How Luxury Brands Lost the Plug-in Hybrid War

06/16 2026

06/16 2026

372

372

Lead-in

Introduction

Do you think it's just about pure electric range and battery size?

By mid-2026, the structure of China's plug-in hybrid market has become clear enough that it requires little speculation.

In fact, signs emerged last year. China's retail sales of new energy passenger vehicles reached 12.809 million units, up 17.6% year-on-year, with a retail penetration rate as high as 54%. Within the new energy segment, plug-in hybrid vehicles (PHEVs) accounted for 3.697 million units in retail sales, up 8.8% year-on-year.

This represents a blue ocean market of nearly 4 million units.

Who is seizing this opportunity? Data from December 2025 provides the answer: in the wholesale segment of new energy passenger vehicles, pure electric vehicles accounted for 60.2%, narrowly defined plug-in hybrids 30.4%, and extended-range electric vehicles 9.4%. In other words, broadly defined plug-in hybrids (including extended-range models) have captured nearly 40% of the new energy market share.

On the other hand, luxury brands that once thrived in Europe are now losing ground in this promising market.

This is not a simple narrative of winners and losers but a deeper misalignment in technical routes, policy pace, and market understanding.

01 Structural Factors Behind Sales Changes

Let's start with the overall data.

In 2025, China's retail penetration rate for new energy passenger vehicles exceeded 54%, with plug-in hybrids (including extended-range models) contributing nearly 40% of new energy sales.

As we enter 2026, the growth momentum of plug-in hybrids remains steady.

Meanwhile, traditional luxury brands have seen varying degrees of sales decline in the Chinese market.

Mercedes-Benz delivered 551,900 units in 2025, down 19% year-on-year; BMW delivered 625,500 units, down 12.5%; and Audi delivered approximately 617,000 units, down 4.9%.

Combined, the three brands saw a reduction of about 260,000 units in one year.

Notably, Mercedes-Benz's 19% decline in China far exceeded its -1% in Europe and -12% in North America.

BMW grew by 7.3% in Europe and 5.7% in the Americas but was dragged down by its performance in the Chinese market.

The case of Jaguar Land Rover is even more typical. Its annual sales in China were 146,000 units in 2017 but fell to less than 30,000 units by 2025.

In 2025, when China's new energy penetration rate exceeded 50%, Jaguar Land Rover still derived over 95% of its sales from fuel-powered vehicles, with plug-in hybrid models being almost negligible.

So, what role does plug-in hybrid technology play in the changing sales of high-end models?

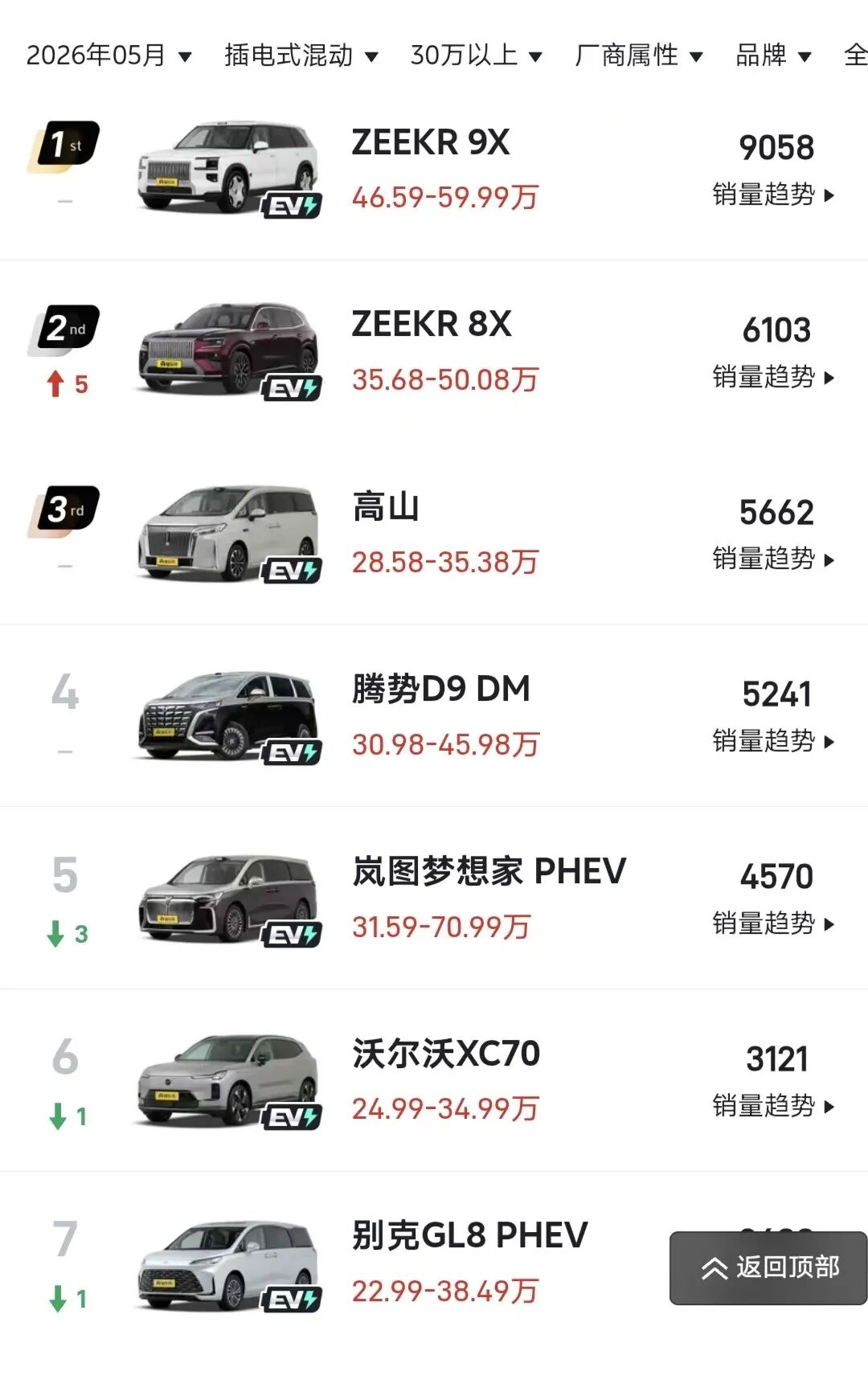

The May sales ranking of plug-in hybrid models priced above 300,000 yuan provides a sobering perspective.

The top ten models for the month were: Zeekr 9X (9,058 units), Zeekr 8X (6,103 units), WEY High Mountain (5,662 units), Tengshi D9 DM (5,241 units), Voyah Dreamer PHEV (4,570 units), Volvo XC70 (3,121 units), Buick GL8 PHEV (2,683 units), Tank 700 Hi4T (2,628 units), Fangchengbao Leopard 5 (2,296 units), and Tengshi N8L DM (2,032 units).

It should be noted that this ranking refers to narrowly defined plug-in hybrids (excluding extended-range models). Brands like Li Auto and Seres, which focus on extended-range technology, are not included. However, if broadly defined plug-in hybrids are considered, Chinese brands' dominance would only strengthen.

In this top-ten list, only one traditional Western luxury brand appears: Volvo.

And Volvo has long been dominated by Chinese capital under Geely's ownership.

Another international presence is the Buick GL8 PHEV, but it is a product of SAIC-GM's deep localization efforts, tightly bound to the Chinese market.

Audi, BMW, and Mercedes-Benz's plug-in hybrid models are nowhere to be found in the top ten or even the top fifteen.

These numbers are not the result of a single factor.

Policy, product offerings, technical routes, and localization levels are all intertwined.

02 It's Not Just About Battery Size or Range

Starting from January 2026, China raised the tax-exempt pure electric range threshold for plug-in hybrid vehicles from 27 miles (43 kilometers) to 62 miles (100 kilometers).

This adjustment was not sudden, but its impact is structural.

Many European luxury brands' plug-in hybrid models were originally designed with a "good enough" logic.

Based on internal combustion engine platforms, the engine was the protagonist, and the electric motor played a supporting role. The batteries were small, offering a pure electric range of 50-60 kilometers.

This was barely sufficient for daily commuting but only if charged every day.

Once the battery was depleted, the vehicle became a fuel-powered car carrying a heavy battery, with no improvement in fuel efficiency.

In contrast, the mainstream approach of Chinese brands is to develop hybrids based on pure electric platforms or dedicated hybrid platforms.

These models feature larger batteries and longer pure electric ranges.

The Lotus Eletre PHEV is equipped with a 70kWh battery, offering a CLTC pure electric range of 420 kilometers and 350 kilometers under WLTP standards.

The Volvo XC70 achieves a WLTP pure electric range of 180 kilometers, following the same logic.

These models do not require daily charging. Once a week is sufficient to cover daily commuting.

For long-distance travel, the engine serves as a supplement rather than the main power source.

The differences between these two technical routes are sharply magnified under the new policy threshold.

Additionally, the new regulations tighten efficiency requirements for plug-in hybrids in fuel-powered mode.

Many luxury brands' plug-in hybrids use large-displacement engines as their "fuel backup." V6 and V8 engines are not uncommon.

In fuel-powered mode, these vehicles struggle to meet the new efficiency standards in terms of fuel consumption and emissions.

With limited pure electric range and uneconomical fuel consumption, their advantages on both ends are weakened.

This is not a deliberate policy move to "target" these brands but a natural progression of industry standards keeping pace with technological development.

Chinese brands' performance in the plug-in hybrid market is not solely driven by "price wars."

In the high-end segment priced between 300,000 and 500,000 yuan, domestic plug-in hybrids have formed a stable product matrix.

Models like the Zeekr 9X, WEY High Mountain, Tengshi D9 DM, and Voyah Dreamer in the May ranking all have relatively high average selling prices.

The Zeekr 9X exceeded 9,000 units in a single month, a figure never reached by any international luxury brand's plug-in hybrid model.

Technologically, Chinese brands widely adopt series-parallel hybrid architectures or multi-speed DHT solutions, achieving a good balance between fuel consumption in low-battery conditions and power smoothness.

From a cost control perspective, the maturity of local supply chains (batteries, electric controls, chips) makes large-battery solutions economically viable.

From a product definition standpoint, these models are more closely aligned with the actual usage scenarios of Chinese consumers—primarily urban commuting with occasional long-distance travel.

The Volvo XC70's presence in the top ten illustrates a key point: adhering to China's market rules and adopting China-led technical routes still offers opportunities.

The Buick GL8 PHEV's inclusion demonstrates another possibility of deep localization.

Brands that cling to internal combustion engine platforms and underestimate China's policy resolve will naturally be marginalized by the market.

03 Can the European Market Still Provide a Buffer?

A common viewpoint is that while European luxury brands may struggle in China, they can still rely on plug-in hybrids in their home European market.

In the short term, this holds true.

Plug-in hybrid models in Europe still enjoy certain tax incentives, and many consumers are willing to pay for the convenience of "using electricity or fuel."

However, long-term trends warrant attention.

In the first four months of 2025, China's plug-in hybrid exports to Europe surged by 421%, capturing an 8.3% market share.

In 2025, China's new energy passenger vehicle exports reached 2.422 million units, up 86.2% year-on-year.

The Lynk & Co 08 PHEV has already been shipped to Europe in bulk. BYD and Great Wall Motor are also making layout (layouts).

When Chinese brands' long-range plug-in hybrids arrive at European ports, can European domestic brands' "short-range plug-in hybrids" maintain their edge?

The iteration of technical routes is global and will not remain fragmented across markets indefinitely.

Large batteries, long ranges, and plug-in hybrids based on pure electric or dedicated hybrid platforms are becoming a global consensus.

Luxury brands that continue to make minor adjustments on internal combustion engine platforms must answer a question: When Chinese brands bring more mature products to your home turf, where is your competitive moat?

The reshaping of the plug-in hybrid market is not about one side "defeating" the other.

It is more about different players moving at different paces based on their technical accumulate (accumulations), policy environments, and market judgments.

China's new regulation raising the pure electric range threshold to 100 kilometers is not targeted at anyone but reflects the industry's phased (phase-based) consensus on what plug-in hybrids should be.

Luxury brands that adjust their technical routes and accelerate localization in their next-generation products can still rejoin the game.

However, if they continue down the path of "converting fuel vehicles to electric," they will lose not just the Chinese market but an entire era.

Editor-in-Charge: Shi Jie Editor: Chen Xinnan

THE END

-

![]()

The Hidden Update of visionOS 27 is Incredible: Uncovering the Major Upgrades Apple Didn't Mention

-

![]()

Volunteer Application Agent: Tencent is Restrained, Alibaba is Aggressive

-

![]()

A Glimmer of Innovation Dances on the Tightrope

-

![]()

The AI Glasses Track is Fully Taking Off: How Far Are We from Them Being 'Must-Haves'?

-

![]()

US Media Criticizes China’s Auto Exports: ‘No Domestic Buyers, High Oil Prices Force Consumers into Chinese EVs’

-

![]()

In May, Battery Installations Soar to 71.9 GWh, with CATL and BYD Dominating Over 60% of the Market

-

![]()

Three Times a Week, Avatr Passionately Advocates Originality: A World-Class Brand Cannot Exist Without Innovation

-

Best-Selling Car Model to Be Phased Out: Is Porsche Heading Toward a Tough Patch?