Avita Takes Another Stab at HKEX Listing: Facing the Urgency of Sustaining Operations Amid 11.2 Billion Yuan Loss Over Three Years

07/02 2026

07/02 2026

386

386

The Imperative for a Second Capital Growth Trajectory

Author|Wang Lei

Editor|Qin Zhangyong

After a six-month hiatus, Avita has once again set its sights on an Initial Public Offering (IPO).

According to disclosures from the Hong Kong Stock Exchange, Avita Technology (Chongqing) Co., Ltd. has revised and resubmitted its application materials for listing on the main board.

In contrast to its previous submission in November of the previous year, Avita now exudes greater confidence. Its financial data has been updated to cover the entire year of 2025, revealing sales exceeding 127,000 vehicles—marking a year-on-year increase of over 60%—and revenue that has quadrupled over the past three years. These figures amply demonstrate the stability of Avita's performance.

This time, Avita has also officially included Yinwang in its prospectus, with a 10% stake. It achieved positive returns in the first year, securing 182 million yuan in dividends.

On the surface, Avita appears well-prepared, but behind the veneer, the Avita of 2026 seems somewhat “fragmented.”

01 Revenue Quadruples Over Three Years

Back in November 2025, merely two months after completing its shareholding reform, Avita officially submitted its prospectus, with CICC and CITIC Securities serving as joint sponsors, aiming to raise $1 billion. Just as many believed Avita would be the first central state-owned new energy vehicle company to sprint for an IPO, progress came to an abrupt halt.

Until May 27th of this year, the Hong Kong Stock Exchange's official website indicated that Avita's prospectus had expired. According to HKEX regulations, if a company fails to complete the listing hearing and listing process within six months from the date of prospectus submission, the application documents automatically expire.

On the same day the prospectus expired, Avita publicly responded, stating that the expiration was a routine technicality in the IPO process. The company was updating the prospectus as required and would promptly resubmit it, with the overall listing timeline remaining unaffected.

This led to the scenario of a second prospectus submission. Just a month later, Avita reapplied for listing, signaling its intent to expedite the process.

Moreover, with the second prospectus submission, the latest financial data was updated from the first half of 2025 to the entire year of 2025, clearly presenting Avita's comprehensive operating performance over the past three years to the public.

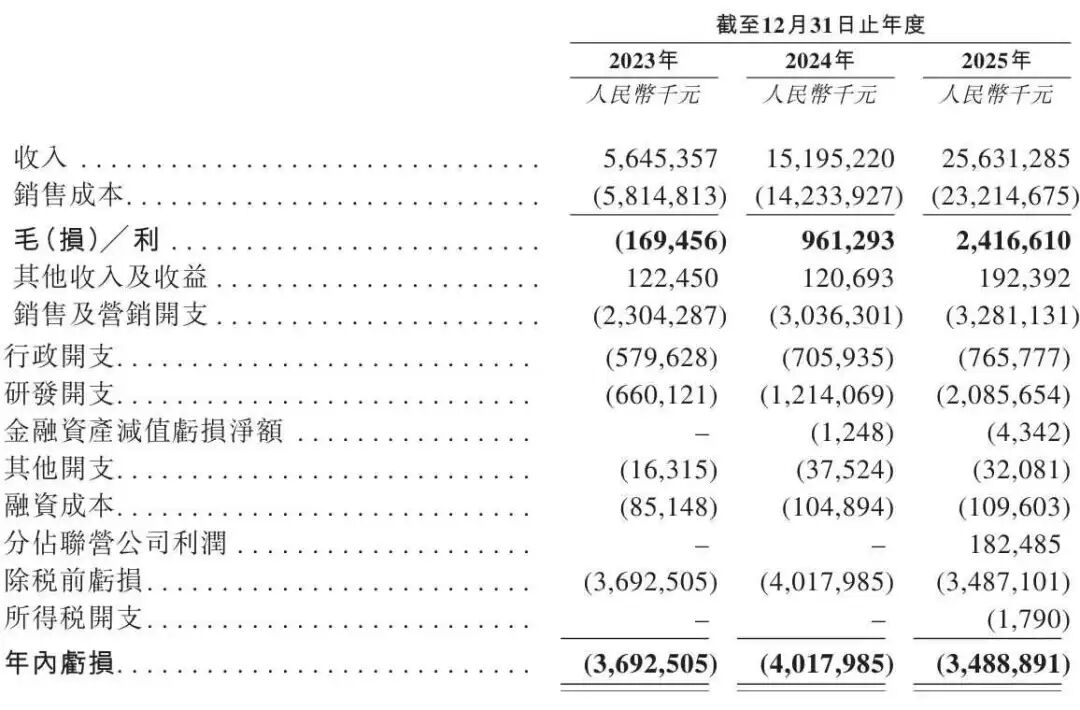

From 2023 to 2025, Avita's operating revenues were 5.645 billion yuan, 15.195 billion yuan, and 25.631 billion yuan, respectively. The cumulative revenue over these three years amounted to approximately 46.5 billion yuan, with a compound annual growth rate exceeding 113%. Revenue grew 4.5 times over the three-year period, with revenue from the core vehicle business increasing about 4.3 times.

In terms of sales volume, since commencing vehicle deliveries in December 2022, Avita's total deliveries surged from 20,000 units in 2023 and 61,600 units in 2024 to 122,700 units in 2025, with a total of over 204,300 units delivered over the three-year span.

Notably, 2025 marked a breakthrough year for Avita. With a 68.7% year-on-year increase in revenue, annual deliveries reached 122,700 units, nearly doubling year-on-year. The annual gross profit margin also improved to 9.4%, with annual gross profit reaching 2.417 billion yuan, a 151.7% increase, significantly up from 6.3% in 2024 and -3% in 2023.

However, this gross profit margin remains relatively low among domestic new car manufacturers. In 2025, the gross profit margins of domestic new car manufacturers were all in double digits. For instance, Li Auto and XPeng boasted gross profit margins above 18%, while NIO's was 13.6%.

It is also noteworthy that in the initial prospectus, the gross profit margin for the first half of 2025 was 10.1%, with revenue at 12.208 billion yuan, less than half of the annual figure. This implies that Avita's gross profit margin declined in the second half of 2025 despite a year-on-year and sequential increase in revenue, indicating a deterioration in its profitability.

Furthermore, overseas markets emerged as a highlight for Avita in 2025, with overseas revenue reaching 1.398 billion yuan, accounting for 5.5% of total revenue, and an average overseas selling price exceeding 300,000 yuan. By the end of 2025, the brand had penetrated 38 countries and regions, boasting over 80 sales outlets.

Apart from vehicle sales, Avita's revenue from other businesses surged from 103 million yuan in 2023 to 777.9 million yuan in 2024, accounting for 1.8% and 5.1%, respectively.

In 2025, Avita's revenue from components and other businesses was 1.729 billion yuan, accounting for 6.7%. Moreover, the growth rate of this segment far outpaced that of the core vehicle business, increasing nearly 17-fold over the three-year period.

Of course, Avita has not yet extricated itself from the quagmire of losses, but the magnitude of losses has significantly diminished year by year.

The net loss in 2025 was 3.489 billion yuan, narrowing from 4.018 billion yuan in 2024 and 3.69 billion yuan in 2023, with cumulative losses over the three years exceeding 11.2 billion yuan.

This is primarily attributable to operating losses stemming from high production, research and development, and channel expansion costs. For example, in 2025, the cost of sales still accounted for a hefty 90.6% of revenue, reaching 23.2 billion yuan, with raw material costs alone at 20.804 billion yuan, accounting for 89.6% of the cost of sales.

Avita also acknowledged in its prospectus that its cost structure has not yet fully benefited from economies of scale: “Our relatively modest procurement volumes limit our bargaining power with component suppliers, while manufacturing-related costs are spread over relatively low delivery volumes during the growth stage, adversely affecting our gross profit margin and overall profitability.”

Additionally, research and development remains a key focus for Avita. Over the past three years, R&D expenses were 660 million yuan, 1.214 billion yuan, and 2.086 billion yuan, respectively. About 55% of the company's employees are engaged in R&D, with R&D spending increasing by 71.8% year-on-year in 2025.

Notably, in this updated prospectus, Avita officially included the Yinwang investment completed in 2025, disclosing that it had invested 11.5 billion yuan to acquire a 10% stake in Yinwang and achieved positive investment returns in the first year, with a 182 million yuan share of the associate company's profits in 2025.

It also unveiled three new products co-created with Huawei Yinwang, including a new full-size SUV and new mid-size and full-size SUVs, all featuring both pure electric and extended-range dual powertrains.

However, precisely because of the one-time expenditure of 11.5 billion yuan last year, Avita's liquidity tightened from 2024 to 2025, with the current ratio dropping from 1.3 to 0.6 and the quick ratio declining from 1.1 to 0.5 during the same period.

This underscores that Avita still requires a capital infusion to sustain operations, with the IPO being the linchpin for the next round of funding.

02 Avita Needs a Fresh Narrative

Undeniably, from the overall prospectus, Avita at the end of 2025 exudes confidence, with sales exceeding 10,000 units for 10 consecutive months and over 120,000 units annually, marking a year-on-year increase of over 60%, and demonstrating the stability of its performance.

Coupled with the endorsement of the “CHN Iron Triangle” composed of Changan, Huawei, and CATL, this narrative holds significant sway in the capital markets.

Prior to submitting the prospectus, based on the disclosed transfer of a 0.24% stake in Avita by Botai Automotive to an external party for 62.44 million yuan, Avita's valuation reached 26 billion yuan when back-calculated from this equity purchase price.

However, just half a year later, the landscape has shifted. This year, Avita's sales growth momentum has significantly waned. In January, it failed to release monthly sales data as scheduled, sparking industry speculation about delivery pressures. From January to May, Avita delivered 2,216, 4,033, 5,143, 5,279, and 7,336 units, respectively.

As of May, Avita's total car sales were merely 24,007 units, including 2,949 units sold overseas. Sales in the past six months were a fraction of last year's annual total.

In comparison, not only have first-tier domestic new car manufacturers surpassed 30,000 units in monthly sales, but even most “factory-backed” brands have maintained monthly sales of around 10,000 units.

When sales can no longer bolster its valuation, can Avita's IPO journey proceed as planned?

Although many consider Avita to be born with a “golden key,” backed by Changan, CATL, and Huawei, and unlike other car manufacturers that heavily invest in factory construction (a “heavy asset” model), Avita adopts a “light asset” approach.

Changan Automobile provides vehicle R&D and manufacturing support, CATL supplies battery technology, and Huawei offers intelligent vehicle solutions. The advantage of this model is that Avita does not have to build its own intelligent driving and battery capabilities from scratch, but the downside is that each party takes a share of the profits.

Behind the 9.4% gross profit margin, the proportion allocated to Huawei as royalties and to CATL as procurement costs is not detailed in the prospectus but is somewhat reflected.

In the first half of the previous year, Avita purchased products and materials worth 1.834 billion yuan from Shenzhen Yinwang, controlled by Huawei, and its affiliates, paying 376 million yuan in R&D service fees, totaling 2.21 billion yuan. Combined with Avita's sales volume in the first half of the previous year, this equates to approximately 39,000 yuan per vehicle sold being allocated to the Huawei ecosystem.

This is also why, throughout 2025, raw material costs reached 20.804 billion yuan, accounting for 89.6% of the cost of sales.

More dishearteningly, Avita, which once proudly referred to itself as “Huawei's legitimate offspring,” is witnessing its uniqueness significantly diluted. At its inception, fewer than five companies had Huawei's technological support.

However, according to data released at the 2026 Huawei Qiankun Technology Conference, as of April, Huawei Qiankun had partnered with over 25 brands, with over 50 models featuring Huawei ADS in mass production and cumulative vehicle installations exceeding 1.7 million units. Jin Yuzhi, CEO of Huawei's Intelligent Automotive Solutions BU, also revealed that by 2026, over 80 models will feature Huawei Qiankun intelligent driving, with cumulative installations expected to reach 3 million units.

Although Avita heavily invested 11.5 billion yuan to acquire a 10% stake in Huawei Yinwang, signaling to the outside world its priority in technology, it still cannot halt the dissipation of Huawei's technological dividends.

Today, this “luxury friend circle,” once a boon, is becoming a deep-seated contradiction that hampers its independent development. Avita needs to discover new breakthrough directions within its own brand essence.

While the prospectus can be resubmitted, the market will not afford multiple opportunities for redress. Whether Avita will “soar upon listing” or “peak upon listing” remains to be seen.

-

![]()

Behind the Release of Its First Self-Developed Chip, Is OpenAI's Full-Stack Ambition on Display?

-

![]()

Has Anthropic Targeted Chinese Users? Is a New Era of AI-Driven Racial Discrimination Emerging?

-

![]()

MathWorks: Generative AI Holds Great Potential, Yet a Trusted Toolchain is Essential for Flawless Operation

-

![]()

Small Earphones, Big Business

-

![]()

Volkswagen Slashes 100,000 Jobs, Mercedes-Benz Axes Year-End Bonuses: What’s Ailing German Auto Titans?

-

![]()

Doubao Can No Longer Offer Free Services to 345 Million Users: China's Era of Free AI Is Drawing to a Close

-

![]()

How Can Chinese Small Home Appliances Conquer Southeast Asia Through 'Dimensional Competition'?

-

![]()

Why are top intelligent driving players betting on reinforcement learning?