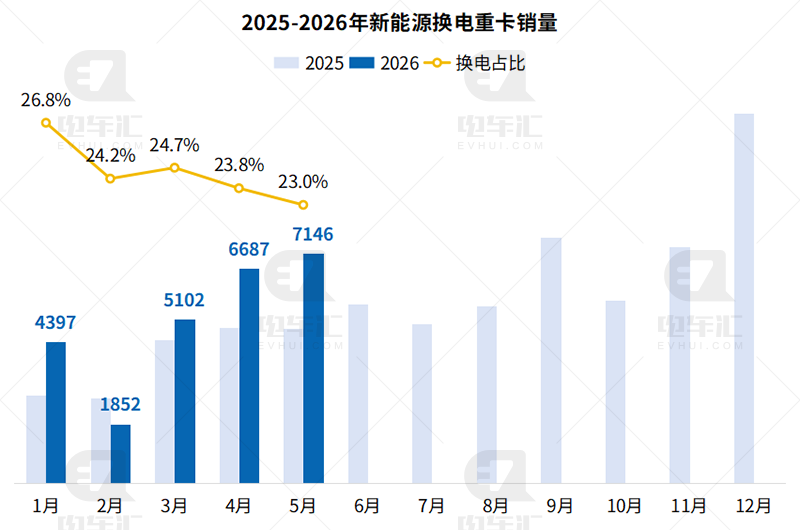

From January to May, New Energy Battery-Swap Heavy Truck Sales Surge 29% Year-on-Year, with Geely, XCMG, and Foton Daimler Leading the Pack

06/25 2026

06/25 2026

442

442

The statistical data presented here is derived from actual terminal sales figures, excluding any export sales.

Analyzing the sales trend of new energy battery-swap heavy trucks from 2025 to 2026, we observe a notable uptick. According to terminal sales statistics compiled by Dianchehui, from January to May 2026, sales of these vehicles climbed steadily month by month, culminating in a cumulative total of 25,184 units, marking a 29% increase year-on-year. However, the overall growth rate trailed behind that of new energy heavy trucks as a whole, which saw a gradual decline from 27% at the start of the year to 23% currently.

In terms of corporate performance, the top 10 groups in sales of new energy battery-swap heavy trucks from January to May 2026 were led by Geely, which sold 5,481 units, a significant 146% increase compared to the 2,230 units sold in the same period in 2025. This positions Geely as the fastest-growing leading enterprise in this sector.

Among the other automotive companies, XCMG and Foton Daimler maintained steady growth, with sales reaching 5,164 and 4,151 units, respectively, representing year-on-year increases of 38% and 40%. FAW secured the fourth position with 2,849 units sold, a 26% increase over the previous year. In contrast, Sinotruk, Shaanqi, Dongfeng, and Sany experienced varying degrees of decline, with Sany seeing a notable 26% decrease year-on-year.

A standout performer was Deepway, manufactured by Rayttle, which achieved a remarkable breakthrough from zero sales to 834 units. Additionally, JAC Anhui Jianghuai Truck, with a staggering 405% year-on-year increase, entered the top 10, showcasing the strong explosive potential of emerging forces in the market.

When examining vehicle model sales, battery-swap pure electric tractor trucks emerged as highly favored, with sales reaching 22,092 units, a 34% increase year-on-year. These models accounted for nearly 90% of total sales, firmly establishing themselves as the dominant choice for mainline logistics scenarios.

Vehicle models tailored for segmented scenarios also performed outstandingly. Battery-swap pure electric concrete mixer trucks sold 954 units, a surge of 172% year-on-year, indicating a growing demand in engineering scenarios. Battery-swap pure electric wing-opening van trucks and detachable garbage trucks achieved ultra-high growth rates of 1,660% and 294%, respectively, accelerating their penetration into segmented scenarios such as urban distribution and sanitation. In contrast, models like dump trucks and methanol range-extended plug-in hybrid tractor trucks experienced declines.

In terms of city-wise sales, Guangzhou rose to the top with 1,012 units sold, a 66% increase year-on-year. However, traditional core cities like Shenzhen and Shanghai witnessed significant declines in sales (Shenzhen down 55%, Shanghai down 71%). Xi'an and Tangshan performed remarkably, with year-on-year increases of 86% and 79%, respectively. Yichun saw a staggering increase from 38 to 444 units, a 1,068% rise year-on-year. Hangzhou grew from 97 to 440 units, a 354% increase, achieving explosive growth and emerging as a new market growth point. Northern cities like Shijiazhuang and Tianjin maintained steady growth, further expanding the regional coverage of battery-swap heavy trucks.

In the short term, with the recovery of logistics demand post-holidays and the advancement of infrastructure projects, sales of battery-swap heavy trucks are expected to continue their upward trajectory. If the current growth momentum is sustained, annual sales are poised to reach a new historical high. In the long term, the industry will confront challenges such as the insufficient density of battery-swap station networks and divergence in battery-swap technology routes. Ultimately, the companies that can forge core advantages in scenario customization, cost control, and cross-regional operations will gain the upper hand in the second half of the battery-swap heavy truck market.

-

![]()

Can Computers, Despite Daily Price Hikes, Still Be a Viable Purchase?

-

![]()

January-June Auto Stocks' 'Resilience Ranking': Geely Alone Posts Gains, Six Plummet Over 40%, One Tumbles 54.5% | Mirror Pro

-

![]()

China’s Public Charging Market: Didi Charging, Teld, and Yunkuai Take the Lead

-

![]()

The First Year of AI-Native Mid-Year Shopping Festival: Technology Reconstructs Human-Product Matching for 618

-

![]()

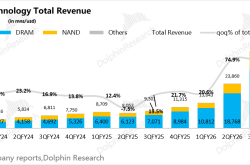

Micron has released its financial report, showing revenues of $41.5 billion, a 74% increase quarter-over-quarter, with a gross margin of 84.6%. The company provided both short-term and long-term guida

-

![]()

Expert Interpretation of New Policy Combination: Activating the Trillion-Dollar Automotive Aftermarket

-

![]()

Doubao Goes 'Professional', Volcano Rolls the Snowball

-

AI: No Sign of a Bubble!