Users Vote with Their Feet, Propelling Didi Charging to Industry Leadership

06/26 2026

06/26 2026

506

506

In the nascent stages of many industries, particularly when supply falls short of demand, there is a tendency to prioritize scale above all else. The primary concern often revolves around whether a service or product “exists” at all.

The public charging sector is no different in this regard.

However, establishing a public charging network involves more than just setting up charging stations across cities. There is a vast difference between merely placing a charging station on the map and ensuring it is actively utilized by users.

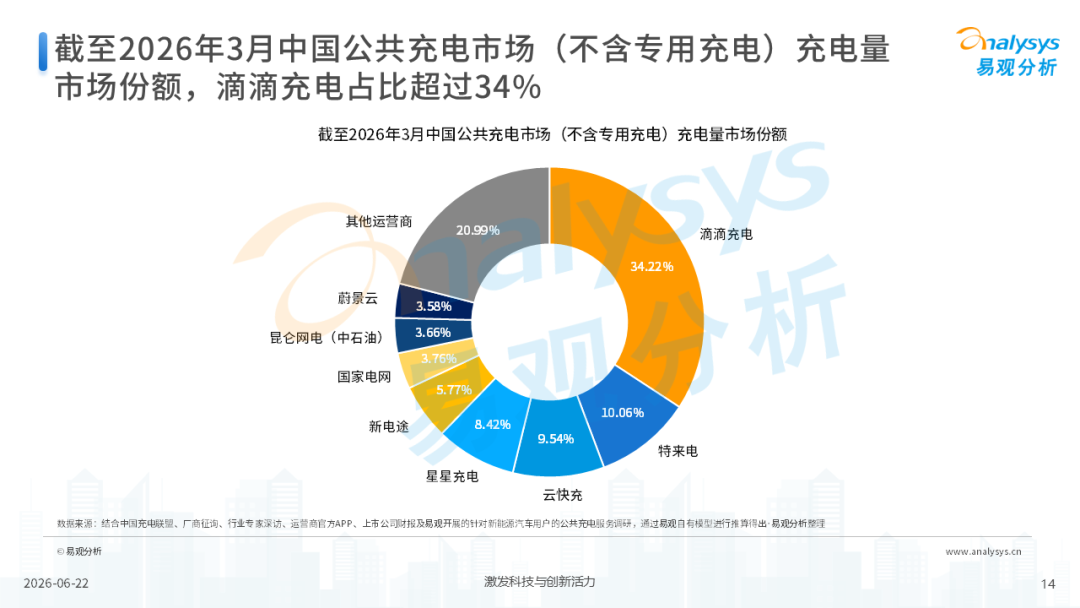

On June 22, 2026, the authoritative research institute Analysys released the report “New Trends and User Value Research in China’s Public Charging Consumer Market.”

The report reveals that as of March 2026, Didi Charging leads the market in terms of charging volume, capturing 34.22% of the market share, followed by competitors such as Teld (10.06%) and Yunkuai (9.54%).

Figure: Market Share of Charging Volume in China's Public Charging Market (Excluding Dedicated Charging)

It is noteworthy that this leadership position diverges from the traditional “scale-first” approach. It underscores a shift in the evaluation criteria within the public charging industry.

This transformation also signals that competition in the public charging sector is transitioning from the initial phase, driven by “scale,” to a subsequent phase, driven by “user value.”

From “Existence” to “Quality”

Infrastructure development has traditionally focused on achieving “existence” before addressing “quality.”

In the early days of the telecommunications industry, competition centered on the number of base stations, with “connecting every village” serving as both a goal and a metric. Once basic coverage was achieved, the focus shifted to internet speed and cost-effectiveness. Similarly, the express delivery industry initially competed on the number of outlets. Once delivery networks reached most villages and towns, user demands evolved to include next-day delivery and doorstep service.

The domestic public charging industry has been a prime example of scale-driven growth in recent years.

However, industry development is a dynamic process. At this stage, the core contradiction within the public charging industry is subtly shifting due to changes in supply and demand dynamics.

According to Analysys’ AMC industry cycle model, China’s public charging service market officially entered the application maturity phase in 2025. As of March 2026, the number of public charging stations in China reached 4.863 million, with the ratio of charging stations to vehicles narrowing from 1:3.7 in 2021 to 1:1.4 in the first quarter of 2026. Infrastructure development has largely kept pace with the growth of the new energy vehicle sector.

When the “availability of charging stations” is no longer the primary concern, the limitations of the old evaluation system become evident. The report indicates that 18.0% of vehicle owners report difficulty in finding charging stations, often encountering occupied or broken units. Additionally, 15.4% complain about poor station environments, 13.8% are dissatisfied with slow charging speeds, and 13.0% frequently experience equipment malfunctions.

Behind these statistics, many charging stations suffer from low utilization rates or even long-term idleness, with “zombie stations” becoming increasingly common. Much like a restaurant, no matter how many tables are set or how spacious the venue is, if no customers dine there, success remains elusive. Similarly, no matter how many charging stations are built, without frequent user engagement, their value cannot be fully realized.

The Top Spot Is Determined by Users

Peter Drucker, the father of modern management, once stated that the sole purpose of a business is to create customers. All hardware assets and layouts can only complete the closed loop—from investment to value—when genuinely chosen and frequently used by users.

In the public charging industry, the most direct quantitative result of this closed loop is charging volume. While the number of stations measures what companies “have,” charging volume measures what users “choose.”

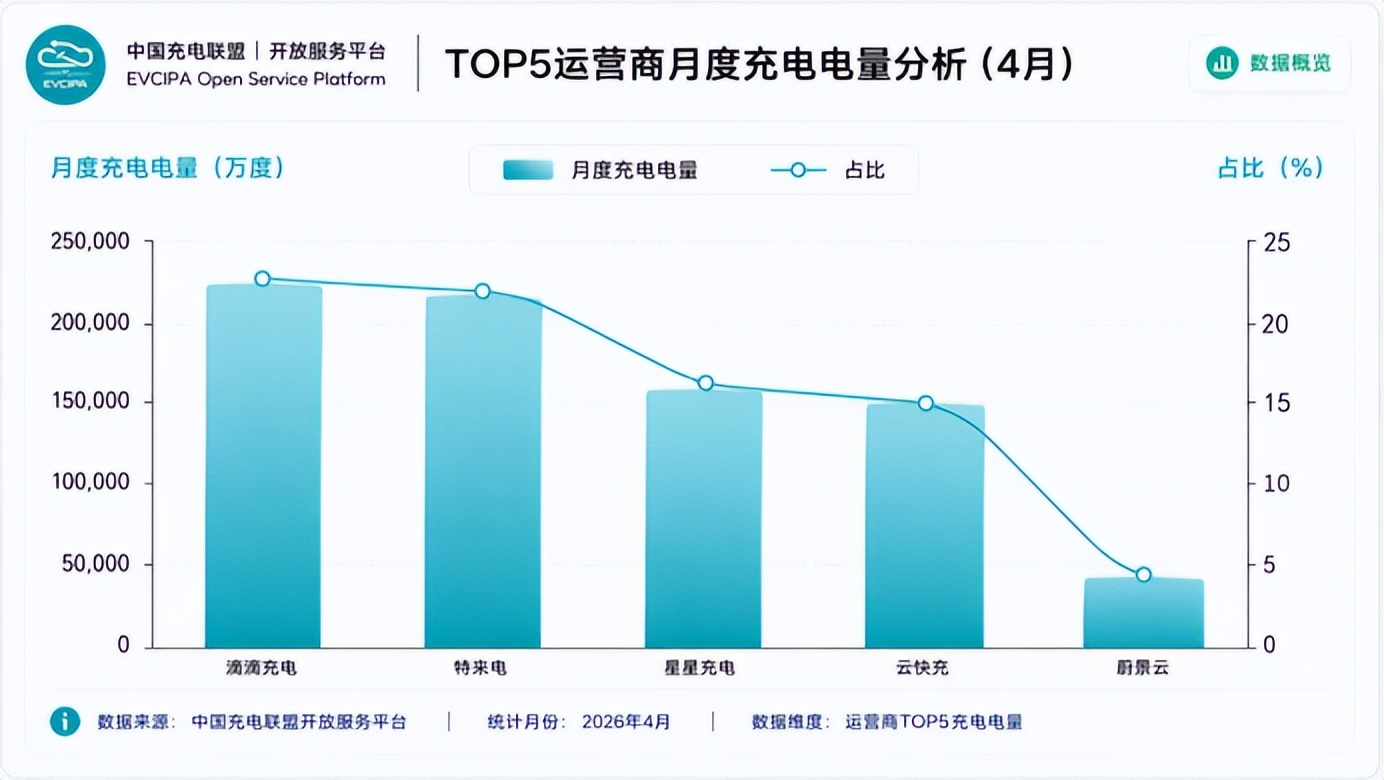

According to the aforementioned Analysys report, in the domestic public charging market (excluding dedicated charging), one out of every three units of electricity is delivered through the Didi Charging platform. Data from the China Electric Vehicle Charging Infrastructure Promotion Alliance’s open service platform corroborates this pattern: in April 2026, the top five operators by monthly charging volume delivered approximately 8 billion kWh, with Didi Charging ranking first at around 2.23 billion kWh.

Figure: Monthly Charging Volume Rankings from the China Electric Vehicle Charging Infrastructure Promotion Alliance’s Open Service Platform

Behind these rankings lies the direct reflection of service experience advantages in users’ actual choices.

On one hand, there is a precise matching of supply and demand structures. The report points out that 72.1% of new energy vehicle owners prioritize fast-charging stations when charging. As of March 2026, Didi Charging (92.3%), Haihuide (89.8%), and Kaimaisi (85.5%) lead in fast-charging station availability, aligning high-quality supply with core user demands.

On the other hand, operational efficiency is a key differentiator. If charging stations are compared to restaurant tables, the average number of vehicles charged per station per day represents the “table turnover rate” in the charging industry. A higher turnover rate indicates better utilization of individual stations. Analysys calculations show that Didi Charging serves an average of 7.7 vehicles per station daily, more than 2.5 times the second-ranked operator.

While most players focus on expanding their total number of stations to drive charging volume growth through asset expansion, Didi Charging amplifies the value of individual stations through operational and service capabilities.

Service Capability Is the Core of Future Competition

Metrics like “table turnover rate” or Net Promoter Score (NPS) may seem like mere numbers or decimals. However, as the charging industry enters its mature phase, leading players are shifting their strategic focus toward the user experience. Only those familiar with the industry’s evolution understand the effort and refinement behind each metric and data point.

Didi Charging initially entered the market by addressing the high-frequency energy replenishment needs of ride-hailing drivers. Leveraging an intelligent operational system, it built advantages in efficiency and service. Over the years, these strengths have expanded to serve a more diverse user base.

For example, at the equipment maintenance level, Didi Charging stations maintain an availability rate of over 97%. In terms of station layout, Didi Charging does not rely on blind expansion but instead strategically places stations in core travel areas with high traffic and strong energy replenishment demand. In these areas, users can typically find a Didi Charging station within a 3-kilometer radius.

To address the pain point of slow charging, Didi Charging continuously innovates with intelligent supercharging solutions. For instance, its “Accelerated Charging 2.0” reduces the average charging start time to around 10 seconds and increases charging speed by an average of 8%.

Beyond refining core charging dimensions, Didi Charging also looks at broader aspects.

Consider a typical scenario: during peak hours, users may hesitate to leave their vehicles while waiting in line to charge, fearing they might miss their turn if they step away to buy a meal. Addressing this practical and fragmented pain point, Didi Charging partnered with KFC to launch a “meal delivery to station” service, resolving the dilemma of choosing between charging and dining.

These meticulous refinements in frontline operational scenarios have culminated in Didi Charging’s exceptional service capabilities.

The public charging industry has evolved from “scarce stations” to “choice overload.” While each industry transformation involves changes in supply structures, one constant remains: only platforms that consistently create user value will endure in the long run.

-

![]()

Discounts Now on Offer: Is Xiaomi No Longer Grappling with Vehicle Shortages?

-

![]()

Samsung Doesn't Make Money the Hard Way

-

![]()

Japanese Media Acknowledges: China's Engine Technology Outstrips That of Japanese Firms

-

![]()

Japanese Media Concedes: China’s Engine Technology Outpaces Japanese Firms

-

![]()

Doubao Professional Version Unveiled! China Now Boasts Its Own National-Level Professional AI Agent

-

![]()

ByteDance and Alibaba Both Step Back from the Gaming Arena

-

Xiangeo International Clears BSE Review: Setting a Global Standard for the ‘Chinese Sound’ | A-Share Financing Brief

-

![]()

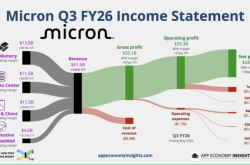

86% Gross Margin, Revenue Hits 48-Year High: Micron Warns of Prolonged Supply Tightness Beyond 2027