2025's First 10x Stock Arrives!

07/28 2025

07/28 2025

814

814

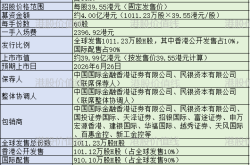

On July 28, SWANCOR once again hit a 20% daily limit, surpassing 79 yuan per share, making it the first stock to achieve a 10x return in 2025.

SWANCOR's surge also lifted the performance of the entire sector.

However, the field of robotic technology is becoming increasingly competitive.

Huawei ventured into the realm of humanoid robots long ago. Unitree's robots gained popularity during the Spring Festival Gala, and giants like Tesla and BYD have also set their sights on this burgeoning area.

From Boston Dynamics to Honda, and now to OpenAI and Microsoft, with the advent of the generative AI era, a new era of robot competition has begun.

Robots are comprised of three core technological modules: motion modules, sensing modules, and AI modules. Traditional robots often only require proficiency in one of these technologies to be effective. For instance, industrial robots primarily focus on motion control technology, while sweeping robots concentrate on navigation and sensing technology.

Humanoid robots, however, are different. They must be versatile in various application scenarios rather than performing a single task in a specific setting. This complexity necessitates higher technology integration and fusion, modeling of larger datasets, and a stronger understanding of language and instructions. Previously, AI data and models were developed in isolation, resulting in slow iteration speeds and high costs.

The popularization of large models has significantly altered this landscape.

In just a few years, the number of model parameters has skyrocketed from billions to trillions. Consequently, large models are evolving from single-modality models for text, speech, vision, etc., to general AI that integrates multiple modalities. This allows for the direct integration of speech, vision, decision-making, control, and other technologies with humanoid robots, comprehensively enhancing their capabilities.

In April 2023, AI company Levatas collaborated with Boston Dynamics to integrate ChatGPT and Google's speech synthesis technology into the Spot robot dog, successfully enabling human interaction.

The rapid evolution of underlying technologies has showcased the potential for large-scale commercialization of humanoid robots. Major global technology companies are actively making attempts and preparations. However, based on the current situation, humanoid robots still have a long way to go before truly becoming a household item.

Firstly, the capabilities of humanoid robots currently on the market are relatively limited and lack substitution benefits.

For example, household service humanoid robots do not yet possess the ability to fully replace existing human daily services; humanoid robots in the field of commercial guidance and reception can only answer simple questions and cannot respond to all inquiries raised by customers.

Given this, humanoid robots that lack rigid substitution benefits are still not very appealing to C-end consumers.

It is also evident from the product positioning of participants that the current main focus is still on exploration in B-end scenarios. For instance, the first batch of mass-produced Tesla robots will likely be deployed in superfactories; UBTECH's work is also focused on exploring the application of humanoid robots in related industrial scenarios such as new energy vehicles and 3C electronics in collaboration with enterprises.

Secondly, many shortcomings in basic technologies have yet to be addressed. For example, robot batteries need to support continuous operation for up to 20 hours, but most current humanoid robots can only operate continuously for less than 2 hours; another issue is cost, which can easily reach tens of thousands of dollars, a price that is obviously not conducive to widespread adoption. Manufacturing costs need to be reduced by 15%-20% annually in the future.

Within 3 years, humanoid robots may not present a lucrative business opportunity, but within 30 years, it is an industry that cannot be ignored. From the industry's fundamental principles, the value of humanoid robots lies in replacing high-cost human labor, which is a highly certain event.

As for the current technical and cost challenges, they will not pose long-term problems.

Take cost as an example. As commercialization progresses, any new technology and product will eventually transition from high to low prices, much like computers, smartphones, and electric vehicles have done. In the past, the cost of a single humanoid robot such as Honda's ASIMO and Boston Dynamics' Atlas was as high as US$3 million and US$1.9 million, respectively. Now, Tesla can achieve a cost of US$20,000, and this price is bound to drop further in the future.

Technology follows a similar trajectory. It will continue to iterate and upgrade. Due to the immaturity of lithium battery technology, when Boston Dynamics launched the first-generation humanoid robot Atlas in 2013, it still needed to be powered by cables. However, when the second-generation Atlas was launched in 2016, it utilized an independent lithium battery.

Musk predicts that the long-term demand for humanoid robots will reach 10 billion units. Even if only one-tenth of this expectation is ultimately achieved, the industrial space will still be incredibly impressive.

With the largest population and manufacturing industry, China is already the world's largest robot consumer market, with strong demand in both B-end and C-end markets. Furthermore, China has not lagged significantly in software and hardware technologies in the field of robots. The combination of these two factors fundamentally determines that China holds great promise in nurturing a batch of robot companies that can stand on the world stage.

Currently, the leading domestic humanoid robot enterprises are UBTECH and CloudMinds, which were founded in 2012 and 2015, respectively. Based on the current situation, compared to UBTECH and CloudMinds, the domestic humanoid robot enterprises that will truly emerge in the future are likely to be major players like Xiaomi and ByteDance. Major companies have obvious advantages in terms of talent, capital, market, and brand. Moreover, although companies like UBTECH started earlier, they have not accumulated a strong leading edge. The revenue proportion of UBTECH's humanoid robots is currently only in the single digits.

The visibility and profitability of upstream components are much stronger. Analyzing the material costs of robots, reducers, servos, and controllers account for 35%, 20%, and 15% of the cost of industrial robots, respectively, totaling 70%. Considering that humanoid robots have more joints and degrees of freedom, the proportion of these components may be even higher.

The reducer field boasts many players, including Han's Transmission, Leaderdrive, Tongchuan Technology, Zhongdalide, Guomao, etc., all of which have certain production capacities. However, Leaderdrive stands out as the leader. The company has established a virtuous development cycle of "R&D - expansion - profitability - re-R&D - re-expansion". As a manufacturing enterprise, Leaderdrive has achieved a net profit margin of over 30%, which is no mean feat.

The class differentiation in the servo motor field is relatively clear. High-end production capacity is primarily held by foreign companies such as Mitsubishi, Yaskawa, Fanuc, and Siemens. Inovance, Jiangte Electric, Jiangsu Leili, Leisai Intelligence, and Holzer are concentrated in the mid-to-low-end field, with Inovance being the absolute leader. In 2022, Inovance's market share in the domestic servo field reached 21.5%, an increase of 5 percentage points compared to 2021. With the combination of domestic substitution and the increase in robot production, Inovance's potential expectations are also relatively high.

In the controller field, domestic controller enterprises are quite dispersed. Although there are a number of professional controller enterprises such as Canopen, Wanxun Automation, Googol Tech, Invt, and Haide Control, they have not yet formed effective market competitiveness. The current domestic production rate is less than 20%, and whether they can emerge in the future remains to be seen.

In the long run, humanoid robots are a budding flower that will eventually bloom. Short-term speculation is futile. What is needed is long-term tracking and attention to identify those key enterprises.

Disclaimer

This article involves content related to listed companies, which is based on the author's personal analysis and judgment derived from information publicly disclosed by listed companies in accordance with their statutory obligations (including but not limited to temporary announcements, periodic reports, and official interaction platforms, etc.). The information or opinions expressed in this article do not constitute any investment or other business advice. Market Value Observation does not assume any responsibility for any actions taken as a result of adopting this article.

——END——

-

![]()

These new policies have taken away the livelihoods of scalpers, and car owners say they finally don't have to waste money

-

![]()

The Misunderstood Doubao: More Than Just Social Aspirations

-

![]()

Kunlunxin’s IPO: Baidu’s Strategic Move to Forge Alliances

-

![]()

AI Gives Volcano Engine a Chance to 'Change the Table'

-

![]()

AI Gives Volcano Engine a Chance to 'Change the Table'

-

![]()

A Smart Parking IPO Emerges in Xiamen with a 204% Surge on the First Day of Listing

-

![]()

Alibaba Exits Gaming Industry: A Strategic Move Forward?

-

![]()

New Car Model Faces Unprecedented Negative Campaign; Leapmotor Navigates Through Challenges Amid Profitability Concerns