Market Share Dilemma: DJI vs. Insta360—Is It '40-40' or '60-30'?

07/01 2026

07/01 2026

456

456

In 1950, renowned director Akira Kurosawa crafted the film Rashomon. The narrative unfolds through the accounts of a woodcutter, a bandit, and the spirit of a murdered man (speaking via a medium), each recounting their version of the same crime, resulting in three conflicting narratives.

Similarly, in the consumer electronics sector, market share data can sometimes resemble a Rashomon scenario—where, within the same market segment and timeframe, different reports can paint vastly different pictures.

Since the start of this year, both DJI and Insta360 have witnessed robust sales for their latest offerings. In April, the DJI Pocket 4 sold out instantly online and faced backorders at physical stores for up to a month. In June, the Insta360 Luna Ultra and DJI Pocket 4P were launched, both selling out immediately and achieving impressive sales figures during the 618 shopping festival.

However, when the conversation shifts to "who's leading," the answers vary widely.

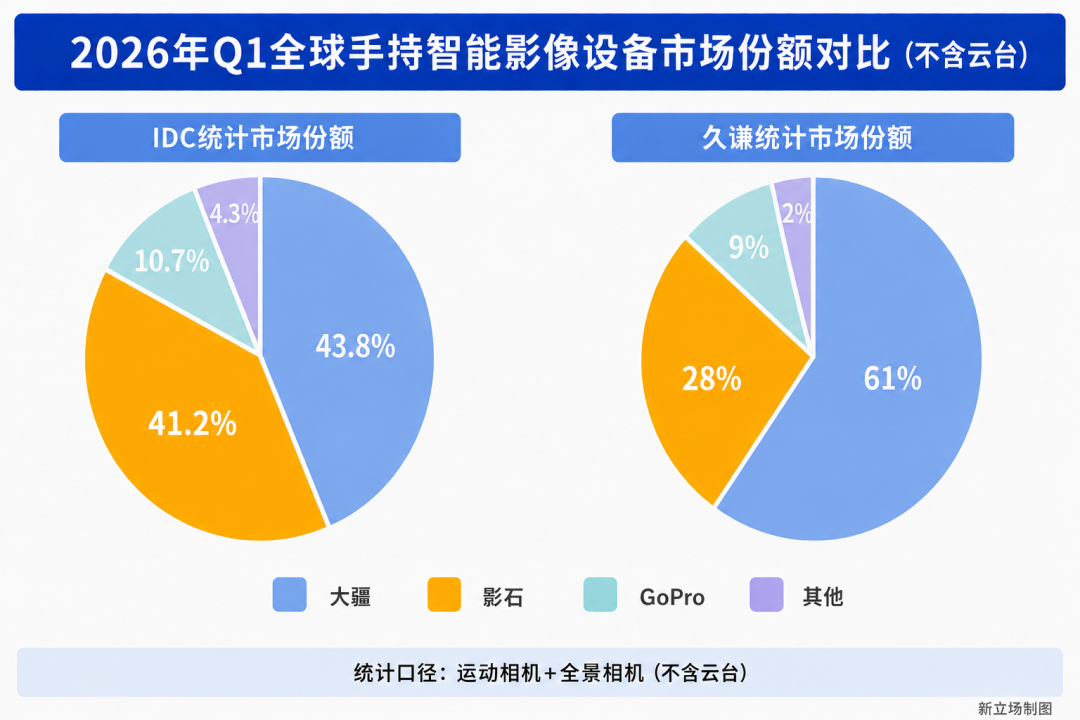

According to IDC's latest global tracking report, in the first quarter of 2026, DJI and Insta360 reached a near '40-40' split in the action camera market. Simultaneously, Insta360 maintained over 68% of the global shipment share in the 360-degree camera market.

Yet, over the past month, another widely referenced industry dataset tells a starkly different tale: Insta360's market share in the 360-degree camera market has reportedly dropped to 49% or even 33%, with DJI taking a commanding lead.

Why do two reports covering the same market and quarter arrive at nearly opposite conclusions?

Is there a miscalculation, or are they simply not measuring the same market?

The answer may lie in the 'statistical criteria' that few take the time to scrutinize carefully.

The handheld smart camera category has undergone significant transformations in recent years. DJI's Pocket series, Insta360's 360-degree X series, and the much-discussed Luna Ultra this year have all taken turns dominating the market spotlight.

Features such as AI editing and one-click video generation have matured, enabling ordinary users to effortlessly create polished short films. The user base has also expanded from early 'creators' to 'recorders.'

Clearly, this is a market driven by growth logic. DJI and Insta360 are undoubtedly the two most closely watched companies in this space.

Founded nearly a decade apart—DJI in 2006, with 2025 revenue reportedly expected to exceed 100 billion yuan, and Insta360 starting as a Nanjing University startup team in 2015, with 2025 revenue around 9.7 billion yuan—though vastly different in size, Insta360 holds a trump card: 360-degree cameras. This segment, which even Ricoh and Samsung failed to dominate, has been firmly held by Insta360, maintaining a 60-80% global share for years—a small but stable stronghold.

For a long time, the two companies operated in their respective lanes without direct conflict, and the outside world was content to label them simply as 'drones for DJI, 360-degree cameras for Insta360.'

But now, that label seems inadequate.

The recent clashes have centered on gimbal cameras. This category traces its roots back to GoPro's Karma Grip in 2016 and REMOVU K1 in 2017, which integrated a gimbal, screen, and handle into one device.

DJI's success lay in transforming gimbal cameras into a mass-market consumer product. Since then, DJI has essentially dominated this category, with the market waiting for a significant challenger.

In June 2026, the Insta360 Luna Ultra was released, becoming the first product in the gimbal camera space truly comparable to DJI's Pocket series. Its sell-out in five minutes confirmed market expectations.

But in reality, the true clash between the two companies began nearly a year earlier than the Luna Ultra's release.

In July 2025, Insta360 announced its 360-degree drone brand 'Antigravity,' and just three days later, DJI released its first 360-degree camera, the Osmo 360. In September of the same year, DJI launched the Osmo Nano, targeting Insta360's GO Ultra and entering the thumb camera category pioneered by Insta360.

According to Liu Jingkang's public statements, Insta360's decision to enter the drone market was made five years ago, and in 2022, they even released a 360-degree camera compatible with drones. With technical groundwork already laid, Insta360 is expanding from its niche 360-degree camera market into larger markets like drones and gimbal cameras, while DJI is moving from the large drone and gimbal camera market into the smaller 360-degree and thumb camera markets created by Insta360—the two companies are expanding in opposite directions but are being pushed into each other's paths by their growth strategies.

But now, this space is becoming crowded. OPPO and Vivo have announced their entry into the gimbal camera market, directly targeting DJI's long-dominated Pocket series, while Honor has launched a 'robot phone,' attempting to enter the same scene with a different product logic.

The influx of new players is actually a positive signal: it suggests this segment is far from a zero-sum game.

Yet, as the market becomes more crowded, discrepancies in statistical criteria become increasingly glaring.

Two contradictory narratives are emerging about the same market.

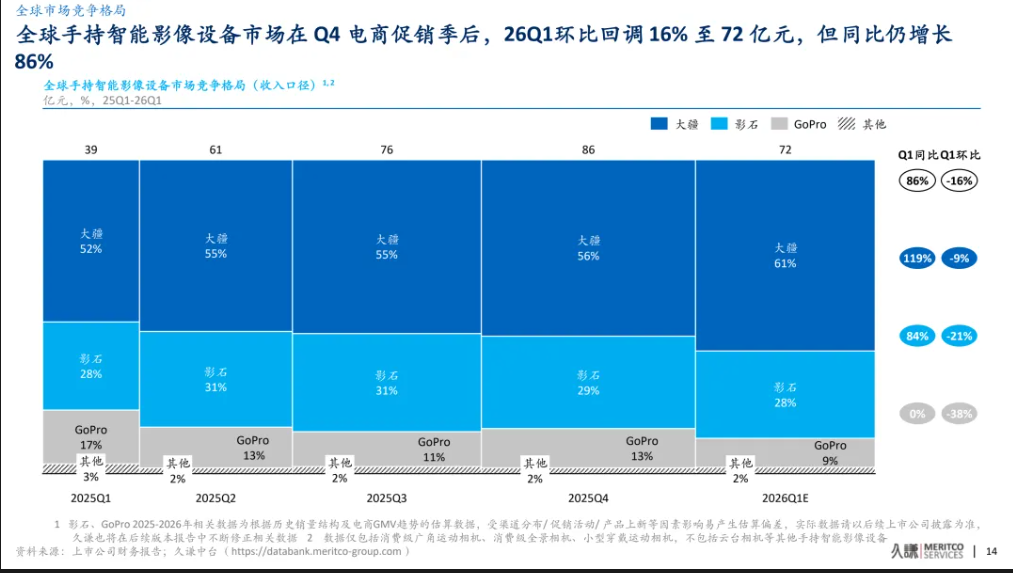

A report by Jiuqian Zhongtai shows that in the first quarter of 2026, DJI held 61% of the global handheld smart imaging device market, with Insta360 at 28%. These figures have been repeatedly cited in the industry over the past month and have nearly become 'accepted facts,' frequently referenced in industry articles and even some investment analyses.

However, IDC's latest global market tracking report paints a different picture. In the same broad category, DJI holds 65% and Insta360 22%. At first glance, the numbers seem similar, but a closer look reveals inconsistencies.

Jiuqian's data covers action cameras, 360-degree cameras, and wearable cameras, excluding gimbal cameras; while IDC's 'handheld smart cameras' include gimbal cameras. The issue is that Insta360's Luna Ultra only officially launched in June, so there were no shipments in Q1.

In other words, nearly all gimbal cameras available online in Q1 were from DJI, a major category with 1.63 million units shipped, yet DJI's share only rose slightly from 61% to 65%, a mere 4-point increase—a figure that seems questionable.

If we standardize the criteria and exclude gimbal cameras, the two companies are still in a '40-40' split.

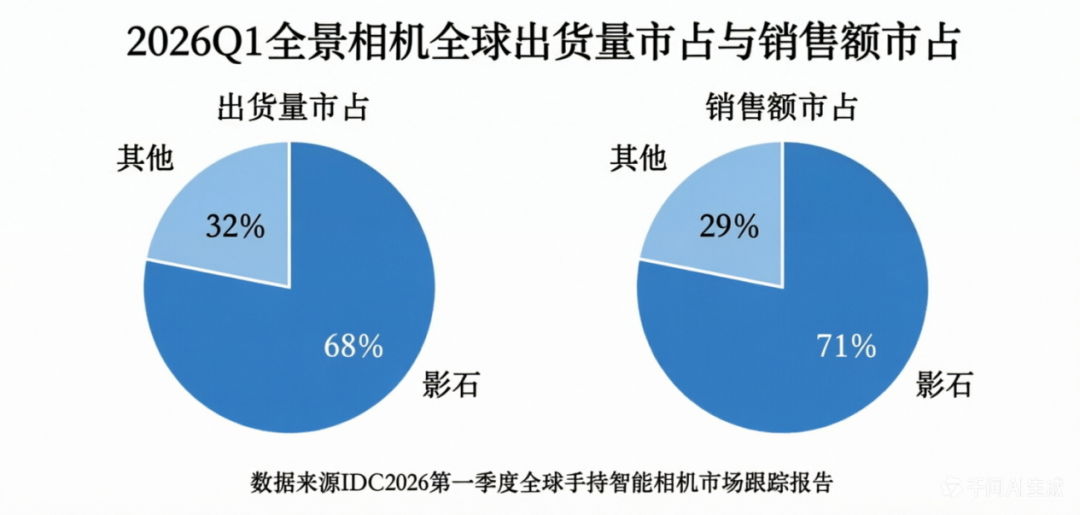

When we zoom in on the 360-degree camera segment, IDC data shows Insta360 with over 68% of shipment share and 71% of revenue share, firmly holding the global top spot. This sharply contrasts with Jiuqian's figures, widely cited by media, which show Insta360's market share in 360-degree cameras plummeting to 49% or even 33%, with DJI rising to 57%.

When both reports are placed side by side, the discrepancy is striking, as if they describe two entirely different markets. Where does the problem lie?

Currently, the gap mainly stems from two differences in statistical criteria.

Jiuqian Zhongtai primarily monitors e-commerce platform data, using 'estimates based on historical sales structure and e-commerce GMV trends.' In other words, these are global estimates derived from e-commerce trends and then modeled outward.

Using online retail share to infer global competitive standing is like judging national traffic conditions by looking at vehicle flow in one city—it inevitably involves some generalization.

Second is the difference in statistical methods. E-commerce sales capture real-time retail popularity, which can be amplified or suppressed by spikes in performance during events like 618 or Double 11; while shipment and revenue data more closely reflect manufacturers' actual global operating conditions, with smoother fluctuations.

Early last year, an institution cited Jiuqian's offline store survey data to conclude that Pop Mart's domestic store growth was slowing. Yet, Pop Mart's 2025 annual report and Q1 2026 operating data showed domestic offline channel growth as high as 75-80%, completely contradicting the earlier judgment.

So, the same estimation-dependent method, when applied to the smart camera segment—with its wider price range and more intertwined online/offline channels—has no reason to be more reliable than in the toy segment.

IDC's situation is slightly different. As one of the most cited data agencies in consumer electronics, IDC's global shipment statistics for categories like smartphones, PCs, and tablets are standard references for industry research.

In more mature categories like smartphones and home appliances, discrepancies between IDC's shipment data and e-commerce retail data have long existed, but in the smart imaging device segment—still small in scale—even slight percentage differences appear glaring.

One easily overlooked point is that Insta360 is a publicly traded company, with every financial report and announcement subject to audit and regulatory scrutiny, making data falsification extremely costly. DJI, still privately held, relies solely on media reports for its data, with no audited financial statements for cross-verification.

The clash between these two statistical criteria is, to some extent, related to this asymmetry—one side can be verified, the other cannot.

Of course, discrepancies in criteria themselves are understandable; the issue is that these 'estimated' figures have been repeatedly cited over the past month, transforming from one perspective into industry consensus, potentially influencing investors and consumers—that is what deserves the most vigilance.

Discrepancies in data criteria are just one facet of this all-out competition.

Supply chain conflicts emerged earliest. Before Insta360's first 360-degree drone launch, key suppliers faced exclusivity pressure, with one supplier stating they could dine together but not do business. Around the same time, an Insta360 store in Changsha was required to remove its signage due to exclusivity agreements.

On pricing, DJI's first 360-degree camera, the Osmo 360, was priced nearly 800 yuan lower than Insta360's flagship X5, directly entering a market segment Insta360 had dominated for years. The price war escalated from there, with DJI offering steep discounts on multiple products during Double 11, sparking consumer backlash over price protection, with related topics trending online.

At this point, competition was bound to deepen.

In 2026, patent litigation became the new focal point. DJI first sued Insta360 in China, followed by reciprocal lawsuits in the U.S. Later, Insta360 executives publicly accused organized attacks by 'blackwater' (online troll) armies during the litigation, stating that 'organized public opinion attacks on cases still in judicial proceedings are a red line that cannot be crossed,' sharing evidence and announcing they had filed police reports.

Objectively speaking, in the broader consumer tech and internet industry, 'taking it to court' is hardly a blemish.

Temu and Shein have been suing and countersuing each other since late 2022; Didi and Meituan's Brazilian brands also faced off in court over trademarks and unfair competition.

Only competitors with significant scale and influence have the confidence to bring disputes into the courtroom.

Viewed in this context, it represents a necessary phase as China's smart imaging industry transitions from 'product competition' to 'rule-based competition.'

Ultimately, while the two companies are fiercely competing, their core strengths differ. DJI's foundation lies in gimbal stabilization and flight control systems, while Insta360's edge is in 360-degree stitching and AI imaging algorithms. These two technological DNAs point to different product logics and user scenarios.

Competition is competition, but the segment itself is still growing—far from a zero-sum game.

*The featured image and illustrations in the text are sourced from the internet.

-

![]()

Market Share Dilemma: DJI vs. Insta360—Is It '40-40' or '60-30'?

-

![]()

Market Share Dilemma: DJI vs. Insta360 – A '40-40 Split' or '60-30 Split'?

-

![]()

It's Kunlunxin's Turn to Play

-

![]()

Is the New Performance Peak Just the Starting Point? What Will Be Crystal-Optech's Next Destination?

-

![]()

Goertek Pours 69 Million Yuan into Elite Precision: Ramping Up Optical Precision Manufacturing and R&D Capabilities

-

![]()

Avatr Attempts HKEX Listing Again, With 20,000 Vehicles Sold in First Five Months

-

![]()

NVIDIA Announces 10-Fold Production Capacity Increase in 2 Years, Disrupting the Energy Storage Industry

-

![]()

AI Enters the Second Half: Models Are No Longer Scarce, What’s Truly Scarce Are Computing Power, Scenarios, and Trust