"The 'Seven Sisters' Market Cap Erased Over RMB 3.6 Trillion Overnight: Who's Behind the Carnage?

03/31 2025

03/31 2025

579

579

Reviewing the week's car stocks and analyzing the dynamics of the automotive market.

Let's start with US stocks. On the final trading day of the week, amid the looming threat of 'Trump tariffs' and mounting data indicating a collapse in US consumer confidence, all three major US stock indices suffered substantial losses.

At the close, the S&P 500 index fell 1.97% to 5,580.94 points; the Nasdaq Composite index declined 2.7% to 17,322.99 points; and the Dow Jones Industrial Average dropped 1.69% to 41,583.9 points.

Nasdaq bore the brunt of the decline due to the collective slide of the US tech 'Seven Sisters' (Apple, Microsoft, Nvidia, Google, Amazon, Meta, and Tesla).

Specifically, Apple lost 2.66%, Microsoft fell 3.02%, Amazon dipped 4.29%, Nvidia declined 1.58%, Google-A tumbled 4.88%, Tesla dropped 3.51%, Meta shed 4.29%, AMD declined 3.22%, and Intel fell 3.85%. Even CoreWeave, the heavily indebted data center star stock and Nvidia's 'offspring,' barely managed to close flat on its first trading day after lowering its IPO price, opening below its IPO price.

American investment bank Goldman Sachs also revised down its forecast for US first-quarter GDP by 0.4 percentage points to 0.6% due to 'weak data'.

Clearly, Trump has emerged as the 'biggest thorn' in the side of the US stock market and economy. Since his election, the S&P 500 index has lagged behind European indices, with the German DAX index surging by approximately 14%.

Just last week, the market was still hopeful that the impact of tariffs might not be as severe. However, the abrupt imposition of car tariffs on Wednesday starkly demonstrated that Trump's deliberate policy of undermining the global trade order is inevitable in its repercussions on the US and even the global economy.

Regarding Trump's next round of provocations against global trading partners next week, analysts hold widely divergent views. Some believe that next week will mark the peak of Trump's tariff policy announcements, advocating a strategy of 'selling on rumors and buying on news.' Others, however, argue that Trump's policies are notoriously unpredictable and caution should prevail until clear positive signals emerge.

Alex King, CEO of research firm Cestrian Capital Research, stated: 'The first quarter of 2025 has dealt a harsh blow to anyone anticipating a continuation of the easy gains witnessed in 2023 and 2024. On the surface, it may seem like a mere correction, but the issue is that all US stock indices have fallen below their 200-day moving averages, which alone could serve as a simple risk-aversion signal for algorithmic investors.'

It's noteworthy that for the White House, which aims to reduce the deficit, Trump's announcement of new tariff policies targeting the automotive industry as a key focus is not surprising.

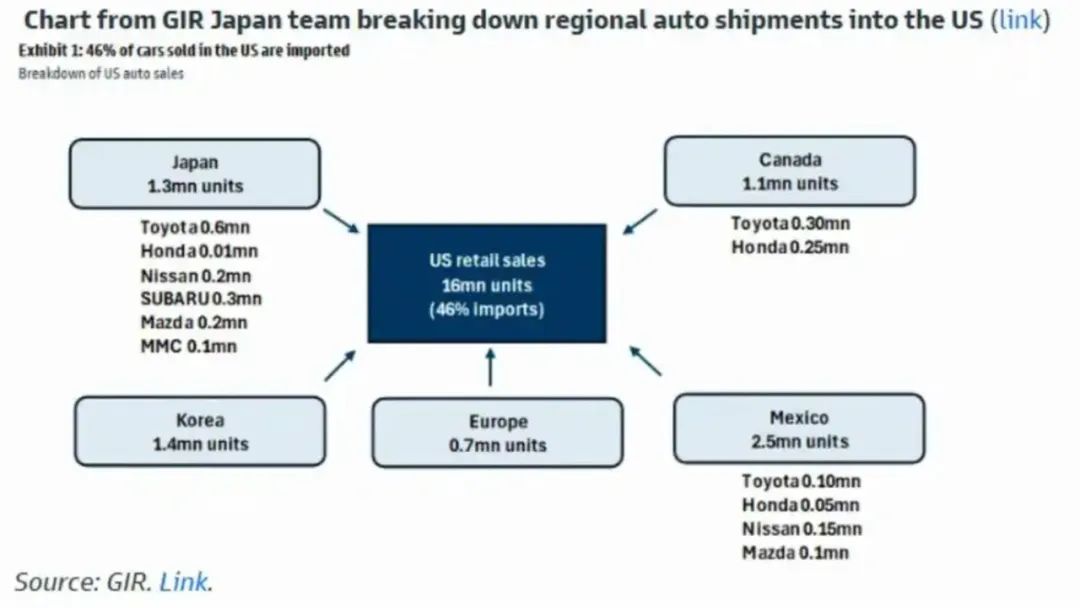

White House data reveals that out of the 16 million light vehicles sold in the US in 2024, only about 8 million (50%) were assembled in the US. Even for vehicles assembled in the US, only 40%-50% of their components originate from the US. IHS data shows that the US produces 10-10.5 million vehicles annually, some of which are exported.

Morgan Stanley's research indicates that the total US auto trade deficit stands at $245 billion, encompassing passenger vehicles, commercial vehicles, and auto parts (including EV batteries). Among these, Asia contributes $115 billion, accounting for 47%. A 25% tariff on cars and parts will have the most significant impact on Japan and South Korea, as their auto exports to the US represent 7% of their total exports.

It's highly probable that car prices will rise in the future. According to Goldman Sachs' calculations, a 25% tariff on complete vehicles could lead to a price increase of $5,000 to $15,000 (assuming vehicle prices range from $20,000 to $60,000); a 25% tariff on parts could increase the cost of locally produced cars by $3,000 to $8,000.

Following the US announcement of car tariffs, Japanese automakers such as Toyota and Honda saw significant reactions in their stock prices. Imports accounted for 46% of US car sales in 2024, with Japan contributing 1.3 million vehicles, ranking third (after Mexico's 2.5 million and South Korea's 1.4 million).

Domestically, the impact of tariffs is relatively limited, as the US tariff on Chinese cars has already exceeded 100%, and an additional 25% will have minimal effect.

According to the China Automotive Strategy and Policy Research Center, 'In 2024, China's exports of complete vehicles to the US fell to 107,000 units, accounting for only 1.7% of total exports, so the increase in tariffs will have a limited impact on overall exports; however, the US remains China's largest export market for auto parts and lithium-ion batteries, accounting for 15% and 25% of exports, respectively. If tariffs are further increased or the product range is expanded, there may be a significant decline in the scale of parts exports. Additionally, the US will impose a 25% tariff on imports from Canada and Mexico, which will also increase the trade costs for Chinese auto products assembled and produced locally entering the US market.'

Moreover, currently, with the combined effect of Trump 1.0 and Biden's tariff policies towards China, before this round of car tariffs, the US tariff on Chinese new energy vehicles was already 122.5%, and the tariff on fuel vehicles was 47.5%. As early as 2024, after Biden significantly increased taxes, most Chinese independent brand enterprises had already indicated their intention to abandon the US market, and the impact of this 25% car tariff did not exceed expectations.

Previously, the main companies exporting to the US were joint venture and foreign-funded automakers, among which SAIC-GM, Volvo, Ford, etc., had already formed a scale of re-export to the US. However, as the US gradually imposes high tariffs on Chinese auto products, these companies may transfer their production lines to other countries or adjust their export market layout.

According to customs statistics, the US has been China's largest export market for auto parts for many years, and it is essential to monitor the impact of Trump 2.0 tariff measures on China's exports of auto parts to the US in the future.

Shifting focus to A-shares, while other Asian stock markets declined alongside US stocks, the A-share market performed relatively stably. Currently, there is a 'seesaw effect' between the Chinese and US capital markets. This round of decline in Nasdaq might signal a significant shift in the 'attack and defense' dynamics and 'bull and bear market' switch between Chinese and US stock markets. Not only the stock market but also the RMB has embarked on a round of appreciation.

In the A-share market, AI-related stocks shone brightly, with stocks like Zhenghai Magnetic Materials and Sanfeng Intelligence, which are associated with humanoid robots, witnessing gains exceeding 10%, underscoring the market's enthusiasm for the AI industry.

In its latest research report, CICC highlighted that advanced AI applications such as humanoid robots and autonomous driving merit attention. Due to the evolution of AI large model capabilities, humanoid robots are anticipated to achieve breakthroughs in generalization ability and interactive experience. Autonomous driving technology is evolving towards the VLA (Vision-Language-Action) direction and is expected to achieve mass production in 2025, accelerating the commercialization process of advanced intelligent driving.

China Securities shares a similar perspective, believing that the AI industry chain is at a turning point from a performance inflection point to a market share inflection point and from technological value to commercial value. The institution advises investors to keep an eye on changes in the AI industry chain, encompassing the independent controllability of computing power chips, the integrated machine and hyper-converged development, and the application of AI in the B-end and C-end markets.

Ping An Securities noted that although the A-share market's rapid upward momentum and catch-up dynamics driven by the initial AI wave have somewhat slowed down, policy implementation and industrial transformation are still expected to gradually bring about marginal improvements in fundamentals, supporting the market's medium-term upward trend. The confirmation of corporate earnings will further drive the in-depth differentiation of the market.

The chief analyst of China Galaxy Securities' machinery industry is more optimistic about the development prospects of 'AI+' in the field of embodied intelligence.

"Open-source low-cost large models, represented by DeepSeek, promote brain equality, drive progress in embodied intelligent robot research and development, commercial landing, and industrialization is expected to accelerate. On the industrial front, giants such as Tesla, Huawei, Xiaomi, Nvidia, and BYD have entered the market, and startups like Unitree, Zhiyuan, and Galaxy General are making continuous strides. The embodied intelligent robot industry is on the cusp of transformation. The hardware supply chain is gradually maturing, and attention should be given to suppliers with a positive fundamental outlook and potential order acquisition capabilities."

Furthermore, foreign institutions' enthusiasm for Chinese assets continues to surge. Recently, Fidelity International, Goldman Sachs, Morgan Stanley, and others have been vocal about their optimism regarding the investment value of China's stock market. Driven by factors such as the explosion of artificial intelligence (AI) technology, the release of policy dividends, and the improvement of corporate performance, China's capital market is exhibiting a potent 'magnetic effect'.

Note: Some images are sourced from the internet. If there is any infringement, please contact us for removal.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving