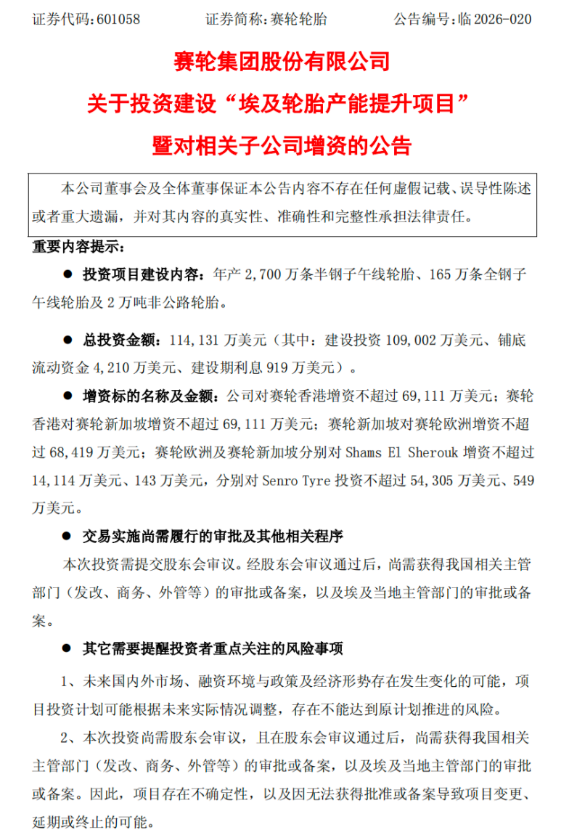

Splashing Out 7.8 Billion to Boost Production Capacity in Egypt, Sailun Tire Faces Dual Pressures of Profitability and Capital in Global Expansion

06/25 2026

06/25 2026

551

551

Recently, Sailun Tire (601058.SH) unveiled a massive overseas investment announcement, fully displaying its global ambitions. The company plans to invest USD 1.141 billion (approximately RMB 7.8 billion) in a project to enhance tire production capacity in Egypt, aiming for an enormous output of 27 million semi-steel radial tires, 1.65 million all-steel radial tires, and 20,000 tons of off-road tires annually. Securities Star noted that this marks Sailun Tire's third major investment in Egypt within the past 12 months, bringing its cumulative investment in Egypt to over USD 1.7 billion.

However, on the flip side of rapid capacity expansion, the company is experiencing "increased revenue without increased profits" in overseas markets. As aggressive global expansion encounters multiple challenges, including declining profitability, intensifying trade barriers, and slowing growth in global tire market demand, whether Sailun Tire's "high-stakes gamble" can deliver on its blueprint of annual revenue of USD 1.161 billion and net profit of USD 170 million as scheduled has become a focal point of market attention.

01. Further Boosting Production Capacity in Egypt, with Cumulative Investments Exceeding USD 1.7 Billion

Sailun Tire recently officially disclosed a tire capacity expansion plan located in Egypt, with a total project investment of USD 1.141 billion. According to the plan, the project will result in new annual production capacities of 27 million semi-steel radial tires, 1.65 million all-steel radial tires, and 20,000 tons of off-road tires.

To achieve efficient progress and resource synergy, Sailun Tire has arranged for two of its overseas wholly-owned subsidiaries to collaborate on a regional basis. Specifically, the established Shams El Sherouk will be responsible for constructing a facility with an annual production capacity of 9 million semi-steel tires, with an investment of USD 227 million and a construction period of 15 months. Meanwhile, the newly established Senro Tyre will undertake the construction of the remaining capacity, including 18 million semi-steel tires, 1.65 million all-steel tires, and 20,000 tons of off-road tires, with an investment of USD 914 million and a construction period of 24 months.

Securities Star noted that this marks the company's third major investment in Egypt within the past year. Looking back, in August 2025, the company first announced its entry into the Egyptian market with an investment of USD 291 million, planning to construct a facility with an annual production capacity of 3.6 million radial tires (including 3 million semi-steel tires and 600,000 all-steel tires). By April of this year, Sailun Tire added another USD 285 million in investment for an expansion project to produce 7.05 million radial tires annually. Coupled with this new investment of USD 1.141 billion, the cumulative investment over the three times has exceeded USD 1.7 billion. Once all projects are completed and reach full production, the Egyptian base will form a complete production capacity matrix with an annual output of 36 million semi-steel radial tires, 3.3 million all-steel radial tires, and 20,000 tons of off-road tires.

From a financial perspective, upon full project completion, it is expected to generate an average annual increase in revenue of USD 1.161 billion and an average annual net profit of approximately USD 170 million, with an investment payback period of about 5.67 years and a project return rate close to 15%. The book figures appear quite impressive.

However, the project still requires approval from the company's shareholders' meeting and must obtain approvals or filings from the relevant competent authorities in both China and Egypt. Uncertainties at the procedural level remain the primary variable at this stage. Additionally, fluctuations in the local political and economic environment in Egypt, uncertainties in raw material price trends, exchange rate changes, downstream market demand, and the actual operating efficiency after project commencement are also realistic risk factors affecting the project's performance.

02. Declining Overseas Gross Profit Margins, Intensive Investments Strain Cash Flow

Market analysis generally believes that the core motivation for Sailun Tire to accelerate its overseas capacity layout lies in the realistic pressure brought about by the continuously deteriorating international trade environment. In recent years, European and American markets have frequently initiated anti-dumping and countervailing investigations against Chinese tire products, with tariff barriers increasing layer by layer. This external pressure has forced domestic tire companies to shift their production capacity outward to circumvent trade barriers and maintain their overseas market shares. Sailun Tire's recent dense [jǐn mì] (Note: ' dense ' means 'intensive' or 'frequent') overseas expansions are a typical example of this industry-wide relocation trend.

Reviewing its overseas expansion trajectory, Sailun Tire's global layout has undergone an evolutionary process from steady to rapid, and from point to area. Between 2012 and 2020, the company took the lead in establishing its first overseas production base in Vietnam. Subsequently, from 2021 to 2023, it added a base in Cambodia, initially extending its overseas production capacity footprint. Entering 2024 to 2025, the pace of expansion significantly accelerated, with bases in Mexico and Indonesia commencing operations within just two years. With the gradual implementation of production capacity from this Egyptian project, Sailun Tire will ultimately form a global production capacity matrix covering six production bases in China, Vietnam, Cambodia, Mexico, Indonesia, and Egypt, spanning Asia, North America, and Africa, and ranking among the top in terms of layout breadth within the industry.

However, in stark contrast to the rapid expansion of its overseas footprint, operational pressures have gradually emerged on the domestic financial statements. According to the 2025 annual report data, Sailun Tire's annual revenue reached RMB 36.792 billion, a year-on-year increase of 15.69%, hitting a historical high. Among this, overseas main business revenue reached RMB 28.226 billion, a year-on-year increase of 18.54%. From the revenue perspective, the pulling effect of the global layout is significant.

However, the performance on the profit side has been less than satisfactory. The company's net profit attributable to shareholders declined by 13.30% year-on-year to RMB 3.522 billion, with the net profit attributable to shareholders after deducting non-recurring items also decreasing by 13.40% year-on-year. The annual gross profit margin dropped to 24.63%, a decrease of 3.08 percentage points from the previous year, with the gross profit margin of overseas business narrowing from 29.88% to 25.75%, a decline of more than 4 percentage points.

Market analysis attributes this situation of "increased revenue without increased profits" to the superposition [dié jiā] (Note: ' superposition ' means 'superimposition' or 'accumulation') of multiple factors. Firstly, the 232 tariffs imposed by the United States starting from April 2025 directly impacted export profits. Secondly, the one after another [lù xù] (Note: ' one after another ' means 'successively' or 'one after another') commissioning of new factories in Indonesia and Mexico led to a significant increase in depreciation, amortization, and preliminary operating expenses, significantly compressing profit margins in the short term. The company also admitted that the factories in Mexico and Indonesia are currently still in the capacity ramp-up stage and have not yet achieved break-even.

Data also confirms this trend: In 2025, the company's combined sales, administrative, research and development, and financial expenses reached RMB 4.690 billion, a year-on-year increase of nearly 20%, with sales expenses alone increasing by 25.34%.

Meanwhile, intensive capacity construction has also brought significant pressure on the company's cash flow and asset-liability structure. Throughout 2025, the company's net cash flow from investing activities was -RMB 5.334 billion, a year-on-year increase of 33.44%, primarily due to the acquisition of long-term assets and equity acquisitions. The balance of construction in progress reached RMB 2.915 billion, a year-on-year increase of 39.34%, intuitively reflecting that the construction of new factories is in full swing.

On the liability side, the company's short-term borrowings reached RMB 5.957 billion, with non-current liabilities due within one year amounting to RMB 1.554 billion, totaling a staggering RMB 7.511 billion. However, the company's existing monetary funds are only RMB 4.579 billion, revealing a short-term debt repayment gap. Although the net cash flow from operating activities increased by 82.58% year-on-year to RMB 4.179 billion, given the enormous funding requirements for the simultaneous advancement of multiple overseas bases, the feasibility of future financing arrangements and the controllability of debt repayment pressure warrant examination.

From the market demand perspective, the overall prosperity of the global tire industry is currently not ideal. Demand for original equipment tires has declined year-on-year, while the replacement tire market can only maintain basic stability. Market demand growth in China has slowed down, with original equipment tire demand in European and North American markets also on a downward trajectory. Against this backdrop, whether the global demand can effectively absorb the massive new production capacity after the Egyptian project commences operation, and whether the company can repair its profitability while continuing to scale up, are both critical unresolved issues.

Perhaps Exactly [zhèng shì] (Note: ' Exactly ' means 'precisely' or 'exactly') due to these uncertain expectations, the company's stock price performance has been under sustain [chí xù] (Note: ' sustain ' means 'continuous' or 'sustained') pressure this year. As of the close on June 24, Sailun Tire closed at RMB 11.54, with a cumulative year-to-date decline of 27.88%. (This article was first published by Securities Star, Author | Xia Fenglin)

- End -

-

![]()

Can Computers, Despite Daily Price Hikes, Still Be a Viable Purchase?

-

![]()

January-June Auto Stocks' 'Resilience Ranking': Geely Alone Posts Gains, Six Plummet Over 40%, One Tumbles 54.5% | Mirror Pro

-

![]()

China’s Public Charging Market: Didi Charging, Teld, and Yunkuai Take the Lead

-

![]()

The First Year of AI-Native Mid-Year Shopping Festival: Technology Reconstructs Human-Product Matching for 618

-

![]()

Micron has released its financial report, showing revenues of $41.5 billion, a 74% increase quarter-over-quarter, with a gross margin of 84.6%. The company provided both short-term and long-term guida

-

![]()

Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket

-

![]()

Doubao Goes 'Professional', Volcano Rolls the Snowball

-

AI: No Sign of a Bubble!