Net Profit Soars by 156%! What’s the Secret Behind This Seasoned Optical Company’s Success?

04/21 2026

04/21 2026

629

629

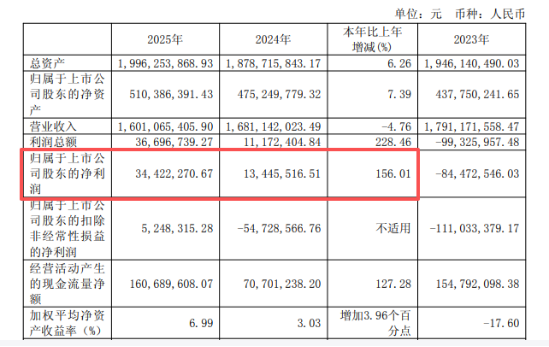

On April 21, Phoenix Optics unveiled its 2025 annual report. Data revealed that the company recorded an annual operating revenue of RMB 1.601 billion. The net profit attributable to the parent company soared to RMB 34.4223 million, marking a remarkable 156.01% year-on-year increase. After deducting non-recurring items, the net profit stood at RMB 5.2483 million, a stark contrast to the RMB 54.7286 million loss incurred during the same period last year. This represents a significant turnaround from losses to profits.

At first glance, the revenue appeared to decline by 4.76% year-on-year. However, this was largely attributable to the company’s strategic decision to proactively divest its lithium battery business. Excluding this factor, the two core businesses—optical and smart controllers—both experienced steady growth. This annual report from the 61-year-old optical veteran signals that its strategic pivot to focus on core operations has begun to pay dividends, with the fundamental business gradually regaining its footing.

From a business structure perspective, the optical segment emerged as the primary growth driver for Phoenix Optics in 2025. Annual revenue from the optical business surged to RMB 1.041 billion, up 16.44% year-on-year. Meanwhile, revenue from the smart controller business reached RMB 515 million, reflecting a 3.87% year-on-year increase.

The company’s emphasis on high-end product upgrades is also noteworthy. In the optical realm, Phoenix Optics continued to concentrate on core application areas such as automotive, security, infrared, and medical sectors. The mass production of the black film coating process for lenses was achieved, while the performance of infrared LWP film systems and composite laser infrared lenses was further enhanced.

In the realm of optical instruments, several educational microscopes successfully entered mass production and sales. The new-generation research-grade inverted fluorescence microscopy imaging system completed prototype assembly and testing. The company’s technological prowess in precision optical instruments is being effectively translated into tangible product strength.p>

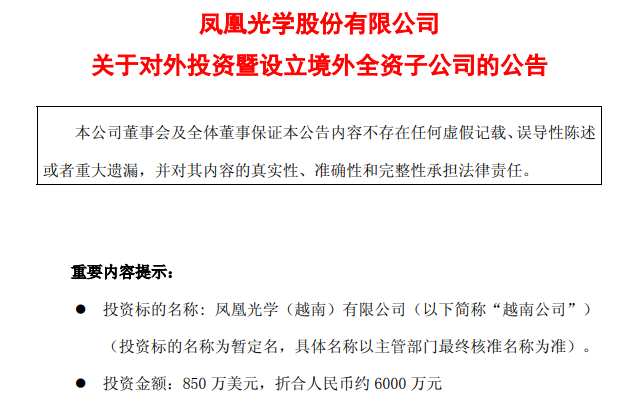

Furthermore, overseas market expansion emerged as a key highlight in Phoenix Optics’ 2025 annual report. The company’s annual foreign revenue reached RMB 312 million, up 14.3% year-on-year, with an overseas business gross margin of 23.21%, significantly higher than domestic levels. Behind these figures lies substantial progress in the company’s global market strategy. During the reporting period, Phoenix Optics not only actively constructed service systems for overseas and emerging markets but also established a wholly-owned subsidiary in Vietnam with a total investment of $8.5 million, marking a pivotal step in its overseas capacity deployment. Changes in R&D investment also warrant careful analysis. In 2025, the company’s R&D expenses amounted to RMB 92.8966 million, accounting for 5.80% of revenue, reflecting a year-on-year decrease. However, this was primarily due to the exclusion of new energy businesses from consolidated financial statements and the transfer of XR R&D projects in the previous period. Excluding these non-recurring factors, the company’s actual R&D resources allocated to core optical and smart control technologies became more focused. The R&D team remained stable at 371 people, accounting for 16.37% of the total workforce, with technical reserves remaining robust. At the cash flow level, net cash generated from operating activities in 2025 reached RMB 161 million, up 127.28% year-on-year. This directly reflects a substantial improvement in the core business’s cash-generating ability. Sales expenses declined by 15.17% year-on-year, coupled with gross margin improvements, driving the company’s net profit margin back to 2.15%. The effectiveness of cost control is translating into tangible improvements in the income statement. Currently, China’s optical industry is undergoing profound structural transformation, with application scenarios rapidly expanding from traditional smartphone cameras to diverse fields such as automotive optics, AR/VR, and medical imaging. While downstream market expansion has opened up broad growth opportunities for optical companies, technical barriers and competitive intensity are also on the rise. For Phoenix Optics, rather than pursuing scattered deployments across multiple fields and superficial scale expansion, it is more prudent to concentrate resources in core areas and achieve depth. The medium- to long-term strategy clearly outlined in the annual report—to position the company as a core product and solution provider in the smart IoT sector—also indicates that Phoenix Optics is consciously moving upstream toward higher value-added segments of the value chain from its traditional role as an optical component manufacturer. Overall, Phoenix Optics achieved a dual transformation in 2025 by focusing on its core business and returning to profitability after deducting non-recurring items. The company now has a relatively clear direction for fundamental business recovery. Amid the ongoing expansion of optical industry applications and deepening import substitution, the path Phoenix Optics is pursuing—focus, internationalization, and upgrading—may well represent an effective strategy for numerous optical companies seeking to break through fierce competition.

-

On the Eve of Its IPO, Avatr Finds Itself Embroiled in a 'Farce of Controversy and Belittlement'

-

![]()

Yutong Optics' Japanese Subsidiary Unveiled in Tokyo, Shifting Strategic Focus to Technology-Driven Growth

-

![]()

Half-Year Revenue Outstrips Last Year’s Total! Zhongrun Optics Forecasts 80.2% H1 Revenue Growth

-

![]()

Why Does AI Competition Start with Computing Power?

-

![]()

Apple AI Finally Makes Its Debut in China, Yet iPhone's 'AI Autonomy' Faces Uncertainty

-

![]()

Apple AI and QianWen Make Up Lessons: Alibaba Has Its Own 'Doubao Phone'

-

![]()

QianWen Joins Apple, Signal for Large Models to ‘Fade into the Background’

-

![]()

The ‘Anchor’ Strategy of Google Hidden Behind the Bleeding Financial Report