Huawei Follows Suit: Has the Era of Guaranteed Coverage for Intelligent Driving Accidents Arrived?

06/24 2026

06/24 2026

455

455

"A New Battle of Responsibility"

Guaranteed coverage policies are becoming a new competitive tool for automakers.

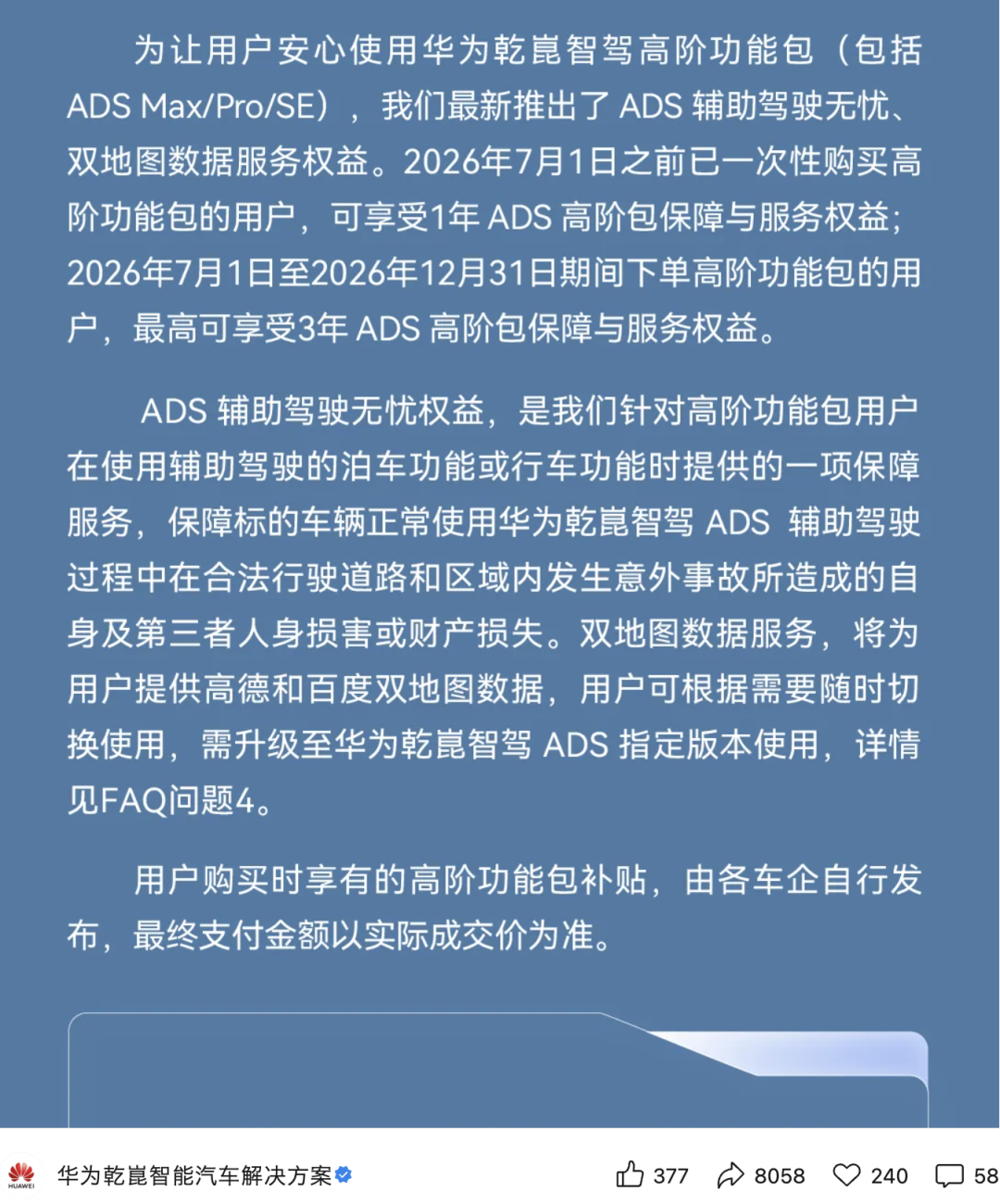

On June 22, Yinwang released the "Huawei Qiankun Intelligent Driving ADS Advanced Function Package Recommended Sales Price and Latest User Rights Announcement," which mentioned that Yinwang has added ADS advanced function package protection and service rights, including ADS assisted driving worry-free service rights.

Notably, as early as 2025, automakers such as Hongmeng Intelligent Driving and Avita had implemented worry-free assisted driving services on select vehicle models. This year, the benefit is being expanded to the entire product lineup of the Huawei Qiankun Intelligent Driving system, including Hongmeng Intelligent Driving's five brands, Huawei Qiankun's two realms, and all models equipped with the ADS assisted driving system, such as Mengshi, Avita, and LanTu.

Bangning Studio called the Hongmeng Intelligent Driving official customer service on the 23rd and was informed that users can choose not to activate auto insurance or to activate it after an accident occurs while using ADS assisted driving. In the former case, losses are covered by the worry-free service provider and will not affect the user's premium for the following year. In the latter case, any amount exceeding the auto insurance coverage is covered by the worry-free service provider, which will affect the user's premium for the following year.

In short, Yinwang has implemented a conditional intelligent driving coverage plan that allows users to choose whether or not to utilize auto insurance.

A month ago, BYD also announced similar measures.

In late May, BYD announced guaranteed coverage for urban navigation safety—new users of the Divine Eye A and Divine Eye B, as well as existing owners who upgrade to Divine Eye 5.0 via OTA, can enjoy one year of guaranteed coverage service rights for urban navigation.

In addition, automakers such as XPENG Motors, Xiaomi Auto, and GAC Group have also introduced various types of intelligent driving protection services.

A new competitive logic in the industry seems to be emerging: Daring to take responsibility for accidents is the ultimate proof of an automaker's technological confidence.

▍01 Which Automakers Are Providing Coverage?

Based on the information released, the current intelligent driving protection plans in the automotive market can be divided into three tiers, with certain differences in compensation limits, premium impacts, usage costs, and underlying models.

The first tier is represented by BYD's full and unrestricted coverage, which is provided free of charge with no compensation limit and does not affect the user's premium for the following year.

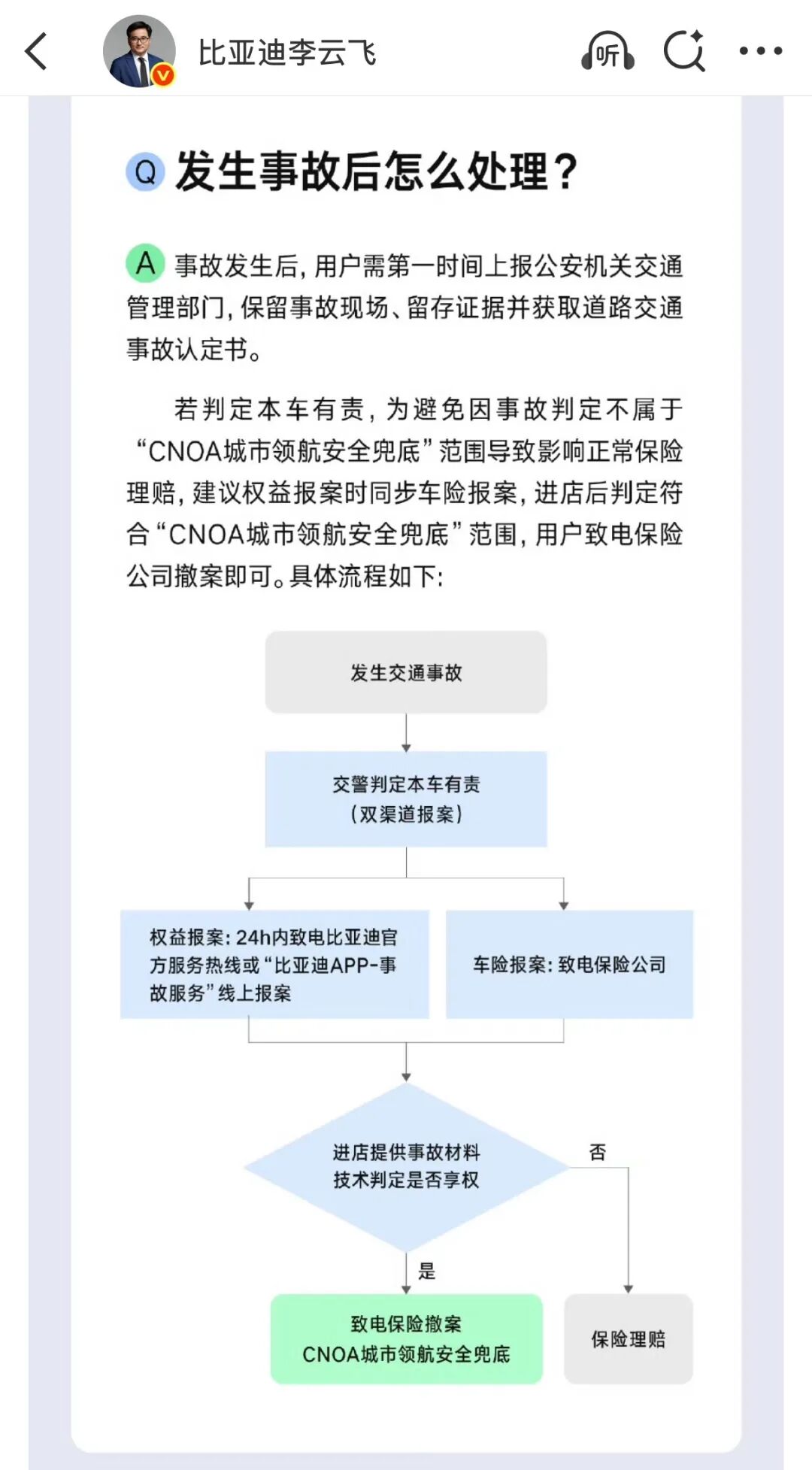

BYD's coverage rights are divided into two categories. The first is intelligent parking coverage, which was implemented in July of last year. If an accident occurs while using the Divine Eye's parking function, the manufacturer fully covers the repair costs without involving insurance.

The second is the urban navigation coverage added in May of this year. As mentioned earlier, in the event of a liable accident while compliance (legally) activating urban NOA, BYD will cover vehicle repairs, third-party property damage, and personal injury losses with no compensation cap.

An industry insider stated that BYD's model has a high threshold, which most brands find difficult to replicate for three reasons:

First, the high-end version equipped with LiDAR comes with an additional charge, with the latest pricing set at 12,000 yuan. Second, BYD has its own property and casualty insurance business. In the first quarter of 2026, BYD's property and casualty insurance recorded a net profit of 92 million yuan, nearly matching the total for 2025. Sufficient profitability can safeguard the risk reserve fund for guaranteed coverage compensation. Third, BYD's millions of intelligent driving vehicles in circulation, vast driving data pool, and extensive offline service network form a complete closed loop of data, capital, and after-sales support.

In contrast, most joint ventures and independent brands lack self-operated insurance to share risks, have insufficient numbers of intelligent driving vehicles in circulation, and have imperfect offline claims networks. They can only choose to collaborate with insurance companies to offer limited intelligent driving insurance.

The second tier is represented by Huawei Yinwang's capped rights. These rights are included with the advanced intelligent driving package and set a compensation limit of 3 to 5 million yuan. Compliant intelligent driving accidents can be processed through exclusive compensation channels, avoiding an increase in personal premiums the following year.

Compared to BYD, Huawei Qiankun's worry-free rights for intelligent driving cover a broader range, including three core functions: highway NCA, urban NCA, and all-scenario intelligent parking, applicable to all models equipped with ADS advanced functions.

The compensation mechanism is designed to balance user needs and insurance rules, with dual reporting channels after an accident. If the incident meets the coverage criteria, the insurance claim can be withdrawn to avoid an increase in the following year's premium. If losses exceed the worry-free rights compensation range, the remaining amount can still be covered by auto insurance.

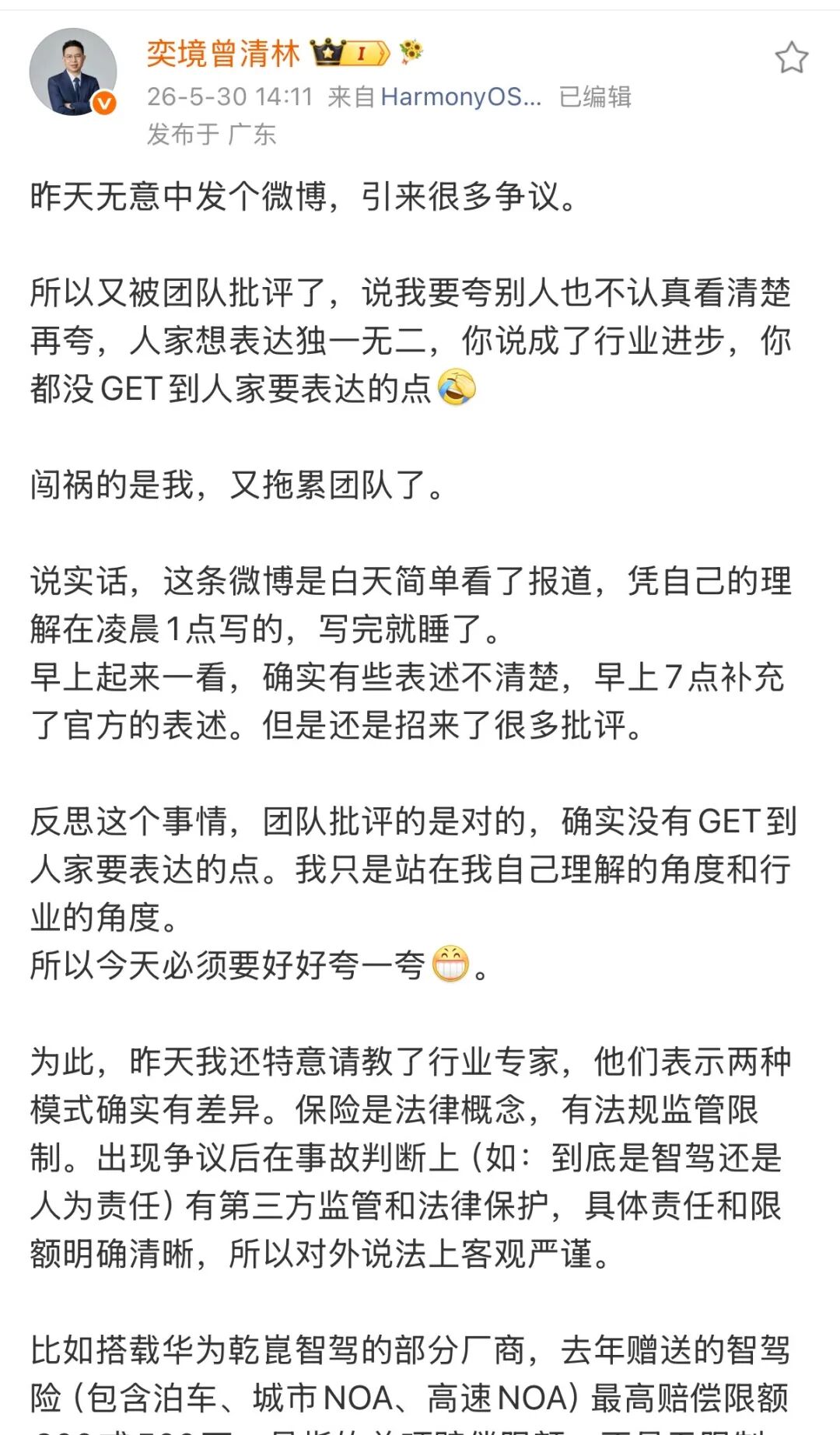

Zeng Qinglin, General Manager of Yijing Auto, stated in a post in late May that some manufacturers equipped with Huawei Qiankun's intelligent driving system offered intelligent driving insurance (covering parking, urban NOA, and highway NOA) with a maximum compensation limit of 3 or 5 million yuan last year, referring to single-item compensation limits, not unlimited coverage.

"This unlimited coverage commitment model from competitors is indeed boundary-pushing, breaking traditional models and unique—kudos," Zeng Qinglin said. He noted that BYD's coverage policy is a corporate self-pay commitment, not constrained by insurance compensation limits, and fundamentally differs from Huawei Qiankun's intelligent driving insurance in legal attributes and compensation caps.

The official customer service of Hongmeng Intelligent Driving stated that the assisted driving worry-free service is third-party insurance jointly offered by Yinwang and insurance companies. However, this insurance is not within the consumer's personal insurance scope and will not affect the owner's premium for the following year.

The third tier consists of intelligent driving protection plans offered by automakers such as XPENG, Xiaomi Auto, GAC Group, and GAC Toyota. These plans generally feature capped compensation amounts, with accident records synchronization (simultaneously) entered into personal auto insurance files, potentially raising premiums the following year. They also have restrictions on coverage scenarios and compensation rules.

For example, GAC Toyota introduced manufacturer "three responsibilities" rights on the Platinum Wisdom 3X (Bozhi 3X), including responsibility for intelligent parking assistance accidents. If an intelligent parking accident occurs during vehicle use, the manufacturer is directly responsible for repairs.

XPENG's Intelligent Driving Assurance Service charges an annual fee, compensating 800 yuan for vehicle damage under 10,000 yuan, 10% of losses for damage exceeding 20,000 yuan, with passenger and third-party compensation caps of 200,000 yuan and 1 million yuan, respectively. All claims records are synchronization (simultaneously) entered into personal auto insurance files, affecting the following year's premiums. The Xiaomi SU7 Ultra operates similarly, requiring accidents to be reported to the insurance company.

It is clear that there is a distinct hierarchy in intelligent driving protection plans. Different policies reflect gaps in automakers' financial reserves and technological accumulation.

▍02 Reshaping the Industry Ecosystem

The prevailing view in the industry is that automakers' rush to introduce guaranteed coverage rights for intelligent driving is not a short-term marketing gimmick but an inevitable trend as competition in the intelligent driving track ( track , " track " here means "field" or "arena") enters its second half. It will significantly increase the importance of intelligent driving in users' vehicle purchase decisions, promote the adoption of advanced assisted driving, force innovations in the auto insurance system, and reshape the industry's development landscape.

For users, coverage policies directly address hesitations, eliminating concerns about using intelligent driving due to fear of accidents and financial losses.

Data from Chezhi.com shows that from 2023 to 2025, a large number of complaints focused on driving assistance system failures, with the core issue being unclear accident liability. Users worry that if an accident occurs while using intelligent driving, they will have to bear high repair costs and increased premiums. Some car owners have stated on social media that due to these concerns, they prefer not to use the intelligent driving functions even if they have purchased them.

PICC Property and Casualty's 2025 claims data shows that the average per-vehicle loss in accidents involving assisted driving that year reached 47,000 yuan, 35% higher than traditional accidents.

Intelligent driving protection is addressing this pain point.

Media reports indicate that BYD's internal staff recently stated that after the coverage policy was announced, weekend store visits in first-tier cities generally increased by 40% to 60% compared to the previous period, with single-store daily foot traffic often exceeding 100. More than 60% of these visitors specifically inquired about the coverage details.

Huawei Qiankun's move to extend the coverage period by three years on June 22 also targets long-term usage concerns, alleviating user worries after the one-year rights expire and promoting the penetration rate of advanced ADS packages.

Data released by Huawei Qiankun shows that as of the end of May, Huawei Qiankun's intelligent driving had accumulated 11.47 billion kilometers of assisted driving and proactively avoided 5.57 million collisions.

From an industry development perspective, coverage policies are forcing automakers to end the inefficient mode of simply stacking hardware while avoiding responsibility, promoting positive iterations in intelligent driving technology.

This competition over responsibility will create a divide in the industry. Automakers lacking technology, capital, and after-sales systems that cannot introduce relevant coverage rights will gradually lose attractiveness in the intelligent driving field and be accelerated out of the race.

The auto insurance industry will also undergo profound changes. Autonomous coverage policies like BYD's are reconstructing the decades-old logic of auto insurance liability. Under the current legal framework, the Supreme People's Court's guiding cases clearly state that the driver remains the legal operator of the vehicle. Traditional compulsory third-party liability insurance and commercial third-party insurance only cover risks associated with human driving, leaving intelligent driving risks due to algorithm or system failures without protection.

In March of this year, Beijing took the lead in piloting exclusive auto insurance for intelligent connected new energy vehicles, but a unified national insurance system for the industry cannot be established in the short term. Automakers' coverage policies exactly (precisely) fill the protection gap during this transitional phase, serving as an important supplement to traditional auto insurance.

In the long run, automakers and insurance companies may move toward a symbiotic model represented by Yinwang—automakers possess comprehensive data on vehicles, algorithms, and driving behavior, giving them an advantage in risk identification. Insurance companies have actuarial, reinsurance, and bulk claims processing capabilities. Combining these strengths could create an integrated service encompassing "vehicle production and sales + exclusive risk protection + after-sales maintenance."

The official customer service of Hongmeng Intelligent Driving also stated that the automaker is the primary party responsible for determining intelligent driving accidents. Specifically, staff at user centers determine whether an accident falls within the scope of assisted driving worry-free coverage, without requiring secondary determination by the insurance company. The determination result is directly communicated to the insurance company, which then executes the compensation measures.

Of course, these intelligent driving protection services all face unavoidable structural contradictions. For example, automakers act as both referees and compensators, meaning whether an accident meets compensation standards is determined solely by the automaker's internal technical department, without the involvement of a neutral third party.

From a long-term regulatory perspective, for the industry to truly unlock the market potential of advanced assisted driving, collaboration among regulators, insurance companies, and automakers is still needed to establish a standardized, neutrally judged intelligent driving risk protection system. This would ensure that liability divisions for intelligent travel are evidence-based and that compensation processes are transparent and fair.

-

Why is CATL Partnering with Octopus Energy to Build a Battery-Swapping Network for Heavy-Duty Trucks in the UK?

-

![]()

Research on New Trends and User Value in China's Public Charging Consumption Market

-

【Insight】NPO (Near Package Optics) as a Transitional Solution for CPO, Industry Development Embraces Opportunities

-

![]()

Charging Industry Shifts from Quantity to User Experience as New Benchmark

-

![]()

Qianli Technology Aims for Autonomy from Geely's Sphere: Why Does BAIC Initiate the Alliance First?

-

![]()

Three Major New Policies Come into Force on the Same Day, Revolutionizing the Growth Dynamics of China's Auto Market

-

![]()

The Complete Blueprint of Tsinghua-Affiliated Embodied AI 'Startup Dream Team': 7 Companies, 25 Billion in Funding, and the Dawn of an Era

-

![]()

The Ministry of Industry and Information Technology Forces Auto Companies to 'Self-Examine and Rectify,' Banning Unsafe Old Electric Vehicles from the Roads