China's Auto Industry Accelerates Expansion in Spain: From Vehicle Sales to 'Local Manufacturing in Europe'

06/22 2026

06/22 2026

504

504

In recent years, Chinese automakers have primarily focused on channels, branding, and imported models in European markets, relying on trade-based export strategies. However, with the EU's imposition of anti-subsidy tariffs on Chinese electric vehicles and the impending implementation of Europe's IAA Industrial Accelerator Act—as discussed in our previous article "Deep Dive into the EU's Industrial Acceleration Act: Rewriting the Rules for China's Auto Industry Expansion"—the traditional model of relying solely on Chinese manufacturing and exporting complete vehicles faces higher costs and greater policy uncertainty.

Spain, Europe's second-largest automotive producer, has now caught the attention of Chinese automakers due to its manufacturing infrastructure, mature parts (component) supply chain, deep-water ports, rail logistics, and high share of renewable energy.

Furthermore, Spain launched a 2030 Automotive Plan late last year—a strategic roadmap developed by the automotive industry, the Ministry of Industry, and the entire value chain. This plan aims to reshape the automotive ecosystem and accelerate electrified mobility.

As a result, Spain's role is evolving. It is no longer just a sales market for Chinese vehicles but is becoming a key hub for localized production in Europe for Chinese automakers, battery companies, and component suppliers.

This article synthesizes authoritative information to share the layout (layout) and plans of China's auto industry expansion in Spain.

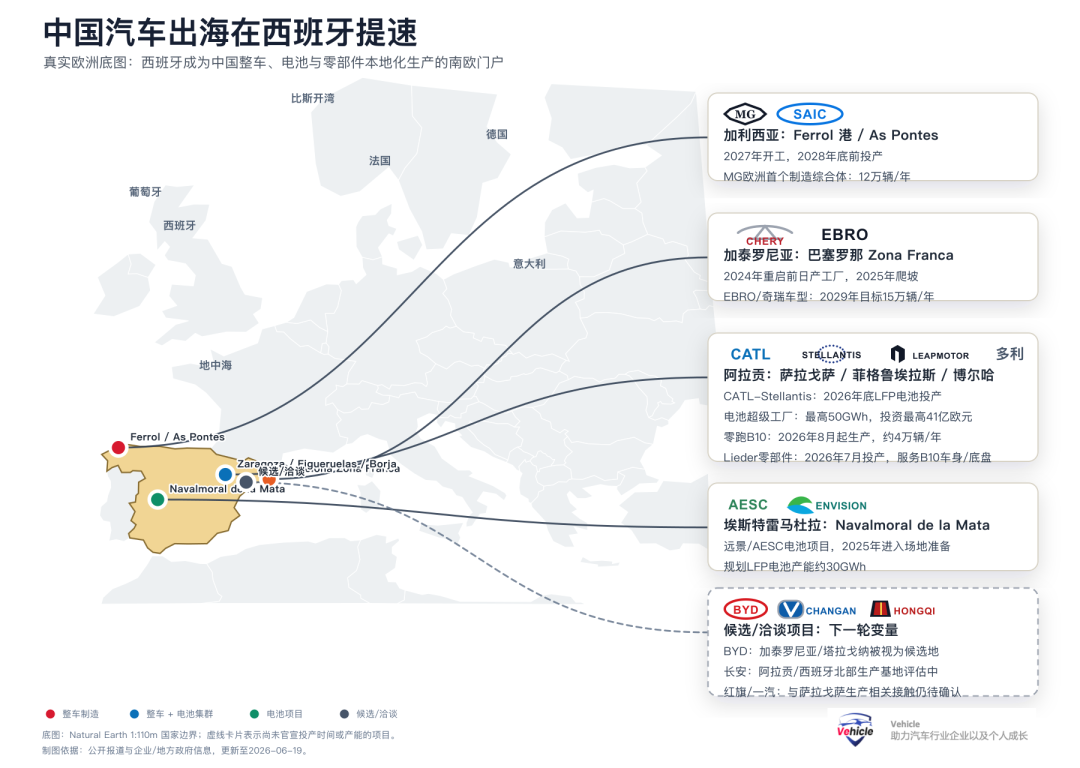

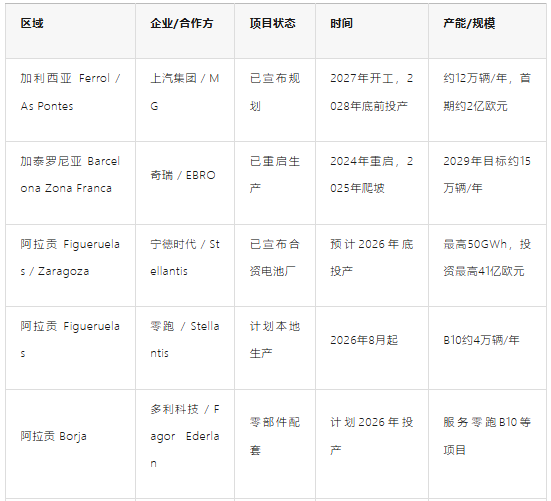

Barcelona: Chery Leads the Revival of European Vehicle Manufacturing

The flagship project for Chinese automakers in Spain is Chery's collaboration with Spanish EV Motors/EBRO in Barcelona's Zona Franca.

This site was formerly a Nissan factory that had been shut down. Chery and EBRO have reactivated it to produce EBRO-branded models while gradually introducing Chery's vehicle lineup. Public reports indicate that production resumed in 2024, with a ramp-up phase starting in 2025. Initially, assembly methods such as CKD/DKD will be used, followed by increased localization rates. The partners originally aimed for an annual production capacity of approximately 150,000 units by 2029. Recent Spanish media reports mention plans to expand the industrial footprint of the EBRO Factory and increase the 2030 production vision to around 200,000 units.

The significance of this project extends beyond "Chery having a factory in Europe." More importantly, it provides Chinese automakers with a relatively low-risk path to European manufacturing: revitalizing existing European automotive assets rather than building factories from scratch; entering through local brand partnerships and employment narratives rather than solely as Chinese brands; and covering not just pure electric models but also internal combustion, hybrid, and electric vehicles to meet Europe's still-diversified market demands.

Galicia: SAIC/MG Establishes Its First European Factory in a Port City

The Galicia project by SAIC and MG is the most closely watched vehicle manufacturing initiative among the latest wave of Chinese automaker layout (layouts) in Spain.

According to Spanish media and local sources, SAIC plans to build its first European manufacturing complex in Ferrol Port and As Pontes, Galicia, with an initial investment of approximately €200 million. The target is annual production of around 120,000 units, with construction expected to begin in 2027 and production launching before the end of 2028, creating approximately 2,300 local jobs. The project will primarily serve MG's production and supply in Europe.

MG already has a strong sales presence in Europe, but SAIC is among the companies facing higher tariffs under the EU's anti-subsidy investigation. For SAIC, local production in Europe will not only alleviate tariff pressures but also shorten delivery cycles and enhance the brand's "localized credibility" within European regulatory and consumer frameworks.

Galicia was selected due to its port conditions, industrial land availability, and aggressive local government recruitment efforts. Ferrol offers deep-water port and maritime distribution capabilities, while As Pontes provides space for industrial transformation. For Spain, this project aligns with local goals of re-employing and re-industrializing traditional industrial zones.

Aragon: A Cluster of Chinese EV Supply Chain Players Emerges Within Stellantis

If Barcelona represents a model for reviving vehicle manufacturing and Galicia a new port-based hub, Aragon resembles a "cluster testing ground" for China's new energy vehicle supply chain in Europe.

First is CATL's LFP battery mega-factory in partnership with Stellantis. The two sides plan to invest up to €4.1 billion in Zaragoza/Figueruelas to build up to 50GWh of LFP battery capacity, with production expected to start by the end of 2026. The strategic value of this project lies in connecting Chinese battery technology, Stellantis's European production capacity, and Spain's renewable energy advantages to provide a battery foundation for local EV production.

Second is the collaboration between Leapmotor and Stellantis. According to public information, the Leapmotor B10 is scheduled to be produced at Stellantis's Figueruelas factory starting August 2026, with an annual output of around 40,000 units. Subsequent models, including the Leapmotor B05, A10, and A05, are also planned for localized production in Europe. Furthermore, Stellantis plans to produce an Opel electric C-SUV using Leapmotor's technology platform in Zaragoza, indicating that Chinese companies' overseas expansion now extends beyond exporting complete vehicle brands to outputting platforms, electric drivetrains, battery architectures, and engineering capabilities.

Component suppliers are following suit. Chinese component maker Duoli Technology has partnered with Spain's Fagor Ederlan to establish Lieder Automotive, building a factory in Borja, Aragon, to supply body and chassis components for projects like the Leapmotor B10, with production slated to begin in 2026. This signifies that localization is progressing from "vehicle assembly in Europe" to "key component sourcing in Europe."

Aragon's advantages include its status as a major Spanish automotive manufacturing hub, with Stellantis already having mature production lines and a skilled workforce. Additionally, its location in northeastern Spain, connecting France, Mediterranean ports, and Iberian inland markets, makes it suitable as a European supply chain node.

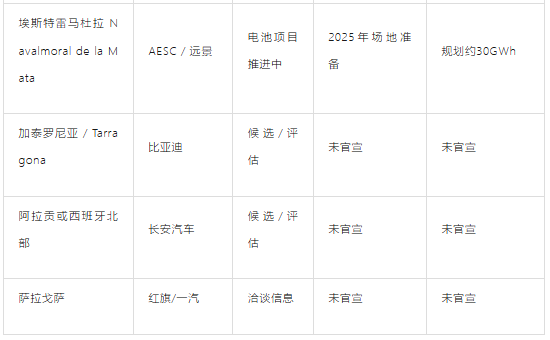

Extremadura: Battery Supply Chain Extends Further Inland

Beyond CATL, AESC—backed by Envision Group—is also advancing battery projects in Spain. The Navalmoral de la Mata project in Extremadura focuses on LFP batteries, with a planned capacity of around 30GWh. Public reports indicate that the project entered site preparation in 2025 and has received policy support from Spain's electric vehicle industry.

This project demonstrates that Spain is attracting more than just vehicle manufacturers. As European automakers shift toward low-cost LFP batteries, the investment value of Chinese and Chinese-backed battery companies in Spain will continue to rise. For Spain, battery projects also enable industrial layout (layout) to expand from coastal ports and traditional vehicle factories further inland, creating more dispersed employment and energy utilization scenarios.

Candidate Projects: BYD, Changan, and Hongqi Await Official Announcements

In addition to confirmed projects, several Chinese automakers remain in candidate, negotiation, or market entry stages.

For BYD, Spanish media report that Catalonia, particularly the Tarragona port area, is considered a potential candidate for its new European factory. However, as of now, BYD's confirmed European passenger vehicle production base remains primarily in Hungary, with no official project announced in Spain yet.

Changan Automobile has advanced its sales network in Spain through brands like Deepal and is evaluating production base options in Aragon. Given Aragon's existing clusters of Stellantis, Leapmotor, and CATL, Changan's potential choice of northern Spain or Aragon would align with the logic of Chinese automakers locating near mature automotive industry belts. However, it remains under evaluation.

Hongqi/FAW has also been mentioned by Spanish media as engaging with production resources in Zaragoza, but no confirmable production timeline, models, or capacity plans have emerged. Such information is better suited for ongoing observation rather than as confirmed investments.

Why Spain?

Finally, let's address the question: Why are Chinese automakers choosing Spain? The answer is not determined by a single factor.

First, Spain has a mature automotive industrial base. As Europe's second-largest automotive producer after Germany, it boasts complete vehicle factories, component suppliers, engineering talent, and experience in union negotiations. For Chinese companies, this is more practical than building a European manufacturing system from scratch.

Second, Spain offers port and logistics advantages. Ports like Ferrol, Barcelona, and Tarragona can handle the import and export of complete vehicles, components, and battery materials while facilitating access to markets in France, Germany, Italy, and North Africa.

Third, Spain has a high share of renewable energy. Battery manufacturing and EV production are increasingly sensitive to low-cost, low-carbon electricity. The landing of battery projects by CATL, AESC, and others in Spain is directly tied to the local environment of wind power, solar energy, and industrial electricity prices.

Fourth, the Spanish government and local authorities are actively recruiting investments. The transition to electric vehicles has left traditional internal combustion engine factories idle, creating employment pressures and industrial upgrading needs. Chinese investments align perfectly with policy goals of "re-industrialization" and "green supply chains."

Fifth, EU tariffs have altered overseas expansion calculations. For Chinese automakers, local production in Europe reduces tariff impacts, enhances supply chain resilience, and mitigates political pressures associated with being perceived as a "pure import shock." Spain offers a relatively balanced entry point in terms of costs, industrial foundations, and policy receptiveness.

A New Phase of Overseas Expansion

These projects indicate that China's auto industry expansion in Spain has entered a new phase: shifting from vehicle sales to factory construction, from complete vehicles to batteries and components, and from single-brand exports to collaborative restructuring of industrial chains with European automakers, local governments, and supplier systems.

Three key milestones warrant close attention in the coming year:

1. Whether SAIC/MG's Galicia project advances as planned with land acquisition, approvals, and construction commencement;

2. Whether Leapmotor B10, CATL's battery factory, and Lieder's component projects form a genuine localized supply closed loop (loop) in Aragon;

3. Whether one of the candidate projects—BYD, Changan, or Hongqi—elevates Spain from a "backup location" to an official European production base.

If these milestones are met, Spain will not only serve as a sales market for Chinese automakers in Europe but will become one of the most critical manufacturing gateways for China's new energy vehicle supply chain within the EU. Vehicle guess (speculates) that this outcome is highly likely and advises monitoring interactions between China and Spain.

Snapshot of Chinese Auto Projects in Spain

References and Images: Spain's Automotive 2030 Plan PDF - Spain.

*Unauthorized reproduction or excerpting is strictly prohibited-

-

![]()

"Current gasoline vehicles are akin to horse-drawn carriages of yesteryear."

-

![]()

Gasoline Vehicles Wait for Electric Vehicles to 'Stumble', Electric Vehicles Anticipate Gasoline Vehicles to 'Decline'

-

Entire 330-Kilometer Area Fully Unveiled! Hengqin Set to Eliminate Safety Officers and Steering Wheels Next Week, Ushering in China’s First Fully Autonomous City

-

![]()

New Energy Vehicle Order Rankings: Insights Revealed

-

![]()

China Invests Nearly 200 Billion Yuan This Year to Boost Car Sales

-

![]()

Oil Prices Revert to 7-Yuan Range: Are Gasoline Cars Getting a Reprieve?

-

![]()

Momenta Secures CSRC Approval: Is It Poised to Be the 'Pioneer in Physical AI Stocks'?

-

![]()

What's the Use of Having a General-Purpose Motion 'Cerebellum' for Humanoid Robots?