Technology Independence Undergoes Rigorous Review but Ultimately Triumphs: This Optical Enterprise Advances Through IPO

03/27 2026

03/27 2026

625

625

On March 27, Wuhan Changjin Photonics Technology Co., Ltd. (hereinafter referred to as "Changjin Photonics") successfully cleared the IPO review process on the STAR Market. This specialty optical fiber manufacturer, helmed by Professor Li Jinyan from Huazhong University of Science and Technology and supported by prominent shareholders like Huawei Hubble and China Mobile Fund, has garnered significant market attention.

The IPO of Changjin Photonics transcends a mere capital-raising endeavor by a single enterprise; it serves as a pivotal test for the domestic self-reliance process within the specialty optical fiber industry chain. Amidst the industry's dual impetus of domestic substitution and escalating AI computing power demand, this "little giant" enterprise's successful passage underscores the opportunities and challenges present in China's optical materials sector.

Changjin Photonics specializes in the R&D and industrialization of specialty optical fibers, with its flagship product, rare-earth-doped fibers, occupying a crucial position in the upstream of the laser industry chain. According to its prospectus, the company has developed a comprehensive product matrix encompassing ytterbium-doped fibers, erbium-doped fibers, erbium-ytterbium-doped fibers, thulium-doped fibers, and functionally enhanced rare-earth-doped fibers, offering full coverage from low-power to high-power applications. It stands as one of the enterprises with the most complete product lines in the domestic market.

In terms of technical prowess, Changjin Photonics' ultra-wideband L-band erbium-doped fibers have achieved performance metrics on par with international advanced standards, facilitating the large-scale commercialization of China's 400G optical transmission networks. Within the laser sector, the company has achieved batch production and sales of related export-controlled products, establishing itself as a core supplier to leading fiber laser manufacturers such as Raycus Laser, Maxphotonics, and JP Optics.

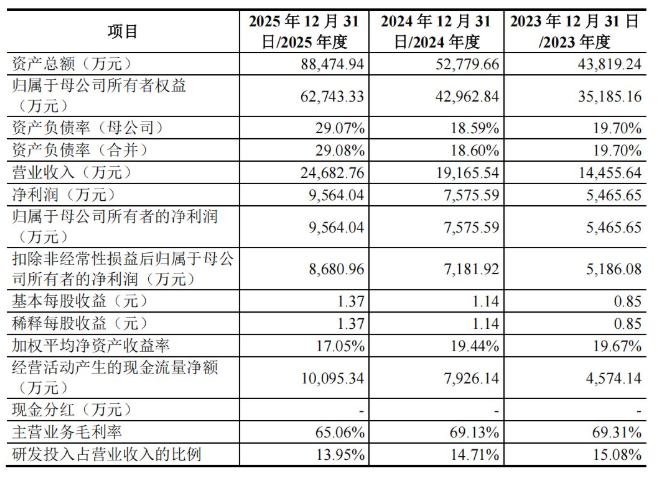

From a financial perspective, the company's revenue surged from RMB 145 million to RMB 247 million, while its net profit climbed from RMB 54.66 million to RMB 95.64 million between 2023 and 2025. This growth trajectory is underpinned by the company's consistent increase in R&D investment, with cumulative R&D expenditures exceeding RMB 84 million during the reporting period, accounting for a stable 14% of revenue.

However, behind its stellar performance, Changjin Photonics' technological "value" faced intense scrutiny from regulators. The primary focus was on the longstanding "industry-university-research" entanglement between the company and Huazhong University of Science and Technology. As of the end of 2025, Changjin Photonics held 37 invention patents, 12 of which were assigned from Huazhong University of Science and Technology.

Notably, the financial flows associated with these two patent assignments warrant close examination: In 2017, the company acquired six invention patents from Huazhong University of Science and Technology for RMB 1.0014 million. In accordance with the university's policy on the transformation of scientific and technological achievements, 70% of the net proceeds were returned to the R&D team as research incentives, with approximately RMB 700,000 ultimately reinvested into the company through capital increases. The controlling team only paid a differential of approximately RMB 318,000 to complete the transfer of core intellectual property rights. In August 2025, the company acquired another six invention patents from Huazhong University of Science and Technology for RMB 2.1 million.

Regulators directly questioned during inquiries whether the technological ownership was clear and whether there existed risks of technological disputes. Although Changjin Photonics responded that it had obtained full ownership of the relevant patents and issued a Letter of Integrity Commitment, the fact that a company claiming to have "shifted to independent R&D" purchased patents from its alma mater on the eve of its IPO drew market attention to its technological independence arguments.

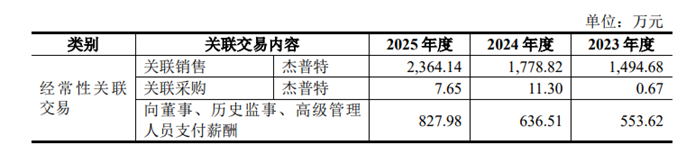

Greater operational risks arise from the duality of its customer structure. During the reporting period, the revenue share from the company's top five customers decreased from 82.26% to 66.20%, yet concentration remained high. Core customers such as Raycus Laser, Maxphotonics, and JP Optics were not only major revenue sources but also potential direct competitors, as these customers had already developed some self-supply capabilities for specialty optical fibers.

Meanwhile, JP Optics, the second-largest shareholder, was also among the company's top five customers, and its sales prices were often lower than those of non-affiliated parties, raising questions about the fairness of related-party transactions.

On the upstream supply chain front, Changjin Photonics' situation is equally noteworthy. In 2025, the company's imports of quartz tubing and optical fiber coatings accounted for approximately 62% and 97%, respectively, of its procurement of similar raw materials, indicating a high dependence on overseas suppliers for core raw materials. For a science and technology innovation enterprise positioning itself around "domestic substitution," having its upstream supply chain constrained by overseas sources poses potential supply chain risks.

The IPO review of Changjin Photonics offers dual insights for the optical industry. Firstly, the specialty optical fiber sector is ushering in a historical opportunity for demand explosion. With the accelerated construction of AI computing power networks, the large-scale commercialization of 400G backbone networks, and the in-depth advancement of the "East Data, West Computing" project, the optical fiber and cable market continues to heat up. Changjin Photonics' strategic布局 (layout) in high-growth sectors such as optical communications, national defense, and commercial aerospace aligns with this industrial trend.

Secondly, technological autonomy and the clarification of industry-university-research boundaries have become critical propositions. Entrepreneurship by university professors is an important pathway for transforming scientific and technological achievements, but the clear definition of technological ownership and the independence of R&D teams are thresholds that enterprises must overcome when accessing capital markets. The regulatory scrutiny faced by Changjin Photonics provides a cautionary tale for more "academic-oriented" science and technology innovation enterprises.

Beneath the grand narrative of domestic substitution, true competitiveness stems from continuous technological innovation and a robust commercial closed loop. For enterprises in the optical industry chain, this is the fundamental path to navigating through cycles.

-

![]()

Internet Valuation Logic Shifts: From Scale Narrative to Profit Accountability

-

VOYAH Struggles to Find Its Niche in the Competitive Auto Market

-

![]()

Maxwell Technologies Gains Indirect Stake in Precision Optics via New Venture

-

![]()

Raising 1.8 Billion! This Domestic Optical Inspection 'Little Giant' is Going Public

-

China's AI 'Normandy Moment': The Explicit and Implicit Threads of BATL

-

![]()

Starting at 4999 Yuan! Nubia RedMagic Gaming Tablet 5 Pro Review: Impressive Performance, But Hefty Price Tag

-

![]()

ByteDance Initiates First Major Management Reform

-

![]()

AI is Quietly Destroying a Trillion-Dollar Industry