Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

06/05 2026

06/05 2026

520

520

"Has the Era of CPUs Arrived?"

Just yesterday (June 3), Foxconn Industrial Internet, the global leader in server contract manufacturing, marked a historic moment: its stock surged over 5% intra-day, pushing its market capitalization to briefly exceed 1.68 trillion yuan—a record high since its listing. It became the most valuable A-share electronics contract manufacturing stock ever, even surpassing Kweichow Moutai briefly to rank fifth among A-shares. Behind this remarkable market cap lies performance support from sustained order growth from downstream clients like Dell and Lenovo—it is the "hidden champion" behind these giants.

Prior to this, Dell Technologies released its FY2027 Q1 financials on May 29: quarterly revenue hit $43.84 billion, up 88% year-on-year; net profit attributable to shareholders reached $3.438 billion, soaring 256%. Both metrics far exceeded market expectations. On the same day, Dell's stock price surged 32%, marking its largest single-day gain since listing.

Ben Reitzes, Head of Technology Research at Melius Research, stated during Dell's earnings call, "I've probably never seen a quarter like Dell's." This remark was widely cited to express shock over Dell's financials.

Also on May 29, Lenovo's stock soared in the Hong Kong market: it jumped 22% in a single day, with a cumulative monthly gain of 109% in May—its strongest monthly performance in 27 years. Additionally, Lenovo's year-to-date surge once exceeded 172%, reaching 172.57% as of June 1, making it the top-performing stock among Hang Seng Index constituents.

The direct catalyst for its stock surge was the FY2025/26 and Q4 results released seven days earlier (May 22): annual revenue hit $83.1 billion, up 20% YoY, a record high; Q4 revenue reached $21.6 billion, up 27% YoY, with net profit of $521 million, soaring 479% YoY.

In recent years, market attention has focused on NVIDIA's GPU dominance and the computing power arms race for large AI models, labeling traditional vendors like Dell, Lenovo, and Foxconn Industrial Internet as "old guard" or "contract manufacturers." However, the simultaneous strength of these three companies signifies a complete rewrite of the narrative—under the AI wave, "old guard" players across different segments are undergoing a new wave of value revaluation.

The growth drivers behind the three companies vary: Dell benefits from the Agentic AI boom, with explosive demand for AI servers; Lenovo's core driver is AI PCs—as Agentic AI rises, more computing power shifts locally, enabling a single, more powerful AI PC to handle tasks previously requiring cloud computing. As the world's largest PC manufacturer, Lenovo is the direct beneficiary of this local computing upgrade; Foxconn Industrial Internet emerges as the hidden winner behind Dell and Lenovo, handling contract manufacturing for both servers and PCs, with manufacturing orders from both growth lines flowing to its production lines.

Traditional Servers Reignite Growth: Agentic AI Drives New Demand

To understand this market rally, one must first dispel a misconception: the rise of AI large models is not eroding traditional servers' market share but adding a new layer of demand on top of it.

In recent years, the traditional server market has stagnated or even declined. The consensus was that traditional servers would be gradually replaced by AI servers. However, this round of growth is entirely different—it is not about substitution but opening a new growth market.

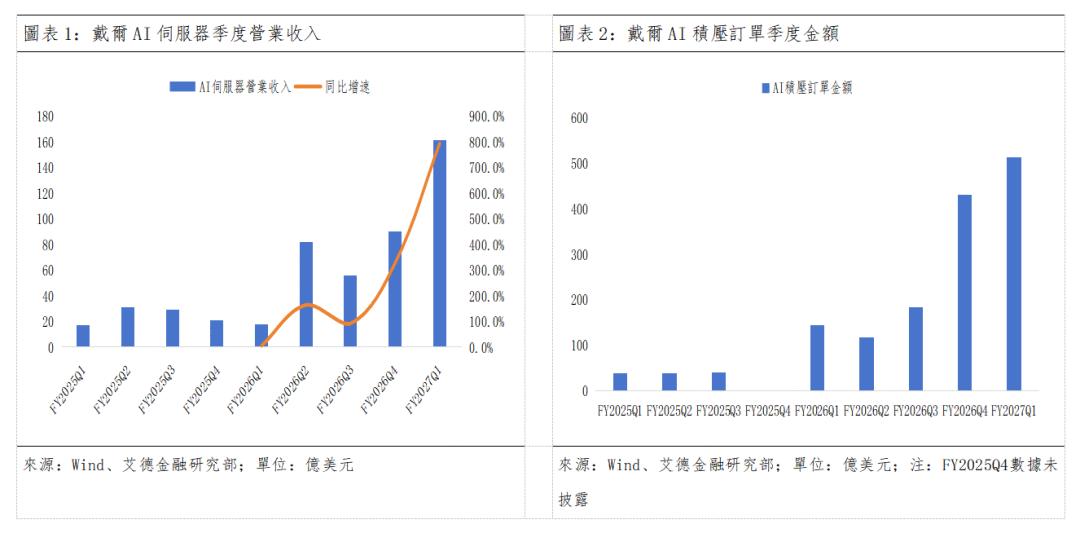

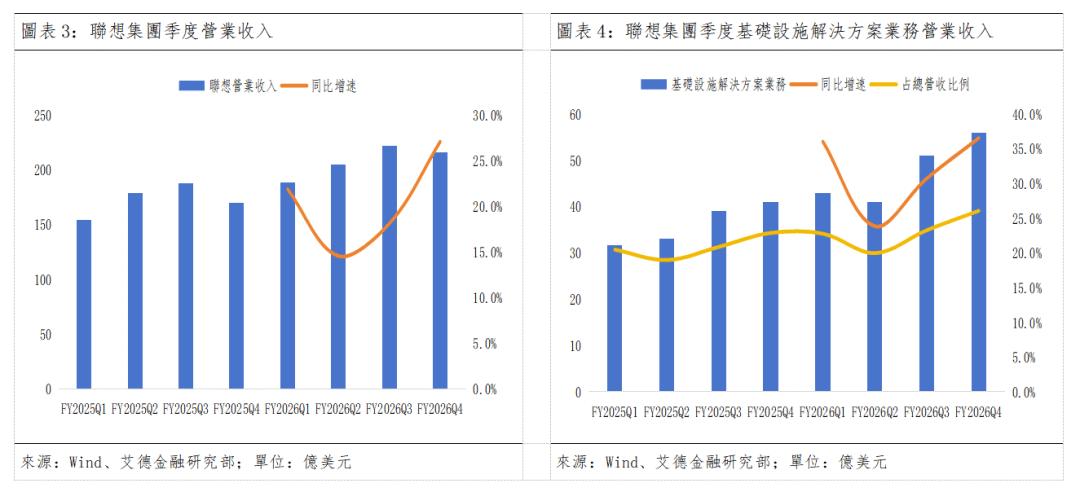

Dell's data best illustrates this: In FY2027 Q1, Dell's Infrastructure Solutions Group (ISG) revenue reached $29 billion, up 181% YoY. Traditional server and networking revenue hit $8.543 billion, up 92% YoY—1.6 times the market expectation of $5.2 billion, a record high. Meanwhile, AI server revenue surged to $16.1 billion, up 757% YoY. Clearly, traditional and AI servers are growing in tandem, not in a zero-sum relationship.

Lenovo's data corroborates Dell's. For FY2025/26 ending March 31, 2026, Lenovo achieved $83.1 billion in revenue, up 20% YoY, with adjusted net profit of $2 billion, up 42% YoY. Annual AI-related business revenue surged 105% YoY, accounting for 33% of total revenue, rising to 38% in Q4. ISG business grew fastest, with full-year revenue up 32% YoY to $19.2 billion, a record high. AI server revenue achieved double-digit YoY growth.

The fundamental reason lies in the workload characteristics of Agentic AI. Unlike traditional AI training tasks, which heavily rely on GPUs, Agentic AI workloads require CPUs for task orchestration, significantly driving up DRAM and storage demand. Simply put, an Agentic AI completing a complex task often needs to call multiple services and process large volumes of intermediate data, with this computational work falling on traditional servers. As Dell COO Jeff Clarke said in an analyst call: "GPUs do the magical work, but the massive sequential work around them is CPU-driven."

Semiconductor analysis firm SemiAnalysis notes that in Agentic AI workloads, CPU processing latency accounts for 50%-90% of total latency, with GPUs often idling while waiting for CPU scheduling. Consequently, the CPU-to-GPU ratio must adjust. Creative Strategies CEO and Chief Analyst Ben Bajarin points out: "During the model training era, the CPU-to-GPU ratio in AI deployments was roughly 1:4. Agentic inference rewrites this to nearly 1:1 (or even lower GPU share)." This aligns with Intel CEO Chen Liwu's judgment in the Q1 2026 earnings call.

AMR's data is even more striking: in the Agentic AI era, CPU core demand per gigawatt of data center power will surge from 30 million to 120 million—a fourfold increase. Morgan Stanley further predicts that by 2030, Agentic AI could add $32.5 billion to $60 billion in new demand for data center CPUs, with the total server CPU market exceeding $100 billion.

Beyond CPU demand, Agentic AI significantly boosts DRAM and storage needs—it requires contextual awareness, persistent memory, retrieval-augmented generation, KV Cache, and intermediate state storage, all heavily reliant on CPU-side DRAM rather than GPU-side HBM.

Mizuho Securities' latest semiconductor industry report states that Agentic AI's token generation volume may exceed traditional generative AI by over 1,000 times, with massive agent collaboration driving far higher CPU and DRAM consumption than traditional AI inference. It predicts that Agentic AI will add 9%-13% global DRAM demand by 2027, reaching ~7,200PB in the most optimistic scenario, accounting for 13% of global DRAM demand. Morgan Stanley's latest forecast is even more bullish, projecting ~74EB in new DRAM demand by 2030 under baseline scenarios and up to 221EB in bullish scenarios—equivalent to 1.7x and 4.9x the current global DRAM market size, respectively.

More importantly, this procurement boom is spreading from top cloud service providers to secondary cloud vendors and large enterprises, with traditional sectors like banking and manufacturing deploying AI servers. The enterprise infrastructure (E/SMB) business targeting these clients has far higher gross margins than cloud infrastructure (CSP) business. For example, Lenovo's E/SMB revenue in China surged 52% YoY in Q3, far outpacing CSP growth. Lenovo CEO Yang Yuanqing also noted that relying solely on large cloud providers is no longer sufficient.

IDC Vendors' Transformation: From "Cabinet Rental" to "Computing Power Services"

While traditional servers' surge represents a demand-side growth story, the IDC industry's transformation is a deeper business model (business model) Refactoring (restructuring).

Historically, the IDC logic was simple: build data centers, rent cabinets, and charge by bandwidth, primarily serving internet companies' traffic hosting needs. This business model featured heavy assets, high depreciation, and low added value. However, the rise of AI large models fundamentally altered this logic: training and inference require high-density computing power, ultra-low-latency networks, and efficient cooling—ordinary cabinets cannot meet these demands. This necessitates an upgrade from general-purpose storage centers to intelligent computing power infrastructures.

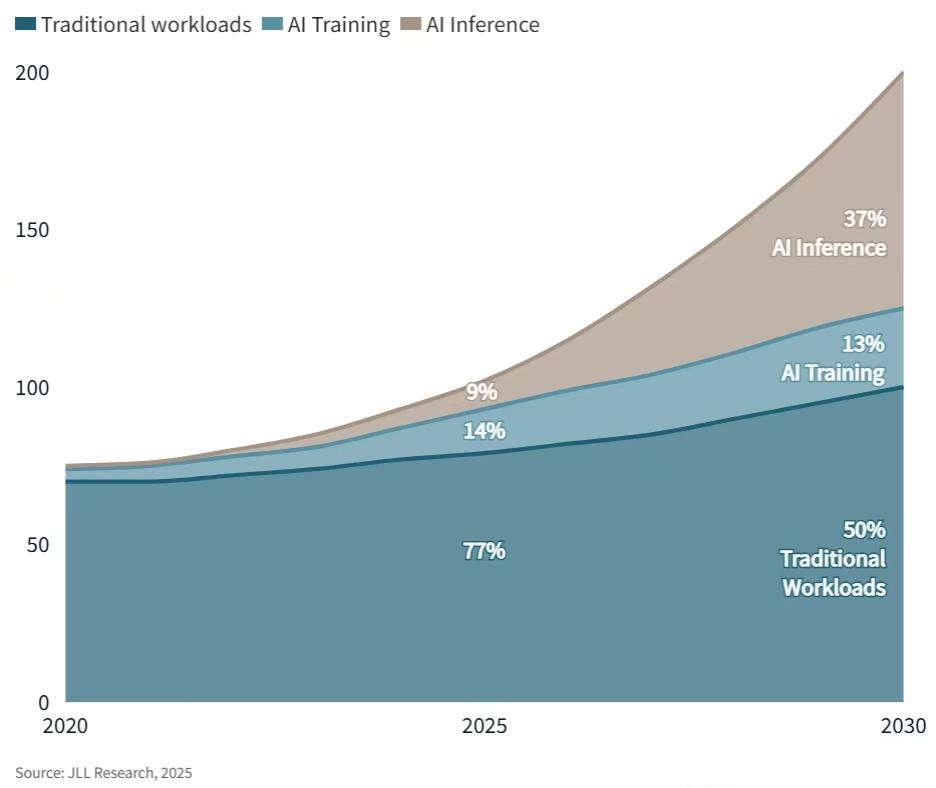

According to JLL Research's *Global Data Center Outlook 2026*, AI workloads will account for 50% of global data center capacity by 2030, up from ~25% in 2025. It also predicts that inference workloads may surpass training to become the primary AI demand by 2027. The China Academy of Information and Communications Technology estimates that global computing power will exceed 16 ZFlops by 2030, with intelligent computing power's share rising from 63% in 2023 to over 90% by 2030.

Source: JLL Research Report

This structural demand upgrade directly drives IDC vendors' business model transformation. Leveraging their data center infrastructure, energy quotas, and mature operational capabilities, traditional IDC vendors are shifting toward computing power leasing services. This not only reduces clients' initial AI computing deployment costs but also provides end-to-end services from hardware setup and network deployment to model optimization, offering high added value.

This approach is highly attractive to finance, government, and enterprise clients. These customers have strong AI computing needs but lack the capacity to independently build and operate large-scale computing clusters. Moreover, they have stringent data security and compliance requirements, often preferring local or dedicated computing services over public clouds. Traditional IDC vendors, with their accumulated client resources and compliance expertise, hold natural advantages in these areas.

Policy tailwinds further support this transformation. In March 2026, "computing-power-electricity coordination" was included in the government work report as a national-level new infrastructure initiative. In May, the National Development and Reform Commission, Ministry of Industry and Information Technology, National Energy Administration, and National Data Administration jointly issued the *Action Plan for Promoting Bidirectional Empowerment of AI and Energy*, specifically deploying efficient computing-power-electricity coordination.

Computing-power-electricity coordination is not merely about providing power for computing growth but involves deep integration and resource restructuring between the computing and power industries. The core logic is bidirectional empowerment: "power enables computing cost reduction, computing enhances grid efficiency." In this context, vendors with green power access and energy-saving technologies can significantly lower operational costs through green power trading and energy efficiency management, forming differentiated advantages in increasingly competitive markets.

Technological Upgrades Reshape Industry Core Competitiveness

In fact, both the traditional server demand surge and IDC business model transformation are underpinned by technological upgrades—they adapt to AI-era demands through technological advancements, with technical capabilities determining corporate core competitiveness.

On the server side, higher per-unit memory configurations have become standard. AI workloads require larger DRAM capacities per server for model parameters and large-scale context processing. According to industry estimates, a single AI server's DRAM demand is ~8-10x that of traditional servers.

In IDC terminals, liquid cooling technology is rapidly gaining popularity. Liquid cooling solutions can reduce the Power Usage Effectiveness (PUE) of data centers to below 1.2, cutting energy consumption by over 30% compared to traditional air cooling. Lenovo's Neptune liquid cooling technology achieves a heat dissipation efficiency of 98%, enables 90% waste heat recovery and reuse, reduces energy consumption by 42%, and lowers the data center PUE to 1.1. In the third fiscal quarter, revenue from Lenovo's Neptune liquid cooling technology surged by 300% year-on-year, nearly doubling compared to the second fiscal quarter (154%), indirectly confirming the accelerating trend.

Furthermore, intelligent operations and maintenance (O&M) and modular construction are significantly enhancing the operational efficiency of IDCs. Intelligent O&M systems can monitor the operational status of data centers in real-time through AI algorithms, predict equipment failures, automatically adjust resource allocation, and reduce O&M costs by over 30%. Modular construction can halve the construction timeline of data centers, greatly improving overall delivery efficiency and enabling faster responses to market demands. These technological benefits are improving the long-strained profit structures of IDC vendors.

Summary

The proliferation of AI technology is reshaping the entire digital infrastructure industry, with previously underestimated 'old forces' now undergoing value reassessment.

The logic behind this is straightforward: as AI models proliferate and their applications broaden, the computational infrastructure required to support them expands accordingly. The rise of Agentic AI has extended demand from GPUs to CPUs, from training clusters to enterprise servers, and from the cloud to PC desktops. The widespread adoption of intelligent computing is transforming IDCs from passive hosting providers to proactive enablers.

According to research data from Dell'Oro Group, global data center capital expenditures are projected to grow by 57% year-on-year to USD 726 billion in 2025, marking the fastest growth rate since the firm began tracking in 2014. This figure is expected to surpass USD 1 trillion in 2026. Ultimately, these investments will translate into server orders for companies like Dell, Lenovo, and their backend supplier Foxconn Industrial Internet.

Therefore, it is foreseeable that the stock price rebounds of 'old forces' such as Dell, Lenovo, and Foxconn Industrial Internet are not merely short-term Valuation repair (valuations corrections) but rather a repricing by the market reflecting a longer-term trend. In the AI era, computational infrastructure—whether cloud-based data centers or end-user PCs—will serve as the core foundation supporting the entire digital economy. Companies that build and operate this foundation will enter a new realm of value creation.

-

Ofilm Teams Up with ADSensE to Propel Large-Scale Deployment of All-Solid-State LiDAR Powered by ADS6311 Chip!

-

![]()

Loss of 2.5 Billion Yet Facing Strong Demand for Shares? Another Battle for Control of Lianchuang Electronics

-

![]()

Huawei’s Enjoy Series Flies Off the Shelves, Prompting Xiaomi to Double Down on Budget Smartphones

-

![]()

Beijing Hyundai's Top Executive Criticizes Industry Disorder: Certain Brands Treat Customers as Beta Testers

-

![]()

The domestic mobile phone market has declined for five consecutive quarters! Huawei defies the trend with significant growth: maintains its top market share

-

Annual Revenue Surpasses 3 Billion: An Automotive Trim 'Little Giant' Makes Its Debut on the Beijing Stock Exchange

-

![]()

The Space Force Wants to Spend $30 Billion on Rocket Launches: Is Trump Doubling Down, and Is SpaceX the Big Winner?

-

![]()

Going Crazy! One out of Every Three Plug-in Hybrids Sold in Europe is a Chinese Vehicle