Sales Slump for Two Years Running: China CEO Departs in Disappointment—Is BMW’s China Strategy a Monumental Misstep?

02/05 2026

02/05 2026

603

603

On January 30, 2026, BMW Group made a sudden announcement regarding a major personnel shift: Effective April 1, Cramer will assume the role of President and CEO of BMW Group Greater China, succeeding Gao Xiang. Gao Xiang, who has dedicated over a decade to his tenure in China, will conclude his service here and return to the group for new assignments.

Announcing a leadership transition two months in advance is unusual in itself. What further astonished observers was that Gao Xiang had only held the position for two years. His successor, Cramer, despite being a 27-year veteran of BMW Group, lacks prior experience in the Chinese market.

This "parachute" appointment starkly contrasts with the career paths of most of BMW's Greater China presidents over the past two decades. From Stefan Schober to Olaf Kastner, and from Jochen Goller to Gao Xiang, they all climbed the ranks from grassroots positions within the Chinese market.

More critically, this high-level shakeup occurs at a pivotal moment. BMW's sales in the Chinese market have plummeted by double digits for two consecutive years, with sluggish progress in electrification and intelligent transformation rapidly eroding the advantages traditionally held by luxury brands.

As "leadership change" and "loss of momentum" coincide, the future of BMW China is enveloped in a fog of uncertainty.

A Two-Year "Free Fall"

If one word could encapsulate BMW China's performance over the past two years, "free fall" would be most fitting.

2023 marked a high point for BMW China. That year, BMW sold 825,000 vehicles in the Chinese market, a record, with China remaining BMW's largest single market globally for the tenth consecutive year. However, BMW may not have realized at the time that this was the peak before a steep decline.

In 2024, BMW's sales in China dropped sharply to 714,500 vehicles, a year-on-year decline of 13.4%. This is no small drop, meaning BMW sold over 110,000 fewer vehicles in China within a year.

Yet the nightmare did not end there. When BMW China's 2025 sales data was released, the entire industry was taken aback: 625,500 vehicles, down another 12.5% year-on-year. In just two years, BMW lost nearly 200,000 sales in the Chinese market, a figure almost equivalent to the annual output of a mid-sized joint-venture automaker.

More embarrassing for BMW is that this decline is unique on a global scale. In 2025, BMW Group's global sales reached 2,463,700 vehicles, up 0.5% year-on-year. In other words, while other markets worldwide contributed to BMW's growth, China, once a "profit cow," was hemorrhaging at a double-digit rate. Among BMW's major global markets, China is the only region experiencing such a severe decline.

If the overall sales decline is alarming, the collapse of the imported vehicle business is truly shocking. According to data released by the China Passenger Car Association, BMW's imported vehicle sales in China in 2025 were only 64,000 units, a staggering 62% plunge from 171,000 units the previous year. This means that once-popular BMW flagship imported models like the 7 Series and X7 are losing their following at an alarming rate.

In fact, BMW's predicament is not an isolated case but a reflection of the collective setback faced by the entire German luxury lineup in China. In 2025, Mercedes-Benz sold 552,000 vehicles in China, down 19% year-on-year; Audi sold 617,000 vehicles, a 5.6% decline. The once-dominant "German Big Three" in the Chinese market are now experiencing their darkest hour.

The "Prisoner's Dilemma" of the Price War

Faced with sustained sales declines, BMW once attempted to demonstrate its "resolve."

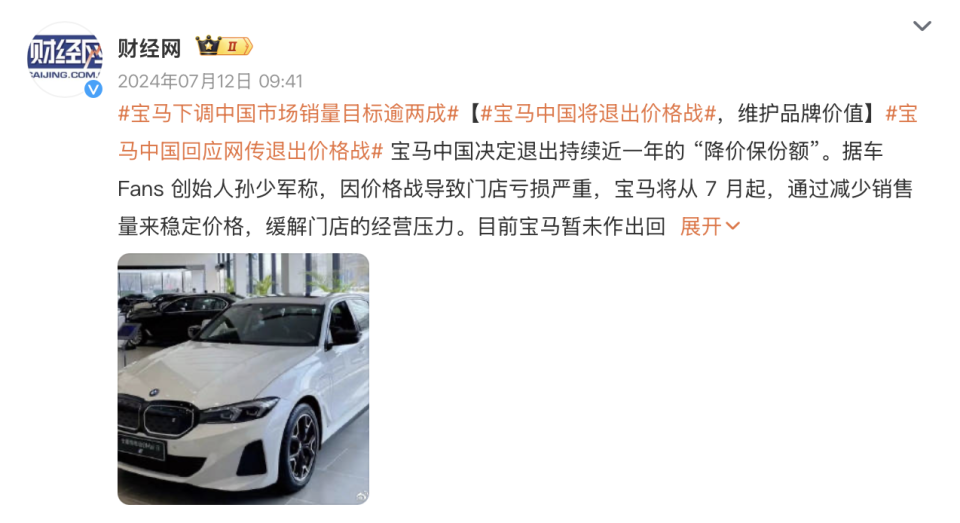

In mid-2024, BMW made a decision that sent shockwaves through the industry: leading the exit from the price war. At the time, BMW argued that prolonged price wars not only eroded profits but also undermined brand premium capabilities. This stance was interpreted by outsiders as a "rebellion" by luxury brands against endless price competition, earning BMW considerable praise for "not going with the flow."

However, reality soon dealt BMW a harsh blow.

The strategy of exiting the price war failed to stabilize sales and instead accelerated market share loss. While BMW attempted to hold the price line, Chinese domestic brands were accelerating in the fields of intelligence and electrification. Models launched by brands like BYD, AITO, Li Auto, and Zeekr not only surpassed joint venture brands in product competitiveness at similar price points but also demonstrated aggressive pricing strategies that alarmed traditional automakers.

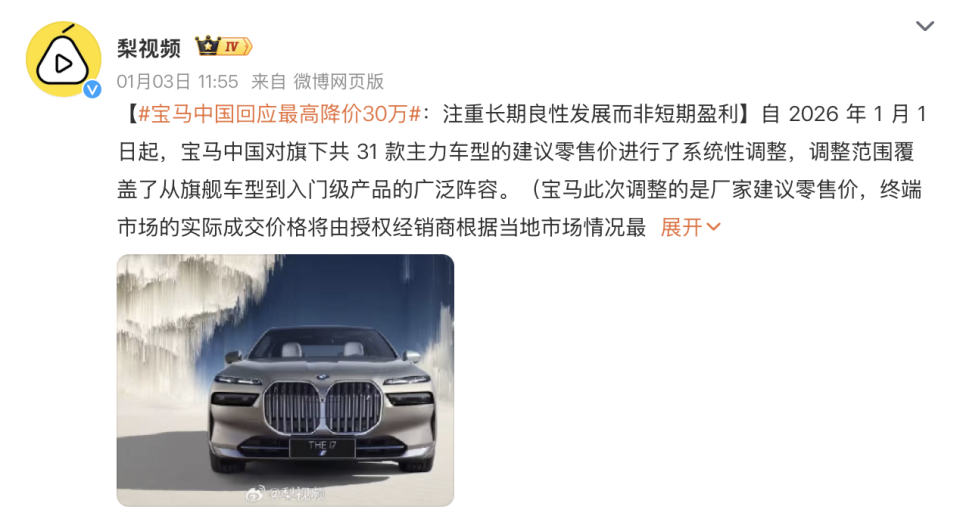

By January 1, 2026, BMW finally bowed its proud head. On this day, BMW announced a comprehensive official price reduction for 31 key models of its fuel and new energy vehicles, with maximum reductions reaching an astonishing 300,000 yuan. Such a significant official price cut is extremely rare in BMW's three-decade-plus history in the Chinese market.

The problem is that once the "anchor" of price begins to loosen, it is nearly impossible to re-fix it. BMW's dilemma is that without price cuts, sales will continue to erode; but with price cuts, brand premium will be further diluted, creating a vicious cycle. This "prisoner's dilemma" is a common challenge faced by all traditional luxury brands today.

Deeper issues also lie at the channel level. BMW relies on a traditional 4S dealership network in China, but in recent years, 4S store closures and rebrandings have become commonplace. On one hand, declining sales have made it difficult for dealers to remain profitable, leading some weaker dealers to exit; on the other hand, as the allure of traditional luxury brands fades, some dealers have begun representing new energy brands instead. The instability of the channel network further impacts BMW's sales performance, creating a vicious cycle.

A Desperate Gamble on Electrification

Amid such internal and external challenges, BMW's choice to have Cramer take the helm is undoubtedly a controversial gamble.

Cramer is no ordinary figure. Since joining BMW Group in 1998, his career has remained within the sales system. From leading MINI's German business to overseeing BMW's sales in Germany, and then coordinating sales in Nordic countries like Sweden and Norway, since March 2024, he has been fully in charge of BMW's operations in its home market of Germany. BMW Group board member Jochen Goller described him as follows: "Under Cramer's leadership, for every five BMWs sold in the German domestic market, one is a pure electric vehicle."

Electrification is precisely the core reason behind BMW's bet on Cramer.

In today's Chinese automotive market, the penetration rate of new energy vehicles has exceeded 50%. In the 300,000 to 500,000 yuan price range, the main battleground for luxury vehicles, Chinese consumers' decision-making logic is undergoing fundamental changes. They no longer focus solely on brand history and engine specifications but increasingly prioritize "soft power" such as intelligent cockpits, autonomous driving, and vehicle-to-everything connectivity. In these areas, traditional powerhouses like BMW have become the pursuers.

BMW is certainly aware of this. 2026 has been designated as BMW's "product breakthrough year," with plans to launch around 20 new BMW and MINI products in the Chinese market. Among them, high hopes are pinned on the long-wheelbase version of the new-generation BMW iX3, customized for the Chinese market. This model features a 108mm longer wheelbase and deeply integrates ecosystem applications like Huawei's HarmonyOS; its intelligent driving assistance system was developed in collaboration with China's Momenta, directly addressing BMW's previous shortcomings in intelligent driving, all to fully integrate into China's new energy vehicle market.

However, Cramer's ability to adapt to the Chinese market as BMW China's new leader is even more critical.

Unlike his predecessors, Cramer has no work experience in China or even in any Asian market. The last time BMW chose a "parachute" leader without Chinese experience to head Greater China was from 2013 to 2015 under Angelstein. That attempt was unsuccessful. In late 2014, tensions between Angelstein and BMW dealers escalated, culminating in a joint rights defense incident by dealers. BMW had to issue a massive 5.1 billion yuan subsidy to pacify the situation. While history will not repeat itself exactly, cultural differences, market awareness, and decision-making speed are all real challenges facing this German "veteran."

Cramer's European experience is undoubtedly valuable. The problem is that the Chinese market is more complex, more volatile, and more ruthless than any market in Europe. Here, one must compete not only with global giants like Tesla but also face encirclement from Chinese domestic brands like BYD, AITO, and Li Auto. These domestic brands are not only making rapid strides in product competitiveness but also demonstrating dazzling innovation speeds in marketing strategies, user operations, and ecosystem construction that leave traditional automakers bewildered.

BMW's story in China is at a critical crossroads. The loss of nearly 200,000 sales over the past two years is not just a numerical decline but a signal of the end of an era: the time when foreign luxury brands could "win easily" in the Chinese market is gone forever.

2026 will be a year to test the mettle of this "parachute" leader and determine BMW China's fate. Will it rise from the ashes or continue to decline? The answer may lie in those 20 new models set to launch.

One can only wonder how much time this rapidly changing market will give BMW and Cramer.

-

![]()

Doubao Charges Fees: Zhang Yiming Helps Zhang Xiaolong Explore the Path

-

In-depth Analysis | Wave Power Generation + Seawater Cooling: The Technological Logic Behind Panthalassa's Offshore AI Data Center

-

Chip Sector Insights | NVIDIA & Google Reveal AI Liquid Cooling Approaches, A-Share Firms Strategize Across Industrial Chain

-

Industry Insight | The Underestimated Backbone of Computing Power: The Transmission Chain of MLCC, PCB, Copper Foil, and Electronic Fabric

-

Tech News丨'Lingxi AI' Secures Hundreds of Millions of Yuan in Funding

-

![]()

Apple’s Price Hike Repercussions: Hardware Pricing Reflects the Tech Giant’s Growth Challenges

-

![]()

Xiaomi Sparks Car Modification Trend, BYD Joins In: Will the 1/4 Screw Hole Become the Automotive Industry's USB-C?

-

![]()

Enflame Tech's IPO Journey: Navigating Over 5.9 Billion Yuan in Losses and Soaring Debt in Q1 This Year