Accounting Manipulations Inflate Profits! 2 Billion Yuan Cumulative Loss Over Six Years—How Long Can the AI Narrative Sustain?

07/01 2026

07/01 2026

401

401

On June 15, 2026, UCloud (UCloud, 688158.SH) issued a correction notice addressing accounting errors, revising its financial data for the first half and third quarter of 2025, and responding to a regulatory inquiry from the Shanghai Stock Exchange concerning its annual report.

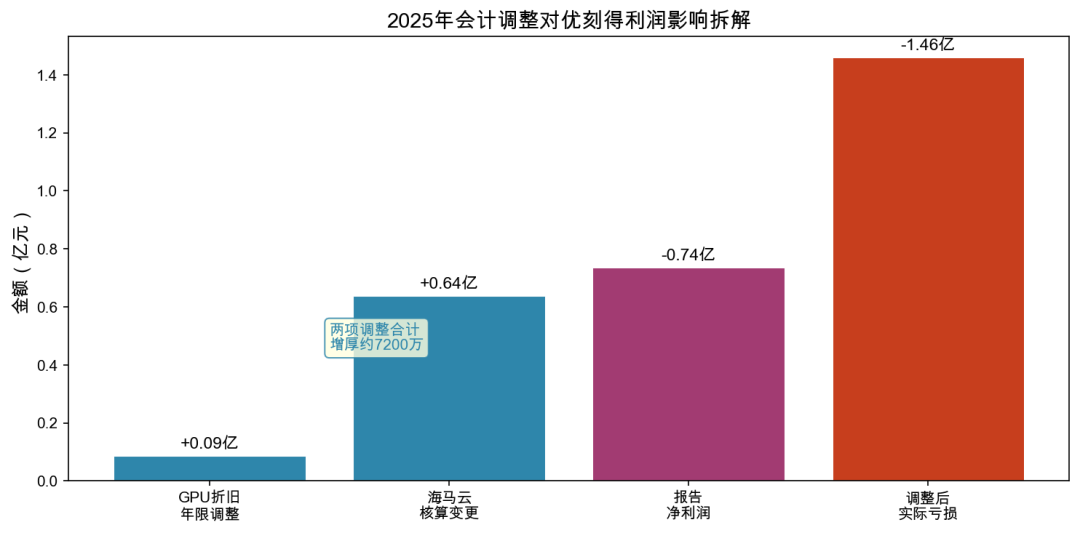

This announcement exposed the truth behind UCloud's "significant loss reduction" in 2025: through adjustments to the depreciation period of GPUs and changes in accounting methods, the company's 2025 financial statements artificially inflated profits by over 72 million yuan. After excluding these accounting adjustments, the actual loss amounted to approximately 146 million yuan.

This situation reflects broader challenges faced by independent third-party cloud service providers.

Amid competition from industry giants like Alibaba Cloud, Tencent Cloud, and Huawei Cloud, third-party cloud providers such as UCloud, QingCloud, CapitaOnline, and Paratera are grappling with dual pressures of transformation and profitability.

When UCloud went public, financial commentator Xingkong Jun (a pseudonym) expressed skepticism, questioning how UCloud could achieve profitability when even Alibaba Cloud had not done so at the time.

In its prospectus, UCloud positioned itself as a third-party cloud service provider, emphasizing its suitability for party and government entities and e-commerce companies.

However, the reality is that most party and government entities lease cloud resources from telecom operators, while e-commerce companies are reluctant to store their data on Alibaba Cloud.

1

The Magic of Accounting Adjustments

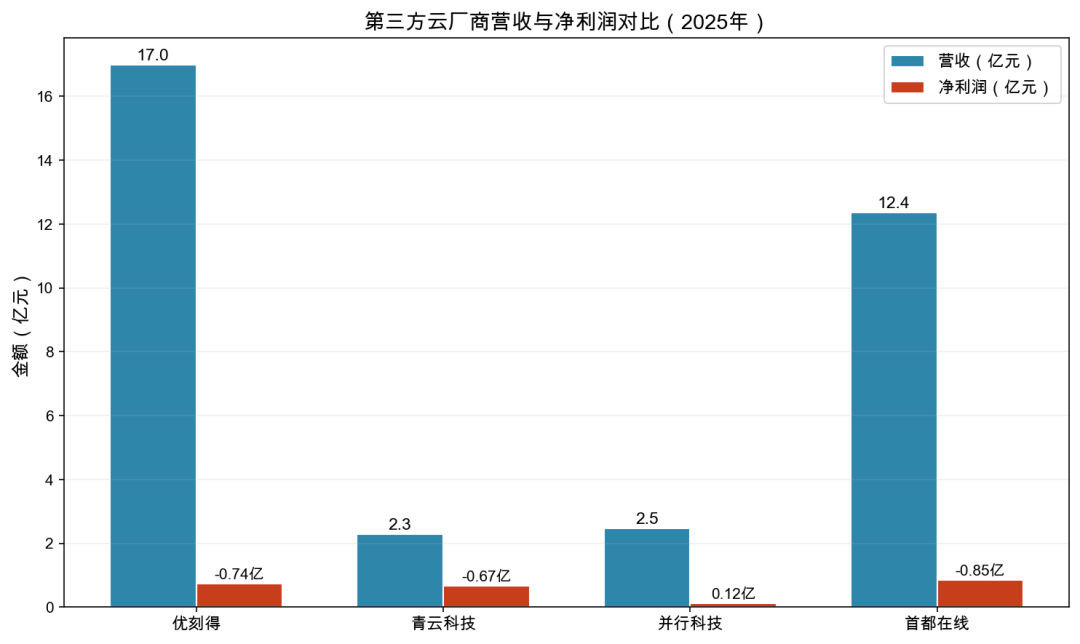

UCloud's 2025 annual report indicated revenue of 1.699 billion yuan, up 13.07% year-on-year, with a net loss attributable to shareholders of 73.5534 million yuan—a 69.49% reduction in losses compared to the previous year. This "nearly 70% loss reduction" initially captured market attention.

However, a regulatory inquiry from the Shanghai Stock Exchange unveiled the facade.

First Adjustment: The depreciation period for GPUs was extended from four years to five years.

The company stated that after evaluation, it deemed a five-year depreciation period for GPU servers more appropriate, aligning better with the assets' actual usage and business value. This change reduced fixed asset depreciation expenses by 8.8619 million yuan in 2025, boosting net profit by 8.5925 million yuan.

Second Adjustment: Change in accounting method for equity investment in HaiMaYun.

Following a reshuffle of HaiMaYun's board of directors, UCloud's nominated director was not elected, resulting in the loss of significant influence. Consequently, the company reclassified HaiMaYun from a long-term equity investment to a financial asset measured at fair value, recognizing an investment gain of 63.8029 million yuan.

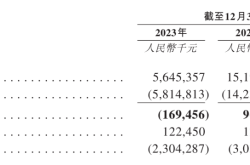

Together, these accounting adjustments artificially inflated the financial statements by approximately 72.3954 million yuan in profits. Excluding these adjustments, UCloud's actual net loss in 2025 was approximately 146 million yuan—roughly double the 73.55 million yuan reported in the annual report.

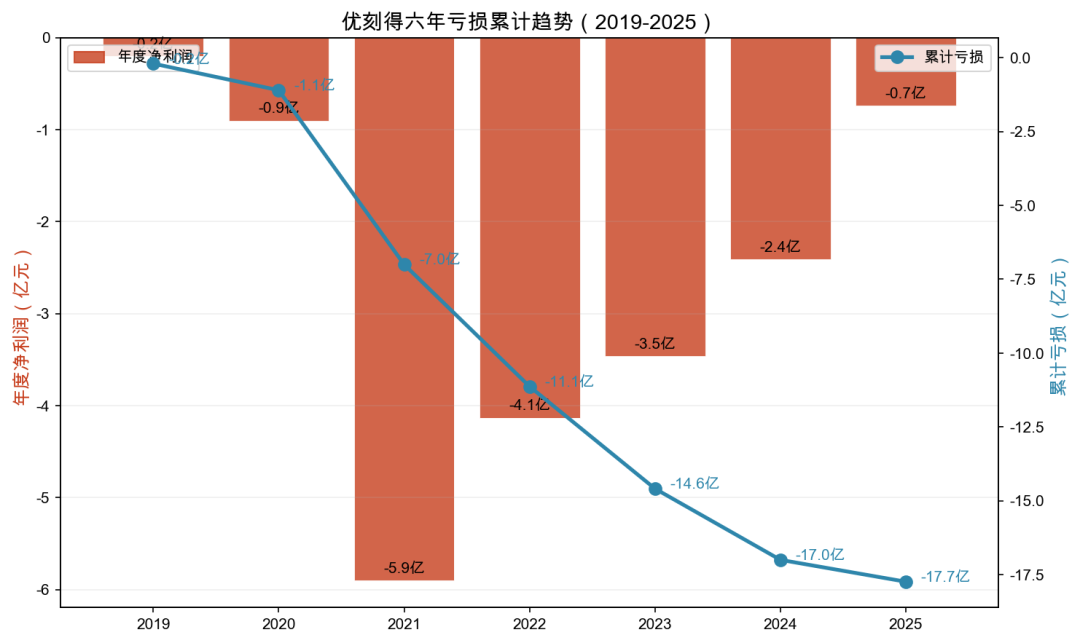

Since listing on the STAR Market in January 2020, UCloud's annual net losses attributable to the parent company have been as follows: approximately 20 million yuan in 2019, 90 million yuan in 2020, 590 million yuan in 2021, 413 million yuan in 2022, 346 million yuan in 2023, 241 million yuan in 2024, and 74 million yuan in 2025. The cumulative losses over six years exceed 2 billion yuan.

Notably, in 2022, UCloud issued a pre-loss announcement estimating a loss of 430-470 million yuan, but the final audited annual report showed a loss of 413 million yuan.

Similar discrepancies between pre-announcements and annual reports persisted in subsequent years.

In terms of loss trends, 2021 marked the peak loss (-590 million yuan), followed by a year-on-year narrowing of losses.

The "loss reduction" in 2025 was the most significant, but as previously mentioned, a substantial portion of it stemmed from accounting adjustments.

To assess UCloud's profitability turning point, attention should focus on two indicators less reliant on accounting estimates: non-recurring profit and loss and operating cash flow. In 2025, non-recurring profit and loss showed a loss of approximately 217 million yuan, and net operating cash flow was approximately -85 million yuan—neither turned positive.

2

The Survival Dilemma of Third-Party Cloud Service Providers

UCloud is not alone in its struggles. Among A-share independent third-party cloud providers:

QingCloud Technology reported revenue of 228 million yuan in 2025, with a net loss attributable to the parent company of 66.66 million yuan.

Paratera reported revenue of approximately 248 million yuan in 2025, with a net profit of 12.22 million yuan (non-recurring profit and loss of -70,000 yuan, close to breakeven).

CapitaOnline reported revenue of 1.237 billion yuan in 2025 (source: annual report), with a net loss attributable to the parent company of approximately 85 million yuan.

Among these four companies, only Paratera achieved a slight profit, while the other three remained unprofitable. In terms of revenue scale, UCloud led with 1.699 billion yuan, but compared to Alibaba Cloud (annual revenue exceeding 100 billion yuan), Tencent Cloud (annual revenue exceeding 80 billion yuan), and Huawei Cloud (annual revenue exceeding 60 billion yuan), the scale gap for independent third-party cloud providers is vast.

3

Crafting the Computing Power Narrative

UCloud is fully committed to the AI computing power business.

As of June 2026, the company operates globally across 28 regions and 36 availability zones, including a newly added zone in Uzbekistan.

In the first quarter of 2026, the company achieved revenue of 439 million yuan (up 16.77% year-on-year), with a net profit of 2.74 million yuan—marking its second consecutive quarter of profitability.

AI computing power is the core logic behind UCloud's potential turnaround. Its GPU servers, with a net value of approximately 357 million yuan, primarily serve AI training and inference scenarios.

Against the policy backdrop of domestic substitution and autonomous, controllable computing power, independent third-party cloud providers enjoy compliance advantages over foreign cloud providers and greater flexibility and customization capabilities compared to leading internet cloud providers.

However, risks remain significant.

Giants such as AWS, Azure, Alibaba Cloud, and Tencent Cloud continue to lower prices, exerting pressure on industry gross margins. According to UCloud's 2025 annual report, its overall gross margin in 2025 was 24.75%. Referring to Paratera's trend of gross margin declining from 32.09% to 22.03%, the price war in cloud computing infrastructure persists.

Additionally, UCloud's strategic adjustment regarding HaiMaYun warrants attention.

HaiMaYun is preparing for an IPO, with UCloud holding approximately 11.78% of the shares. If HaiMaYun goes public successfully, the financial assets held by UCloud may see significant fair value revaluation gains, but these are non-recurring items.

4

Conclusion

UCloud has accumulated losses exceeding 2 billion yuan over six years, artificially inflating profits by over 70 million yuan through accounting adjustments in 2025.

While accounting adjustments can influence short-term financial data, they cannot alter the underlying business fundamentals. The company achieved profitability for the second consecutive quarter in Q1 2026, but non-recurring profit and loss and operating cash flow have not yet turned positive.

For independent third-party cloud providers, AI computing power may represent the biggest variable for breakthrough. However, amid intense competition from industry giants and ongoing price wars, whether the profitability turning point will arrive as scheduled remains to be seen over time.

Accounting adjustments may temporarily enhance the appearance of financial statements, but true value creation ultimately depends on substantial business revenue.

-END-

Disclaimer: This article is based on the public company attributes of listed companies and core information disclosed by them in accordance with their legal obligations (including but not limited to interim announcements, periodic reports, and official interaction platforms) for analytical research. Shiyu Xingkong strives for fairness in the content and views presented in the article but does not guarantee its accuracy, completeness, or timeliness. The information or opinions expressed in this article do not constitute any investment advice, and Shiyu Xingkong assumes no responsibility for any actions taken based on this article.

Copyright Notice: The content of this article is original to Shiyu Xingkong and may not be reproduced without authorization.

-

【In-depth】Current Market Status and Key Enterprise Analysis of Confocal Fluorescence Microscopes in 2026

-

![]()

Avita Releases Updated Prospectus: Projecting Over 120,000 Vehicle Sales and Over 60% YoY Revenue Growth by 2025

-

![]()

Navigating the Electric Wave: Mercedes-Benz Embraces the Three-Pointed Star, Audi Sheds the Four Rings

-

![]()

BYD Delegates Power, Geely Centralizes It: Which Transformation is Better Suited for the Future?

-

![]()

National Standard for Agent Interconnection Released: Why Might the Physical World Still Be Unreachable Despite Unified Interfaces?

-

![]()

Mobile Imaging: As Capabilities Grow, So Do the 'Add-Ons'—Why?

-

![]()

The imaging capabilities of smartphones are continuously improving, but why are there more and more 'add-ons' for shooting?

-

![]()

Alibaba's AI 'Crucible': Navigating Overseas Blockades, Organizational Upheaval, and the Lag in Commercialization