergence in technology routes becoming increasingly clear. With the penetration rate of new energy vehicles continuing to rise and energy storage presenting a new large market, the Chinese power battery sector is poised for even greater dynamism in the future.

-

![]()

What is the Future for Domestic Large-Scale AI Models?

-

![]()

Insights into China's Gimbal Camera Market Structure, Player Dynamics, and Development Trends in 2026

-

![]()

Massive Capital Influx! NVIDIA's $25 Billion Bond Issuance Secures $85 Billion in Oversubscribed Demand, How Will the AI Chip Giant Secure Long-Term Liquidity?

-

![]()

Has DJI Caught Up with Insta360?

-

![]()

The Hidden Update of visionOS 27 is Incredible: Uncovering the Major Upgrades Apple Didn't Mention

-

![]()

Volunteer Application Agent: Tencent is Restrained, Alibaba is Aggressive

-

![]()

A Glimmer of Innovation Dances on the Tightrope

-

![]()

The AI Glasses Track is Fully Taking Off: How Far Are We from Them Being 'Must-Haves'?