Collective Failure of BBA, Only '56E' Holding On

07/15 2026

07/15 2026

432

432

「 Dramatic Changes in the Luxury Car Market: From Blind Trust to Avoiding BBA 」

Author | Zhen Yao

Editor | Li Guozheng

Produced by | Bangning Studio (gbngzs)

“BBA is no longer cutting it. The market has completely collapsed. Prices can't hold up.” Whenever Kang Fu, the sales manager at a LeStar Mercedes-Benz store in Beijing, comes across such content, he always feels compelled to share his honest thoughts.

Having been in the industry for many years, he has never experienced such dramatic price fluctuations—prices for the entire BBA lineup have generally dropped by 30,000 to 40,000 yuan. The trend remained stable in February and March this year, and the market barely held up in April. “Starting from May, prices began to drop significantly. To be honest, even after all these years in the car business, I can't make sense of this,” he admitted.

The terminal prices are continuously breaking through his psychological defenses.

He cited the Mercedes-Benz E-Class, a benchmark for mid-to-large sedans, as experiencing the most rapid decline. In March, discounts were still in the 70,000 to 80,000 yuan range, but “now it's a direct drop of 110,000 yuan,” with loan-financed luxury models landing at around 380,000 yuan.

“We used to rely on the GLC to hold the fort, but now it's all about the E-Class,” Kang Fu said. Eighty percent of buyers are upgrading or replacing their vehicles, with budgets capped at 400,000 yuan, no longer considering SUVs.

This trend is not limited to Mercedes-Benz; nearby BMW and Audi 4S stores are experiencing the same.

In previous years, the Mercedes-Benz GLC, BMW X3, and Audi Q5L were the sales mainstays for each store. Now, the prices of these three mid-size SUVs continue to drop, and the primary sales focus has shifted entirely to the “56E” lineup—comprising the BMW 5 Series, Audi A6L, and Mercedes-Benz E-Class—which now supports the majority of dealership revenue.

Sales rankings also reflect this market upheaval. In the first half of 2026, the GLC, X3, and Q5L all fell out of the top five in mid-size SUV retail sales, with their rankings steadily declining.

In the large SUV segment, BBA has virtually disappeared, replaced by a lineup of Chinese domestic new energy brands. The industry influence accumulated over decades in the era of large-displacement fuel vehicles is now nearly wiped out.

Even when considering the mainstream B-class luxury sedan market, the luxury trio of the Audi A4L, BMW 3 Series, and Mercedes-Benz C-Class has lost its luster, with sales shrinking monthly and no longer being the top choices for family upgrades or first-time young buyers.

There is no dramatic collapse, only a continuous decline in rankings and shrinking market share, silently confirming the collapse of the traditional fuel-powered luxury car order. Under the impact of the electric vehicle wave, BBA is left with only the 56E mid-to-large sedans holding the line, maintaining the last vestiges of traditional luxury car dignity.

▍01 Can They Still Justify a 400,000 Yuan Premium?

Five years ago, there was an unspoken rule among the domestic middle class regarding car purchases: for prestige, the 56E was the must-choose option.

At that time, these three models firmly maintained a starting price of 400,000 yuan. During the golden age of fuel vehicles, BBA held absolute pricing power: dealership markups, waiting lists for orders, and consumers willingly paying the price. A 56E was seen as a passport to middle-class status.

Is this still the case today?

Recently, Bangning Studio visited frontline 4S stores and conducted cross-city online price inquiries, discovering that the terminal transaction prices of the 56E have collectively hit historic lows. The main selling models generally land between 300,000 and 450,000 yuan, with the once-solid luxury moat now breached.

The first to break through the price bottom line (bottom line) was the Audi A6L. For certain models, many 4S stores across the country are currently offering maximum discounts (including government subsidies, store discounts, trade-in offers, direct price reductions, and financing deals) exceeding 170,000 yuan.

Shanghai is one of the price troughs in the national auto market, with even more aggressive discounts. At some stores, the full-cash price for the entry-level A6L 40TFSI has dropped to 268,000 to 280,000 yuan, and with manufacturer trade-in subsidies, the lowest price can reach 255,000 yuan. The volume-focused 45TFSI front-wheel-drive version has a bare car transaction threshold of just 285,000 yuan.

Price inversions are no longer an industry exception but a store norm. “Now, the first question customers ask when they enter the store is about trade-ins. Without discussing trade-ins, we basically can't retain customer traffic,” said a sales manager at an Audi 4S store in Shanghai.

The Mercedes-Benz E-Class, with its luxury brand halo, has also failed to hold the psychological defenses of consumers.

The E260L Classic has a manufacturer's suggested retail price of 378,800 yuan, but with trade-in subsidies and various other discounts, the full-cash bare car price has dropped to 276,800 to 287,000 yuan. In cities with looser financing policies, the bare car price has even dipped to 265,000 yuan.

On social media, the phrase “budgeting for a Mercedes-Benz C-Class but upgrading to an E-Class” has become a popular meme. Behind the humor lies the rapid shrinkage of Mercedes-Benz's brand premium accumulated over the years.

“In the past, the E-Class was the cornerstone of Mercedes-Benz's passenger car profitability; now, it can only rely on price cuts to compete for consumers who originally aimed for the C-Class,” lamented a frontline Mercedes-Benz sales manager. Consumers are shedding their brand logo worship, with few willing to pay extra for the allure of the three-pointed star.

Now, let's look at BMW. The entry-level 5 Series has seen its starting price drop to 368,000 yuan, and with dealer discounts and various subsidies, the terminal bare car price has reached 260,000 yuan.

The 2026 525Li entry-level model lands between 286,000 and 325,200 yuan; the volume-selling 530Li leading version stabilizes between 350,000 and 370,000 yuan.

“Previously, the brand deliberately tried to stabilize the price system, but seeing Audi and Mercedes-Benz continuously cutting prices, we ultimately had to follow passively,” said a BMW sales manager in Beijing's Chaoyang District. “Not cutting prices means no customer traffic, but cutting prices means losses per unit. It's a dilemma.”

Currently, the landing prices of the main 56E models highly overlap, forming a new price band: 300,000 yuan.

However, it's not just traditional fuel-powered luxury cars occupying this price range.

A host of domestic mid-to-large new energy sedans, including the Xiaomi SU7, Denza Z9GT EV, Xiangjie S9T, Zeekr 001, Avatr 12, and Shangjie Z7, are all targeting this market segment, diverting a significant portion of the core business and family customer base.

This is the core issue behind the collective decline of the 56E: intense competition within the existing market and new energy vehicles capturing incremental demand.

Their price cuts have barely managed to secure some sales. Since 2026, none of the 56E models have achieved monthly sales exceeding 10,000 units, representing a significant decline compared to their peak fuel vehicle era.

On July 13, 2026, Xiaomi Auto officially announced that in the sedan market above 200,000 yuan (across all energy types), the Xiaomi SU7 claimed the top sales spot in June. Simultaneously, in the pure electric sedan market above 200,000 yuan, the SU7 secured the first-half 2026 sales championship.

“The new-generation SU7: Sales Champion,” Xiaomi founder, chairman, and CEO Lei Jun reposted on social media.

The Xiaomi SU7 delivered 80,500 units in the first half of the year, leading by a wide margin.

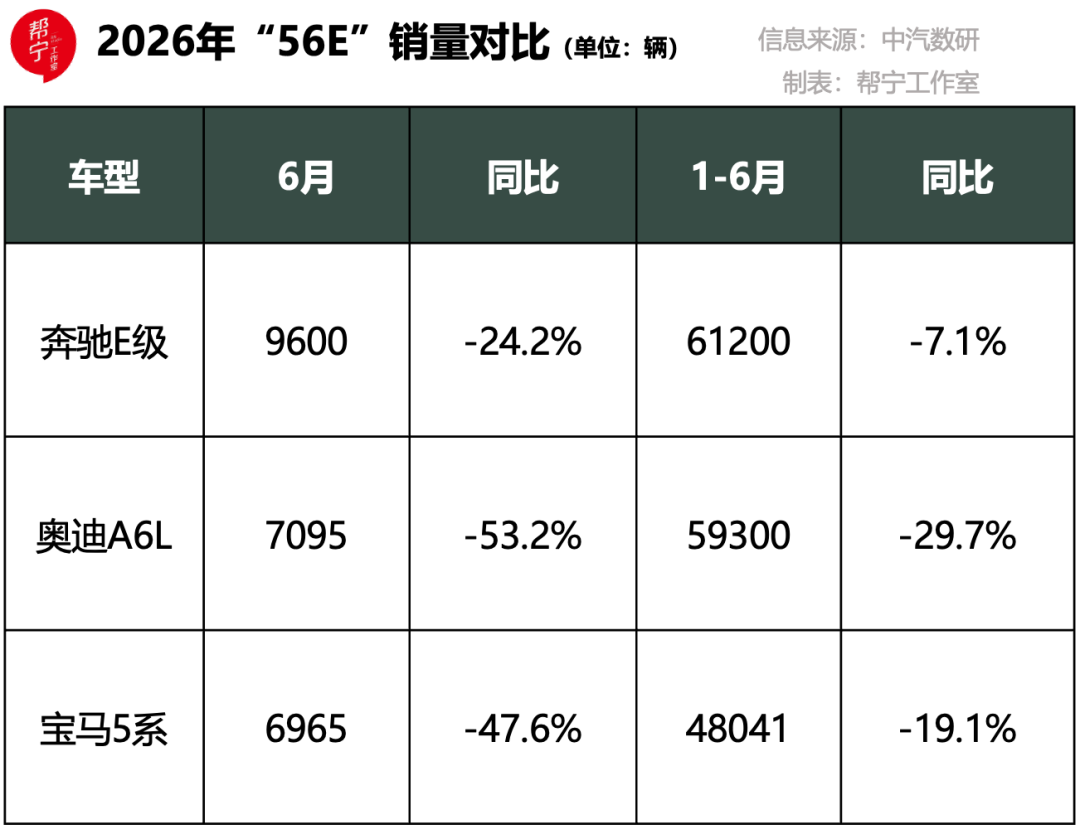

In comparison, the Mercedes-Benz E-Class sold 61,200 units in the first half of the year, down 7.1% year-on-year; the Audi A6L sold 59,300 units, a sharp 29.7% decline, falling from the segment leader to third place; and the BMW 5 Series sold only 48,000 units, down 19.1% year-on-year.

▍02 The High-End Mindset Has Found a New Owner

The precipitous decline in the overall fuel vehicle market has amplified all crises facing BBA.

Data from the China Passenger Car Association shows a 39% year-on-year drop in fuel vehicle retail sales in June, with domestic brands, mainstream joint ventures, and luxury brands all experiencing a 39% decline, as they were all indiscriminately hit by the sharp rise in fuel prices.

In June, luxury car retail sales reached 170,000 units, down 30% year-on-year. With luxury car prices reasonably returning to normal, the retail market share for luxury brands stood at 10.3% in June, down 1.1 percentage points year-on-year.

This marks the third consecutive month of over 30% declines in fuel vehicle sales, with the industry share falling below 40%. The most striking signal is that not a single fuel vehicle appeared in the top ten passenger car sales list for May.

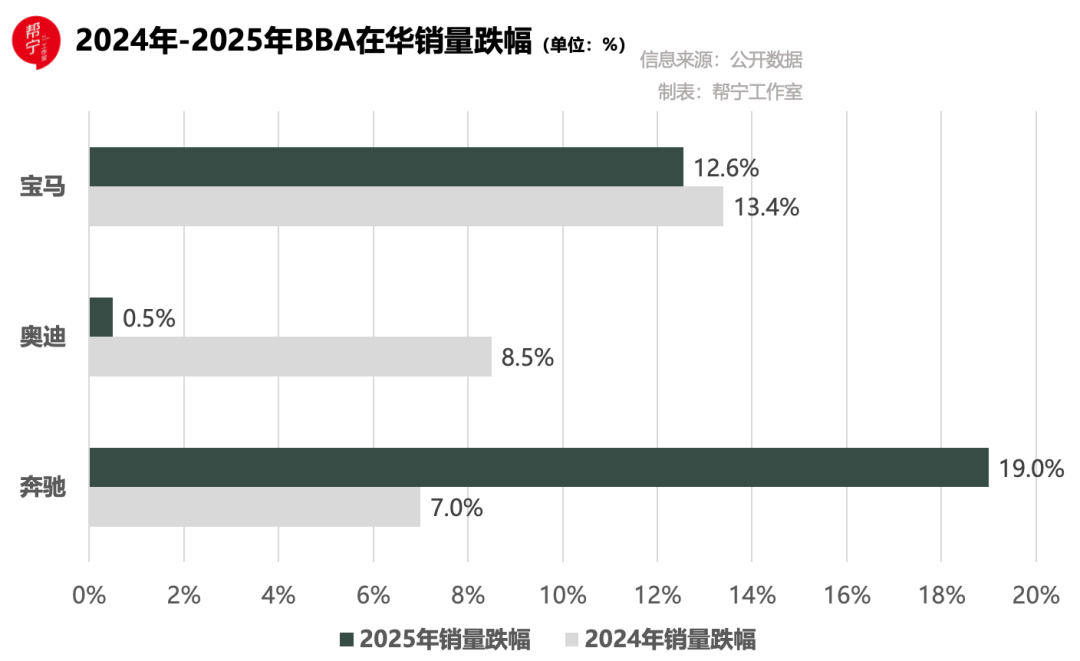

In fact, signs of decline were evident earlier. In 2024, BBA's sales in the Chinese market collectively turned downward: Mercedes-Benz fell 7%, Audi dropped 8.5%, and BMW's decline reached 13.4%. In 2025, the downturn worsened, with Mercedes-Benz's decline expanding to 19%, BMW dropping 12.55%, and Audi barely stabilizing with a slight decline thanks to significant terminal price cuts.

The outside world has long been curious: Where have all the lost BBA owners gone?

User intention data from Yiche Research Institute shows that in 2025, the proportion of intended repeat buyers from BBA for the four brands Seres, Li Auto, Tesla, and Xiaomi reached 36.81%, 27.22%, 24.21%, and 19.15%, respectively. A significant number of high-end existing users directly migrated from the German luxury camp to domestic high-end new energy brands.

This shift is most pronounced in the SUV segment.

The Mercedes-Benz GLC, once dominant in the mid-size luxury SUV segment, sold 52,537 units in the past six months, ranking seventh; the Audi Q5L sold 51,363 units, placing eighth; and the BMW X3 sold only 39,920 units, falling to tenth place. These three veteran luxury SUVs have been outpaced by domestic extended-range and pure electric models.

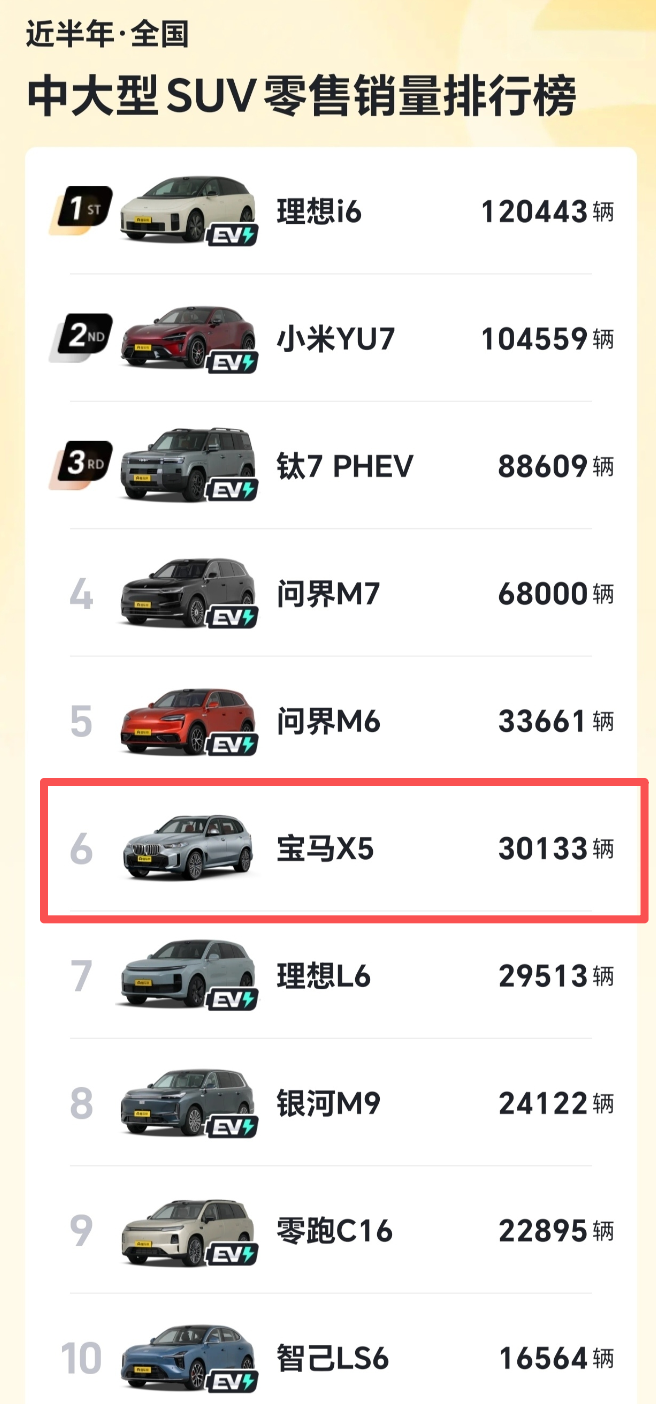

The situation is even more dire in the mid-to-large SUV segment. Only the BMW X5 remains barely holding on, with 30,133 units sold in the first half of the year, ranking sixth. The top five spots are all occupied by domestic brands, including the Xiaomi YU7, Li Auto i6, Titan 7 PHEV, Seres M7, and Li Auto L6.

“More than half of the long-time X5 customers who were considering replacements have now gone to test-drive Li Auto and Seres models,” said a BMW store sales manager helplessly (helplessly).

In the top-tier large SUV segment, BBA has completely exited the sales leaderboard, with NIO ES8, Zeekr 9X, Seres M9, and Li Auto L9 dividing up the entire mainstream market.

“In the home flagship SUV market, consumers now default to new energy vehicles as the mainstream choice, with traditional fuel-powered large SUVs seeing continuously shrinking market demand,” said an industry insider.

Peeling back the layers of sales figures reveals that the essence of BBA's continuous decline is the loss of the luxury definition rights.

For decades, German brands built a high wall around luxury perceptions based on engine, transmission, and chassis mechanical qualities, monopolizing what luxury meant to consumers. Today, electrification and intelligence are reshaping consumer standards, with transmissions and large displacements no longer being selling points, while infotainment systems, intelligent driving, and cabin texture becoming the new benchmarks.

The advantages BBA accumulated over half a lifetime have become obsolete overnight.

On one side, BBA is depleting its brand equity with price cuts, seeing its residual value decline year after year; on the other, domestic new energy brands are steadily refining their products, gradually reshaping the local perception of luxury.

As one declines and the other rises, the automotive market landscape has transformed.",

-

Why Can''t AutoNavi Maps Excel in Local Services?

-

![]()

Cameras: A New Frontier in Smart Hardware at More Affordable Prices

-

Raising Nearly US$400 Million in Intensive Financing Over Six Months: Can This New Heavy Truck Player Pioneer a New Model for Autonomous Heavy Trucks?

-

![]()

Memory Chip Price Surge Imposes Heavy Burden on Smartphone Market, with Q2 Global Shipments Slumping to 13-Year Low

-

![]()

Tencent’s Acquisition of Manus: No Less Anxious Than Meta

-

![]()

Collective Failure of BBA, Only '56E' Holding On

-

![]()

Step's Apple Dream

-

![]()

The value of AI Coding is quietly shifting from 'whose model is stronger' to 'whose toolchain is denser'.