The Tale of Rapid Iteration: Even Elite Students in the Auto Industry Struggle to Keep Pace

07/15 2026

07/15 2026

386

386

Edited by Xiaowei

July 16th was destined to be a hectic day for China's automotive market, with six automakers choosing to unveil seven new models on the same day. The shortest interval between the latest model and its predecessor was a mere eight months and four days.

To put this into perspective, the average gap between launches of same-series models in China's smartphone market in 2025 was 10.3 months.

In stark contrast to the traditional 60-month development cycle for internal combustion engine vehicles, the development timeline for new energy vehicles in China has been condensed to just 18-24 months. In the first half of this year, 550 new models were introduced, with new energy vehicles taking center stage.

Under this 'Chinese speed,' even laid-back foreign companies find themselves 'perplexed yet impressed.' In July of this year, Ferrari's Global Marketing Director, Manuele Carando, likened Chinese automakers' product development strategies to those of fast-moving consumer goods in an interview. He noted that while the progress of Chinese vehicles in terms of performance and features is remarkable, the rapid iteration also renders older models obsolete quickly, making it challenging to foster long-term brand loyalty among drivers.

Ferrari, the venerable European automaker with annual earnings of 1.6 billion euros, can afford to discuss 'brand loyalty' at a leisurely pace.

However, for Chinese automakers still embroiled in a fierce struggle for survival, 'slowing down' would be a disastrous outcome, equating to voluntarily surrendering hard-earned market share to competitors who frequently introduce more cost-effective new models.

Previously, discussions about the costs of this speed race primarily focused on the consumer side. Existing owners lamented being 'betrayed' by automakers, as their newly purchased vehicles swiftly became 'outdated' models, suffering from depreciation.

Now, the financial burden is beginning to shift back to the automakers themselves.

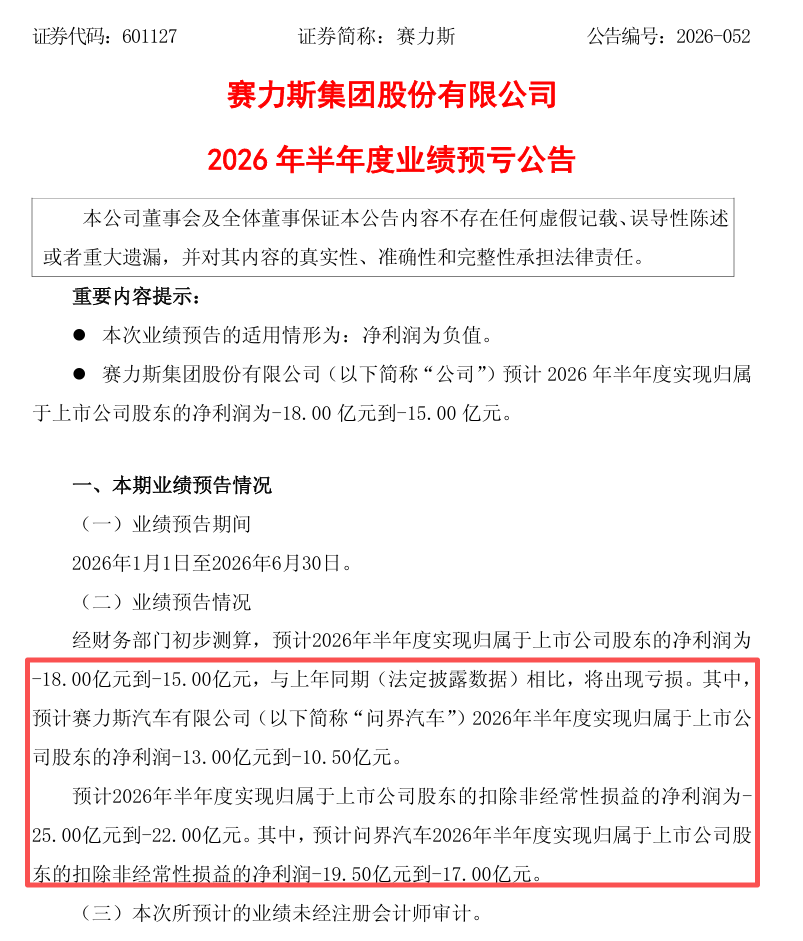

On July 12th, Seres issued a profit warning for the first half of 2026, projecting a net loss attributable to shareholders of 1.5 to 1.8 billion yuan. Among these, its core subsidiary, Aito Automobile, is expected to incur a loss of 1.05 to 1.3 billion yuan. In comparison, Seres' net profit attributable to shareholders in the first half of 2025 was still a robust 2.941 billion yuan.

▲Source: Shanghai Stock Exchange official website

Even industry leaders, high-end brands born with a silver spoon, boasting average prices of nearly 400,000 yuan and leading the industry in gross profit margins, are now beginning to feel the pinch from their past rapid expansion.

Curiously, these substantial losses coincide with sustained sales growth. In the first half of this year, Seres Automobile sold a cumulative 160,800 vehicles, up 5.6% year-on-year. Aito's cumulative deliveries during the same period grew by 10.2% year-on-year. If Aito's loss of 1.05 to 1.3 billion yuan is spread across its sales volume, it equates to a loss of approximately 6,500 to 8,100 yuan per vehicle.

It's crucial to note that Seres is not an automaker that relies on low margins to drive sales. In 2025, Seres' new energy vehicle business boasted a gross profit margin of 28.8%, with annual net profit attributable to shareholders nearing 6 billion yuan. Among independent new energy automakers, it ranks high in both profitability and average product price.

Thus, this shift from profit to loss is particularly noteworthy. In response, Seres officials provided two explanations:

Firstly, the challenging macroeconomic environment, with rising prices for key raw materials such as memory chips, industrial metals, and lithium carbonate, has increased production costs. Seres Chairman Zhang Xinghai stated that the average cost per Aito vehicle has risen by 15,000 to 20,000 yuan.

Amidst fierce price competition, automakers find it difficult to fully pass on these cost increases to consumers, ultimately squeezing their own profit margins.

Secondly, based on expectations of future asset returns, the book value of certain 'existing assets with limited adaptability due to technological iteration and model replacement' has been adjusted.

And this second point brings us back to the initial financial burden.

Launching a new model requires significant upfront investment from automakers, including R&D results, testing and validation, production equipment, molds, raw materials, and component inventories.

Under traditional automotive industry business models, these assets should gradually recover their costs over several years of production and sales.

However, the increasingly rapid market environment has disrupted this old cycle. As new technologies and model replacements become more frequent, even updating on a six-month basis, a mismatch begins to emerge between the lifespan of automakers' assets and their product lifespans.

Seres is not alone in facing this challenge. NIO CEO William Li directly stated in an April interview that 'the entire automotive industry is experiencing revenue growth without corresponding profit growth, largely due to the rapid iteration of new models.'

Assume a model was originally planned to sell for five years, with its matching technologies, equipment, and components amortized over that period. Once the product undergoes significant updates every two to three years or even sooner, future revenue from older technologies declines, specialized components lose their relevance, and some equipment and molds can no longer be fully utilized.

GAC Group's financial reports also corroborate this point. In 2025, it provisioned approximately 1.223 billion yuan for inventory impairments, about 1.246 billion yuan for intangible asset impairments, and combined with related impairments for fixed assets, totaling about 2.7 billion yuan. Among these, inventory impairments were mainly due to sluggish sales and inventory backlogs in the independent brand segment. Intangible asset impairments reflected the rapid obsolescence of internal combustion engine technology routes, causing quick depreciation of assets formed by past R&D investments.

▲GAC Honda's pure electric model P7 underperformed in sales after launch, with cumulative sales failing to reach 1,000 units three months after launch.

GAC Group acknowledged in its profit forecast response: 'Intangible asset impairments from 2023 to 2025 were provisioned at 856 million yuan, 1.19 billion yuan, and 1.21 billion yuan, respectively. The economic lifespan of historical technology assets has shortened due to the transition from internal combustion engines to electrification and intelligence, leading to a systematic decline in related asset values.'

Rapid model iteration means that investments originally expected to be recovered over five years may lose their revenue source by the third year. The impressive financial reports driven by strong sales start to shift from profit to loss at this moment.

But like other brands, even Aito has no room to slow down in China's highly competitive automotive market today.

Externally, intelligent driving, battery technology, and cabin experience remain key drivers for consumers to upgrade their vehicles. Competitors continuously introduce new technologies, and any automaker that lags may miss its product window.

Internally, Aito's benchmark position within the Harmony Intelligent Mobility ecosystem also requires it to be at the forefront of adopting new-generation technologies. As the number of collaborative brands and models under Harmony Intelligent Mobility grows, Aito must continuously integrate and be the first to implement the latest technologies within the ecosystem to maintain its high-end brand positioning established previously.

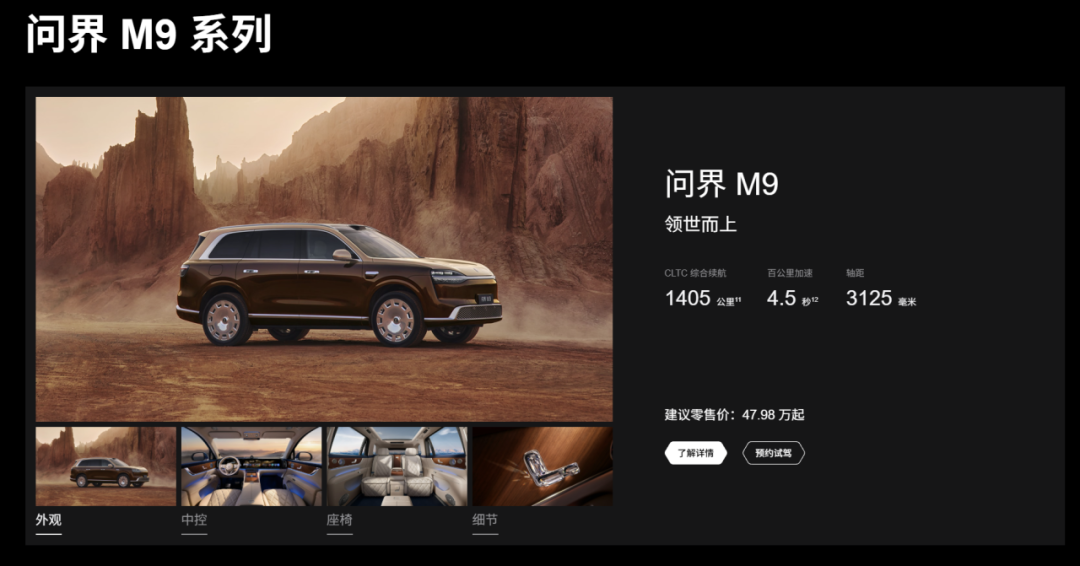

▲Aito M9 launched on May 27, 2026. Source: Brand official website

Thus, Aito continues to accelerate its iteration while attempting to appease existing owners left behind.

Over the past six months, Aito has undergone a wave of intensive product updates.

In March, Harmony Intelligent Mobility launched a new-generation 896-line dual-optical-path image-grade LiDAR, subsequently equipped on the refreshed Aito M9, M7, and M8 models.

In April, Aito introduced the all-new M6 model covering the 250,000 to 300,000 yuan market, offering both pure electric and extended-range versions.

In May, the Aito M9 was refreshed again, with updates extending from the body and cabin to the powertrain, chassis, and intelligent driving systems, incorporating over 140 new technologies and adopting an 800V high-voltage dual-silicon carbide power platform across the lineup.

Admittedly, these updates have strengthened Aito's product competitiveness. The M6 model surpassed 30,000 cumulative deliveries just 54 days after launch. The all-new Aito M9 also maintained high heat post-launch. For Aito, the frequent integration of Huawei's latest technologies has been a key reason for its brand ascent in recent years.

However, a technological leap at a new model launch translates into a long cost chain at the production end.

Industry insiders explained to us that even replacing a small forward-facing perception sensor may require readjusting the physical fit of the bumper and entire body structure, as well as recalibrating algorithms. If the intelligent driving system changes, it may also necessitate joint tuning of the powertrain, chassis, and electronic control systems, along with retesting.

On the other hand, model iterations do not always proceed according to automakers' plans. As William Li put it, 'When intelligent driving chips iterate, the vehicle must iterate; when battery technology advances, or lights and interiors iterate, the vehicle must iterate too.' No new energy vehicle consumer wants to buy a new model with core components a generation behind.

Ultimately, investments that cannot be carried over to new models from previous generations return to automakers' profit statements through inventory liquidation, asset impairments, and other means.

Compared to the first half of 2025, Seres' asset impairment losses were approximately 275 million yuan. By the end of 2025, this figure had increased to 1.579 billion yuan. Among these, intangible asset impairments were 759 million yuan, inventory write-downs were 655 million yuan, and fixed asset impairments were approximately 76 million yuan.

Of course, not all of these 1.579 billion yuan can be attributed to model replacements. But like GAC Group, Seres' annual report still emphasized that some molds and machinery equipment were impaired due to accelerated product upgrades and the discontinuation of certain models.

Currently, Seres has not disclosed which assets are involved in this book value adjustment or the amounts, with specifics to be clarified in the semi-annual report.

But one thing is certain: the automotive market, once a major beneficiary of rapid iteration, is now starting to pay the price for this model.

When rapid iteration shifts from a competitive tactic to an industry-wide default action, speed becomes a cost. Automakers lack the luxury to slow down, yet not all may have the capital to keep accelerating indefinitely.

-

Why Can''t AutoNavi Maps Excel in Local Services?

-

![]()

Cameras: A New Frontier in Smart Hardware at More Affordable Prices

-

Raising Nearly US$400 Million in Intensive Financing Over Six Months: Can This New Heavy Truck Player Pioneer a New Model for Autonomous Heavy Trucks?

-

![]()

Memory Chip Price Surge Imposes Heavy Burden on Smartphone Market, with Q2 Global Shipments Slumping to 13-Year Low

-

![]()

Tencent’s Acquisition of Manus: No Less Anxious Than Meta

-

![]()

Collective Failure of BBA, Only '56E' Holding On

-

![]()

Step's Apple Dream

-

![]()

The value of AI Coding is quietly shifting from 'whose model is stronger' to 'whose toolchain is denser'.