The decline of fuel vehicles is irreversible, and extended-range and plug-in hybrids may fare even worse

06/22 2026

06/22 2026

425

425

Li Xiang has suddenly begun to shift his attitude toward fuel vehicles.

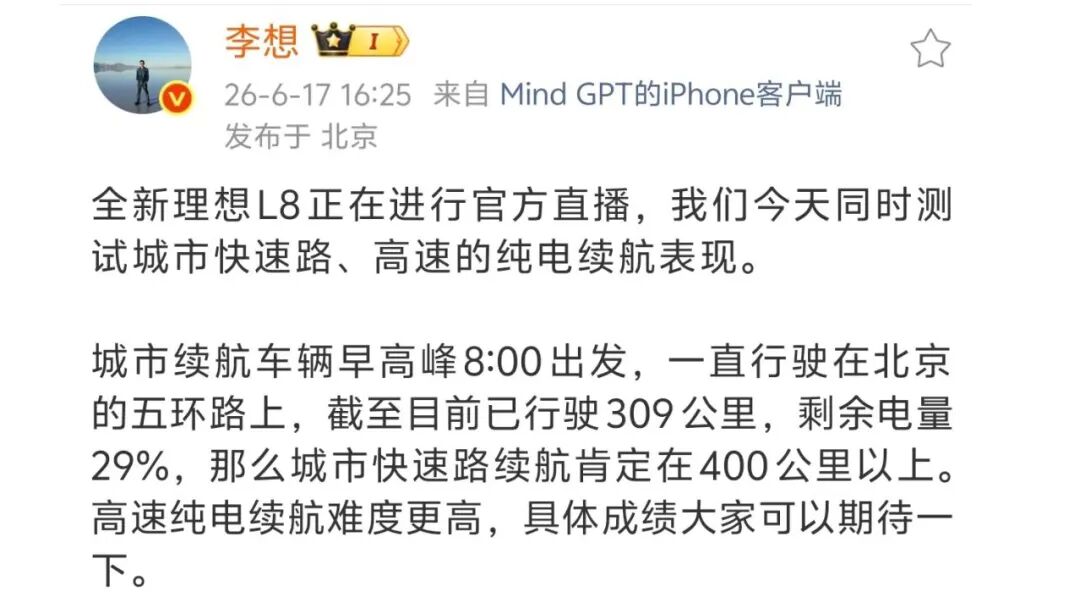

With the impending launch of the Li Auto L8, the new vehicle has entered a new round of promotion. Livestreaming, naturally, is one of the mainstream methods today, and Li Auto wants to showcase that its third-generation 5C extended-range BEV range can rival that of pure BEVs. However, in the latter part of Li Xiang's remarks, a term emerged—one that has long existed but has not been well-articulated: the energy disdain chain.

He stated that recently, some have noted a decline in the market share of extended-range vehicles and have begun to disparage the entire market. He argued that BEVs and extended-range vehicles should not engage in a ' Step on it, hold it up ' (criticizing one while praising another) approach or create an energy disdain chain. Instead, they should reflect on areas where they fall short and address unmet needs to collectively grow the pie of new energy vehicles.

This statement contains several points of contention. For instance, the perceived decline is not recent but occurred nearly a year ago. The energy disdain chain began five years ago when plug-in hybrids and extended-range vehicles looked down on BEVs. Additionally, this statement hides an underlying structure of opposition between fuel and electric vehicles.

Regardless, it is clear that Li Xiang has changed and adopted a less sharp (sharp) attitude. Previously, he claimed that 'extended-range vehicles can largely replace fuel vehicles,' that 'fuel vehicles reek of gasoline and feel stuffy,' and that 'the market share of fuel vehicles will soon be wiped out.' His current attitude is notably softer, acknowledging that fuel vehicles still attract nearly 40% of buyers and recognizing the competitiveness of models like the BMW X5 and Mercedes-Benz GLE.

The change in attitude naturally stems from shifts in market rhythm and trends, but the topic of the energy disdain chain is certainly intriguing.

More and more leading automakers are switching lanes

The energy disdain chain undoubtedly exists and will not disappear because of Li Xiang's remarks.

Different stances and mainstay products lead to implicit meanings in marketing attitudes and rhetoric. Since 2020, with the introduction of BYD's Blade Battery and DM-i technology, its sales have surged.

As a result, automakers did not need to promote which energy type was superior; the constant stream of customers in 4S showrooms and the increasing number of green-licensed vehicles on the roads spoke for themselves. However, in response to counterattacks from fuel vehicle manufacturers, a price war ensued between joint-venture automakers and BYD, with descriptions like 'electricity cheaper than fuel' or 'fuel cheaper than electricity.'

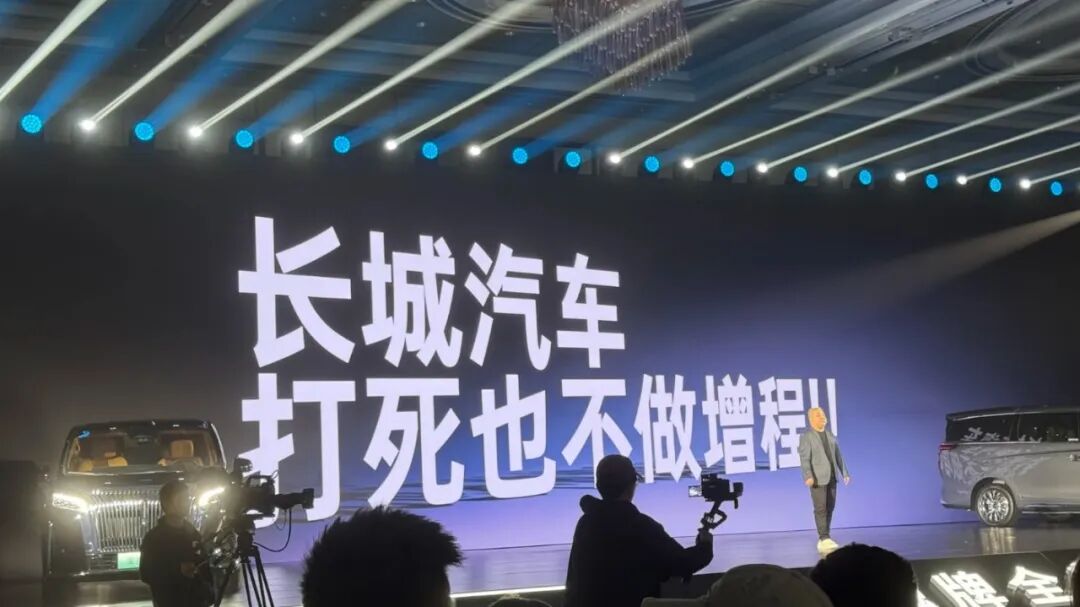

Plug-in hybrids were considered superior to BEVs due to their efficiency, fuel consumption, and consistency advantages, leading Great Wall Motors to declare that it would 'never make extended-range vehicles.'

Within plug-in hybrids, there is also an energy disdain chain: 3DHT systems are considered superior to single-speed systems, and higher thermal efficiency is favored over lower efficiency. The same applies to extended-range vehicles, where larger battery capacities are increasingly sought after to rival BEV capabilities, giving vehicles with larger batteries an advantage over those with smaller ones.

The same logic applies among BEVs: 800V systems are considered superior to 400V systems, full 800V architectures are preferred over partial ones, and 900V systems outperform 800V systems. Even among full 800V systems, comparisons extend to battery capabilities, with 6C rated batteries considered superior to 5C and 4C rated ones.

Wasting time on a question without a clear answer is no different from fan wars.

In the end, actions speak louder than words. Extended-range, plug-in hybrid, and BEV models can all serve their respective user bases, but the automotive market is unforgiving. The mainstream is determined by which technology gains wider acceptance.

Based on market performance during the Dragon Boat Festival week, three leading automakers are clearly changing their strategies: AITO, BYD, and Leapmotor.

BYD's launch of the Tang model followed the approach used for the Song Ultra, prioritizing BEVs before introducing plug-in hybrids. From a business perspective, this makes sense. The most significant technology launched in 2026 is the second-generation Blade Battery with megawatt flash charging, which aims to shatter traditional consumer perceptions. The results have exceeded expectations, with multiple expansions of second-generation Blade Battery production.

During a group interview following the launch of the Leapmotor C10, C11, and C16, Zhu Jiangming was asked about his views on the development trend of BEVs and Leapmotor's related adjustments and actions.

He replied, 'I am the most radical when it comes to new energy. The trend toward electrification will further accelerate. The proportion of BEVs will continue to grow, while the opportunity for extended-range vehicles lies with affluent consumers who can opt for larger batteries, such as extended-range models with a 500-kilometer BEV range. In colder regions, using fuel may be more comfortable and economically balanced during certain periods.'

Additionally, the AITO M6 exhibits a striking phenomenon that can be seen as an exploratory move to further disrupt the market with BEVs.

The 'good days' for plug-in hybrids and extended-range vehicles are over, but they are not being eliminated

On June 14, 2026, news began to circulate about the launch of the AITO M6 BEV variant. On June 16, the new model was launched with a price range of 229,800 to 249,800 yuan. From a purely vehicular perspective, this pricing is reasonable, as the battery capacity was reduced from 100kWh to 81kWh, along with some configuration adjustments, leading to a price decrease.

However, it is important to note that the previous entry-level price of the AITO M6 was 259,800 yuan, representing a 30,000 yuan reduction this time, effectively targeting a different user group. The current pricing of the new AITO M6 also puts the smaller AITO M5 in a difficult position, as the BEV Ultra rear-wheel-drive version of the M5 is priced at 239,800 yuan, making it 10,000 yuan more expensive than the M6.

Furthermore, AITO is breaking away from its original product logic by allocating more resources to BEV models than to extended-range ones.

It is evident that automakers are responding to the latest consumer demands with concrete actions. In addition to the three mentioned above, leading companies like Geely and Changan have also significantly increased their BEV-related activities in 2026.

Geely's Galaxy Starship 7 quickly added a BEV variant, while the all-new Seres S07 adopted a marketing strategy of launching the BEV version before the extended-range one. Additionally, Huawei-affiliated products are making more pronounced attempts at BEVs. In the emerging market for sporty coupes and sporty wagons, the Qijing GT7, Shangjie Z7, and Shangjie Z7T are currently offering only BEV versions.

After analyzing so much, it is clear that the automotive market has always undergone cyclical changes.

Those who make longer-term, more accurate, and forward-looking choices will have higher and more favorable upper limits for subsequent development. This applies not only to companies but also to individuals. From another dimension of the market, the trajectories of two automakers easily illustrate this point.

In 2025, a new landscape emerged in the Chinese automotive market. Among new energy vehicle manufacturers, only two had not embraced internal combustion engines: Tesla and NIO.

Tesla has long been pursued by multiple automakers in various attempts, including powertrain forms, pricing strategies, and intelligent driving assistance. As of now, its latest performance is telling. Although Full Self-Driving (FSD) has not yet officially launched, Tesla has only lost its market-defining authority but still retains market influence. In May of this year, its retail sales in the Chinese market reached 47,700 units, up 22.5% year-on-year, ranking tenth.

NIO's story is even more compelling. From nearly facing a funding crisis to its current state, the label of 'the most miserable person' attached to Li Bin has long since disappeared, replaced by terms like 'blockbuster,' 'most down-to-earth,' and 'most hardworking.'

More importantly, amid the current intense competition, where most automakers are experiencing declines, NIO has managed to grow without engaging in price wars or offering discounts.

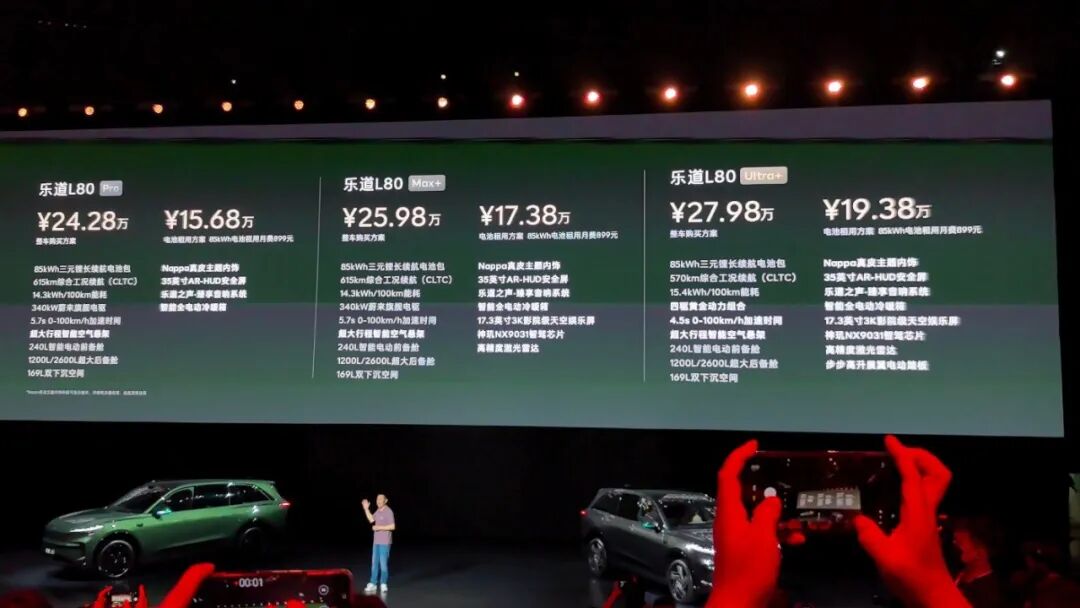

The NIO ES8 has achieved monthly sales exceeding 10,000 units for seven consecutive months, consistently ranking at the top of the sales charts. The NIO Firefly has been on the market for over a year, with recent orders further increasing and delivery lead times slightly extending. The newly launched Leapmotor L80 achieved nearly 6,000 units in sales within just half a month.

The newly launched Leapmotor L60 has also received feedback from many dealerships indicating stable daily sales of over 20 units, with test drives requiring queues. In some populous cities, scheduling test drives for the next day is often necessary.

In summary, the data clearly shows that Chinese automotive consumption, especially for family vehicles, has deeply shifted toward the BEV mainstream. Beyond technological advancements and infrastructure changes that have altered perceptions, the core reason lies in economic operating principles.

Why can new energy vehicles quickly take market share from fuel vehicles? The core reason lies in the significant improvement in technological efficiency. Coupled with the shift in energy strategy, the usage cost of new energy vehicles has undergone an irreversible upgrade through continuous technological advancements.

A recent hot topic is that fuel vehicles have disappeared from the TOP 10 list in May, whereas just six months ago, they occupied seven spots. The underlying logic here is that in the low-budget segment, new energy vehicles have become the absolute mainstream. Currently, between 150,000 and 200,000 yuan, they still possess significant vitality. For example, in Geely's May sales, the sales of the China Star series actually surpassed those of new energy vehicles. Another example is that among the TOP 10 mid-sized sedans, the ratio of fuel vehicles to new energy vehicles is 60% to 40%. In the luxury car market above 250,000 yuan, fuel vehicles still have considerable vitality.

It is evident that the current situation faced by plug-in hybrids and extended-range electric vehicles is similar to the trend of fuel vehicles. The market operates in such a way that technologies that can meet new demands will capture more market share, and this is difficult to change.

In Conclusion

In addition to insights from bosses, executives, automakers, and frontline sales, there is more data supporting the case for pure electric vehicles.

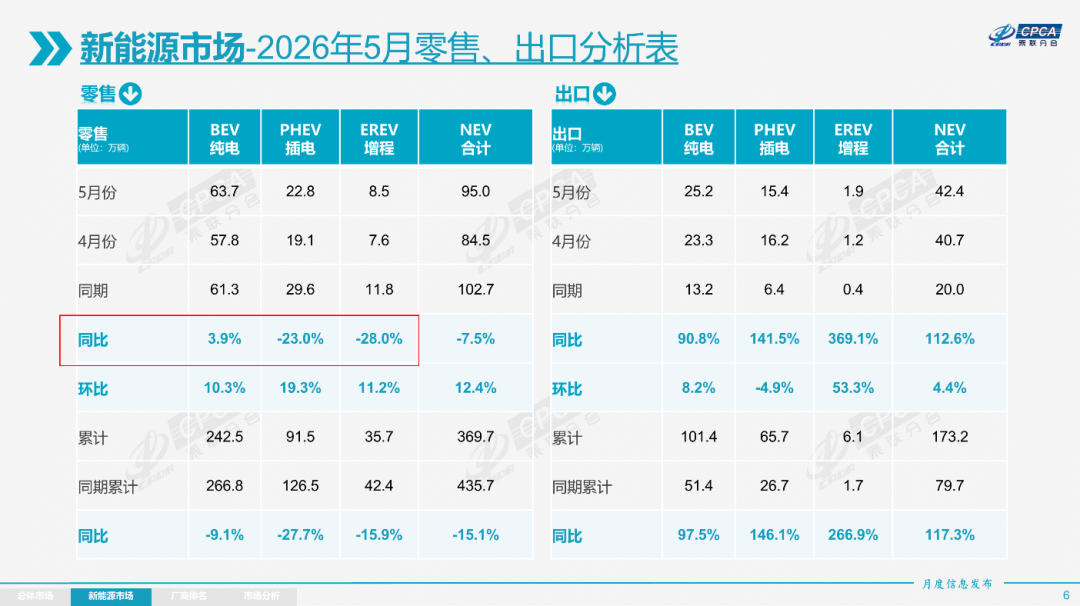

In the retail sales of the Chinese market from January to May 2026, the proportion of pure electric vehicles in new energy vehicle sales further increased from approximately 60% for the entire year of 2025 to 63.7%. Plug-in hybrids saw an 18% year-on-year decline, with their proportion dropping from around 28% in 2025 to 26.5%. Extended-range electric vehicles, which were high-growth stars from 2024 to 2025, became the segment with the largest decline in 2026, with wholesale volumes in May dropping nearly 25% year-on-year.

Of course, when facing these data, one must remember not to adopt a binary viewpoint. It does not mean that the end of good times for extended-range and plug-in hybrids equates to their elimination; they still have their own survival space and capabilities.

However, there is no doubt that the rise of pure electric vehicles is irreversible. Automakers that have held firm in this area from the beginning are now reaping greater rewards.

-

![]()

Enflame Technology Clears IPO Hurdle: A Daring Venture into CUDA-Incompatible Realm

-

![]()

Significant Shifts in Home Appliance Market Trends During This Year’s 618 Shopping Festival

-

![]()

Insta360 Fights Back! Standing Up to Black PR Operations", "Insta360 Innovation, Black PR Operations, Patent Litigation, Market Competition, Financial Performance", "Insta360 Innovation, targeted by b

-

![]()

Home Appliance Enterprises: Shifting Focus from Traffic Acquisition to User Retention

-

![]()

Re-imported Cars Dilemma Unveils the Fallacy of Japanese 'Craftsmanship Spirit'

-

![]()

Stepping onto a New Path, Yet Hongqi Faces Familiar Challenges

-

![]()

Should Honda Offer Toshiaki Mibu a Second Chance?

-

![]()

The Qualification Remains, But Where Does Zotye’s Future Lie?