Broadcom AVGO: AI in Full Swing, Is It Outshining NVIDIA?

03/05 2026

03/05 2026

570

570

Broadcom (AVGO.O) released its Q1 FY2026 financial results after the U.S. market closed in the early morning of March 5, 2026, Beijing time (ending January 2026):

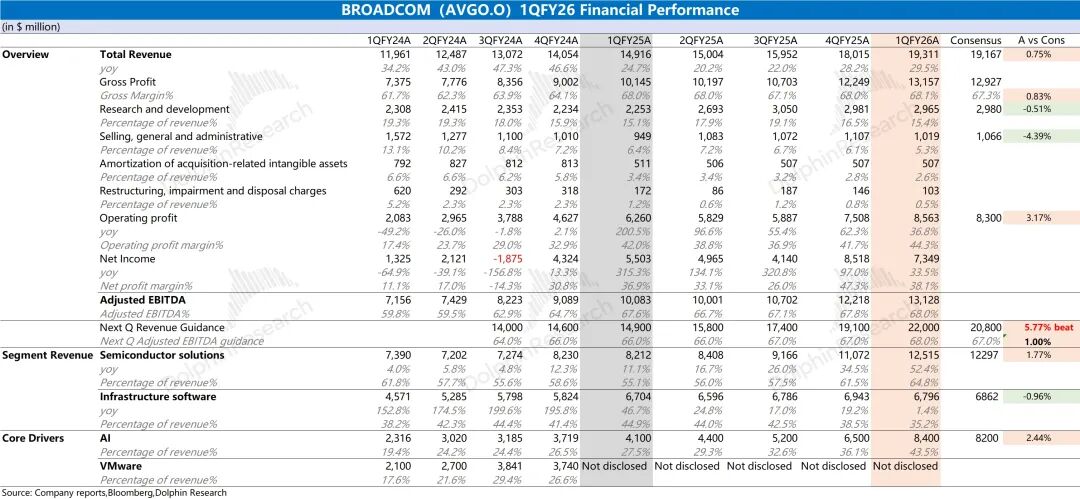

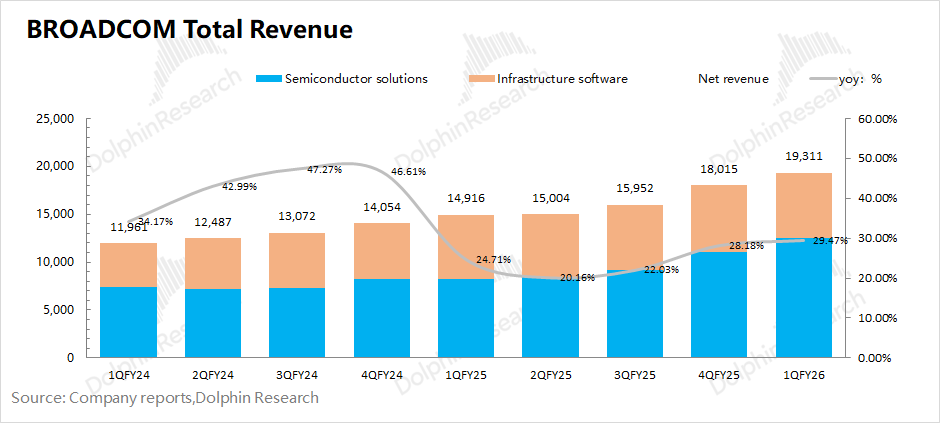

1. Overall Performance: Broadcom (AVGO.O) achieved $19.3 billion this quarter, a 29% YoY increase, meeting market expectations ($19.2 billion). The $1.3 billion QoQ growth was primarily driven by the AI business.

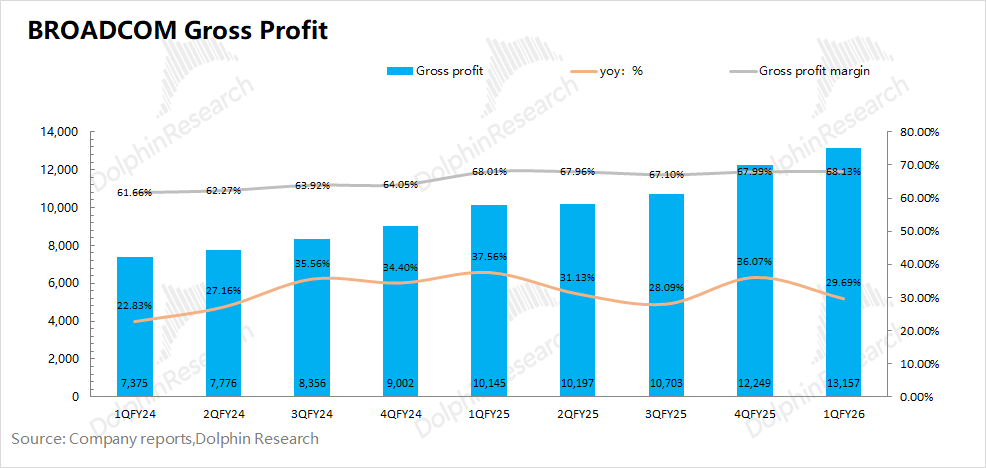

The company's gross margin this quarter was 68.1%. After excluding the impact of acquisition amortization and restructuring expenses, the actual operational gross margin was 75.8%, slightly declining QoQ (-0.8pct), mainly due to the relatively lower gross margin of the custom ASIC business and its increasing share, which brought structural impacts.

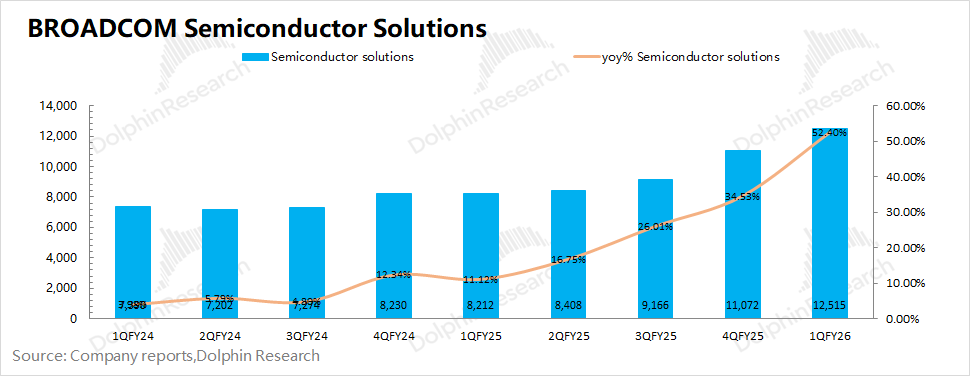

2. Semiconductor Business: Revenue reached $12.5 billion this quarter, a $1.5 billion QoQ increase, with the AI business contributing the main growth. Details are as follows:

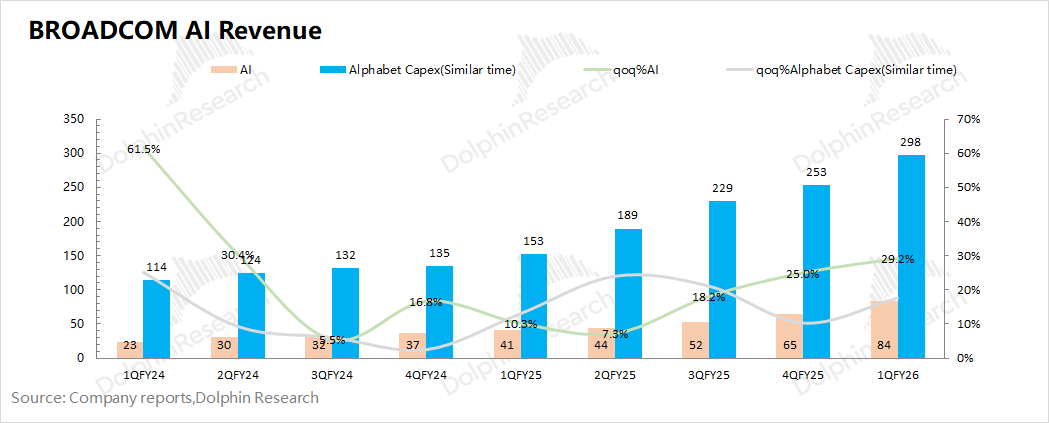

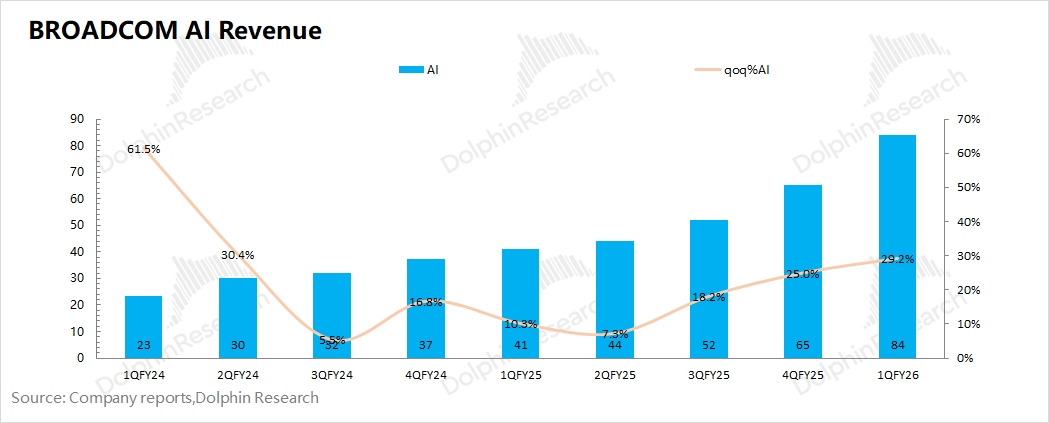

① AI Business: $8.4 billion, a $1.9 billion QoQ increase, exceeding market expectations ($8.2 billion). The company's AI revenue comes from three major customers (Google, Meta, and ByteDance), with quarterly growth primarily driven by increased shipments of Google's TPU.

Major companies like Google and Meta have recently raised their capital expenditure outlooks for 2026. Broadcom's AI business growth is expected to continue accelerating, with the company expecting AI business revenue to reach $10.7 billion next quarter, a $2.3 billion QoQ increase.

② Non-AI Business: $4.1 billion, roughly flat YoY, showing stable overall performance.

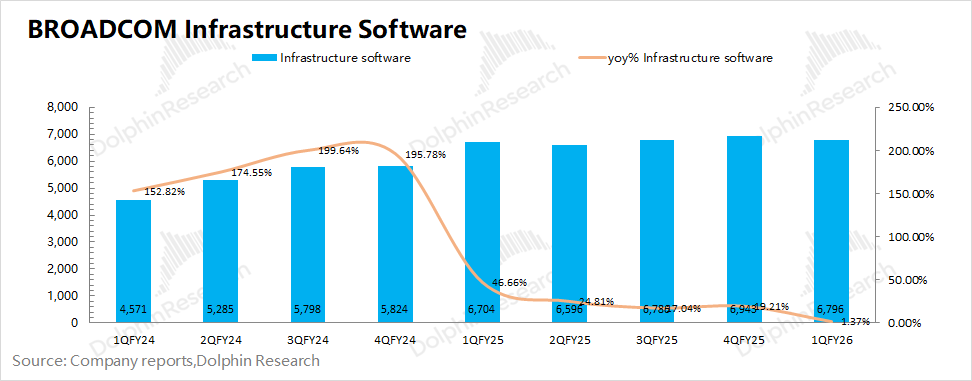

3. Infrastructure Software: Revenue reached $6.8 billion this quarter, a 1.4% YoY increase. Previous growth was mainly driven by the VMware merger integration and pricing model adjustments (a full shift from permanent license mode to subscription mode). The high growth from the merger has ended, and future software business growth will primarily focus on the organic growth of VMware's subscription model.

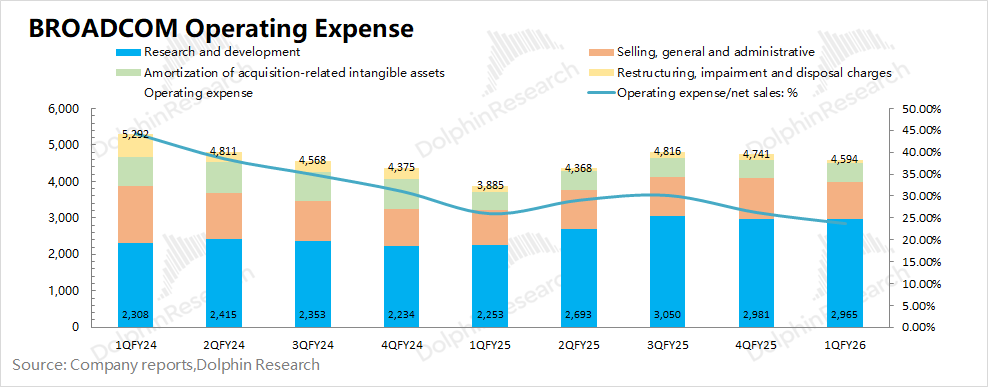

4. Operating Expenses: Core operating expenses (R&D expenses + sales and administrative expenses) were $3.98 billion this quarter, slightly declining QoQ. Affected by scale effects, the core operating expense ratio dropped to around 21%.

In operating expenses over the past two years, the company has significantly increased equity incentive-related expenditures (currently accounting for nearly half). Excluding the impact of equity incentives, the company's core operating expenses this quarter were $2.04 billion, a $0.09 billion QoQ decrease.

5. Inventory: The company's inventory this quarter was $2.96 billion, a 30% QoQ increase. Compared to past single-digit QoQ growth, this significant increase is not a concern, as it is mainly due to strong demand and the company's preparation for advance stockpiling.

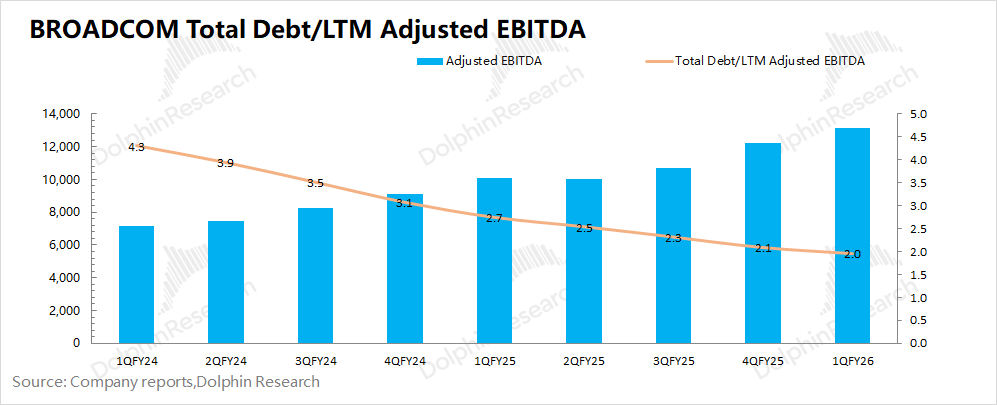

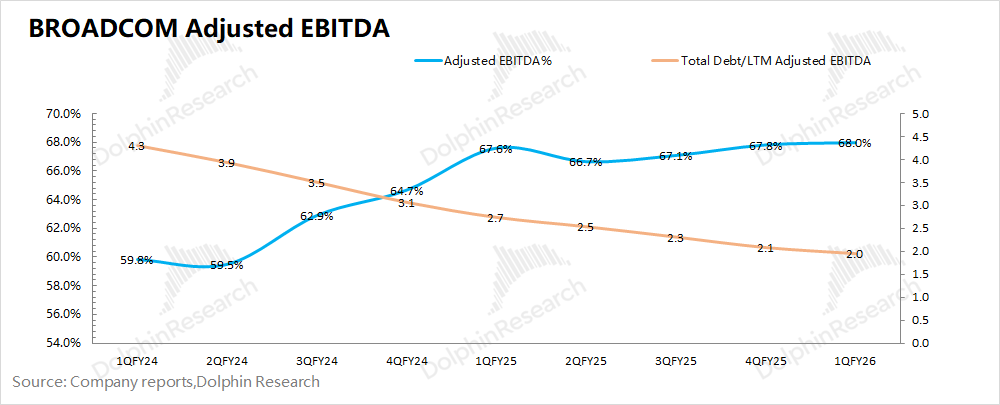

6. VMware Integration Progress: Dolphin Tab introduced the debt repayment metric (Total Debt/LTM Adjusted EBITDA), which further declined to 2 this quarter. This metric has returned to pre-acquisition levels, indicating that the impact of the VMware acquisition on the company's debt has been digested within two years.

7. Broadcom's Guidance: Revenue is expected to be around $22 billion in Q2 FY2026, exceeding market expectations ($20.8 billion). The company expects an adjusted EBITDA margin of 68% in Q2 FY2026, better than market expectations (67%), with the AI business expected to continue growing to $10.7 billion.

Dolphin Tab's Overall View: AI Growth Accelerates, Clear Guidance Injects Confidence

Broadcom AVGO's revenue and gross margin this quarter met market expectations. Revenue growth was primarily driven by the AI business. In terms of gross margin, after excluding the impact of acquisition amortization and restructuring expenses, the actual operational gross margin was 75.8%, slightly declining QoQ due to the structural impact of the increasing share of the lower-margin ASIC business.

Regarding next quarter's guidance, the company expects revenue to reach $22 billion, a $2.7 billion QoQ increase, exceeding market expectations ($20.8 billion), with growth primarily driven by the AI business.

1) Impact of Acquisition: The company's debt repayment metric (Total Debt/LTM Adjusted EBITDA) declined to 2 this quarter, returning to pre-acquisition levels. The impact of the VMware acquisition on the company's debt has been digested within two years.

2) AI Performance: The company achieved $8.4 billion in AI revenue this quarter, a $1.9 billion QoQ increase. The company expects AI revenue to reach $10.7 billion next quarter, a $2.3 billion QoQ increase, exceeding market expectations ($9.7 billion).

After the integration of VMware, the market primarily focuses on Broadcom AVGO's progress in the AI business:

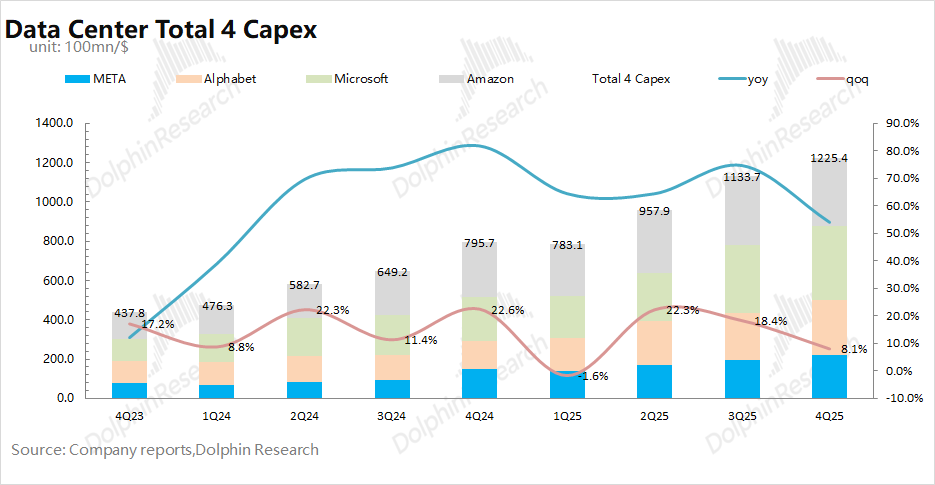

a) Capital Expenditures by Major Companies as the "Driving Force": Large cloud service providers are the main "buyers" of Broadcom AVGO's custom ASIC chips, directly affecting expectations for the company's AI business.

Combining guidance from major companies, Dolphin Tab expects the total capital expenditures of the four core cloud providers (Google, Meta, Microsoft, and Amazon) to reach $660 billion in 2026, with a YoY growth rate exceeding 60%, ensuring growth in the AI chip market in 2026.

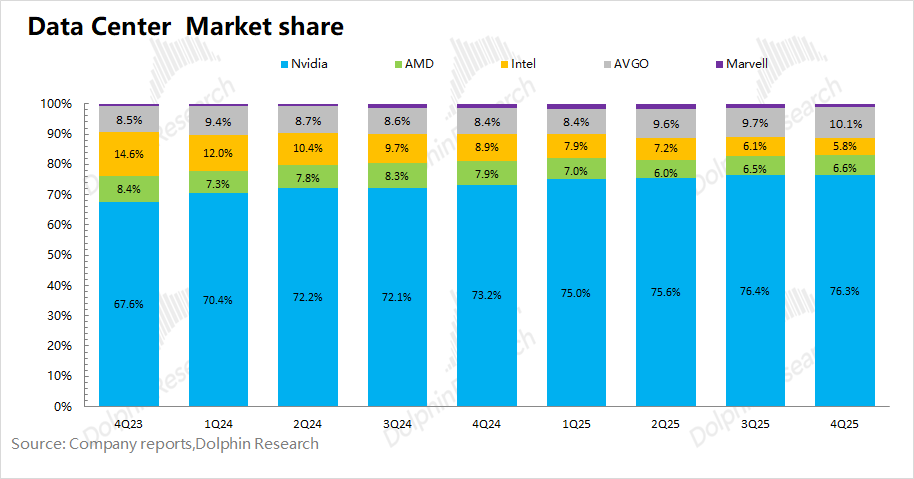

b) AI Chip Market Share: NVIDIA remains the absolute leader in the AI chip market, with Broadcom AVGO playing a "catch-up" role.

Currently, Broadcom AVGO holds around a 10% share in the AI chip market. Driven by demand for Google's TPU and Anthropic, the company's share is expected to rise to around 20% in the future, showing an upward trend.

c) Product Iteration: Broadcom AVGO has secured orders from customers like Google, Meta, and OpenAI. Google's TPU is currently the company's core product, and its performance directly impacts the growth of the company's AI business.

Currently, TPUv7 has started mass production and shipments. Compared to NVIDIA's GPU, TPUv7's performance in areas like FP8 is roughly on par with NVIDIA's B200 (mass-produced in Q4 2024), with Google's TPU roughly lagging behind NVIDIA by about a year.

The biggest differences between Google's TPU and NVIDIA's GPU currently are: ① Google currently only supports up to the FP8 domain, focusing more on stability and large-scale cluster efficiency; ② NVIDIA pursues speed, introducing the NVFP4 format in the Blackwell series, doubling inference performance based on FP8.

Considering (a+b+c), downstream major companies are still increasing capital expenditures, and Broadcom AVGO's market share is also rising. Why has the company's stock price remained "flat" recently? Dolphin Tab believes it is mainly due to market concerns about the uncertainty of major companies' subsequent capital expenditures.

Taking Meta as an example, the company's management provided guidance for capital expenditures of $115-135 billion in 2026, equivalent to more than 50% of Meta's full-year revenue, far higher than the previous range (20-25%). Similarly, the capital expenditure ratios of companies like Google and Microsoft will rise to 40% or more.

Meta's revenue growth is generally around 15-20%, while capital expenditures/expected revenue in 2026 has reached 50-60%, with limited room for further increase. This means that the high growth in major companies' capital expenditures is unsustainable.

As a result, the market generally expects major companies' capital expenditure growth to decline significantly around 2027, ending the industry's "high growth, high valuation" phase. For Broadcom AVGO in FY2026, it is a stage of performance growth and valuation digestion, with the company's current valuation dropping below 30x.

The above mainly reflects industry-level challenges, especially those faced by NVIDIA. A more specific issue for Broadcom is that while it is a cost-saving option for cloud service providers, companies like Google may further outsource to Taiwanese manufacturers or develop in-house solutions.

For example, Broadcom's major customer Google is developing the next-generation TPUv8 in parallel with Broadcom AVGO and MediaTek (MTK). If existing customers do not place additional orders, the market may worry about orders being shifted to alternative solutions like Taiwanese manufacturers.

The growth in orders from existing customers is one of the questions the company needs to address. At the same time, unlike NVIDIA's increasingly high gross margins as the AI business grows, Broadcom's gross margin is structurally declining, which is also a major market concern.

Combining Broadcom AVGO's current market cap ($1.5 trillion), it corresponds to around 27x PE for the company's core operating profit after tax in FY2026 (assuming YoY revenue growth of +74%, actual operational gross margin of 72%, and a tax rate of 9.7%).

Referring to the industry chain, Broadcom AVGO's valuation is still higher than NVIDIA's (20x PE). The relatively high valuation reflects the potential opportunities for ASIC to gain market share, but the overall industry valuation has significantly declined.

Regarding future growth, the company's management explicitly provided AI guidance for 2027, with six major AI core customers (Google, Anthropic, Meta, OpenAI, etc.) having a combined computing power demand of nearly 10GW, roughly corresponding to over $100 billion in AI revenue.

Clear guidance can alleviate market concerns to a certain extent and boost short-term confidence. More importantly, management can provide more detailed explanations (including Taiwanese manufacturers/in-house development, gross margin performance), which are the main factors suppressing the company's valuation.

Here is a detailed analysis:

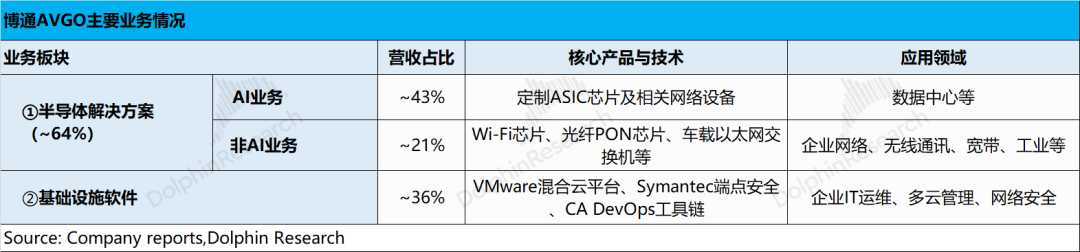

I. Broadcom's Main Business Overview

Broadcom's previous performance growth was primarily driven by the AI business and the acquisition and consolidation of VMware. Therefore, the custom ASIC chips in the AI business and VMware's pricing adjustment strategy are the market's main concerns. From a business perspective:

1) Semiconductor Solutions: Mainly benefited from growth in AI revenue, driven by demand for custom ASICs from customers like Google, Meta, and ByteDance. Other non-AI businesses remained roughly flat.

AI Business: Currently, the main growth comes from shipments of Google's TPU. The company has six major AI core customers (including Google, Anthropic, Meta, OpenAI, etc.), with OpenAI becoming a substantial customer.

For the 2027 outlook, the combined computing power demand of the six major customers is close to 10GW, bringing in over $100 billion in AI revenue. Anthropic's computing power demand exceeds 3GW, and OpenAI will mass-produce its first XPU (with computing power exceeding 1GW).

2) Infrastructure Software: VMware consolidation, with software revenue accounting for nearly 40% of the total. The company adjusted pricing strategies for VMware's customers, with price increases driving revenue growth, but this impact has significantly weakened.

II. Overall Performance: AI as the Core Driver

2.1 Revenue

Broadcom (AVGO.O) achieved revenue of $19.3 billion in Q1 FY2026, a 29.5% YoY increase, meeting market expectations ($19.2 billion). The YoY growth was primarily driven by the AI business.

On a QoQ basis, the company's revenue increased by $1.3 billion this quarter, with the AI business contributing a $1.9 billion QoQ increase, while the software business declined slightly QoQ.

2.2 Gross Margin

Broadcom (AVGO.O) achieved a gross profit of $13.2 billion in Q1 FY2026, a 30% YoY increase. The company's gross margin this quarter was 68.1%, slightly increasing QoQ.

After excluding the impact of acquisition amortization and restructuring expenses, the actual operational gross margin was 75.8%, declining by 0.8pct QoQ, mainly due to the relatively lower gross margin of the custom ASIC business and its increasing share, which brought structural impacts.

2.3 Operating Expenses

Broadcom (AVGO.O) had operating expenses of $4.6 billion in Q1 FY2026, slightly declining QoQ.

Excluding equity incentives, the company's core operating expenses (R&D expenses + selling and administrative expenses) for the quarter were US$2.04 billion, a decrease of US$90 million from the previous quarter. After completing the consolidation of VMware, the company's focus on reducing operating expenses has been largely accomplished.

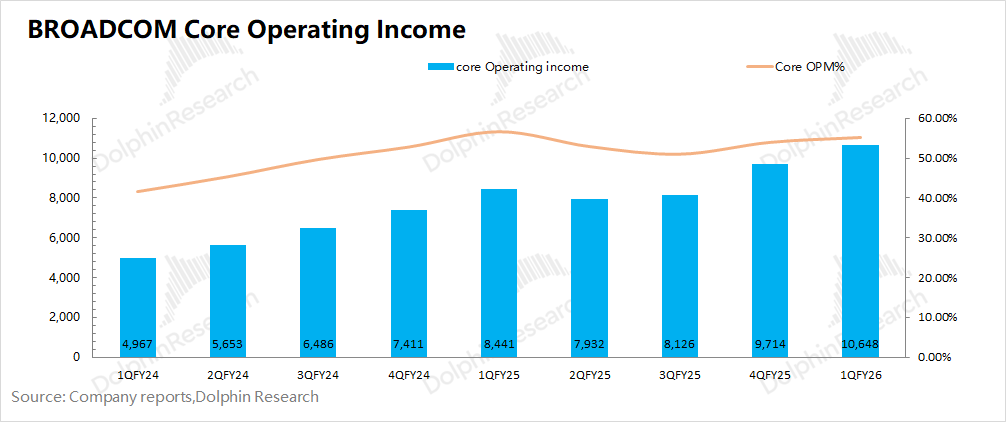

2.4 Profit Performance

Broadcom (AVGO.O) achieved a net profit of US$7.35 billion in the first quarter of fiscal year 2026.

Compared to net profit, Dolphin Research believes that core operating profit (= gross profit - R&D expenses - selling and administrative expenses) better reflects the company's true operating performance. Broadcom (AVGO) achieved a core operating profit of US$10.65 billion this quarter, an increase of US$900 million from the previous quarter, primarily driven by growth in its AI business.

2.5 Broadcom's EBITDA

As Broadcom excels in external mergers and acquisitions, the company typically uses adjusted EBITDA% as one of its key operational performance indicators. Dolphin Research estimates that the company's adjusted EBITDA% rebounded to 68% in the first quarter of fiscal year 2026, aligning with the company's prior guidance (67%).

Further examining the company's debt repayment capacity, the ratio of total liabilities to LTM Adjusted EBITDA continued to decline to 2 this quarter. Driven by growth in AI performance, this ratio has returned to pre-acquisition levels. This indicates that the impact of the company's acquisition of VMware has been fully absorbed over the past two years, and the company may now begin seeking new merger and acquisition opportunities.

III. Business Segment Performance: Six Major Clients to Contribute Billions in AI Revenue

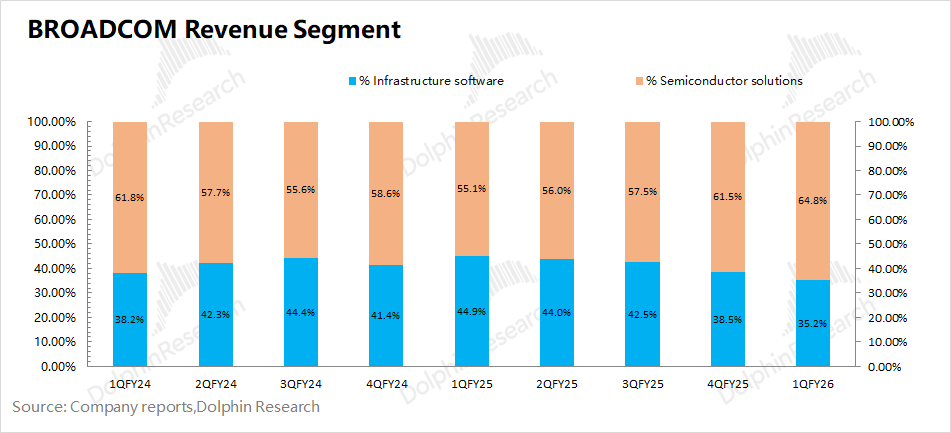

Broadcom (AVGO.O) operates primarily in two main business segments: semiconductor solutions and infrastructure software.

These two broad categories specifically include: 1) Semiconductor Solutions: networking (AI business), wireless, storage connectivity, broadband, industrial, and others; 2) Infrastructure Software: VMware, CA, Symantec, Brocade, etc.

3.1 Semiconductor Solutions

Broadcom (AVGO.O) generated US$12.5 billion in revenue from semiconductor solutions in the first quarter of fiscal year 2026, representing a year-over-year increase of 52%. The growth in the company's semiconductor business this quarter was primarily driven by the AI segment, while non-AI businesses remained stable.

1) AI Business

The AI business is currently the focal point of the company's performance. In this quarter, the company's AI revenue reached US$8.4 billion, a quarter-over-quarter increase of US$1.9 billion, with growth accelerating once again, primarily driven by shipments of Google's TPU.

Currently, the company's AI revenue comes from three major clients (Google, Meta, and ByteDance). With major companies like Google and Meta successively increasing their capital expenditures, the company's AI revenue growth is expected to accelerate further. The company projects AI revenue of US$10.7 billion next quarter, a quarter-over-quarter increase of US$2.3 billion.

Broadcom's ASIC business has explicitly announced six clients: Google, Meta, ByteDance, Anthropic, a fifth client (contributing US$1 billion), and OpenAI, which was added this quarter. This signifies that the "previous framework agreement" is now being implemented, and OpenAI will also become a substantive client.

For the medium- to short-term performance of the AI business, attention remains focused on the product performance of the current three clients, particularly the mass production status of Google's TPUv6 and TPU v7. As for orders from Anthropic and the fifth client (contributing US$1 billion), deliveries will not begin until the second half of 2026. The company's AI business performance for the full year is expected to be "lower in the first half and higher in the second half."

Regarding market concerns about the uncertainty of subsequent growth, the company's management explicitly provided an outlook for the AI business in 2027: the company already has six major AI core clients (Google, Anthropic, Meta, OpenAI, etc.), with a combined computing power demand approaching 10GW by 2027, capable of generating over US$100 billion in AI revenue. Among them, Anthropic's computing power demand exceeds 3GW, and OpenAI will mass-produce its first XPU (with computing power exceeding 1GW).

This clear outlook will inject confidence in the short term. However, it cannot be overlooked that the proportion of capital expenditures among core cloud providers is already relatively high. In particular, Meta's capital expenditure-to-revenue ratio will exceed 50% in 2026, leaving limited room for further increases. This remains the primary factor suppressing the company's/industry's valuation.

2) Non-AI Business

The company's non-AI semiconductor business revenue was US$4.1 billion this quarter, remaining essentially flat year-over-year.

The company's non-AI businesses primarily include enterprise storage, broadband, wireless, and industrial and other segments. Specifically, revenue from enterprise networking, broadband, and server storage increased year-over-year this quarter, offsetting the seasonal decline in the wireless business.

3.2 Infrastructure Software

Broadcom (AVGO.O) generated US$6.8 billion in revenue from infrastructure software in the first quarter of fiscal year 2026, representing a year-over-year increase of 1.4%. The impact of the previous VMware merger and integration has now been fully absorbed, with future attention focused on organic business growth.

Broadcom's software business is primarily divided into two parts: VMware and the original software businesses of CA & Symantec & Brocade. Since the original software businesses of CA & Symantec & Brocade maintain quarterly revenues of approximately US$2 billion, the main focus of the company's software business is on the acquired VMware.

Regarding the impact of VMware on the company's performance, Dolphin Research believes it primarily manifests in two ways: "financial absorption progress of the merger" and "the full transition from permanent licenses to a subscription model." Based on the software business performance this quarter, Dolphin Research expects VMware to have generated approximately US$4.6 billion in revenue this quarter.

Currently, the proportion of license users transitioning to the subscription model has exceeded 85%. With the increasing penetration of the subscription model, VMware and software business revenues are still expected to grow, but it is unlikely to achieve the high growth rates seen during the merger and integration phase.

Given that the current debt repayment metric has declined to 2, the acquisition of VMware has been fully absorbed by the company. The company will no longer separately disclose detailed VMware data, with the AI business now being the primary focus.

- END -

// Reprint Authorization

This article is an original piece by Dolphin Research. Reprinting is permitted only with authorization.

// Disclaimer and General Disclosure

This report is intended solely for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial status, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are intended for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or viewpoints mentioned in this report shall not, under any jurisdiction, be regarded or construed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and data contained in this report are not intended for or proposed for distribution to jurisdictions where such distribution, publication, provision, or use of the information, tools, and data would conflict with applicable laws or regulations, or would result in Dolphin Research and/or its subsidiaries or affiliated companies being subject to any registration or licensing requirements in the relevant jurisdiction, nor are they intended for citizens or residents of such jurisdictions.

This report merely reflects the personal viewpoints, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Smartphone Prices Surge Amid Manufacturer Anxiety

-

![]()

Orbbec Soars to Record Heights, Eyes Further Capital Influx of 980 Million!

-

![]()

Tongding Interconnect Sets Up Shop in Shaoguan with 800 Million Yuan in Registered Capital

-

![]()

Before Kimi’s A-Share Debut, Zhipu Aims to Secure More 'Strategic Funding'

-

![]()

Innovative Leap | Fiber-Pluggable 1470nm Laser Source: Revolutionizing Precision Laser Weeding

-

![]()

73-Day Rapid Listing: Where Does Unitree's Wang Xingxing's 'Sense of Urgency' Come From?

-

![]()

AI Project Mindverse, Backed by Meituan, Faces Data Inflation Allegations Over Its Macaron Product

-

![]()

3000-word In-Depth Analysis | What Makes Physical AI So Magnetic? It Has Captivated Masayoshi Son, Jensen Huang, and Justin Sun All at Once