If intelligent driving is free, it will only harm the automotive industry

12/10 2025

12/10 2025

756

756

Text by Wang Miaomei, Graphic Design by Gu Qingqing, Produced by Wangjie

At this year's Horizon Technology Ecosystem Conference, two statements struck a nerve in the intelligent driving industry like needles.

The first came from Wu Yongqiao, President of Bosch Intelligent Driving Control China: 'If intelligent driving is free, it will actually cause significant harm to the industry.'

The second was from Su Qing, Vice President and Chief Architect of Horizon Robotics: 'Deep learning technology itself is starting to show signs of reaching its ceiling, and the autonomous driving industry will enter an 'extreme optimization phase' in the next three years.'

These contrasting views, presented in almost the same setting, laid bare the true situation of China's automotive intelligence on the table.

From a user perspective, intelligent driving has become an indispensable daily function.

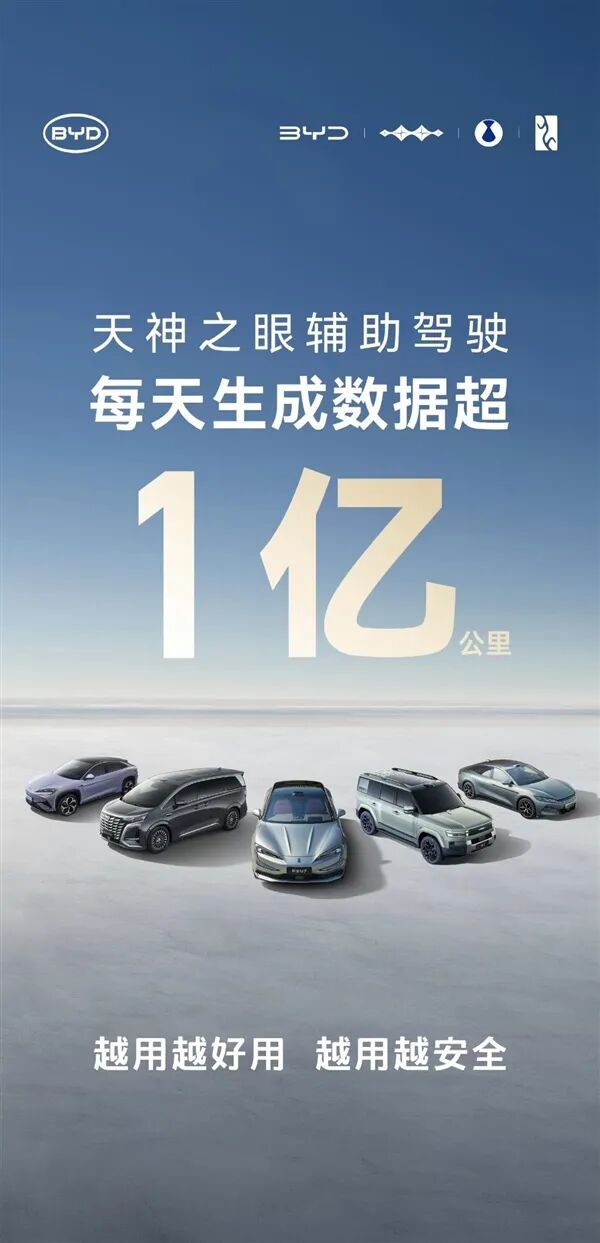

Huawei ADS has accumulated over 5 billion kilometers of assisted driving mileage, BYD's 'Divine Eye' models have sold over 2 million units, generating approximately 130 million kilometers of intelligent driving data daily. Functions like 'automatic lane changes, automatic parking, and urban assisted driving' in various scenarios are becoming increasingly smooth to use.

However, from a corporate perspective, it's a different picture: expensive chips, algorithm team salaries, training cluster costs on massive data, and long-term investment in engineering systems... If all automakers default to 'free high-level intelligent driving,' the industry won't be far from 'heavy losses.'

The question now facing the entire industry is simple: Should intelligent driving be priced? Wu Yongqiao's view is 'it must be priced; otherwise, it's a disaster.' Su Qing's judgment is 'the industry doesn't have another major breakthrough for now; caution is needed.'

On the other hand, automakers like Huawei, BYD, and Changan have reached their highest-ever investment intensity. Intelligent driving is no longer a 'selling point' but a 'fundamental.'

This article aims to bring together these facts and explain an unavoidable reality in 2025:

The business model for high-level intelligent driving must shift from 'configurations war' to 'getting users to pay.' This is a decisive issue for the continued progress of China's automotive industry.

01

Why 'Free' Is Not a Victory for the Industry

The intensity of competition in intelligent driving over the past few years is evident to all: more hardware is piled on, higher computational power is claimed, and the speed of launching urban NOA is constantly increasing.

It looks lively, but behind it lies an issue that the industry dares not delve into too deeply—the cost structure is completely unhealthy.

Wu Yongqiao's viewpoint hits the pain point because it points out not just a superficial controversy over 'pricing or not' but something more fundamental to the industry's operating logic.

He made a crucial judgment: 'If it's all free, it will actually cause significant harm to the industry and could even be a devastating blow. Every company will suffer heavy losses. How can the industry develop healthily?'

This statement needs no embellishment; it is the most genuine warning.

The essence of intelligent driving is not 'selling components' but 'selling capabilities.' This differs from traditional automotive sales of mechanical parts. Once a mechanical structure is finalized, costs are relatively stable.

However, the costs of intelligent driving are continuous, rolling, and never-ending: data must be continuously collected, models must be continuously trained, OTA updates must be continuously rolled out, liability systems must be continuously improved, and algorithm teams must be continuously invested in.

Can you expect a research and development system with a thousand-strong workforce to provide capability upgrades to users for free over the long term? Any idealism, when translated into financial statements, will be brought back to reality.

So, what the industry faces now is not whether 'free is good' but whether 'free is normal business logic.' Moreover, today's intelligent driving has a very strong positive feedback attribute. 'The more it's used, the stronger it becomes; the stronger it is, the more willing users are to use it.'

Huawei ADS's 5 billion kilometers of assisted driving mileage is the best evidence of this positive feedback. The more intense the competition in the industry, the larger the data volume, and the faster the iteration, but the costs also rise. Whoever makes intelligent driving a 'free standard feature' may seem to please users on the surface but is actually imposing unsupportable costs on the entire industry.

Some may argue that Tesla also offers standard features. However, Wu Yongqiao's quoted statement actually points out the key: 'Tesla has set a very good example for the industry in terms of FSD pricing.'

Tesla offers basic capabilities for free but charges for high-level capabilities. Its business model is clear. In China, many companies dare not charge not because their technological costs are low but because they fear others won't charge and they'll 'lose out in the competition.' This is not a business strategy but industry anxiety.

Ultimately, 'free intelligent driving' may seem user-friendly but is actually depleting the future of the entire industry.

02

Technology Is Entering an 'Extreme Optimization Phase'

At the same conference, Horizon's Vice President Su Qing poured cold water from a technical perspective, which actually strongly correlates with the 'necessity of pricing.'

Su Qing judged that there would be no new theoretical core in the autonomous driving industry in the next three years, and the industry would enter a phase of 'extreme optimization on existing systems.' He mentioned two reasons:

- The Scaling Law of deep learning has faint (impercetibly) touched its ceiling.

- The end-to-end revolution is complete, and the next theoretical breakthrough is needed.

What does this mean? It means that the past approach of 'relying on stacking computational power, models, and sensors to exchange for experiences' will become increasingly costly, while experience improvements will slow down and become more difficult.

In other words, the industry is now entering not a 'cost-reduction phase' but a 'phase of doubling cost investment.' If everyone insists on not charging during this time, it will indeed be 'tough times ahead.'

Especially with end-to-end technology becoming the consensus, training costs will rise even higher. The Deepal L06's DEEPAL AD Max uses dual-core high-computational-power chips provided by Horizon and adopts an end-to-end algorithm source similar to Tesla's FSD, with laser radar as standard across all models.

With such an aggressive technological route, expensive hardware, and direct user experience, user experience will undoubtedly be good, but the pressure on the research and development system also doubles.

The more such models exist, the more 'free intelligent driving' resembles an unsustainable commercial illusion.

Now, looking at the regulatory side. The Ministry of Industry and Information Technology and eight departments have included 'conditional approval for L3-level vehicle production access' in their regulations. This is a legal chain that truly starts with a change in liability subjects. A change in liability subjects means not just stronger technology but also greater result risks borne by automakers.

Asking automakers to bear more legal risks and double their research and development investment while still requiring them to offer it for free is logically untenable.

More critically, as the industry moves towards L3 and L4, costs tend to become service-oriented. Urban L4 pilot commercialization will likely follow a 'monthly subscription' or 'pay-per-mile' model, which is inherently an evolution of commercial logic.

From the perspective of the entire industrial chain, the arrival of the 'extreme optimization phase' is not a technological stall but a prelude to industry reshuffling.

To survive this period, companies must have stable and reliable revenue sources. Pricing for high-level intelligent driving is the most reasonable, natural, and sustainable approach.

03

Users Are Willing to Pay for Good Intelligent Driving

While the industry debates 'whether pricing is reasonable,' consumers' actual usage data has already provided an answer.

First, look at Huawei. By November 2025, Huawei ADS had accumulated 5 billion kilometers of assisted driving mileage, over 294 million assisted parking instances, and avoided more than 3 million potential collisions. These numbers are not marketing buzzwords but direct 'user votes.' If the experience were poor, no one would willingly use it daily.

Next, consider the growth of urban NOA. According to data provided by Li Wenguang, President of Yinwang Intelligent Driving Product Line, highway assisted driving mileage accounts for over 60%, assisted parking accounts for over 40%, and urban assisted driving is approaching 20% and continues to rise. Users' willingness to use it implies a willingness to pay for higher-level capabilities.

More critically, there's the experience upgrade. Urban L4 pilots are about to land, and unmanned trunk logistics commercialization will enter the stage in 2027 and 2028.

These capabilities are not 'configurations' but 'services.' Since they are services, they must have a price; since they require continuous iteration, they must have a business model.

BYD's 'intelligent driving equality' route is very typical. Although it has reduced hardware costs through economies of scale, enabling high-level capabilities in models under 100,000 yuan, it has not denied the commercial essence of the industry.

The 2 million 'Divine Eye' models have brought BYD not just sales but also 130 million kilometers of data daily. The larger the data volume, the stronger the algorithms, but the costs of machine learning and training behind it also rise.

All these indicate one thing: users are willing to pay for experiences, and the industry must charge for capabilities. Future intelligent driving cannot be 'free capabilities' but will be 'tiered capabilities + service subscriptions.' This is not a marketing model but the only realistic path for future industrial upgrading.

More importantly, as the liability subject for L3 partially shifts to automakers, the costs of high-level intelligent driving are not just algorithms and data but also legal risks, insurance liabilities, and automotive-grade safety systems.

At this stage, if automakers still insist on not charging, it's not being user-friendly but irresponsible to themselves and the industry.

Ultimately, pricing for high-level intelligent driving is not a 'price hike' but a sign of the industry entering maturity.

Summary

Pricing Is Not a Regression but the True Coming-of-Age Ceremony for Intelligent Driving

Looking back at this critical juncture in 2025, Wu Yongqiao's original statement that 'if intelligent driving is free, it will bring disaster to the industry' indeed serves as a necessary reminder before the industry moves to the next stage.

Today, intelligent driving is no longer a technological show in the lab but a system genuinely running on users' vehicles. Behind the 5 billion kilometers, 2 million units, and 130 million kilometers of daily new data stand computational power, data, algorithms, liabilities, and the long-term investment of countless engineers.

However, if the industry treats such a high-cost system as a 'free benefit,' it will inevitably lead to an outcome no one wants to see: technological stagnation, capital withdrawal, team layoffs, and industry regression. Not because the technology is inadequate but because the business model simply cannot support the industry's scale.

Horizon says the industry is entering an 'extreme optimization phase,' Huawei says users are increasingly willing to use it, policies are advancing L3 access, and BYD is bringing intelligent driving to a larger market.

These seemingly unrelated facts all connect to one common point: intelligent driving is shifting from 'technology-driven' to 'business-driven.' Only with a complete business model can the industry go further.

Pricing is not a regression but common sense; not a barrier but value; not squeezing users but ensuring the industry doesn't reverse course in the coming years.

True 'intelligent driving equality' cannot be achieved through free giveaways but must be supported by a healthy commercial cycle. Only in this way can China's intelligent driving industry maintain strong vitality before the next technological cycle arrives and continue to move forward.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving