BYD, FAW, and Chery Act Swiftly: Chinese Automakers Accelerate Acquisition of European Factories

06/17 2026

06/17 2026

535

535

Lead

Introduction

Chinese automakers are racing to acquire local factories in Europe, seizing what may be their 'last window' to enter the market amidst looming new EU regulations.

For veterans of the automotive industry, the acronym 'IAA' likely brings to mind the 'Frankfurt/Munich Auto Show,' known in German as Internationale Automobil-Ausstellung.

Yet, as 2026 approaches, these three letters no longer signify the grandeur and inclusivity of the 'Olympics of the automotive industry.' Instead, they represent the EU's Industrial Accelerator Act (IAA).

This legislation has sparked a remarkable trend across Europe: Chinese automotive companies are aggressively acquiring European factories or establishing local production facilities.

Why the urgency? The IAA proposes stringent reviews for foreign investments exceeding €100 million, with thresholds such as limiting foreign ownership to 49% and mandating that at least 50% of employees be local nationals set to take effect. This mirrors China's earlier era of the '50% equity red line' for joint ventures in its automotive sector.

Consequently, Chinese automakers are rushing to 'board the train' before the window of opportunity closes.

BYD, Chery, FAW, Geely, SAIC, XPeng, and Leapmotor have either made moves or are currently at the negotiating table. The transition from 'exporting complete vehicles' to 'local production' is accelerating.

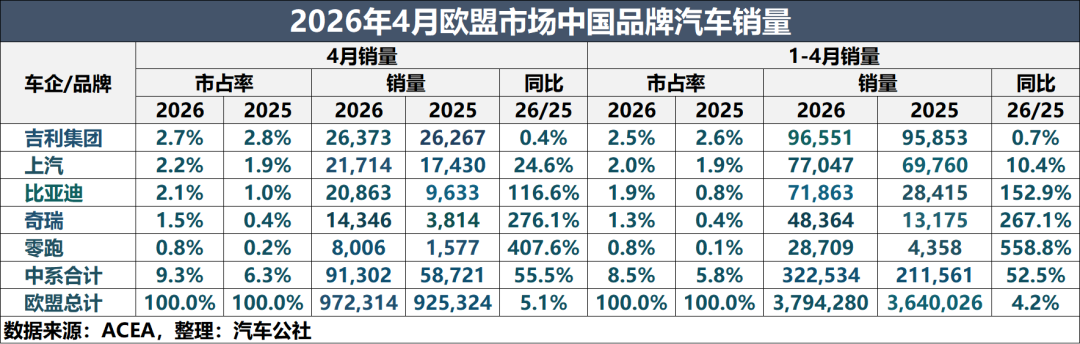

More notably, the market share of Chinese brands in the EU has surged from 0.5% in 2021 to nearly 10% by spring 2026. Sales, which have been almost entirely export-driven, are poised for transformation amidst the wave of local production in Europe.

This race against time signifies a reversal of roles between the automotive industries of the two continents and marks a new phase in the overseas expansion of Chinese automakers.

01 A Race Against Time

The question for Chinese automakers is no longer whether to build factories in Europe, but whether they can establish a presence before the EU fully closes the door.

The proposed Industrial Accelerator Act (IAA), while sounding like an 'accelerator' for European industry, resembles a slowly descending iron gate for Chinese automakers.

The bill mandates regulatory approval for foreign investments exceeding €100 million from countries that account for over 40% of global manufacturing capacity in critical sectors. Approval conditions include capping foreign ownership in joint ventures at 49%, requiring intellectual property licensing to EU entities, mandating that at least 50% of employees hold EU citizenship, and sourcing manufacturing inputs locally.

The 50% EU employee threshold is an inflexible red line.

Philippe Houchois, an analyst at Jefferies, stated bluntly at the June 10 Automotive News Europe Congress: 'The Chinese have always wanted to localize in Europe, but now they see the door closing. I think they're positioning themselves before things change.'

Experts predict that the bill will not formally take effect until mid-2027 at the earliest, leaving Chinese automakers with less than a year's window.

Why the urgency? Three numbers explain it all.

Number 1: 45%

EU tariffs on Chinese-made electric vehicles impose anti-subsidy duties of up to 45% on top of the 10% base import tax. This means a €38,000 Chinese electric car incurs over €10,000 in tariff costs alone. Local production eliminates this expense.

Number 2: From 0.5% to 10%

This is the trajectory of Chinese brands' market share in Europe. According to overseas data, it was just 0.5% in 2021 but neared 10% by spring 2026—a staggeringly steep growth curve.

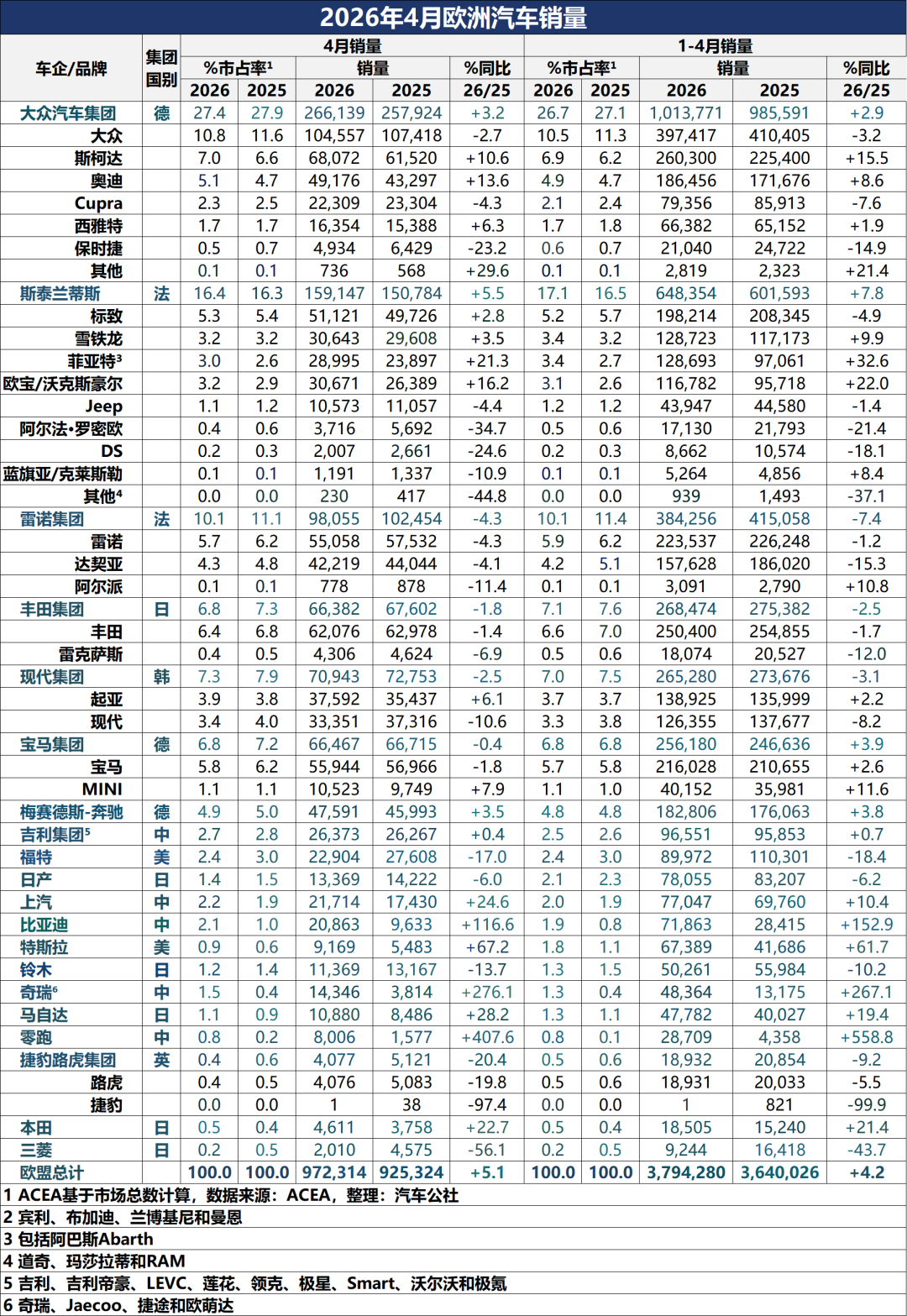

Data compiled by Automobile Commune from Europe's ACEA automotive federation shows that five major Chinese groups—Geely, SAIC, BYD, Chery, and Leapmotor—sold 322,000 vehicles in the EU from January to April, capturing an 8.5% market share and reaching 9.3% in April alone. Brands like FAW, Dongfeng, and XPeng are not yet included in ACEA statistics.

In April 2026, ACEA reported a 52.5% year-on-year surge in Chinese automakers' EU sales, while other agencies reported a 114% spike in Chinese car sales across Europe.

Number 3: 2-3 years

Building a new factory typically takes 2-3 years from site selection to production. With the IAA potentially taking effect by mid-2027, starting construction today risks leaving your factory without a foundation when the door closes.

Alfredo Altavilla, BYD's special advisor for Europe, put it bluntly: 'There's no time to start a greenfield project. All you can do is find existing factories, take them over, and retrofit them.'

This isn't 'building factories'—it's 'snatching them.'

02 Two Paths: Heavy vs. Light Assets

Chinese automakers' strategies in this land grab diverge sharply.

Path 1: Heavy assets

BYD leads this approach. Its €1 billion+ factory in Szeged, Hungary, aims for an annual capacity of 300,000 vehicles and plans to start production in Q4 2026—China's first large-scale factory in Europe.

However, BYD has faced setbacks. Its Hungarian plant, initially slated for late 2025 production, was delayed by about a year and is still installing equipment. Its Turkish project was halted, and a second European production base remains undecided.

Stella Li, BYD's executive vice president, revealed that the company now prefers 'buying factories' over 'building them'—retrofitting existing plants takes 12-18 months, less than half the time for new construction. Spain is the top candidate for its second base.

Path 2: Light assets

This route suits automakers seeking rapid localization without heavy factory investments.

Leapmotor exemplifies the 'light asset' strategy. In 2023, Stellantis acquired a 21% stake in Leapmotor, forming a joint venture called Leapmotor International.

In May 2026, they announced joint production of two models at Stellantis' Zaragoza plant in Spain—the Leapmotor B10 SUV and a co-developed Opel mid-size electric SUV—with production slated for October 2026.

Moreover, they're considering producing Leapmotor's new model at Madrid's plant from 2028, potentially transferring ownership to Leapmotor International.

Chery pursues a 'joint venture + revitalization' route.

In 2024, Chery formed a joint venture with Spain's Ebro Group, holding a 40% stake, to assemble vehicles at Nissan's former Barcelona plant, creating over 1,000 local jobs.

In June 2026, Chery signed a non-binding MOU with Nissan to explore producing Chery vehicles at Nissan's Sunderland plant in the UK.

Another clever 'borrowed path' is emerging: technology for capacity.

XPeng is negotiating with Volkswagen to acquire a European factory. Volkswagen CEO Oliver Blume previously stated he wouldn't rule out sharing European capacity with Chinese partners. Before this, XPeng had already entrusted Magna to contract-manufacture vehicles in Austria, taking its first step in local production.

03 An Expanding List

Here's a rundown of confirmed and ongoing strategic deployments:

BYD: Its Hungarian plant is nearing production, with a second base sought in Southern Europe, Spain being the top choice.

Chery: Its Barcelona joint venture factory in Spain is operational, exploring contract manufacturing at Nissan's Sunderland plant in the UK. In April 2026, Chery officially opened its European Operations Center and Spain Research Institute, elevating its 'localize for local markets' globalization strategy from product to systemic levels.

SAIC: MG is the best-selling Chinese brand in Europe. In 2025, MG registered 307,000 vehicles in Europe, up 37% year-on-year. The first quarter of 2026 saw 80,348 units. SAIC just announced plans to build its first complete vehicle factory in the EU in Spain's Galicia region, targeting an annual capacity of 120,000 vehicles and a 2028 production start.

Dongfeng: Stellantis will produce vehicles for Dongfeng's premium brand, Voyah, at its Rennes plant in France. Currently, the factory produces only one model—a Citroën SUV.

FAW: Its Hongqi brand is negotiating with Stellantis to use its Spanish plant for production.

Geely: Owning brands like Volvo, Polestar, Lotus, Zeekr, and Lynk & Co, Geely plans to purchase some of Ford's capacity in Valencia, Spain, according to reports.

XPeng: Negotiating with Volkswagen and Magna to explore local production paths in Europe.

Leapmotor: Leveraging Stellantis' two Spanish factories, Leapmotor is achieving European localization at breakneck speed.

Jefferies' May report estimates that based on announced and reported deals, Chinese automakers could eventually produce over 2 million vehicles annually in Europe—a figure capable of reshaping the continent's automotive industry.

04 Europe Wants Both, China Adapts

Europeans aren't naive.

The IAA's core goal boils down to one word: jobs. Europe's automotive industry faces unprecedented structural shocks, with Chinese automakers eroding market share through their early advantages in electrification and intelligence.

Stellantis has idled about 1.6 million units of capacity since 2019, while Volkswagen has around 800,000 units of excess capacity. Audi's Brussels plant, Nissan's Barcelona plant, and Ford's Saarlouis plant in Germany have all closed.

Europeans hope Chinese automakers' entry will revive idle capacity and preserve European jobs.

But the contradiction lies in Europe's desire to attract Chinese investment for rescue while fearing Chinese cars will dominate its market. The IAA seeks a balance: 'preserve jobs while retaining market share.'

With foreign ownership capped at 49% and at least half the workforce EU nationals, the message is clear: 'Leave your technology and money, but we keep market control.'

Chinese automakers' market share in Europe soared from 0.5% to 10% in five years. The next 10% won't come as easily.

The IAA bill is just the beginning. The EU is also considering a mandatory 70% local content standard for components, meaning mere final assembly in Europe won't suffice. Core component supply chains for batteries, electric controls, and motors must also 'relocate.'

This marks a comprehensive upgrade from 'exporting complete vehicles' to 'exporting entire systems.'

As Cheng Xiaoguang, XPeng's Northeast Europe head, bluntly stated when discussing the acquisition of Volkswagen's factory: 'It's a bit outdated.' This reflects Chinese automakers' shrewd calculation—they seek not Europe's obsolete robotic arms but 'local manufacturing' status, a responsive supply chain network, and a passport to bypass tariff barriers.

Before reaping these benefits, however, challenges remain: renovating Europe's aging production lines, negotiating with powerful unions, and managing cultural friction in operations.

This capacity race in Europe is less a 'land grab' than a struggle for discourse power and pricing authority. And time is running out.

Editor-in-Charge: Shi Jie Editor: He Zhengrong

THE END

-

![]()

In-depth | Survival Transformation of 38 Million Freight Drivers: How Platformization Defines the Next Decade?

-

![]()

Why Have ‘Computing Power Rental’ Companies Emerged as the Biggest Winners in the AI Era Amid Soaring Chip Prices?

-

![]()

DeepSeek's Financing Details Revealed! How Liang Wenfeng Secured Control

-

![]()

Valued at 210 Billion Yuan, Generating 42 Billion Yuan in Annual Revenue, Xiaohongshu May Proceed with IPO

-

![]()

Three Straight Months of Growth in Heavy Truck Sales: Both New and Veteran Players Are on the Same Wavelength!

-

![]()

AI Rewrites the Logic of Going Global: Cross-border E-commerce Reaches a New Turning Point

-

![]()

DeepSeek Secures Over 50 Billion Yuan in Initial Funding Round: Tencent and CATL Among Investors

-

![]()

Trillionaire Musk