With 370 Million Vehicles on the Road, the Auto Industry Reevaluates Its Post-Sale Business Strategy

06/24 2026

06/24 2026

554

554

On June 23, the State Council Information Office held a press conference to unveil measures aimed at boosting automobile consumption across the entire supply chain. Two key policies were announced: 40 cities will spearhead reforms in automobile circulation and consumption, and nine departments, including the Ministry of Commerce, will introduce 17 measures targeting the automotive aftermarket.

Customization, recreational vehicles (RVs), classic cars, maintenance, insurance, racing, and leasing—businesses that were once on the fringes of the automotive industry—are now encompassed within the same policy framework.

From an operational standpoint in the automotive sector, the message from this press conference is unequivocal: with 370 million vehicles now in circulation, policies are shifting their focus to the post-sale phase.

New cars will continue to be sold, but relying solely on new car sales is no longer viable.

In recent years, automobile consumption policies have primarily focused on purchase tax incentives, trade-in programs, promotion of new energy vehicles in rural areas, and the construction of charging and battery swap infrastructure. These policies have effectively bolstered the market.

As of June 22 this year, trade-in programs for consumer goods have cumulatively driven sales of related products worth 5 trillion yuan, with automobiles accounting for 63%. Over 21 million people have traded in their old cars for new ones through these programs, receiving an average subsidy of 14,000 yuan per vehicle. Last year, domestic passenger vehicle retail sales reached a record high of 23.74 million units.

However, the press conference also acknowledged that automotive consumption growth is facing temporary pressure this year.

The issue is not hard to grasp. The penetration rate of new energy vehicles has exceeded 60% for two consecutive months, making electrification a mainstream choice rather than just an incremental option. After several rounds of price adjustments, consumers have become more price-sensitive and cautious in their decision-making regarding vehicle replacement. While the new car market remains vast, growth increasingly needs to be found within the existing vehicle fleet. Many of our previous articles, such as 'May's Chinese Auto Market Analysis: A Fig Leaf, Two Fault Zones, and Three Surprises,' have discussed the double-digit decline in domestic market sales this year.

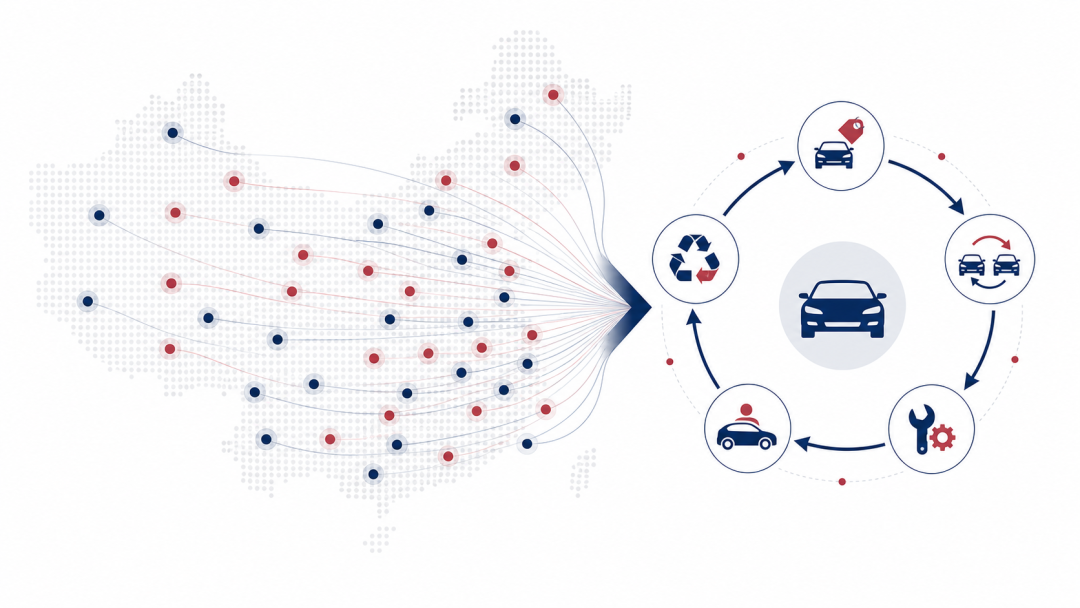

The national automobile fleet has reached 370 million vehicles, with over 50% of passenger vehicles being over seven years old. These vehicles generate daily demand for maintenance, insurance, parking, charging, customization, leasing, and replacement. While the industry used to focus more on annual car sales, it must now begin calculating how much revenue a single vehicle can generate over its ten-plus years of use.

This is why the policy places a separate emphasis on the automotive aftermarket.

Automakers Must Adapt to a New Lifecycle Accounting

For automakers, this policy will provide some short-term sales support, but its deeper impact lies in business model transformation.

Pilot cities such as Hangzhou, Guangzhou, and Shenzhen will explore optimizing car purchase restrictions or usage environments, while accelerating the circulation of used cars will also shorten vehicle replacement cycles. Older cars will be easier to sell, facilitating consumer purchases of new ones. Policies on racing, camping, and customization may create niche demand for off-road vehicles, pickups, performance cars, MPVs, and RV chassis.

However, the policy also touches on some core interests of automakers' after-sales systems.

The document explicitly states that automobile manufacturers cannot restrict consumers' freedom to choose maintenance providers or use this as a reason to refuse fulfilling their statutory 'three guarantees' responsibilities (which include repair, replacement, and refund). The policy also proposes guiding new energy vehicle and battery manufacturers to open up maintenance technology authorizations and encouraging battery repairs instead of replacements.

In the past, when some new energy vehicles experienced battery or electronic system failures, consumers could only return to the brand's service network for repairs, with some faults even requiring complete component replacements. This model led to high repair costs, pressure on insurance companies, and increased the total lifecycle usage costs of vehicles.

As maintenance technologies gradually become more open, automakers will reduce their reliance on proprietary diagnostic systems, exclusive parts, and authorized maintenance. Independent maintenance businesses will gain new market opportunities, and consumers will have more choices.

Automakers will now need to reconsider product maintainability, parts supply cycles, battery repair costs, insurance expenses, and residual values of used cars. All these factors will influence whether the next vehicle can be sold to the same customer.

Dealers Face Opportunities and More Direct Competition

With persistent price competition on new cars, many dealers have found it difficult to profit from vehicle price differentials. Used cars, maintenance, insurance, financing, accessories, and leasing should have become important revenue streams for dealers, but many stores have yet to truly develop these capabilities.

This policy opens up more operational space for dealers.

Large dealer groups can transform their stores into comprehensive automotive service centers, integrating new car trade-ins, used car inspections and sales, insurance, maintenance, factory customization, and leasing services into a single system. Compared to one-time new car sales, these businesses can foster more stable customer relationships and cash flow.

Pressure will also increase. The policy encourages the specialized, branded, and chained development of maintenance businesses and requires new energy automakers to open up maintenance technology authorizations. 4S stores will face more independent maintenance chains and professional new energy maintenance businesses.

Stores that rely solely on manufacturer authorizations, original parts, and labor fees may not find life easier. Dealers who truly seize opportunities will need to excel in used car pricing, battery inspections, insurance and financing, and customer operations. The number of stores alone will not automatically translate into competitiveness.

Used Cars Are a Key Link in This Reform

In 2025, China's used car transaction volume exceeded 20 million units for the first time, with a cross-provincial transfer rate of 31.1%. From January to May this year, 8.1 million used cars were traded, up 2.3% year-on-year. The ratio of new car consumption to used car transactions also reached approximately 1:1 for the first time.

Used cars connect new car sales and end-of-life recycling. The faster old cars circulate, the smoother new car replacements will be.

The main issues remain opaque vehicle condition information, inconsistent inspection standards, fragmented operators, and inconvenient cross-regional transactions. Chengdu proposes establishing an inspection and evaluation service platform to promote mutual recognition of inspection reports while improving price assessments, transaction invoicing, and one-stop registration services. Hangzhou is experimenting with moving traceability, transactions, and registration online.

If these measures can be replicated, the turnover cycle and capital occupation of used cars will decrease, and large dealer groups, branded certified used cars, and professional platforms will gain more market share. Small-scale car dealers relying on information asymmetry will face increased pressure.

New energy used cars still face a significant challenge. There is currently no unified valuation standard for battery health, repair records, intelligent driving features, and software subscription rights. Whoever can provide credible battery inspections and residual value management may gain a crucial entry point into the new energy used car market.

Modifications and Maintenance Must Emerge from the Gray Market

Domestic demand for car modifications has always existed, but the limited number of legal modification projects, unclear registration processes, and inconsistent part standards have kept much of this demand in the gray market.

This policy proposes tiered and classified management, creating a list of modification projects, improving vehicle inspections and registration changes, and studying certification systems for modification parts.

For consumers, this means more modification projects may become legally registrable and insurable in the future.

For the industry, modification parts, inspection certifications, professional installation, and modification insurance could form a more complete chain.

This does not mean car modifications are fully liberalized. The document still contains many phrases like 'study the establishment of,' 'support exploration of,' and 'accelerate the formulation of.' Specifics on what can be modified, how to register, and how insurance will underwrite these modifications will depend on local and departmental implementation rules.

Therefore, in the short term, modification brands with research, certification, and distribution capabilities are likely to benefit first. The survival space for non-standard parts and non-compliant installations will shrink.

RVs, Racing, and Classic Cars: Small Scale, Big Value Beyond Sales

RV camping, car racing, and traditional classic cars are unlikely to become multi-million-unit markets, but they offer additional value by extending automobile consumption into travel, sports, collectibles, culture, and communities.

Chengdu's approach is representative. The city hopes to drive demand for modifications, high-end parts, training, cultural creativity, accommodation, and tourism through car racing. This year's Shanghai F1 Grand Prix attracted 230,000 spectators, with 16% being international visitors. These events may not sell large numbers of cars but can enhance brand loyalty and generate sustained local consumption.

Domestic self-drive travel accounts for 77.4% of tourism transportation methods. Improvements to RV campsites, energy replenishment facilities, tourist routes, and comprehensive service stations will benefit not only RV companies but also parking, charging, maintenance, retail, hotels, and scenic spots.

Cars here are no longer just transportation tools. They have become part of the consumption experience.

Which Companies Are Most Likely to Benefit?

From an industry structure perspective, several types of companies have clear opportunities.

Leading automakers and dealer groups with capabilities in new cars, used cars, maintenance, and customer operations will find it easier to capture revenue from a vehicle's entire lifecycle. New demand will also emerge for new energy inspection and maintenance equipment, battery restoration, insurance pricing, and vehicle data services.

Compliant modification parts, the RV supply chain, car racing, self-drive tourism, parking and charging, and legitimate vehicle dismantling and recycling companies are also expected to receive policy support.

Conversely, dealers relying solely on new car price differentials, businesses depending on closed maintenance systems for high profits, used car dealers operating on information asymmetry, and non-standard modification and illegal dismantling enterprises will face greater pressure.

The Real Changes Will Be Visible in the Next Year

This press conference will not immediately add a significant number to national car sales. Its impact on the market will be slower and more diffuse.

What to watch next are the specific rules that the 40 pilot cities will introduce: how Hangzhou, Guangzhou, and Shenzhen will optimize purchase restrictions and usage environments, how extensive the list of modification projects will be, how new energy maintenance technology authorizations will be implemented, whether used car inspection reports will truly be mutually recognized, and whether RV access and campsite land use can be simplified.

These implementation details will determine whether the policy can ultimately translate into business opportunities.

In the past, China's automotive industry excelled at manufacturing and selling cars. After reaching 370 million vehicles in circulation, the industry must also learn to service and circulate these vehicles effectively while generating sustained profits over their ten-plus years of use. While whole-vehicle sales will remain important in the next year or two, the gaps between companies may increasingly emerge after the point of sale.

References and Images

*Reproduction or excerpting without permission is strictly prohibited.

-

![]()

Can the ‘New Energy Vehicles to the Countryside’ Campaign Revive the Sluggish Auto Market?

-

![]()

The Covert Battle for AI Ride-Hailing Entry Points Among Didi, Qianwen, and Doubao

-

![]()

Momenta Lays Out Its Books: A Strong Report, and a Pricier Story

-

![]()

US New Car Manufacturer Faces Major Crisis: Layoffs Hit 18%, COO Position Eliminated, with Each Vehicle Sold Incurring a Loss of $1.83 Million

-

![]()

Say Goodbye to Wasteful Spending! Innovative Policies to Boost Auto Consumption

-

![]()

With 370 Million Vehicles on the Road, the Auto Industry Reevaluates Its Post-Sale Business Strategy

-

Doubao Learns to Hail Taxis, but Profitability Remains Elusive

-

Fuji Intelligence Clears BSE Listing Hurdle: A Dual-Track Leap for the Precision Manufacturing 'Little Giant' | A-Share Financing Brief