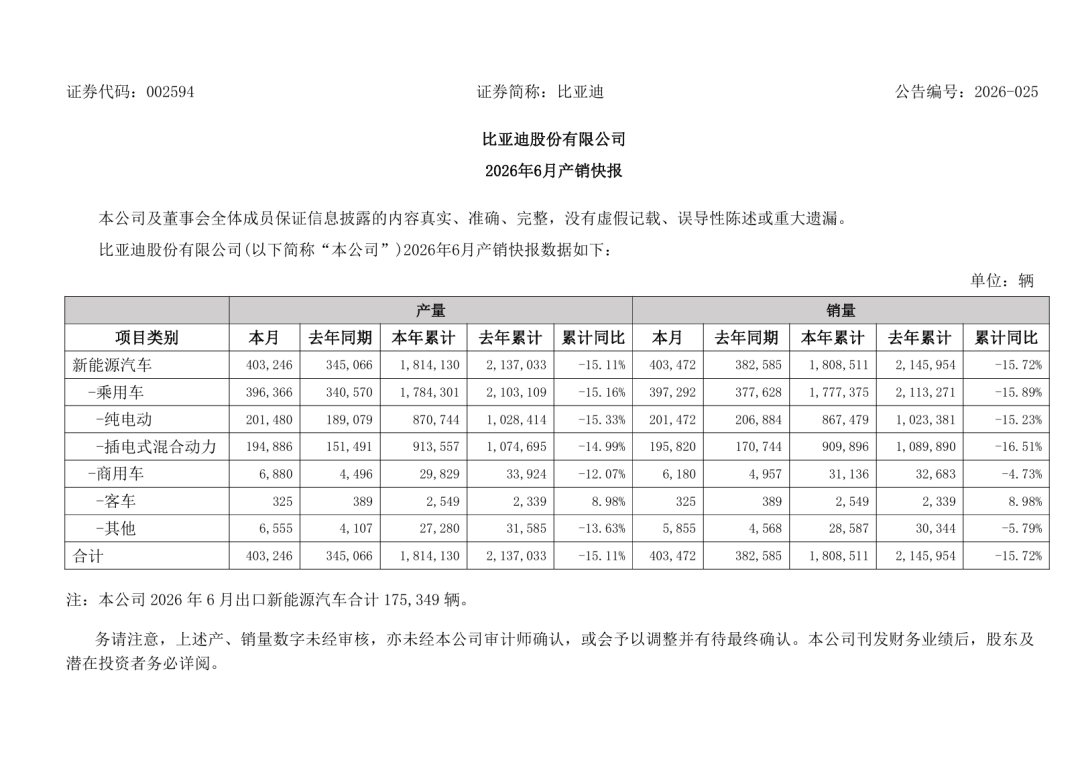

Year’s First Half Sees Nearly 1.81 Million Vehicles Sold, with Exports Contributing Over 40%: How Will BYD Steer Through the Second Half Amidst a Price War?

07/15 2026

07/15 2026

467

467

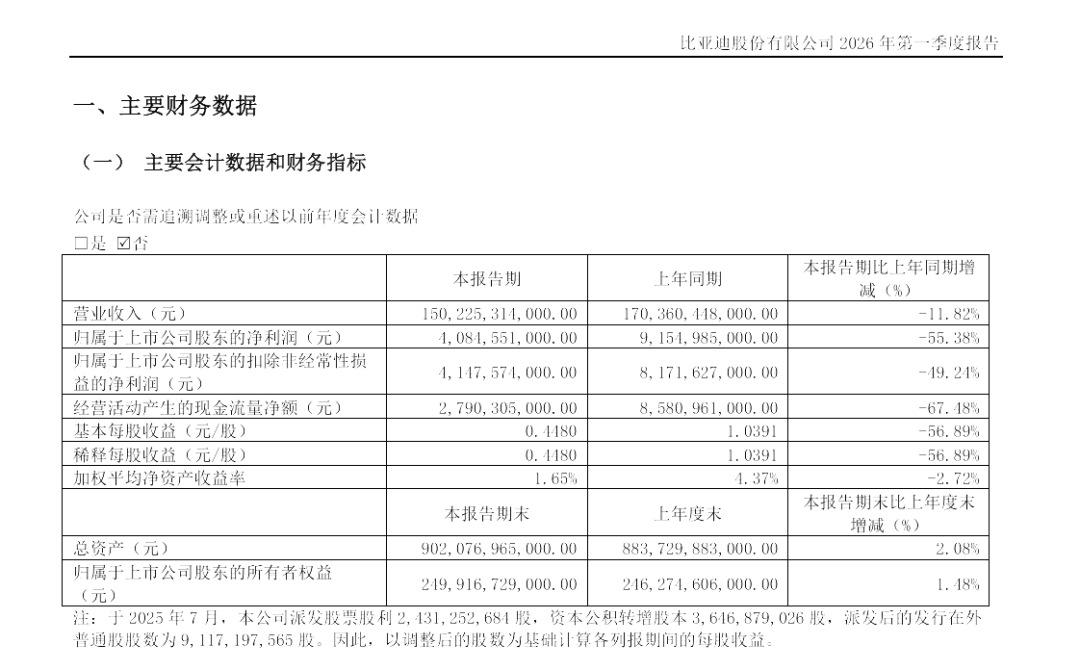

In early July, BYD released its production and sales report for the first half of the year as planned. Throughout this period, BYD's cumulative sales reached 1.808 million vehicles, marking a year-on-year decline of over 15%. Particularly noteworthy were the 700,000 vehicles sold and the 4 billion yuan profit recorded in the first quarter, both of which raised concerns.

The true driving force behind this performance lies in BYD's overseas business. Exports and locally produced vehicles overseas totaled nearly 790,000 units in the first half, accounting for 43.6% of total sales. Analysts point out that BYD's ability to wage a price war in the domestic market is largely underpinned by its strong performance in overseas markets. With pressure mounting on the domestic front and explosive growth overseas, this dynamic largely shapes BYD's strategic direction for the second half of the year.

Some industry insiders have voiced concerns, stating that as long as overseas profits can continue to offset the profit gap caused by low domestic gross margins, the strategy remains viable. However, the real risk lies not in whether a price war can be sustained now, but in whether, once overseas profits account for too high a proportion, BYD will evolve into a global automaker or become an unstable intermediary relying heavily on overseas markets to prop up its domestic operations.

Domestic Market: Lingering Aftereffects of the Price War, but the Worst is Over

The pressure in the domestic market stems from a price war that has persisted for nearly two years.

Last year, BYD took the lead in lowering prices, with the Qin PLUS DM-i dropping from 99,800 yuan to 79,800 yuan, and the entire 100,000 to 200,000 yuan price range experiencing repeated compressions. Entering 2026, the intensity of across-the-board price cuts has indeed diminished. Data from the China Passenger Car Association reveals that only seven models announced price reductions nationwide in June, with an average price drop of about 20% for new energy vehicles in the first half of the year. Most adjustments were made through configuration upgrades or clearance of older models, rather than direct price cuts for the same configurations. However, consumers have developed a "wait-and-see" mentality, leading to hesitant purchasing decisions and slow order conversion, resulting in a 30% year-on-year drop in domestic sales in the first quarter.

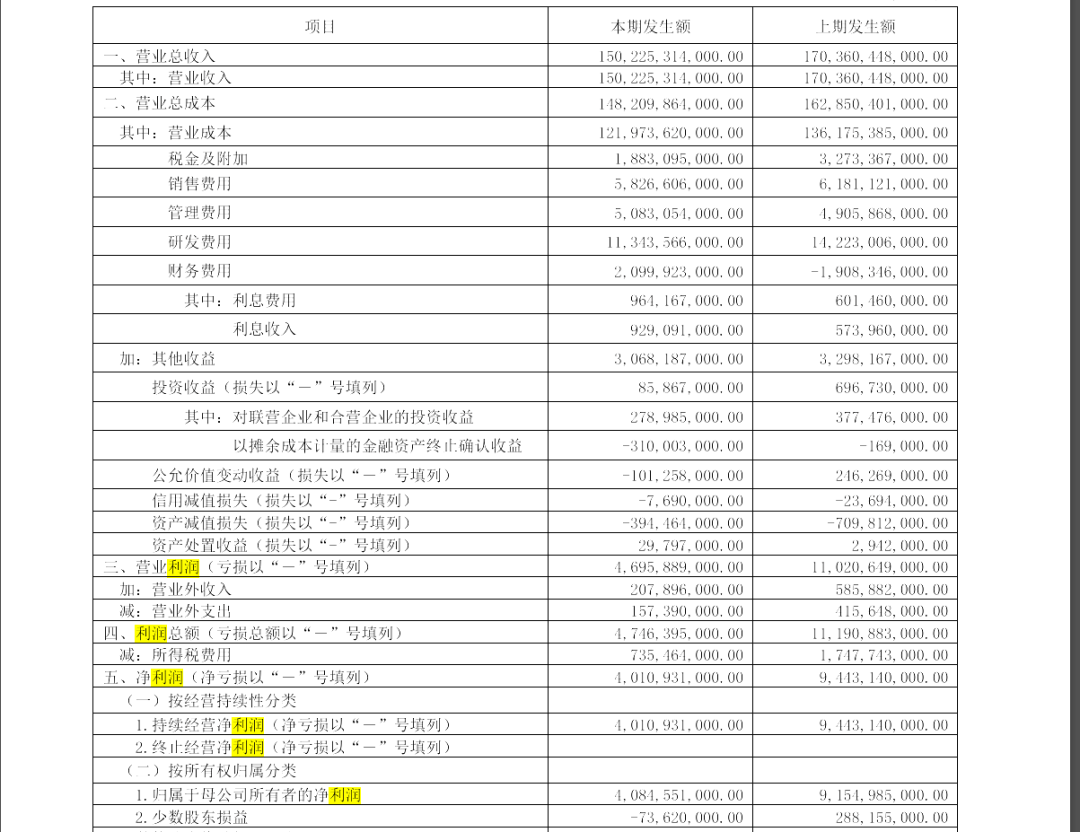

This pressure is directly reflected in the financial statements, with a first-quarter net profit attributable to shareholders of 4.085 billion yuan, a year-on-year decline of 55%. Based on reported figures, the per-vehicle profit was just over 5,800 yuan. However, an often-overlooked factor is that financial expenses for the period were as high as 2.1 billion yuan, primarily due to exchange losses, compared to nearly 1.9 billion yuan in exchange gains in the same period last year. The difference amounts to nearly 4 billion yuan.

Excluding these exchange losses, the per-vehicle profit from the core business is approximately 8,800 yuan, roughly in line with last year's full-year level. In other words, BYD's core vehicle manufacturing business has not collapsed; it is simply being heavily impacted by exchange rates. Entering the second quarter, the situation began to improve marginally. Sales reached 310,000 units in April, 330,000 in May, and surpassed 400,000 in June, with capacity utilization recovering month by month and fixed costs being continuously diluted. The RMB exchange rate also stabilized significantly compared to the first quarter. When the semi-annual report is officially released in August, it is highly likely that a sequential improvement in core business profitability will be evident.

Of course, it is unrealistic to expect per-vehicle profits to return to above 9,000 yuan, given the rigid increase in hardware costs due to the standard inclusion of the "Divine Vision" intelligent driving system across all models. However, overall, the bottom of the domestic market has likely been identified, and the task for the second half of the year is not to continue cutting prices to boost sales but to stabilize the core business and optimize the product mix.

Overseas Markets: From "Icing on the Cake" to "Core Pillar"

If the domestic market is about stemming the bleeding, then the overseas market is about generating blood. Overseas sales reached 789,000 units in the first half of the year, accounting for 43.6% of the total, up from just over 20% last year. More importantly, the profit structure of overseas business is entirely different—the average selling price per vehicle in the domestic market is about 130,000 yuan, while it can reach around 190,000 yuan overseas. Industry estimates suggest that per-vehicle net profit is two to three times higher overseas than domestically. When domestic price wars push profits to near rock-bottom levels, overseas markets become BYD's thickest safety cushion.

Currently, two complete vehicle factories are in operation: the Rayong factory in Thailand, which started production in July last year with an annual capacity of 150,000 units, primarily serving Southeast Asia; and the Camacari factory in Brazil, which came online in March this year, also with an annual capacity of 150,000 units, targeting the South American market. A factory in Uzbekistan is also operational. Factories under construction or planned include one in Hungary (expected to start production by the end of this year with an annual capacity of 150,000 to 200,000 units), one in Turkey (planned to start production this year), and one in Indonesia, with a total long-term capacity plan exceeding 2 million units. However, it should be noted that the vast majority of the nearly 170,000 overseas sales each month are still complete vehicles shipped from domestic ports, and it will take time for localized production to significantly contribute to sales and profits. The situation in the European market is slightly more complex, as anti-subsidy tariffs currently impose a 17.4% tax rate on exports to Europe, creating significant cost pressure.

A sales network covering 110 countries and regions has brought right-hand-drive versions of models like the Dolphin, Seal, and Yuan PLUS onto roads across various continents. On paper, BYD's overseas profits serve as the most critical buffer against the domestic price war, but "buffering" does not equal "underwriting." In the first quarter, incremental overseas profits were approximately 6.6 billion yuan, while the combined impact of domestic sales declines and exchange losses exceeded 7 billion yuan, resulting in a rough break-even. For BYD's financial foundation to truly stabilize, overseas support is only one aspect; the domestic market must first stop the bleeding.

High-End and Intelligent: Two Legs Moving Forward, but Neither at the Starting Line Yet

Beyond the fiercely competitive 100,000 to 200,000 yuan price range, BYD is building two additional growth drivers: a high-end brand matrix and standardized intelligent features.

In the high-end segment, June's data is highly representative: Fang Cheng Bao sold 35,600 units, a year-on-year increase of nearly 190%, with an average transaction price exceeding 220,000 yuan; Denza's monthly sales surpassed 20,000 units for the first time, reaching 20,352 units, and it has already expanded overseas channels in Thailand, Indonesia, and Malaysia, with a European launch event held at the Paris Opera House in April. Yangwang, while smaller in volume, has established a foothold in the ultra-luxury market with over 400 monthly deliveries in the million-yuan-plus segment. Overall, the proportion of sales for models priced above 200,000 yuan has increased from 14% the year before last and about 15% last year to 19% in the first half of this year.

The per-vehicle profit for high-end models is more than five times that of entry-level models. The slower this proportion grows, the harder it is to digest the pressure from the domestic price war. Conversely, if it can surpass 20% in the second half of the year, there will be a visible improvement in the profit structure. In the first quarter of this year, BYD announced the standard inclusion of the "Divine Vision" high-level intelligent driving system across all models, transforming features that previously required an additional 10,000 to 20,000 yuan into standard equipment. In the short term, this directly increases per-vehicle hardware costs, negatively impacting profits; however, in the long term, it represents a strategic trade-off—when the entire industry is competing on cost control in the 100,000 to 200,000 yuan price range, whoever offers a better intelligent driving experience will gain pricing power in the next round of competition.

Currently, this system is equipped on mainstream models in the Wangchao and Ocean series, and market feedback is accumulating, but it will take time for it to become a significant purchasing driver. After all, intelligent driving is something users must experience and compare before it becomes a reason to repurchase. Of these two growth drivers, high-end models are more pragmatic, with Fang Cheng Bao and Denza already contributing visible sales and profits; intelligent features are more like a long-term investment for the next two to three years, with only costs visible for now and returns still far off. Nonetheless, BYD is already attempting to break away from the old path of relying solely on high-volume models, representing the most noteworthy structural change in the second half of the price war. The most critical observation window in the second half of the year is the semi-annual report in August. Everyone will be focusing not on sales volume itself but on a more fundamental indicator: whether the proportion of overseas profits has exceeded 50%.

If this threshold is crossed, BYD's valuation logic will need to be rewritten—it will no longer be an automaker dragged down by the domestic price war but a truly global automotive group. If high-end models continue to climb, the profit structure in the semi-annual report will also look more favorable. As for the cost pressure from standardized intelligent features, that is a necessary tuition fee for the next stage of competition. Of course, the challenges are equally real. Whether the Hungarian factory can start production smoothly by the end of the year, how the shadow of European anti-subsidy tariffs will dissipate, and whether domestic consumers' acceptance of intelligent driving can quickly increase—none of these questions have definitive answers yet. But one thing is already clear: when over 40% of an automaker's sales come from overseas, the key to its success or failure no longer lies in domestic pricing itself. The sales decline and profit pressure in the first half of the year seem more like a phased cost paid for this transition. Whether this price is worth it will become clear in the second half of the year.

Yi's Commentary: The core contradiction in this performance report boils down to one thing: the domestic market is bleeding while the overseas market is replenishing blood. The question is how fast and how long these two legs can run. No matter how fierce the domestic price war is, the core business must not be lost; no matter how thick the overseas profits are, they cannot become a single point of dependence. The key metric to watch in the August semi-annual report is not sales volume but whether the proportion of overseas profits has exceeded 50%—if it has, the valuation logic will be rewritten; if not, the pressure in the second half of the year will be no less than in the first half. The directions of high-end and intelligent models are both correct, but neither has reached the point of truly contributing profits yet. BYD's real test has never been on the surface of the financial statements but within its structural foundations.

-

Why Can''t AutoNavi Maps Excel in Local Services?

-

![]()

Cameras: A New Frontier in Smart Hardware at More Affordable Prices

-

Raising Nearly US$400 Million in Intensive Financing Over Six Months: Can This New Heavy Truck Player Pioneer a New Model for Autonomous Heavy Trucks?

-

![]()

Memory Chip Price Surge Imposes Heavy Burden on Smartphone Market, with Q2 Global Shipments Slumping to 13-Year Low

-

![]()

Tencent’s Acquisition of Manus: No Less Anxious Than Meta

-

![]()

Collective Failure of BBA, Only '56E' Holding On

-

![]()

Step's Apple Dream

-

![]()

The value of AI Coding is quietly shifting from 'whose model is stronger' to 'whose toolchain is denser'.