Avatr’s Second Bid for a Hong Kong Stock Exchange Listing: Fueled by Robust Performance Growth and Backed by Changan, CATL, and Huawei, It Faces Rising Market Competition and General Market Saturation

07/03 2026

07/03 2026

330

330

Avatr’s Urgent Pursuit of a Hong Kong Stock Exchange Listing: High Growth and Substantial Investment, Supported by Three Industry Leaders, Must Demonstrate Profitability and Overcome Market Competition

The new energy vehicle (NEV) manufacturing sector is no stranger to companies that experience revenue growth while incurring profit losses. On one hand, revenues are surging, and on the other, substantial losses continue to loom large—this is the current scenario for Avatr, which is making its second attempt to list on the Hong Kong Stock Exchange.

According to Sina Finance, Avatr Technology updated its prospectus for the Hong Kong Stock Exchange on July 1, restarting its IPO process.

This high-end intelligent vehicle company, backed by Changan Automobile, CATL, and Huawei, is officially embarking on its second venture into the capital market. However, the new energy sector in the Hong Kong stock market has cooled considerably, and the previously frenzied atmosphere has subsided.

Avatr boasts an exceptional pedigree. Its predecessor was Changan NIO, a joint venture established in 2018 between Changan Automobile and NIO. It underwent rebranding and transformation in 2021 and now operates research and development centers in Chongqing, Shanghai, and Munich, Germany.

From its inception, Avatr has been a collaborative effort among industry giants: Changan Automobile is the controlling shareholder, CATL is the second-largest shareholder, and it has deep ties with Huawei’s HiCar ecosystem. The company invested 11.5 billion yuan to acquire a 10% stake, gaining access to intelligent driving and core technology resources.

From a data perspective, Avatr’s growth trajectory is remarkable. Its revenues for 2023, 2024, and 2025 were 5.645 billion yuan, 15.2 billion yuan, and 25.6 billion yuan, respectively, with a compound annual growth rate (CAGR) of 113% over three years. Cumulative revenue exceeded 46.5 billion yuan, more than quadrupling and distinguishing itself among high-end NEV companies.

Gross profit margins are also showing steady improvement. Over the three years, gross profit rose from -169 million yuan to 961 million yuan and then to 2.4 billion yuan, successfully transitioning from losses to profits. This improvement reflects continuous optimization of product structure and supply chain management capabilities.

However, vehicle manufacturing is inherently capital-intensive and cash-consuming. During the same period, losses amounted to 3.693 billion yuan, 4.018 billion yuan, and 3.489 billion yuan, respectively, totaling nearly 11.2 billion yuan over three years. Although losses narrowed in 2025, there was still a net loss of nearly 3.5 billion yuan. That year alone, total costs reached 23.2 billion yuan, including 3.281 billion yuan in sales and marketing, 766 million yuan in administrative expenses, and 2.086 billion yuan in research and development, placing immense pressure on fixed expenditures.

More concerning is the tightening liquidity situation. As of the end of 2025, cash and cash equivalents stood at 9.687 billion yuan, but the current ratio dropped from 1.3 to 0.6, and the quick ratio from 1.1 to 0.5, nearly halving. This decline can be attributed to two main factors: first, the 11.5 billion yuan investment in Huawei HiCar was converted into non-current assets, consuming a significant portion of available funds; second, rapid business expansion, product iterations, sales network expansion, and inventory stocking significantly increased working capital requirements.

To support its expansion, Avatr has maintained frequent financing activities. It completed a 3 billion yuan capital increase in 2023 and raised over 11 billion yuan in Series C financing by the end of 2024, with continuous support from Changan Automobile, Southern Asset Management, Bank of Communications Investments, and Anyu Fund. After this round, Changan Automobile holds a 40.99% stake, and CATL holds a 9.17% stake, ensuring a stable equity structure and ample backing from state-owned and industrial capital.

However, even strong shareholders cannot defy market cycles. Since September 2025, the new energy sector in the Hong Kong stock market has cooled comprehensively, with market capitalizations of leading players like NIO, XPeng, and Li Auto declining and valuations across the sector contracting significantly. Avatr’s second IPO at this juncture is unlikely to enjoy early benefits and faces considerable pressure on valuations and subscriptions.

Objectively speaking, Avatr exemplifies a company with extreme advantages and prominent shortcomings. Its core strength lies in industrial synergy: Changan’s manufacturing heritage, CATL’s battery supply chain, and Huawei’s intelligent driving technology have allowed it to bypass many of the early challenges faced by most new entrants. Combined with high-intensity research and development and channel deployment, it has a solid long-term foundation, and its products have gained market recognition.

However, the capital market now demands guaranteed profitability. Three consecutive years of significant losses, liquidity pressures, and high marketing and research and development expenses pose real challenges. With intensified competition in the high-end sector, including price wars and technological battles, Avatr faces considerable difficulty in achieving scalable profitability and breaking out of the cycle of losses.

Overall, this Hong Kong stock market IPO appears more like an opportunistic breakthrough and advance preparation. With top-tier resources and high-growth data, Avatr has the potential to navigate through cycles; however, losses, funding pressures, and a cooling market also make the path to listing fraught with uncertainty.

For investors, Avatr is a typical high-growth, high-investment, and high-uncertainty company. Whether it can continue to narrow losses, achieve operational profitability, and leverage the resources of the three giants to establish a differentiated advantage will determine its market performance after listing.

-

![]()

Laifen Seeks to Escape 'Budget Dyson' Label but Falls Short of Dyson's Prestige

-

![]()

Who is Holding Back the Development of Dexterous Hands?

-

![]()

How do Autonomous Driving Physical AI and End-to-End Systems Work Together?

-

![]()

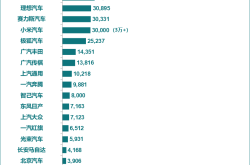

June's New Energy Vehicle Sales Rankings Unveiled! Leapmotor Surpasses Tesla in a Stunning Comeback, Marking the Start of the Automakers' Knockout Phase

-

![]()

Global Agents Embrace 'Loop Engineering': AI's Self-Sufficient Work, Supervision, and Revision

-

Post-90s Straight-A CEO Propels Jihao Technology Toward IPO, Despite Over 90% Revenue Reliance on Smartphones

-

AI 'Dissolves' Visual China's Copyright Moat—What Story Can It Tell to List in Hong Kong?

-

![]()

The AI Industry Chain: A Tale of Fire and Ice - Upstream Thrives, Downstream Struggles