Three Major Pressures Weigh Heavily on Japanese Automakers

06/25 2026

06/25 2026

499

499

Introduction

Introduction

The US policy shift, geopolitical conflicts in the Middle East, and the breakthrough of Chinese automakers have formed three major pressures that are stifling the growth of Japanese automakers.

Recently, traditional automotive giants in Europe and the US have been rumored to be considering a return to their roots by venturing into arms manufacturing. Whether true or not, these rumors are not unfounded. Given their idle production capacities and past experience in arms manufacturing, for many established automakers, transitioning from car manufacturing to arms production would simply involve modifying production lines and facilities—not a difficult task.

This also reveals, from another perspective, the scars left by traditional automotive giants as they transition into the electric era. Declining sales, shrinking market share, halved profits, idle production capacities, and a global decline in brand influence.

This is true for European and American automakers, and it is equally true for Japanese automakers. Given the current global development status of Japanese automobiles, it can even be said that Japanese automakers, who have long been at the forefront of global automotive manufacturing, are now facing a multi-faceted downturn.

As a cornerstone of Japan's manufacturing industry, and possibly its last remaining pillar, the automotive industry's rise and fall directly impacts Japan's economic lifeblood. However, data from the 2025 fiscal year shows a clear downturn for Japanese automakers. Currently, Japan's seven major automakers are collectively experiencing a sharp decline in profits and sales. The total net profit for the 2026 fiscal year is expected to be halved compared to the historical peak in the 2023 fiscal year.

Data shows that Toyota's sales in 2025 increased by 5.5% year-on-year, achieving a slight increase in sales against the trend, but revenue rose without a corresponding increase in profit, with net profit falling by 19.2% and operating profit plummeting by 21.5%. Honda recorded its first annual operating loss in nearly 70 years since its listing in 1957, with a net loss of 414.3 billion yen in the 2025 fiscal year. Nissan suffered consecutive years of heavy losses, with cumulative losses exceeding 1.2 trillion yen over two years.

Second-tier Japanese automakers have not been spared either. Mazda's net profit in 2025 plummeted by 69% to 35.1 billion yen, Subaru's net profit fell by 73% to 90.8 billion yen, and Mitsubishi Motors' net profit dropped by 76% to 10 billion yen.

As Japanese automakers simultaneously experience declining performance, their global sales dominance is also shrinking. In 2025, global sales of Chinese brands exceeded 27 million vehicles, surpassing Japanese brands' 25 million vehicles for the first time, ending Japan's 25-year streak as the global sales leader since 2000.

By 2026, the situation had not significantly improved. Especially against the backdrop of policy shifts in the US market, the impact of Middle East conflicts, and the accelerated electrification of the Chinese market, Japanese automakers are facing severe challenges.

01 In the US: Policy Shifts Undermine North American Foundations

It is well known that the North American market has long been a core market for Japanese automakers and a major source of their profits. For example, the US market contributes nearly 30% of Toyota's global sales and 40% of its operating profit, while supporting over half of Honda's profits. It is the cornerstone of Japanese automakers' global layout .

However, policy shifts are now shaking the North American system that Japanese automakers have been cultivating for decades, becoming a key external factor in their performance collapse.

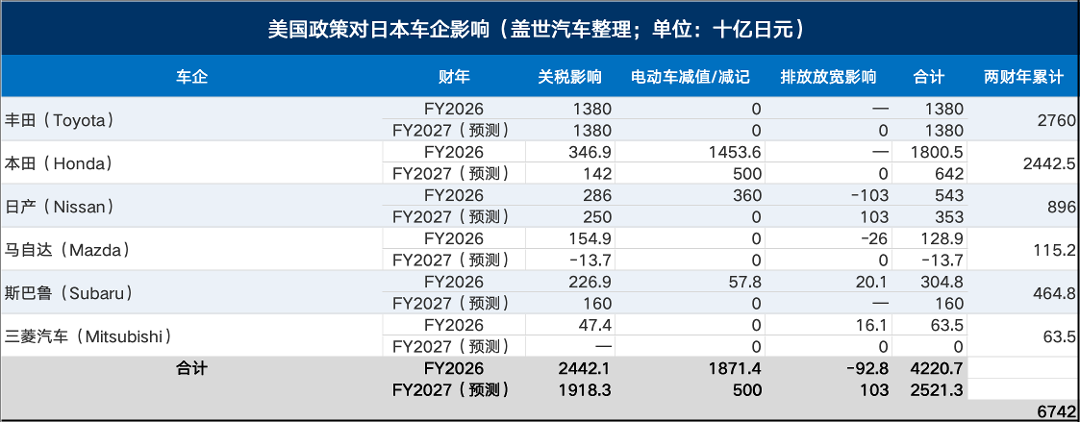

According to financial analysis data from Automotive News, three major adjustments in the US—tariff increases, the cancellation of electric vehicle tax credits, and the relaxation of emissions regulations—have resulted in cumulative losses of approximately $28 billion for Japanese automakers, with the scale of losses continuing to expand. Industry projections suggest that by March 2027, the cumulative costs of these policies will exceed $40 billion.

Among these, the impact of tariffs is the most direct. In 2024, the US imposed a 12.5% tariff on Japanese-made automobiles and implemented comprehensive tariff controls on Mexico and Canada, key production bases for Japanese automakers in North America, disrupting their coordinated production model across the three regions.

Data shows that in the 2025 fiscal year, six major Japanese automakers, including Toyota, Honda, Nissan, and Mazda, faced tariff costs as high as 2.44 trillion yen (approximately $15.23 billion), with an estimated additional tariff expenditure of 1.92 trillion yen (approximately $11.98 billion) in the 2026 fiscal year.

The more profitable leading automakers have suffered the most severe damage. Toyota expects tariffs to result in losses of 2.76 trillion yen (approximately $17.22 billion) over the two fiscal years from 2025 to 2027, directly dragging its North American operations into the red and causing its group operating profit to decline for three consecutive years. Honda's negative tariff impact reached 346.9 billion yen, while Nissan's annual operating profit was only 58 billion yen, with tariffs directly devour ing 286 billion yen in profits, nearly wiping out all its earnings.

The Nomura Research Institute estimates that a 25% US car tariff would directly cause Japan's GDP to decline by 0.2%, almost offsetting Japan's 0.1% economic growth in 2024, elevating the impact on the automotive industry to the national economic level.

If tariffs represent the most direct impact, the reversal of electric vehicle policies has caused even more profound harm. The US cancellation of tax credits of up to $7,500 for new electric vehicles and $4,000 for used electric vehicles has cooled domestic demand for electric vehicles. Japanese automakers' previously formulated electrification plans have become ineffective, forcing many companies to halt or delay electric vehicle projects and incur significant impairment losses.

Honda suffered the most severe damage, canceling three self-developed electric vehicle models in North America and recording $9.05 billion in impairment losses, becoming a core factor in its annual heavy losses. Subaru delayed the launch of its self-developed electric vehicle, with impairment losses reducing its annual operating profit by $361 million. Nissan adjusted production directions at its US factories, shifting electric vehicle capacity to pickup trucks and including it in a hundred-billion-yen impairment project.

The relaxation of emissions regulations has created a double squeeze, exacerbating industry differentiation and losses. The US cancellation of greenhouse gas emissions controls and fuel economy penalties has rendered the early compliance investments, reserved funds, and emissions credit purchases of automakers futile.

Subaru and Mitsubishi incurred $125 million and $101 million in emissions-related impairment losses, respectively. While Nissan and Mazda saw slight revenue increases due to the reversal of reserved funds, they were unable to offset overall industry losses. The erratic nature of multiple policies has left Japanese automakers short on short-term responses and ineffective in long-term layout , causing their North American foundations to continue loosening.

02 In the Middle East: Geopolitical Conflicts Undermine High-Margin Markets

The Middle Eastern market is a crucial high-margin overseas market for Japanese automakers, consistently absorbing around 14% of Japan's automobile exports. Models like the Land Cruiser, Prado, and Patrol, known for their high premiums and strong sales, have become significant profit sources for automakers.

However, ongoing conflicts have paralyzed shipping in the Strait of Hormuz, damaging the supply chain and export system for Japanese automakers in the Middle East and becoming another factor driving down their performance.

The shipping crisis triggered by geopolitical conflicts has directly caused a cliff-like decline in Japanese automakers' exports to the Middle East.

After the conflict erupted, Japan's automobile exports to the Middle East plummeted by over 90% year-on-year in April. Toyota, which has consistently maintained annual exports of over 500,000 vehicles to the Middle East, with a high proportion of high-margin off-road models, saw its core profit-generating models restricted due to shipping disruptions. As a result, Toyota's operating profit for the first three months of 2026 was only 569.4 billion yen, nearly halving year-on-year and reaching its lowest level in three years.

After all, Japanese automakers, who built their success on lean production models, are highly dependent on a stable global supply chain. As a global energy hub, conflicts in the Middle East not only disrupt shipping but also drive up international oil prices and logistics costs, rendering the production advantages of zero inventory and fast turnover for Japanese automakers ineffective. Multiple automakers' factories have experienced delays in the arrival of critical components and soaring costs, disrupting production rhythms.

To alleviate inventory backlogs in the Middle East and offset performance losses, Japanese automakers have been forced to urgently adjust their global production and sales layout . Nissan redirected 1,400 Patrol units originally destined for the Middle East to the US, mitigating losses through regional reallocation. However, this move further intensified competition in the North American market, squeezing profit margins for existing models and creating a dual dilemma of losses in the East and pressure in the West.

Unlike the suppression from US policies, the Middle East crisis represents a sudden, devastating short-term blow that directly shatters the previous global profit logic of Japanese automakers, causing them to completely lose their high-margin incremental markets.

03 In China: Rise of Local Automakers, Loss of Existing Market Share

As the world's largest automotive consumer market, China was once the largest source of incremental growth for Japanese automakers. However, in just five years, with the outbreak of China's new energy vehicle industry and the rise of domestic brands, Japanese automakers' market share in China has continuously declined. Combined with internal issues such as lagging transformation and rigid decision-making, they are losing their voice in the Chinese market.

Six years ago, in 2020, the total sales of five core Japanese automakers in China were 5.3207 million units, with a market share as high as 26.8%. By 2025, this had fallen to around 13.9%, nearly halving in five years. In comparison, in 2025, the combined sales of Toyota, Honda, and Nissan in China were approximately 3.08 million units, less than BYD's annual sales of 3.8 million units for a single brand.

At the same time, shrinking sales have triggered a collapse in the pricing system. In April 2026, Honda's monthly sales in China plummeted by 48.3% year-on-year, while Nissan's main models saw significant price reductions to clear inventory. Japanese automakers in China are now trapped in a dilemma of trading price reductions for volume. Toyota achieved a new global sales high in 2025, but it relied on significant price reductions, directly causing its net profit to decrease by 940 billion yen year-on-year.

The decline in sales and performance explosions are not without reason.

First and foremost is the severe lag in electrification transformation. Japanese automakers have long bet on hybrid and hydrogen energy, missing the window for pure electric vehicle development. The penetration rate of pure electric vehicles in Japan is less than 2%, far below China's over 60%. Domestic pure electric vehicles in China iterate rapidly, offer excellent driving experiences, and are highly cost-effective, leaving Japanese pure electric models without a clear competitive edge.

This is followed by the issue of intelligentization. In the era of software-defined vehicles, Japanese cars' intelligent driving systems mostly remain at the L2+ level, with outdated intelligent cockpit configurations that cannot meet the high-level intelligent driving assistance and ecological connectivity demands of domestic consumers. Even with increased investments in intelligentization and collaborations with Chinese companies, they have missed the first-mover advantage.

Additionally, there is the issue of rigid decision-making mechanisms. Research and development and product definition rights are highly concentrated at Japanese headquarters, resulting in long model iteration cycles and insufficient sincerity in "oil-to-electric" conversion products, severely detaching them from Chinese market demands.

Facing market collapse, Japanese automakers have begun a journey of self-rescue.

On the production capacity front, Nissan closed its Changzhou factory and initiated global layoffs. Honda cut up to 40% of its fuel vehicle production capacity in China and shut down some factories. Mitsubishi completely withdrew from production in China. Strategically, they are accelerating localization transformations. Toyota and Nissan have delegated some research and development permissions and partnered with Chinese tech companies like Huawei to address intelligentization shortcomings. Honda is implementing aggressive reforms, planning to launch China-exclusive models by 2027.

In other words, Japanese automakers' overall market strategy in China has shifted from comprehensive layout to focusing on niche markets like high-end hybrids, voluntarily abandoning the existing market for low-end fuel vehicles. However, the industry consensus is that if competitive intelligent pure electric products cannot be launched by 2027, the living space for Japanese automakers in China will continue to shrink.

Editor-in-Chief: Du Yuxin Editor: He Zhengrong

THE END

-

![]()

Can Computers, Despite Daily Price Hikes, Still Be a Viable Purchase?

-

![]()

January-June Auto Stocks' 'Resilience Ranking': Geely Alone Posts Gains, Six Plummet Over 40%, One Tumbles 54.5% | Mirror Pro

-

![]()

China’s Public Charging Market: Didi Charging, Teld, and Yunkuai Take the Lead

-

![]()

The First Year of AI-Native Mid-Year Shopping Festival: Technology Reconstructs Human-Product Matching for 618

-

![]()

Micron has released its financial report, showing revenues of $41.5 billion, a 74% increase quarter-over-quarter, with a gross margin of 84.6%. The company provided both short-term and long-term guida

-

![]()

Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket

-

![]()

Doubao Goes 'Professional', Volcano Rolls the Snowball

-

AI: No Sign of a Bubble!