Targeting 12 Million in Exports! China’s Auto Industry Faces a Pivotal Test of Maturity

06/23 2026

06/23 2026

327

327

Lead-in

Introduction

This industrial counterattack, traversing mountains and seas, is not only a historic opportunity in a century of upheaval but also a profound test of internal and external competition.

“The bourgeoisie, through the rapid improvement of all instruments of production and the immensely facilitated means of communication, draws all nations, even the most barbaric, into civilization... Its cheap commodities act as powerful artillery, breaking through all Chinese walls and overcoming even the most persistent hatred of foreigners.”

One hundred and seventy-eight years ago, Marx and Engels co-authored The Communist Manifesto, revealing the core secret behind modern capitalism's global sweep: commodities are the invisible heavy artillery with which European and American powers conquer the world. Leveraging low-cost goods enabled by industrialization, Western powers shattered geographical constraints, reshaped global supply and demand, and established a centuries-old “center-periphery” global value chain, cloaking their monopolistic hegemony in the rhetoric of “free trade.”

Looking back at the past three centuries, it was precisely this commodity-based heavy artillery that allowed Western powers to force open the gates of Asian, African, and Latin American nations, including China. Yet today, the roles have reversed—the entity wielding the global industrial competition artillery has undergone a historic shift.

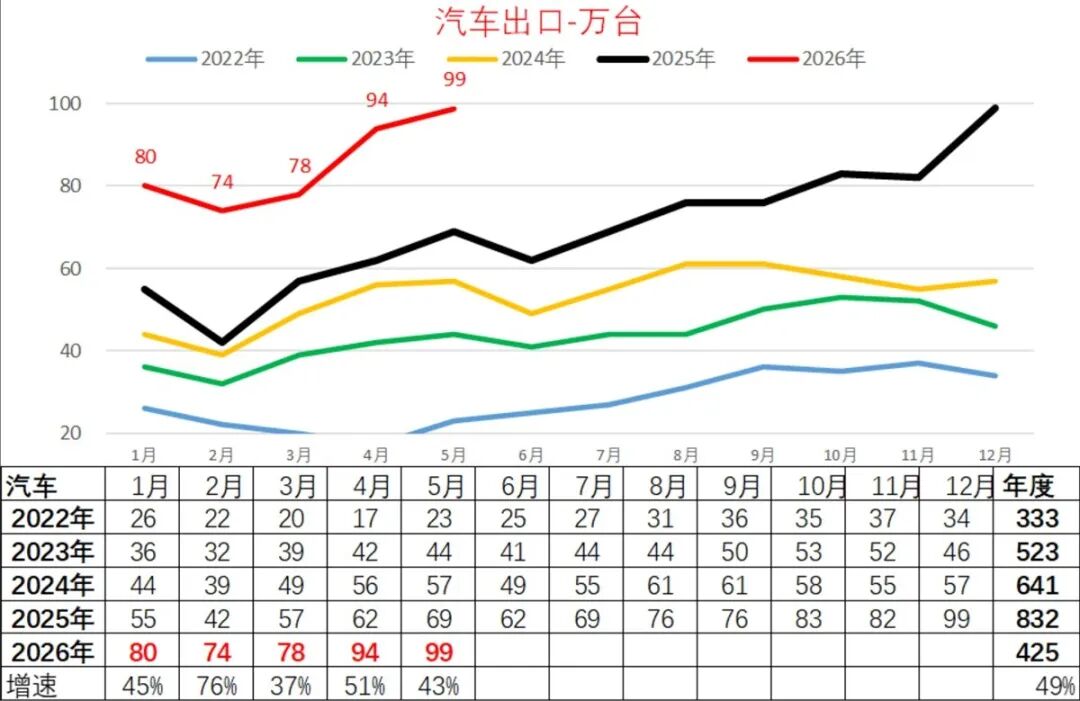

According to the latest data from the China Association of Automobile Manufacturers, the scale of this monumental industrial transformation is evident. In May this year, China exported 930,000 vehicles, a year-on-year surge of 68.7%, marking the second consecutive month of exports exceeding 900,000 units. From January to May, domestic automotive exports reached 4.059 million units, up 63% year-on-year, reflecting a formidable outward push.

Figure 丨 Attention! This image is sourced from a personal analysis article by Secretary-General Cui Dongshu of the China Passenger Car Association, using a broad definition of vehicle exports that may include knockdown kits and other conversions.

Leveraging robust production capacity, ample orders, and increasingly mature overseas channels, industry insiders predict that China's automotive exports will approach 5 million units in the first half of this year, with the annual total likely exceeding 10 million for the first time, setting a new historical benchmark. Cui Dongshu, Secretary-General of the China Passenger Car Association, is even more optimistic, projecting that based on the industry's typical second-half production and sales surge, China's automotive exports could reach 12 million units by 2026, ushering in a new era of global expansion.

This tidal wave of overseas expansion has injected vitality into a domestic automotive industry mired in sluggish demand. In the first five months of this year, domestic automotive sales fell 19.5% year-on-year. The surge in overseas markets has offset downward pressure from domestic cycles, stabilizing corporate operations.

Yet beneath this prosperity, hidden currents churn.

As Chinese-made commodity heavy artillery rolls across the globe, progressively squeezing the living space (market space) of established Western automakers, the century-old trade landscape has begun to shift. A profound question of the era arises: Can the free trade order, once dominated by the West, endure?

With the global “center-periphery” dynamic fully reversed, traditional industrial powers, confronted by reverse encroachment from emerging economies, will inevitably break rules, erect barriers, and launch all-out counterattacks.

01 Exports Buy Time but Are Not the Ultimate Solution

To grasp the deeper significance of exporting 10 million vehicles, one must first understand the industry's essence: automobiles are the most complex terminal products in the modern industrial system, with the longest supply chains and broadest cross-sector linkages. Producing a single vehicle involves tens of thousands of components spanning heavy industry, chemicals, electronics, intelligent algorithms, and more.

China's absolute advantage in global automotive markets today stems from deep cultivation across the entire supply chain. From precision processing of core lithium-ion minerals to autonomous iteration in battery materials and cell manufacturing, and the global new energy footprint established by BYD and CATL, China's new energy vehicle sector has built a self-reliant, controllable full-industry chain. Sharpened by fierce domestic market competition, the entire chain now ranks among the world's elite in production efficiency and cost control.

With domestic auto retail sales declining nearly 20% year-on-year in 2026, exports exceeding 10 million units have become a strategic buffer zone for China's manufacturing sector, a floodgate relieving overcapacity pressures across the supply chain. Without massive external demand, financial risks would cascade through the chain, threatening millions of upstream and downstream jobs.

Yet we must remain sober: the current “cold domestic, hot overseas” imbalance breeds hidden developmental pitfalls. With weak domestic consumer confidence and unresolved demand shortfalls, the industry's growing reliance on foreign markets risks fostering the illusion that external demand can perpetually offset internal weakness. Each wave of large-scale commodity exports restructures and disrupts host countries' domestic industries. Greater export volumes intensify global pushback and containment.

Meanwhile, structural imbalances in export benefit distribution are widening. New energy industry hubs in the Yangtze River Delta, Pearl River Delta, Chongqing, and Hefei reap outsized gains from overseas expansion, while aging heavy industry and foundry sectors in traditional fuel vehicle strongholds decline. The impressive GDP figures from 10 million exports mask deeper regional industrial polarization and sectoral imbalances.

At a deeper level, intertwined contradictions emerge: How to equitably distribute export dividends between public and private capital? Does rising industrial concentration erode workers' employment opportunities and bargaining power? Does excessive export orientation divert resources from nurturing domestic demand?

These interlocking structural contradictions represent core bottlenecks to the industry's long-term healthy development. Until this wave of overseas expansion resolves these deep-seated issues, it remains merely a strategic window for domestic industrial transformation and domestic demand recovery—not a permanent solution.

02 Beware of Europe and America's “Weaponized Rules” Containment

The export blueprint of 10 million units annually, peaking at 12 million, has been oversimplified in today's jingoistic online discourse as a triumphant “domestic brands prevail” narrative, overlooking rapidly accumulating risks.

As previously noted, the automotive industry's sheer scale makes it never merely manufacturing but a vital sector determining regional and national prosperity. When China's automotive exports dominate globally, trade volumes surpassing critical thresholds transform pure commercial exchange into national-level rule game theory (strategic competition) and power confrontation.

The “free trade” doctrine championed by the West for centuries has never been a universal principle but merely a tool to harvest profits during periods of industrial hegemony. When emerging economies threaten their monopolistic gains, the West promptly abandons free market rhetoric, invoking “security” and “compliance”—even weaponizing “human rights” and other issues—to mobilize state machinery against market forces.

Based on existing evidence, Western suppression of China's automotive sector employs more covert, systemic methods than conventional tariff barriers. At its core, this approach repackages judicial sanctions, financial controls, and administrative interventions—state coercive power—as “non-military institutional heavy artillery” to comprehensively contain China's automotive overseas expansion.

Tariffs and quotas represent the most overt initial barriers. The EU imposes tiered tariffs, while the US excludes Chinese-made vehicles entirely. The US employs national security overreach as its precision strike tool, exaggerating data risks in intelligent connected vehicles and distorting commercial competition into national security threats through foreign investment reviews and entity lists. Europe focuses on standards and carbon barriers, erecting formidable compliance walls through battery passports, lifecycle carbon accounting, and supply chain due diligence—all targeting China's new energy upstream sectors and dramatically raising compliance costs.

Beneath these overt trade barriers, darker currents flow: US-Europe coordination to advance technology-finance decoupling and weave global containment nets. The US continuously expands its entity list to suppress Chinese firms, coerces allied nations to cut off technology channels for Chinese automakers' overseas expansion, and pressures transit markets like Mexico, Turkey, and ASEAN to set “Chinese content thresholds” to block circumvention risks.

The Western suppression logic centers on bypassing WTO multilateral arbitration, repackaging “national security” and “climate justice” as moral justifications to unilaterally rewrite trade rules. This reflects the inevitable outcome when monopoly capital and state machinery become deeply intertwined: when market tools fail to contain China's industrial rise, state coercive power takes center stage.

Export risks extend beyond developed Western markets. While Southeast Asia, the Middle East, and other emerging markets represent growth blue oceans for Chinese automobiles, most developing economies suffer weak governance systems and scarce foreign exchange reserves. As Chinese automotive imports surge, these countries may impose import bans, foreign exchange controls, or mandatory local production requirements, creating sudden risks for automakers' overseas expansion.

In short, the more forcefully China's automobiles expand overseas, the greater their power to reshape global industrial patterns. Normalized, multi-tiered, and omnidirectional trade competition has become the enduring backdrop for China's automotive globalization.

03 Beneath the “Artillery Fire,” What Constitutes a True Competitive Moat?

Marx's theory of commodity heavy artillery exposes the core logic of capitalist globalization—markets never operate as vacuum-sealed fair exchanges but as extensions of national power and industrial discourse rights. Viewing the historic leap of exporting 10 million vehicles demands dialectical clarity: this breakthrough represents a magnificent counterattack by modern Chinese industry, yet we must confront our shortcomings: currently, we wield only the “commodity heavy artillery,” while our opponents command entire state apparatuses constructing “rule barriers.”

Tariff barriers merely mark the frontlines of competition. The true crisis lies in Europe and America defining China's automotive industry as a “systemic challenge” and deploying comprehensive state power—through technical standards, data security, and financial isolation—to compress its global space. This means that in the second half of China's automotive globalization, sole reliance on cost-performance advantages cannot sustain long-term breakthroughs.

The true industrial competitive moat lies not in short-term sales peaks but in enduring industrial rooting capacity and systemic resilience. Chinese automakers must transcend superficial “low-price, high-volume” logic, align with regional interest landscapes, and deeply embed into local economies through localized production and supply chains to eliminate pretexts for external containment.

While enterprise-level market deep cultivation (deep cultivation) forms the bedrock of sustained success, market actors alone cannot withstand state-level systemic containment. Commodity heavy artillery can breach market barriers, but only rooted coexistence, rule adaptation, and interest binding (stakeholder alignment) can secure market foundations. Export volumes in the tens of millions represent China's manufacturing sector's coming-of-age ceremony—our debut at global competition's core arena, where we must both pierce through with industrial strength and meet containment with strategic poise.

This surge of overseas expansion has won precious time to repair domestic demand and optimize structures. We must wield commodity heavy artillery to shatter century-old industrial barriers while transforming breakthrough momentum into global industrial resilience. As enterprises engage on the front lines, the state must provide robust support through institutional openness, international rule negotiation, and China-style legal strength to fortify industrial overseas expansion and form a “corporate advance, state escort (state escort)” synergy.

As Marx stated: “The weapon of criticism cannot, of course, replace the criticism of weapons, material force must be overthrown by material force; but theory too becomes a material force as soon as it has gripped the masses.” Automobiles, as contemporary industrial material force par excellence, will ultimately carry China's manufacturing legacy of half a century to complete a metamorphosis from scale breakthrough to systemic victory amid global competition.

Editor-in-Charge: Shi Jie Editor: He Zengrong

THE END

-

![]()

Geely's Three Strategic Cards for Future Layout Unveiled at Hong Kong Auto Show

-

![]()

GAC Toyota’s Sales Boom: Forging Vehicles with Enduring Value for the Long Haul

-

![]()

Insider Insights on Brazil’s Internet Landscape: No Chinese Firm Has Made Significant Profits in 25 Years

-

![]()

【OFweek Weike Cup】HG Genuine Optics Nominated for 2026 Excellent Optical Component Supplier in the Optical Industry

-

![]()

European Sales of Chinese Vehicles Surge 1.5-Fold in a Year! EU Takes Action: Additional Tariffs on China’s Plug-in Hybrid Vehicles

-

![]()

Soaring 19-Fold, Market Value Hits Trillions: Is Zhipu a Legend or a Speculative Bubble?

-

![]()

【Electric Equipment】The first standard for shore power facilities of electric ships is introduced and will be officially implemented on August 1

-

![]()

【Intelligentization】Joint Development of Right-Hand Drive Robotaxi: Geely Yuancheng, WeRide, and Kwoon Chung Bus Sign Agreement