Momenta Lays Out Its Books: A Strong Report, and a Pricier Story

06/24 2026

06/24 2026

475

475

The Valuation Conundrum for Physical AI 'Suppliers'

Original content from Automotive Pixel (ID: autopix)

On June 23, Momenta successfully passed its listing hearing with the Hong Kong Stock Exchange.

Following Pony.ai and WeRide, another player has joined the Hong Kong autonomous driving arena. But Momenta is different. Instead of relying on a fleet of Robotaxis, it has long operated behind the scenes, providing intelligent driving systems to automakers like Mercedes-Benz, Toyota, SAIC, and General Motors.

This time, it has finally laid out its books. After passing the hearing, Momenta’s Prospectus (PHIP) was released for the first time.

Market expectations suggest Momenta could raise $500 million to $1 billion, with a valuation exceeding $9 billion; previously, there were even speculations of a valuation exceeding RMB 100 billion.

In this 430-page document, the two most discussed terms are Robotaxi and Physical AI. But the truly compelling aspect is the financial trend. Momenta, an autonomous driving company, has turned mass-produced intelligent driving into a high-margin software licensing business.

The question lies here: Will the capital markets pay a Physical AI price for an intelligent driving supplier?

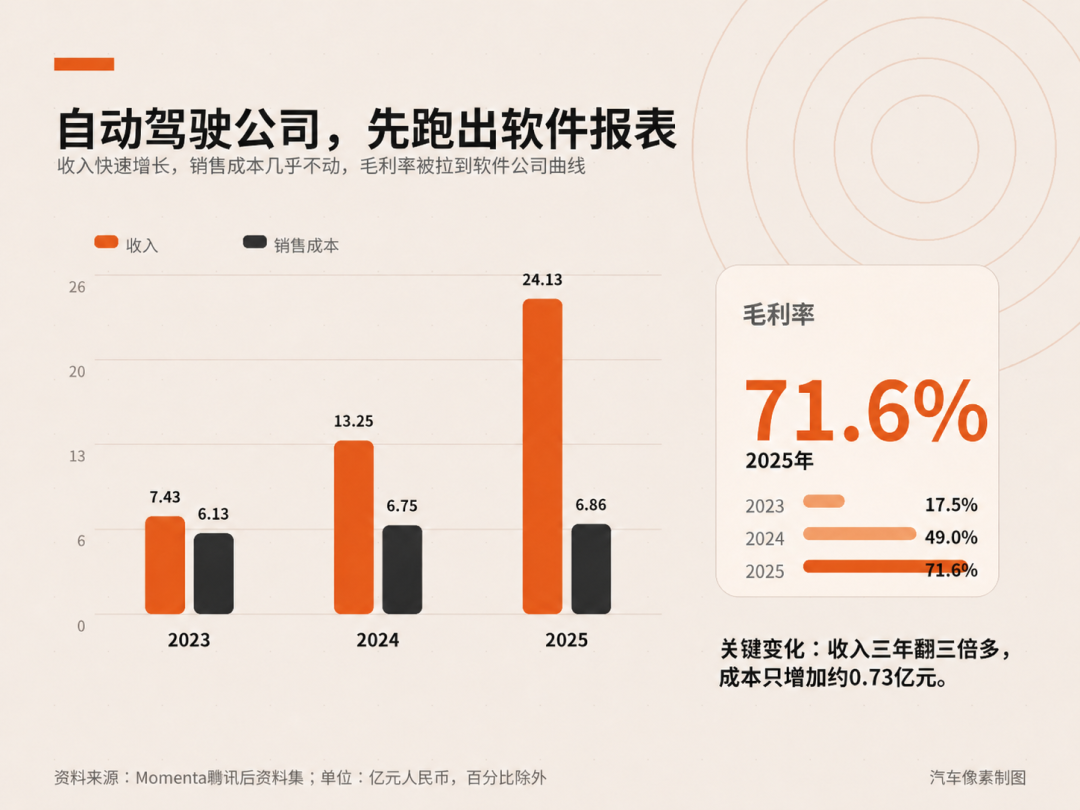

01 Autonomous Driving Company Runs Out a 'Software Report' First

One of the most widespread judgments about Momenta in the market is that intelligent driving suppliers have low gross margins. The usual comparison is Horizon Robotics, which, through integrated hardware-software services, achieved a comprehensive gross margin of 64.5% in 2025.

Momenta’s Prospectus (PHIP) directly overturns this judgment. Momenta’s gross margin rose from 17.5% in 2023 to 49.0% in 2024, and then to 71.6% in 2025, surpassing Horizon Robotics, which also has chip revenue.

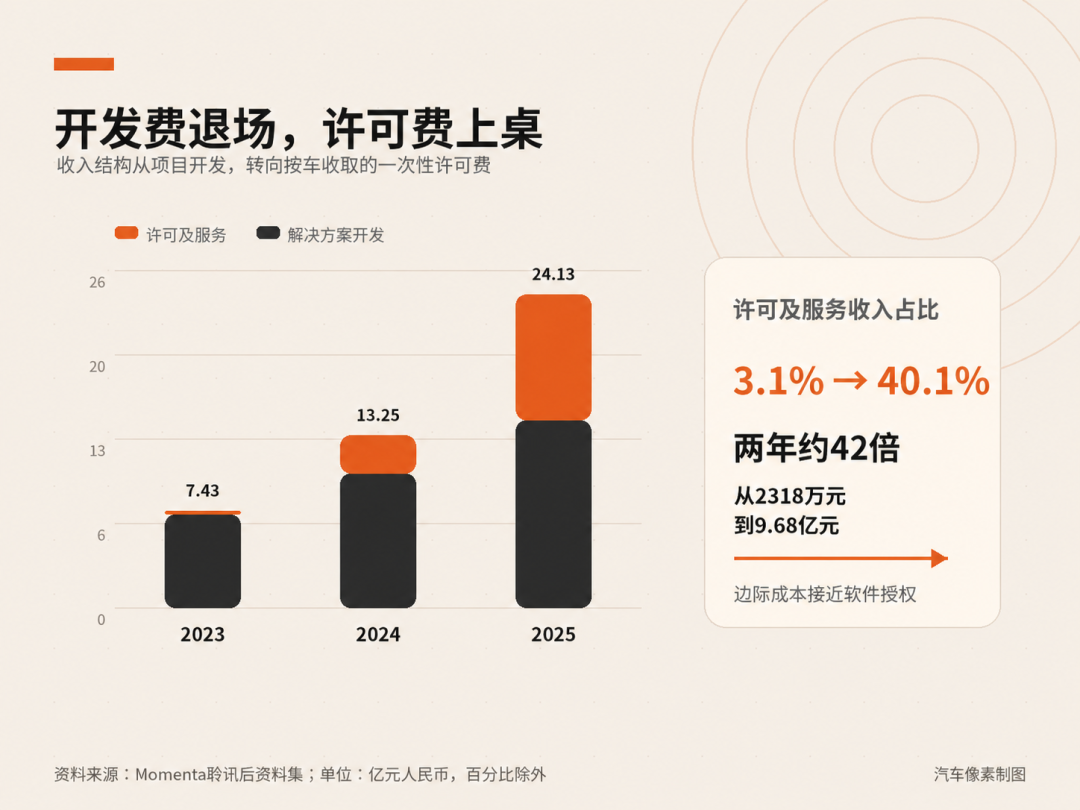

More noteworthy is its growth trajectory. Over three years, Momenta’s revenue surged from RMB 743 million to RMB 2.413 billion, more than tripling; yet its sales costs remained almost flat, at RMB 613 million in 2023 and RMB 686 million in 2025.

Revenue rising while costs stay flat—this is a standard software operating leverage curve.

Supporting this curve is a shift in revenue structure. The prospectus breaks down revenue into two segments: solution development, which accounted for 96.8% in 2023, and licensing and services, which accounted for just 3.1%. By 2025, the latter surged from RMB 23.18 million to RMB 968 million, a roughly 42-fold increase, accounting for 40.1% of revenue.

Licensing fees, charged per vehicle or project, have very low marginal costs, so the higher their proportion, the higher the overall gross margin. This indicates that Momenta is undergoing an identity transformation, shifting from a company earning development fees through project contracts to one earning licensing fees based on installed volume.

The former generates one-time, linear revenue; the latter generates rolling revenue as vehicles operate on the road, with little additional cost. Licensing fees are collected based on the sales volume of equipped models. Each additional vehicle equipped with Momenta’s solution increases revenue with minimal new software costs. It’s not a subscription-based rolling income, but it already possesses the marginal cost advantages of software licensing.

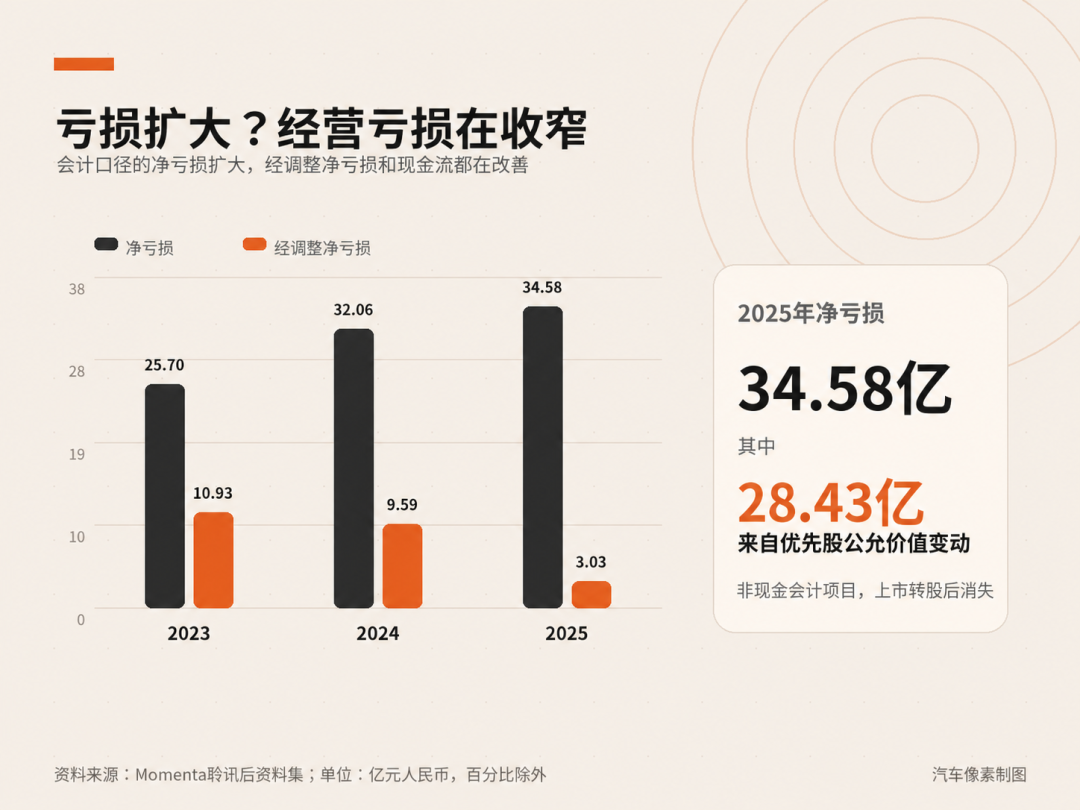

There’s another figure on the profit statement that is easily misinterpreted. Momenta’s net loss in 2025 was RMB 3.458 billion, and it was widening. In 2023, it was RMB 2.570 billion, and in 2024, it was RMB 3.206 billion. This makes it seem like a company still bleeding cash.

But broken down, RMB 2.843 billion of this RMB 3.458 billion loss was due to fair value changes in preferred shares. This is a non-cash accounting item—the higher the company’s valuation, the larger this “loss” becomes, and it will “disappear” at the moment of listing when the shares are converted.

Adding this back along with share-based compensation, Momenta’s adjusted net loss tells a different story. It narrowed from RMB 1.093 billion in 2023 to RMB 959 million in 2024, and then to RMB 303 million in 2025; the corresponding loss rate shrank from -147.2% to -12.6%.

Cash consumption at the operating level is also tightening. Net cash outflow from operating activities fell from RMB 1.069 billion in 2023 to RMB 281 million in 2025. By 2025, Momenta’s gross profit of RMB 1.727 billion almost covered its total R&D spending of RMB 1.869 billion, leaving a gap of just RMB 142 million.

So, on the financial side, the prospectus reveals that in an industry notorious for losses, Momenta has already balanced more than half of its books, producing a software company report close to breaking even. This is what it has truly proven.

The problem is, stability might also be its trouble.

02 Supplier Status Alone Can’t Support Physical AI Valuation

Capital markets won’t pay a high premium for a stable supplier.

At the rumored valuation of RMB 100 billion, or about $14 billion, the price-to-sales ratio based on 2025 revenue of RMB 2.413 billion is roughly 41x; based on gross profit of RMB 1.727 billion, it’s about 58x. Meanwhile, a typical automotive Tier 1 software supplier usually trades at a price-to-sales ratio of 1 to 3x.

The premium the market is paying isn’t for Momenta’s proven intelligent driving licensing business but for what it hasn’t yet proven: Physical AI and the L4 technology behind it. This is why Momenta must elevate itself from an “Intelligent Driving Tier 1” to a “Physical AI Company.”

During the Beijing Auto Show, Cao Xudong stated that world models are responsible for predicting the future states and interactions of the physical world, while reinforcement learning optimizes the model through trial and error in both real and simulated environments. Together, they form the two pillars of Physical AI.

In the prospectus, this narrative is translated into products. The reinforcement learning-based R6 model is already in mass production, equipped in the Buick ZhiJing L7 and Chery Fengyun T11; the next-generation R7 world model is set for mass production in April 2026.

This isn’t just riding the hype. Autonomous driving is indeed the most suitable initial application for Physical AI, as it involves real-world inputs, clear optimization goals, scalable data, and a commercial closed loop (closed loop)—mass-production licensing fees—that can first sustain the company. Treating vehicles as the earliest mass-scalable robots makes logical sense.

But this higher identity as a Physical AI company originally had a more straightforward version: Robotaxi. Momenta didn’t choose it because that story is now hard to tell.

By 2026, the Robotaxi industry has crossed two thresholds. Technologically, Waymo provides roughly 500,000 paid rides per week with a fleet of thousands of vehicles; no one doubts whether autonomous vehicles can operate on roads anymore. Economically, Pony.ai has achieved per-vehicle profitability in Guangzhou and Shenzhen, with Shenzhen’s seventh-generation Robotaxi reaching a peak daily net revenue per vehicle of RMB 394 on March 22, 2026, up from an average of RMB 338 the previous month.

These two developments show that the Robotaxi business model is gradually becoming clear.

The problem is, the leaders are all asset-heavy operators—Waymo, Pony.ai, and WeRide all own and operate their fleets. Meanwhile, Momenta’s commercialization scale in Robotaxi remains small, with revenue not significant during the track record period. It has testing, licensing, and collaboration frameworks but hasn’t formed an operational scoreboard comparable to Waymo, Pony.ai, or WeRide for investors to directly evaluate.

So, one of the most practical uses of “Physical AI” is to shift the battlefield from an abstract height where it lags to another abstract height without a scoreboard yet. At the Physical AI level, Robotaxi is no longer the only answer but just one of the first scenarios where Physical AI lands. What Momenta wants investors to focus on is mass-production installed volume, real-world road data, world models, and data closed loop (closed loops)—not the fleet it doesn’t yet have.

This narrative is effective and necessary. Focusing solely on being an intelligent driving supplier sets a low valuation ceiling; focusing solely on Robotaxi, it can’t compete with those already in operation. However, it needs to be approached with caution because while Physical AI is a valid technological theme, it currently seems more like a valuation veneer.

What Momenta can prove is mainly installing urban NOA in hundreds of thousands of vehicles; what it hasn’t proven is migrating this capability into large-scale L4 autonomous operations; even less so is expanding from vehicles to Robovans, Robotrucks, and broader Physical AI or embodied intelligence.

The 41x price-to-sales ratio is pricing in options for Physical AI and L4 ahead of time.

03 Will the New Story Disrupt the Old Model?

The premise of Momenta’s attractive financial report is its asset-light model.

It has no fleet, no hardware, and no operations. The reason sales costs can be contained and gross margins can reach 71.6% is that it only does one thing—license its autonomous driving software stack to automakers, who then build and sell the vehicles. This is the “Momenta-style supplier” approach: OEMs own the vehicles and users, while Momenta supplies the brain, with clean division of labor.

But if Robotaxi and Physical AI are pursued seriously, can this model still be replicated?

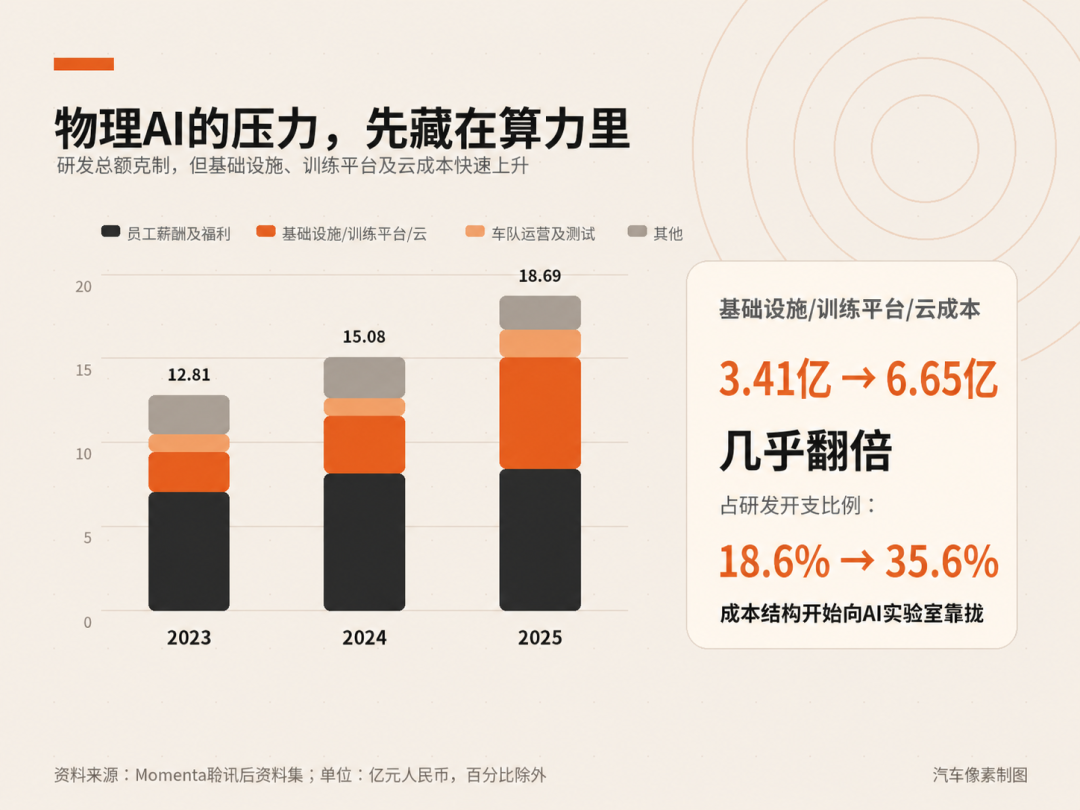

And changes have already begun, hidden in the structure of R&D spending. Momenta’s total R&D spending in 2025 was RMB 1.869 billion, up just 24% year-on-year, appearing quite restrained. But broken down, “infrastructure, training platforms, and cloud costs” surged from RMB 341 million in 2024 to RMB 665 million in 2025, nearly doubling and accounting for 35.6% of R&D spending, up from 18.6%; meanwhile, employee salaries grew by just 3%.

Its cost structure is shifting from a “hire engineers” software supplier to a “buy computing power” AI lab, but as of the prospectus’s release, the investment remains very restrained, maintaining discipline in total R&D spending.

What will truly determine whether financials are rewritten is how Scalable Robo is implemented.

The prospectus points toward an asset-light approach: it plans to have a cumulative L4 fleet of about 5,000 vehicles by the end of 2027, with more than half overseas, achieved through a small self-operated fleet plus larger fleets operated by partners.

If it can maintain this boundary—only supplying the stack, collecting licensing and royalty fees, and letting others handle the fleets—then its core business remains clean. But if Robo operations can’t rely solely on licensing and require Momenta to shoulder fleet responsibilities, it will slide from a software company toward a Robotaxi operator.

This path has already been demonstrated by WeRide. In Q1 2026, its revenue grew by 58% and gross margin reached 34.7%, neither of which is bad in the industry, but its net loss still widened to RMB 389 million.

The longer-term question is whether the “Momenta-style supplier” model can continue to be replicated in the Robotaxi or even Physical AI dimensions.

In the L2 era, the model worked because intelligent driving was just one part of overall vehicle competitiveness, and automakers were willing to let third parties supply the brain. But in Robotaxi, autonomous driving itself is the product and the core of both margins and safety responsibility, making the model’s migration more challenging.

This article is original content from Automotive Pixel (autopix). Unauthorized reproduction is prohibited.

-

![]()

Huawei Follows Suit: Has the Era of Guaranteed Coverage for Intelligent Driving Accidents Arrived?

-

![]()

Over the Past Three Years, Air Conditioner Powder Spraying Has Become a Widespread Issue Among Over a Dozen Automakers and Numerous Models! Is Cost-Cutting the Culprit?

-

![]()

Suzhou Crafts 29-gram AI Glasses

-

![]()

Love and Deep Space: From Setbacks to Success—How Otome Games Sustain a Billion-Dollar Market?

-

![]()

From January to May, 10,823 New Energy Sanitation Vehicles Were Sold, with Yingfeng Environment, Yutong, and Foton Securing the Top Three Positions

-

![]()

Can the ‘New Energy Vehicles to the Countryside’ Campaign Revive the Sluggish Auto Market?

-

![]()

The Covert Battle for AI Ride-Hailing Entry Points Among Didi, Qianwen, and Doubao

-

![]()

Momenta Lays Out Its Books: A Strong Report, and a Pricier Story