Seres: Navigating Beyond the 'Realm'

07/15 2026

07/15 2026

504

504

Following Seres' projected half-year loss of 1.5 to 1.8 billion yuan, a chorus of voices has emerged, proclaiming, "Seres is on the brink of failure" or "Huawei has finally drained Seres' coffers."

While these statements are emotionally charged, they lack substantive new information.

Seres' fortunes are closely tied to AITO, which, in turn, leans heavily on Huawei. With the Harmony Intelligent Mobility Alliance expanding from a single brand to five, the technological, channel, and brand advantages that AITO once enjoyed are now being shared more widely. This issue has been discussed in the market for years, and Seres' stock price has reflected these concerns, fluctuating with each new development in its partnership with Huawei.

The question now looms: Where will Seres find its next turning point, and can it thrive beyond the shadow of AITO?

The outlook is not overly optimistic.

Seres' true independence lies beyond the current 'realm,' but its most immediate financial turning point may still be found within it. Yinwang's involvement transforms Seres from a mere participant to a shareholder in Huawei's automotive ecosystem, while AITO's overseas expansion opens up new markets for the brand. Meanwhile, AIVA represents a critical test of Seres' ability to manufacture high-quality vehicles without relying on Huawei's technological umbrella.

The first two avenues offer potential for financial improvement. However, only the last can truly serve as Seres' second growth engine.

It's premature to consider leaving the 'realm' just yet.

On the evening of July 12th, Seres announced a projected net loss attributable to shareholders of 1.5 to 1.8 billion yuan for the first half of 2026, with a loss after non-recurring items ranging from 2.2 to 2.5 billion yuan. Its core subsidiary, AITO Automotive, anticipates a loss of 1.05 to 1.3 billion yuan for the same period, with a quarterly loss of 1.9 to 2.15 billion yuan in the second quarter. The company attributed these losses to rising prices of memory chips, industrial metals, and lithium carbonate, as well as the decreased applicability of certain existing assets due to technological upgrades and model transitions, necessitating adjustments to their book values.

With the half-year report yet to be released, the breakdown between operational losses and asset impairments remains unclear. Calculating a 'loss per AITO vehicle sold' by dividing the total loss by sales volume at this stage would only yield a misleading figure, suitable for propaganda purposes only.

Nevertheless, market concerns are not entirely unfounded.

In 2025, Seres reported revenue of 165.05 billion yuan, net profit attributable to shareholders of 5.96 billion yuan, a gross margin of 28.8% for new energy vehicles, and net operating cash flow of 28.914 billion yuan. That was an impressive annual report. However, by the first quarter of 2026, while revenue still increased by 34.5% year-on-year, net profit after non-recurring items dropped to 103 million yuan, a 73.87% decrease; operating cash flow turned negative at 20.95 billion yuan. AITO Automotive's sudden projected loss of nearly 2 billion yuan in the second quarter dealt a significant blow to Seres' profit narrative of the past two years.

Previously, it was argued that rising AITO sales would absorb R&D, marketing, and factory investments through economies of scale. Now, despite selling 160,779 AITO vehicles in the first half, a 5.6% year-on-year increase, profits have plummeted.

Even if the M6, M9, or new M7 bring another sales surge, the market will question the costs involved in terms of new model investments, sales incentives, and impairments of old assets.

Moreover, this 5.6% growth occurred in a market where competitors have not stood still. In June, AITO sold 30,331 vehicles, a 30.19% year-on-year decrease; Li Auto delivered 30,895 vehicles the same month and plans to launch the new L6 in July; Xiaomi Auto has delivered over 30,000 vehicles for three consecutive months, with the YU7 becoming a new variable in the 200,000-300,000 yuan SUV market.

While public data cannot prove how many AITO orders were directly taken by competitors, it is clear that the M6 and M7 face not just one or two static rivals but a host of continuously evolving, capacity-expanding products.

Thus, a rebound in AITO's monthly sales merely signifies operational recovery. As long as Seres' revenue, profits, and valuation remain dominated by the same AITO model lineup, it remains trapped in its original problems.

But this does not mean Seres should immediately part ways with Huawei.

AITO remains Seres' only proven high-end brand and the largest contributor to Harmony Intelligent Mobility Alliance sales. Voluntarily severing cooperation now would be akin to sinking the first boat before the second is launched. A more realistic choice is to stay within the 'realm' while seeking to alter its position within it.

First, change positions within the 'realm.'

The expansion to five brands is often seen as bad news for Seres. Behind AITO stands Seres, while Luxeed, Enjoy Auto, MAEXRO, and UXEED are connected to Chery, BAIC, JAC, and SAIC, respectively. Huawei's technology and channels no longer serve AITO exclusively, as consumers entering the same Harmony Intelligent Mobility Alliance portal face a growing array of similarly priced options.

This assessment is not wrong but overlooks a card Seres holds.

Seres invested 11.5 billion yuan to acquire a 10% stake in Shenzhen Yinwang. With other shareholders joining, its stake stood at 9.36% by the end of 2025, accounted for as a long-term equity investment and not consolidated. The annual report's notes on long-term equity investments reveal that Seres recognized 170 million yuan in investment income from Yinwang under the equity method in 2025.

The net equity method investment income from all joint ventures and associates was 80.18 million yuan due to offsets from losses in other projects like Ruichi, not because Yinwang alone contributed only 80 million yuan. Yinwang is still far from transforming Seres' profit structure but is no longer just a story in valuation models.

Herein lies the intrigue.

The more brands in the Harmony Intelligent Mobility Alliance, the lower AITO's share within it; Huawei's intelligent automotive solutions will also cover more models and clients. In 2025, Huawei's intelligent automotive solutions business reported revenue of 45.018 billion yuan, a 72.1% year-on-year increase, with over 38 million intelligent automotive components shipped and partnerships with over 600 entities. According to Huawei's annual report, it was the fastest-growing business segment.

By expanding the Harmony Intelligent Mobility Alliance from AITO to five brands, Huawei reduces its reliance on a single automaker. Seres' stake in Yinwang represents an attempt to convert this dilution into another form of gain: while selling fewer AITO vehicles still means losing vehicle profits, more brands and automakers adopting Yinwang's intelligent automotive solutions offer Seres the chance to share in platform growth as a shareholder.

In other words, Seres previously stood primarily on the payment side of Huawei's automotive business; now, it has placed one foot on the revenue side for the first time. In 2025, Seres procured 22.335 billion yuan in goods and services from Yinwang while recognizing 170 million yuan in investment income from Yinwang. These figures are not under the same accounting standards and cannot be directly compared for a return rate, but together, they illustrate that this repositioning has just begun.

Yinwang is thus closest to impacting Seres' income statement. It already has revenue, clients, and products, avoiding the need to climb from zero like a new brand. However, its approximately 170 million yuan in profit or loss impact in 2025 remains small relative to Seres' 5.96 billion yuan in net profit attributable to shareholders. Investment income alone cannot fix AITO's vehicle gross margin, inventory, or operating cash flow issues.

More critically, this path does not reduce reliance on Huawei. Seres has merely shifted from 'relying on Huawei to sell cars' to 'simultaneously relying on Huawei's platform for profit.'

It has changed positions within the 'realm' but has not stepped outside.

The same applies to AITO's overseas expansion.

In February 2026, AITO signed with a UAE dealer, launching test drives for the overseas version of the M9, the AITO 9, and securing 200 initial orders. The company plans to enter the Middle East and Central Asia first, preparing for Europe, Asia-Pacific, and left- and right-hand drive models. AITO's entry into the UAE offers a relatively practical path to growth: instead of building a brand and product from scratch, it brings the proven AITO to another market.

This is not the same business as Seres' past overseas efforts. Early international sales relied mainly on Dongfeng Xiaokang microvans, commercial vehicles, and fuel-powered SUVs like the Fengguang 580, with approximately 26,000 vehicles exported in 2019. Lantech itself is more of a cost-effective new energy product line for the domestic market, not a direct precursor to AITO's overseas expansion. What AITO exports now are high-end products, brands, and intelligent experiences already validated domestically. The former relied more on channels and cost-effectiveness; the latter must reprove brand premium overseas.

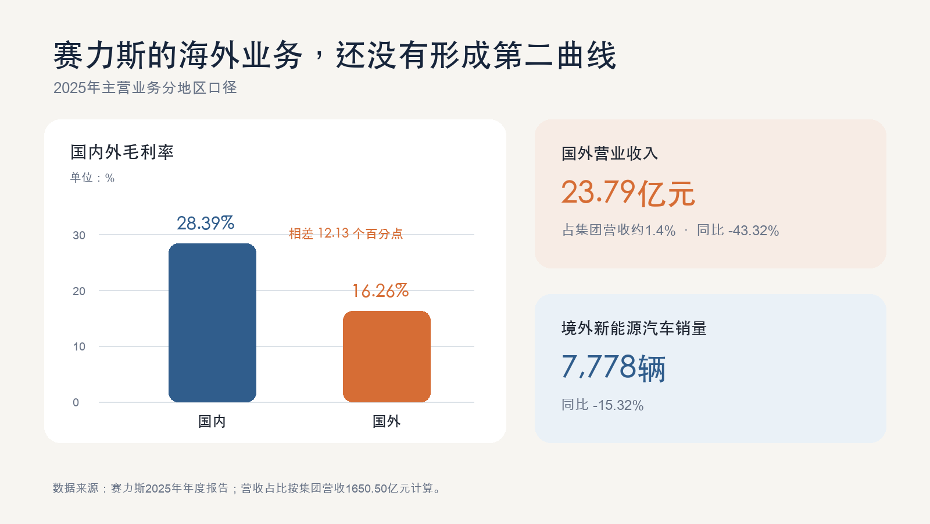

The reality gap remains significant. By region, Seres' foreign revenue was 2.379 billion yuan in 2025, accounting for about 1.4% of group revenue, a 43.32% year-on-year decrease; foreign business gross margin was 16.26%, 12.13 percentage points lower than domestic. Overseas new energy vehicle sales were only 7,778 units, a 15.32% year-on-year decrease. Seres' annual report does not depict an exploding curve but a business just restarting.

Exporting high-end vehicles is also harder than exporting affordable ones. Distribution networks, after-sales service, parts, data compliance, mapping, and advanced driving assistance capabilities must all be readapted. How much of Huawei's domestic edge can AITO retain overseas is a question it must answer.

Even if successful, this only expands AITO's market boundaries. Seres remains within the 'realm,' merely extending its reach.

AIVA is the real test.

In May, Chongqing Lantech Technology received a 6.671 billion yuan capital increase and was renamed Saido Technology. A Chongqing state-owned asset platform became the largest shareholder, with Seres' stake diluted to 32.96%. Employee platforms, CATL, Bojun Technology, and Starry Corporation joined as investors. After the capital increase, Seres lost control.

Zhang Zhengyuan, Chairman of Saido Technology

A month later, Saido unveiled AIVA, with its first mass-produced model, the ME7, set to debut within the year. Volcano Engine provides its Doubao large model and cockpit capabilities, while Seres contributes manufacturing, supply chain, quality systems, and engineering expertise. Public reports also indicate that AIVA's advanced driving assistance solution is from Yuanrong Qixing, not Huawei's Qiankun ADS.

This technological combination is crucial.

AIVA places Seres' automotive business outside Huawei's technological ecosystem for the first time: the cockpit comes from Volcano Engine, advanced driving assistance from Yuanrong Qixing, and manufacturing and engineering from Seres. While it cannot prove Seres has independent software capabilities, it tests a more fundamental question: How much value do Seres' accumulated manufacturing experiences retain outside Harmony Intelligent Mobility Alliance's product definitions, brands, and channels?

This deal may seem like a retreat but could represent Seres' most pragmatic second-curve design to date.

Lantech had not proven itself. Building another automotive brand requires factories, channels, technology, and billions in cash. If Seres continued to fully invest, pressure on AITO would drain cash from both lines. By reducing its stake to 32.96%, it shares risks with local state-owned assets, employees, CATL, and parts suppliers. If AIVA succeeds, Seres can benefit from equity appreciation, investment income, and manufacturing orders; if it fails, the losses are no longer entirely on Seres' books.

What Seres learns here may not be how to create another AITO but how to avoid paying for a second venture alone.

A non-Huawei route does not equate to immediate competitiveness. AIVA targets the 200,000-yuan-plus market, already crowded with the Li Auto L6, Xiaomi YU7, AITO M5, and M6; BYD is also continuously bringing advanced driving assistance to lower price points. For consumers, 'not using Huawei' is not a purchase reason, nor is 'having advanced intelligent driving.' AIVA must explain why the same money shouldn't go to a more established brand.

It faces another layer of awkwardness: even if this curve succeeds, it will not fully appear in Seres' listed company revenue. Having lost control, Seres cannot unilaterally decide on products, budgets, or dividends; Volcano Engine is merely a technology supplier without equity, and Doubao's user base does not automatically convert to car orders. From debut to mass delivery to profitability, AIVA faces several hurdles.

Robots are even further off. Seres has established Phoenix Technology, formed a joint venture with Beihang University called Saihang Embodied Intelligence, and signed an embodied intelligence cooperation framework with Volcano Engine; its annual report also lists intelligent robots as a long-term growth driver. However, only companies, agreements, and R&D directions are confirmed so far, with no verifiable mass products, orders, or revenue. Robots can fuel imagination but not yet serve as a turning point.

Seres' next financial improvement may come first from Yinwang; if AITO's overseas expansion succeeds, it will add a new market for AITO. Both are important but do not reduce Seres' reliance on Huawei's ecosystem.

AIVA faces a different test. It must prove that Seres' manufacturing, supply chain, and engineering capabilities remain in demand without Huawei. However, to lower failure costs, Seres voluntarily relinquished control. This makes AIVA more likely to survive but reduces what can return to Seres' listed company financials if it succeeds.

Hence, the emphasis should not rest exclusively on the sales volume of AITO vehicles in the coming month. The half-year report must first and foremost elucidate asset impairments and operational pressures. Whether the investment income from Yinwang can sustain its growth trajectory (continue to grow) will be pivotal in determining the significance of any repositioning efforts within the 'realm'. The transition of overseas business from 200 orders to consistent deliveries carries more weight than a solitary launch event.

To forge a genuinely independent path, the initial step is to ascertain whether the ME7 makes its debut as scheduled. Subsequently, it is crucial to evaluate whether AIVA can successfully establish distribution channels and acquire its inaugural genuine user base. Before engaging in discussions about turning points, robots must at least possess a verifiable product or a confirmed order.

AITO has been instrumental in keeping Seres afloat. The pressing question now is not whether Seres can promptly disentangle itself from AITO, but rather whether, while still operating within the 'realm', it has left open a viable avenue to the external market.

-

![]()

A Trillion Dollars Poured into AI: Only These Three Types of Companies Are Truly Profiting

-

![]()

Differentiation and Acceleration in Banking AI Implementation

-

![]()

Year’s First Half Sees Nearly 1.81 Million Vehicles Sold, with Exports Contributing Over 40%: How Will BYD Steer Through the Second Half Amidst a Price War?

-

![]()

Chuenergy’s Maiden ET Vehicle Rolls Off Line at SAIC-GM Wuhan South Plant, Poised to Rival AITO M5

-

![]()

StepOn’s AI Terminal: A Tale of Unveiled Potential

-

![]()

StepOn’s AI Terminal: Only Part of the Picture Unveiled

-

![]()

The Tale of Rapid Iteration: Even Elite Students in the Auto Industry Struggle to Keep Pace

-

![]()

Seventy Years On: From China’s First Car to a Pivotal Moment in Automotive Excellence