Oracle's Enchanting 100-Day Saga: From AI Euphoria to Debt Anxiety

12/19 2025

12/19 2025

531

531

Author: Qi Xiao, Editor: Zhao Yuan

Oracle's stock price took another 5.4% hit. The immediate catalyst for this downturn was news that the funding for its data center project was not progressing as smoothly as hoped.

Although Oracle swiftly responded, asserting that the project was "still on course and progressing as anticipated," market concerns lingered.

This skepticism was not without merit, as it struck at the heart of Oracle's burgeoning debt burden, accumulated over months to fulfill a surge in orders.

Three months ago, Oracle revealed that its future order total (RPO) had ballooned to $455 billion, a figure the market perceived as embracing the "golden goose" of the AI era. Its stock price soared 36% in a single day, with its market value jumping by $244 billion overnight, briefly catapulting founder Larry Ellison to the pinnacle of global wealth.

However, when the RPO figure climbed further to $523 billion in the December 10 earnings report, the market's reaction was a post-market plunge of over 11% in the stock price.

The market's vastly divergent responses to similar positive news and its heightened sensitivity to project funding setbacks signal a shift in sentiment: the focus has shifted from future revenue to scrutinizing the "current costs." How high will the costs be to fulfill these escalating orders? What are the underlying financial risks?

I. AI Feast: Sky-High Contracts, Market Euphoria

The fervor surrounding Oracle in 2025 was ignited by a high-profile strategic move.

In January 2025, at the White House in Washington, the leaders of Oracle, OpenAI, and SoftBank, alongside U.S. President Trump, jointly announced the launch of a project dubbed "Stargate."

With a staggering total investment of $500 billion, the project aimed to construct U.S. artificial intelligence infrastructure. This was no ordinary commercial venture; it was framed as a national-level strategic initiative.

For Oracle, this meant a complete transformation of its role.

Originally, Oracle's cloud business struggled amid fierce competition from industry giants. However, since OpenAI had been seeking to bypass Microsoft—its exclusive computing power provider—to secure more and cost-effective computing resources, and in 2024, Oracle had a large data center plan in Texas vacated due to Musk's xAI project stalling, OpenAI struck a $10 billion computing power deal with Oracle.

The Stargate project further solidified Oracle's edge in the cloud business market.

Of course, a strategic blueprint alone was insufficient; the market demanded tangible contracts.

In July 2025, OpenAI officially announced on its website that it had signed an agreement with Oracle to add massive computing capacity for "Stargate," with the total value of the collaboration between the two companies exceeding $300 billion over the next five years.

This, the world's largest cloud computing contract, transformed the grand narrative into a black-and-white business deal for Oracle, placing it at the epicenter of the AI demand explosion.

At the time, the market consensus was that as long as the AI wave persisted, the demand for computing power would translate into a steady revenue stream for Oracle, effectively granting it a "super license" to strike gold in the AI era.

Reflected in financial statements, Oracle's CEO stated that the 2026 fiscal year (June 2025–May 2026) had commenced strongly, with multi-cloud database revenue continuing to grow at over 100%, and the company securing multiple large cloud service agreements, including one set to contribute over $30 billion in annual revenue starting from the 2028 fiscal year.

The capital market expressed its wild enthusiasm for this narrative through soaring stock prices.

Fueled by impressive quarterly results (cloud business revenue surging 52%) and these blockbuster announcements, Oracle's stock price repeatedly hit new highs. From its April low to its peak, Oracle outperformed most of the "AI Seven Sisters."

Especially after the collaboration details spread in July, market sentiment reached a fever pitch, with the stock price soaring over 8% in a single day. By September, the $455 billion RPO added further fuel to optimistic expectations.

The stock price frenzy at the time represented a collective upfront payment of all optimism for this seemingly inevitable future, with valuation focus placed on future revenue scale and growth rate, temporarily overlooking what Oracle would need to sacrifice to fulfill orders or interpreting high capital expenditures as a positive narrative.

II. The Cost: Tight Cash Flow, Massive Debt

The stock price surge pushed market expectations to a fever pitch. At this juncture, any hint of trouble could become the catalyst for a sentiment reversal.

For instance, in early October, news emerged that Oracle's rapidly growing cloud business had been thin on profits in the past year, such as in the first quarter of fiscal year 26 (June 2025–August 2025), where the gross margin for its business of leasing servers equipped with NVIDIA chips was less than 14%, causing Oracle's stock price to plunge over 6% intraday.

Although in mid-October, Oracle used a specific case to illustrate the profitability prospects of its AI infrastructure business—a six-year AI infrastructure project with total revenue of $60 billion, achieving a gross margin of 35%—more and more people realized the need to calculate specific cost-benefit accounts.

Coupled with factors such as a 25-basis-point interest rate cut in October failing to signal an imminently loose monetary environment, with the 10-year Treasury yield beginning to rise, increasing the appeal of risk-free assets and leading some capital to withdraw from rate-sensitive high-valuation tech and AI stocks, as well as AI giants all ramping up capital expenditures, causing the AI sector to weaken overall.

From late October to the present, Oracle's stock price has plummeted 40%. Detailed data from the second quarter of fiscal year 2026 has further convinced investors that concerns about Oracle are warranted.

This quarter, Oracle's capital expenditures were 582% of its net operating cash inflow ($2.1 billion), turning its free cash flow to approximately -$10 billion. This marked the first time Oracle had seen negative free cash flow since 1992.

The earnings call also mentioned that while maintaining the 2026 fiscal year sales target at $67 billion, capital expenditures would be raised to $50 billion, $15 billion more than previously planned.

In simpler terms, the money earned from the company's core business operations was far from sufficient to cover its investments to fulfill future orders. Oracle had to raise funds to support long-term business and growth, with financing divided into debt and equity financing, and in Oracle's management description, almost exclusively the former was considered.

In late September, Oracle raised $18 billion by issuing massive bonds, one of the largest bond issuances in the tech industry's history. According to Citi, Oracle has now become the largest issuer of investment-grade bonds among non-financial enterprises.

As of November 30, Oracle's total debt had exceeded $100 billion. Some institutions predict that if various long-term lease contracts are included, Oracle's related debt burden could approach $300 billion by 2028.

CICC Research believes that from an economic perspective, capital investments often follow the law of diminishing marginal returns. As investment scale expands, the marginal efficiency of AI investments will likely decline. However, the cost of AI investments has not decreased; one phenomenon is that since 2023, computer and information processing equipment prices have continued to rise, contrasting with the sustained decline in capital goods prices during the 1990s internet boom. This indicates that current AI investments have not yet achieved economies of scale and are still in a stage of "diseconomies of scale."

This is undoubtedly a dangerous game of betting the future on massive borrowing.

(Source: CICC Research Department)

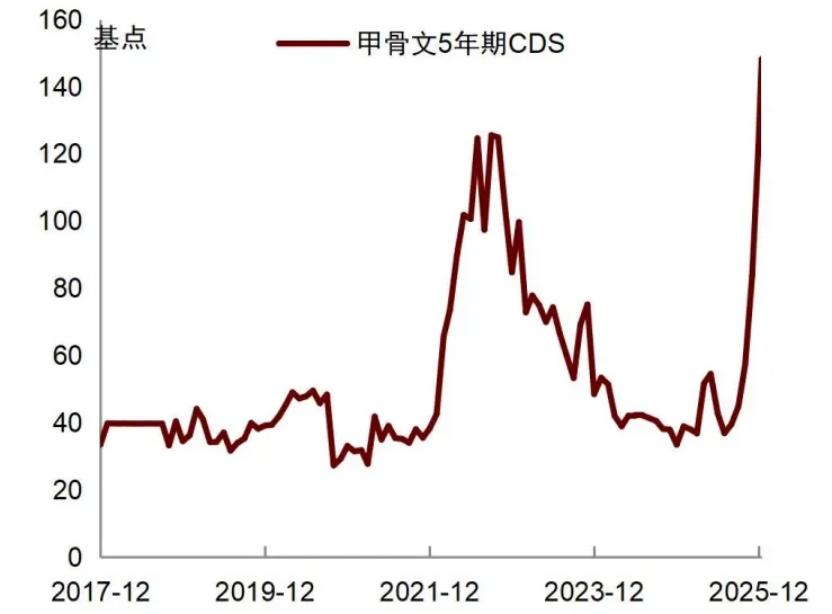

Market panic quickly manifested in a professional indicator: credit default swaps (CDS). Think of it as "insurance" against the risk of "a company being unable to repay its debts." The higher the price of this "insurance premium," the more the market worries about the company's inability to repay.

Currently, the cost of "insuring" Oracle's debt has risen to its highest level since the 2009 global financial crisis. In the 10 weeks ending December 5, related trading volume surged from $410 million a year ago to $9.2 billion, indicating a massive influx of funds trying to hedge against the risk of Oracle defaulting.

Bond investors and financial institutions, who prioritize safety, will closely scrutinize its cash flow and debt repayment ability. When they start demanding extremely high "risk insurance premiums," it shows they see major issues in the dull contract terms.

One key issue is customer concentration. Although Oracle claims a diverse customer base, OpenAI's mega contract still tightly binds its fate to this single client.

Some analysts point out that while OpenAI may have the option to choose whether to continue the partnership in a few years, Oracle's long-term data center leases signed to match the contract are difficult to cancel, putting Oracle in a passive and dangerous position.

Facing a tidal wave of questions about debt, customers, and profit margins, Oracle's management explained during the earnings call that even if OpenAI does not renew, alternative paying customers can be found; Oracle's upfront project construction expenditures will be less than (even far less than) the $100 billion the outside world has guessed; after scaling up, AI data center profit margins can reach 30%–40%, and also proposed new ideas like "customers bringing their own chips" to shift the most cash-intensive equipment investments outward and improve cash flow.

However, the market's valuation logic has fundamentally shifted: from paying for dreams in an irrationally exuberant environment to cautiously assessing the parity of returns and risks, profits and debts.

-

![]()

ByteDance, DJI, and Xiaohongshu Secure Top Three Positions Among China’s Fastest-Growing Unicorns

-

Tesla's in-car voice system in China is finally learning to 'understand human language'

-

![]()

Foreigners Are Amazed: Chinese Electric Vehicle Drive Systems Unveil Innovative 'Poses'

-

![]()

700,000 Brothers and the Future of Robots: Behind JD.com's 'Nirvana Plan'

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving