Equity Changes Hands Three Times in Seven Years: JMCG Leans on Contract Manufacturing for Survival Amid Brand Deficits

06/29 2026

06/29 2026

552

552

Recently, Jiangling Motors Holding Co., Ltd. (hereinafter referred to as "JMCG") has witnessed significant adjustments in its equity structure. Jiangxi Guokong Automobile Investment Co., Ltd. (hereinafter referred to as "Jiangxi Guokong") has completely exited the shareholder lineup, reverting the company to a joint governance model between Changan Automobile (000625.SZ) and Jiangling Motors Group Co., Ltd. (hereinafter referred to as "Jiangling Group"). Since 2019, JMCG has undergone several equity changes, including the failure of its mixed-ownership reform and the entry of Jiangxi Guokong, ultimately returning to its original ownership structure.

Securities Star observes that JMCG initially achieved sales peaks in its early years, largely due to its reliance on Landwind Automobile. However, factors such as model controversies and intense market competition led to Landwind Automobile's decline. Constrained by a lack of core technologies and proprietary brands, JMCG has increasingly become a contract manufacturer for Changan Automobile. The narrow profit margins of this pure contract manufacturing model and the company's heavy reliance on Changan Automobile's sales performance pose significant challenges. Whether this equity restructuring can reverse JMCG's long-standing business difficulties remains to be seen.

01. Jiangxi Guokong's Exit

On May 25, the State Administration for Market Regulation released a list of unconditionally approved cases of concentration of undertakings from May 11 to May 17, 2026. This list included the case of Changan Automobile and Jiangling Group acquiring JMCG's equity. Public records show that Jiangxi Guokong, a local state-owned enterprise, signed agreements with Changan Automobile and Jiangling Group to transfer 25% of JMCG's equity to Changan Automobile and gratuitously transfer another 25% to Jiangling Group.

Prior to the transaction, JMCG's shares were held 50% by Jiangxi Guokong, 25% by Changan Automobile, and 25% by Jiangling Group. After the transaction, Jiangxi Guokong completely exited, ending five years of "tripartite joint governance." JMCG is now equally owned by Changan Automobile and Jiangling Group, returning to a state of joint control by both parties.

According to available data, JMCG was established in November 2004 as a vehicle manufacturing enterprise jointly founded by Changan Automobile and Jiangling Group, with both parties holding 50% stakes and focusing on the Landwind brand passenger vehicles.

In 2019, JMCG initiated a mixed-ownership reform plan. On the one hand, the company underwent a division by way of survivorship, transferring the equity of Jiangling Motors and some liabilities to a newly established company, Nanchang Jiangling Investment Co., Ltd. JMCG retained Landwind Automobile and its operating business, land, and other assets. On the other hand, JMCG introduced strategic investors through public listing. In July 2019, Aiways Automobile Co., Ltd. (hereinafter referred to as "Aiways"), a new car-making force eager to achieve mass production and delivery, increased its capital by RMB 1.747 billion, acquiring a 50% stake and becoming the largest shareholder. Changan Automobile and Jiangling Group's shareholdings were diluted to 25% each. This transaction was once seen as a model of cooperation between central enterprises, local state-owned enterprises, and private enterprises.

Securities Star learned that at the time, Aiways aimed to resolve its production capacity dilemma through this cooperation, while JMCG sought growth engines through mixed-ownership reform. According to the strategic cooperation plan, the reformed JMCG would form a dual-brand, dual-manufacturing base-driven pattern with Aiways and Landwind. Landwind brand products would cover both traditional and new energy vehicle models, while the Aiways brand would focus on new energy vehicles.

However, the partnership was short-lived as Aiways' market performance was unsatisfactory. Its first model, the U5, failed to gain traction in the market after its launch in 2019. Data shows that Aiways sold only 2,600 vehicles in 2020. Facing multiple operational pressures, including sales and funding issues, Aiways transferred its 50% stake to Jiangxi Guokong in June 2021. After acquiring half of the equity, Jiangxi Guokong gained actual control, while Changan Automobile and Jiangling Group continued to hold 25% each. The tripartite shareholding structure persisted until this equity restructuring.

02. 150,000-Unit Annual Production Capacity Tied to Changan Automobile

Throughout JMCG's development, its operational fluctuations have been closely tied to the performance of its Landwind Automobile subsidiary. Leveraging the high attention garnered by the Landwind X7, Landwind Automobile's sales exceeded 80,000 units in 2016 but plummeted to approximately 25,700 units in 2018. In 2019, a court ruled that the appearance of the Landwind X7 plagiarized the Range Rover Evoque, ordering JMCG to cease all sales of the Landwind X7 and pay compensation to Jaguar Land Rover. Landwind Automobile's sales further declined to less than 10,000 units in 2019 and fell below 1,000 units by 2021. Currently, the brand has exited the mainstream independent brand market.

In fact, Landwind Automobile's decline stemmed from its lack of original core technology accumulation. Product iterations relied on imitation and borrowing, failing to form exclusive technological barriers and product characteristics. Against the backdrop of the accelerating wave of new energy vehicles, Landwind Automobile's lagging electrification layout made its marginalization almost inevitable.

The loss of momentum for Landwind Automobile and the exit of Aiways resulted in JMCG losing its independent brand value among consumers. During its operational trough, the company faced severe idle production capacity, once teetering on the brink of bankruptcy, with a total amount of nearly RMB 50 million in enforcement and several subsidiaries being deregistered.

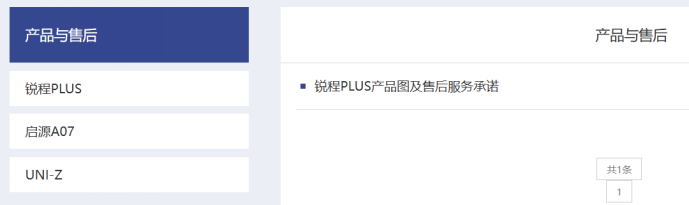

Securities Star notes that currently, JMCG's production capacity layout has shifted to primarily undertaking contract manufacturing orders for the Changan Automobile system. The company currently undertakes the production tasks for three models: Ruicheng PLUS, Qiyuan A07, and UNI-Z, with the latter two being core models in Changan Automobile's new energy vehicle lineup.

According to JMCG's official website, the company has an annual production capacity of 150,000 units and possesses mature automated, intelligent, and flexible production lines for the four major processes of stamping, welding, painting, and assembly. These lines are capable of meeting the production requirements for fuel, hybrid, and pure electric vehicle platforms. During the "15th Five-Year Plan" period, the company aims to rapidly transform into an intelligent manufacturing and new energy vehicle production enterprise, positioning itself as a first-class intelligent manufacturing base for Changan Automobile. This indicates that the company's strategic focus has shifted towards contract manufacturing.

However, this contract manufacturing model has inherent profitability shortcomings. JMCG only earns processing fees and cannot share in the full-chain benefits of vehicle sales and brand premiums. Even if the production lines operate at full capacity, they cannot leverage economies of scale to open up profit growth space. Additionally, JMCG's capacity utilization and revenue will be deeply tied to Changan Automobile's market sales performance.

In 2025, Changan Automobile achieved annual sales of 2.913 million units, reaching a near-nine-year high. However, the growth momentum ceased in 2026. In the first five months of 2026, Changan Automobile sold 916,900 units, down 18.14% year-on-year; new energy vehicle sales were 321,700 units, down 8.31% year-on-year. The company set a sales target of 3.3 million units for 2026, including a new energy sales target of 1.4 million units. The completion rates for the total sales target and the new energy sales target in the first five months were 27.78% and 22.98%, respectively, with less than 30% completed in nearly half a year. Once Changan Automobile's sales fluctuate or its new energy strategy progresses below expectations, JMCG may face risks of idle production capacity and profitability pressure. (This article is first published on Securities Star, author | Lu Wenyan)

- End -

-

![]()

Can Chinese Automakers Pose Such Fierce Competition? Mercedes-Benz Cancels Year-End Bonuses for 90,000 Staff, Volkswagen to Lay Off 100,000 Employees...

-

![]()

Anhui and Zhejiang Vie for the Crown in New Energy Vehicle Dominance: Who Will Prevail?

-

![]()

Tmall 618 Rankings Unveil Trends Transforming the Home Appliance Industry

-

![]()

This Week in Home Appliances: Overseas Boom! Midea, TCL, Dreame Break Through; Casarte, Fotile, Gree, Hisense, Ronshen Lay Foundations

-

![]()

Aiming to Be the Alphard of the Electric Era! After D99's Launch, Leapmotor Will Release All-New Technologies to Pave the Way for a High-End Brand | Mirrormedia Pro

-

![]()

Over 5,200 Orders Placed on First Day: Can the Qijing GT7, Priced from 209,900 Yuan, Compete with the Z7 and SU7? | Mingjing Pro

-

![]()

AI Predicting the World Cup? It’s Time to Stop Insulting AI

-

![]()

iPhone 18 Pro Memory Costs Soar Threefold! Apple Seeks Trump Administration Approval for CXMT Memory Chips