Insights from Unitree Robotics' Prospectus: The Survival Race Among Embodied AI Players in China and Abroad

03/24 2026

03/24 2026

513

513

As embodied AI transitions from national strategic blueprints to industrial practice, competition in the two core sectors of humanoid and quadruped robots has moved beyond laboratory "showmanship" and entered a critical phase of commercialization "struggle."

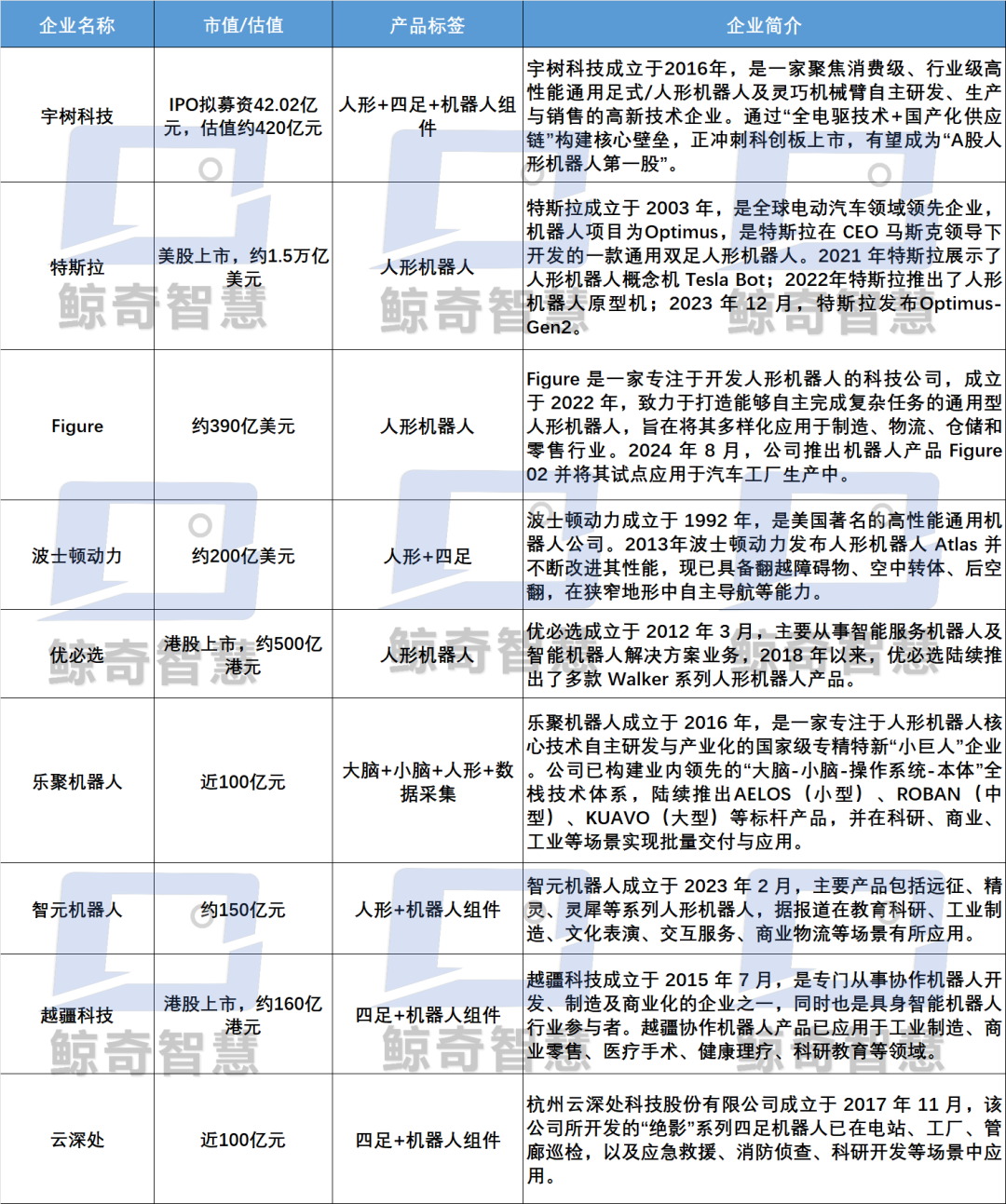

On March 20, Unitree Robotics' IPO application for the STAR Market was officially accepted by the Shanghai Stock Exchange. Dubbed by the industry as the "first A-share humanoid robot stock," Unitree's prospectus not only serves as a scorecard for its "mass production breakthrough" but also reveals that the company views eight embodied AI robotics firms—including Tesla, Boston Dynamics, UBTECH, Leju Robotics, and Zhiyuan Robotics—as its core competitors at the strategic level.

This inadvertently outlines a landscape where Chinese and foreign players showcase their strengths along divergent paths in the embodied AI industry, revealing the underlying logic of the industry's shift from "technological competition" to "ecosystem rivalry."

Unitree Robotics' "Ambition"

As a global leader in delivering embodied AI solutions, Unitree Robotics' STAR Market IPO bid is underscored by core data across multiple dimensions in its prospectus, confirming its commercialization prowess and reflecting the explosive growth potential of the global embodied AI industry.

The prospectus reveals that Unitree Robotics specializes in the R&D, production, and sales of high-performance general-purpose humanoid robots, quadruped robots, and core components. It has established a full-scenario product matrix encompassing humanoid, wheeled, and quadruped robots. Leveraging dual advantages of "performance + mass production," it has become a benchmark for industrialization in China's embodied AI sector.

On the business front, Unitree's strategy is highly targeted toward "mass production and delivery": the company focuses on humanoid and quadruped robots along with core components, extending to key parts such as collaborative robotic arms, LiDAR, and dexterous hands, forming a closed-loop, self-controlled full industry chain.

Official data shows that in 2025, the company shipped over 5,500 humanoid robots, securing the global top spot; cumulative sales of quadruped robots exceeded 30,000 units, leading the global market share. More critically, from January to September 2025, revenue from humanoid robots surpassed that of quadruped robots for the first time, accounting for 51.53%, signaling a strategic shift in the company's growth drivers.

Financially, Unitree Robotics' main business revenue climbed from RMB 123 million in 2022-2024 to RMB 1.167 billion in 2025, with full-year 2025 revenue reaching RMB 1.708 billion, a staggering 335.36% YoY surge. Net profit after non-recurring items soared from RMB 77.5036 million in 2024 to RMB 600 million, a 674.29% YoY increase, clearly highlighting a profitability turning point. This is a rarity in the still "money-burning" embodied AI industry.

Upon closer inspection, this impressive "scorecard" is supported by dual pillars of scaled-up mass production and supply chain optimization. Through self-developed core components and open supply chain collaborations, Unitree has reduced quadruped robot prices to below RMB 10,000 and set the starting price for humanoid robots at just RMB 29,900, creating an overwhelming cost advantage.

Additionally, Unitree's prospectus explicitly identifies, for the first time at the corporate strategic level, core competitors such as Tesla, Figure, UBTECH, Zhiyuan Robotics, Leju Robotics, Deep Robotics, and Dobot. Given the current global competition landscape in embodied AI (with overseas players like Tesla, Figure, and Boston Dynamics focusing on technological depth, while domestic firms like UBTECH, Zhiyuan, and Deep Robotics prioritize mass production), this list adds a hint of competitive "bloodshed."

Note: Data sourced from publicly available online information and industry report estimates, compiled by Jingqi Intelligence for reference only.

Unitree's IPO prospectus is essentially a "declaration of strength" from China's mass production camp to the global industry. Through this declaration, it is clear that the core of global embodied AI competition has shifted from single-dimensional technological parameter comparisons to a comprehensive ecosystem rivalry encompassing "technology + mass production + scenarios."

China Leads in Humanoid Robot Sales as Global Commercialization Race Intensifies

As the "ultimate evolutionary path for artificial general intelligence" and the "most representative track (sector)" of embodied AI, humanoid robots represent the future and have naturally become the most fiercely contested area in global tech rivalry.

Beyond financial and business data, Unitree's prospectus also outlines the immense potential of the industrial sector. Related projections indicate that by 2030, the global humanoid robot market will reach USD 15 billion, with sales exceeding 605,700 units. China's market will approach RMB 38 billion in size, with sales of 271,200 units, accounting for nearly half of the global market.

Using these projections as a benchmark, the industry is still in the early stages of commercialization exploration and has yet to achieve large-scale adoption. However, as Unitree Robotics' prospectus reveals, Chinese and foreign companies have already taken divergent paths—China focuses on mass production, while the U.S. emphasizes technology, setting the stage for a "speed vs. depth" race.

Note: Data sourced from publicly available online information and industry report estimates, compiled by Jingqi Intelligence for reference only.

Currently, overseas players are trapped in a dilemma of "technological leadership but commercialization lag." While Tesla's Optimus and Figure 01 maintain technological leadership, and Boston Dynamics sits firmly at the technological pinnacle, their products remain stuck in prototype iteration and pilot deployment phases. They face challenges of high mass production costs and limited deployment scenarios, relying heavily on venture capital infusions. Their mass production shipment volumes lag far behind domestic firms.

In contrast, domestic Chinese companies have broken free from the "prototype demonstration" cycle, focusing instead on "real-world scenario validation and deployment" and "full-chain integration." They have accumulated valuable scenario data and deployment experience, forming closed loops from supply chains to hardware, models, and products. This pursuit of a virtuous cycle between technological deployment and commercialization represents a systemic advantage that overseas firms struggle to replicate.

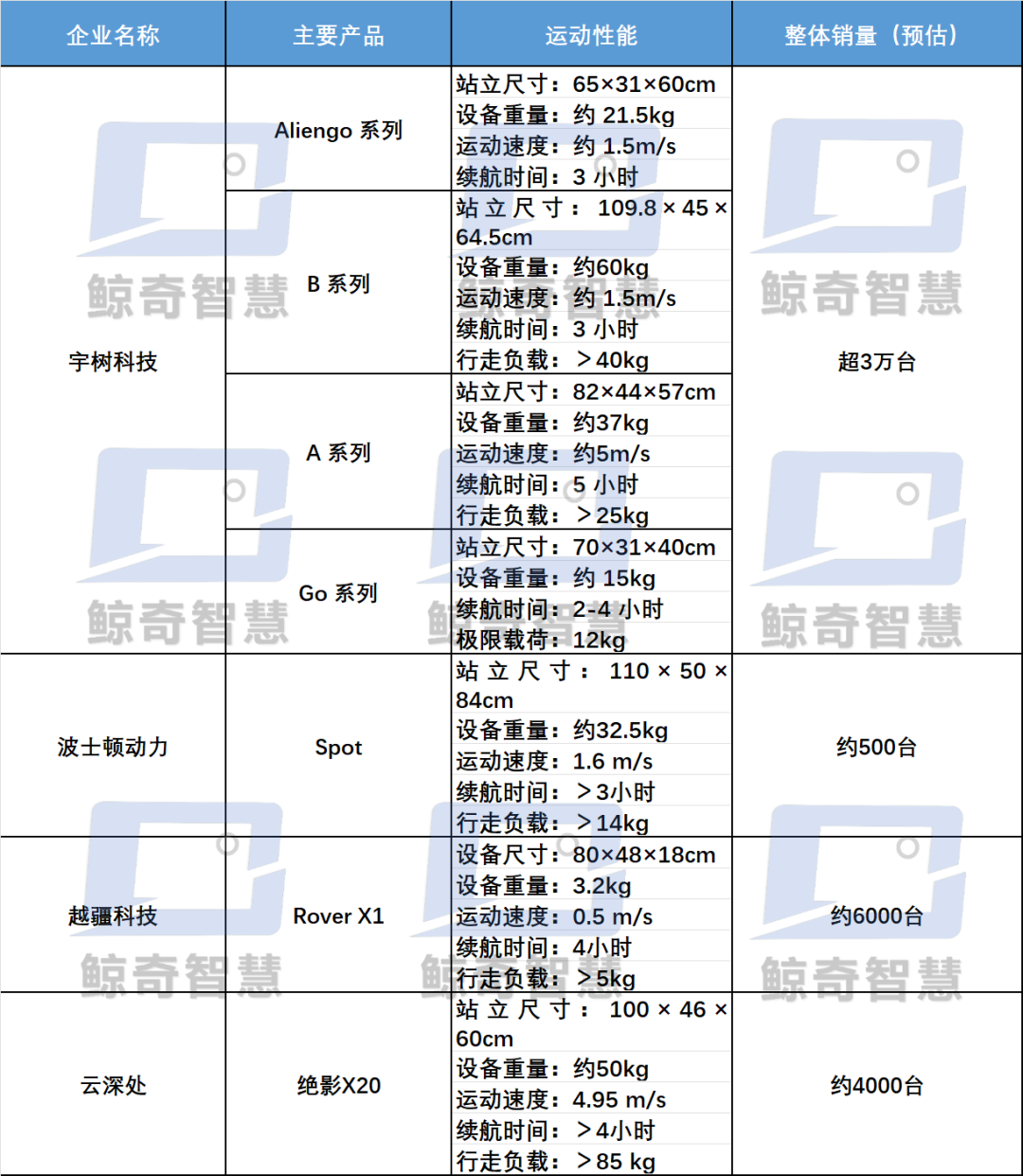

Data shows that Chinese humanoid robot shipments account for nearly 80% of the global total. A few embodied AI firms, including Unitree Robotics, Zhiyuan Robotics, UBTECH, and Leju Robotics, each surpassed 1,000 units in shipments in 2025. Unitree leads globally with 5,500 units shipped, while UBTECH has secured over RMB 1.4 billion in orders, planning to boost production capacity to 10,000 units this year.

This has subtly shifted the core competitive logic of humanoid robots from "whose technology is flashier" to "who can deliver products and iterate continuously." The ability to balance "technological iteration speed" with "mass production efficiency" may emerge as a key determinant of influence in the humanoid robot sector.

Quadruped Robot Rivalry: Technological Premium vs. Scale Dividends

If humanoid robots represent the "future battle," then quadruped robots (or robotic dogs) are the "present war."

Beyond the aforementioned content, Unitree's prospectus also highlights the potential of the quadruped robot (dog) sector: global sales of quadruped robots are projected to exceed 560,000 units by 2030, with a market size surpassing RMB 8 billion. China's market is expected to reach nearly 400,000 units in sales, accounting for 71% of the global total, and a market size exceeding RMB 4.8 billion, representing 60% of the global market, making it the world's largest quadruped robot market.

This market landscape has been shaped by the "scaled breakthroughs" of domestic firms. A group of pioneers, including Unitree, Deep Robotics, and Dobot, have significantly reduced production costs through technological iteration and self-developed manufacturing, while rapidly commercializing across consumer and industrial scenarios by leveraging local market advantages. They now dominate major global market shares.

Note: Data sourced from publicly available online information and industry report estimates, compiled by Jingqi Intelligence for reference only.

For a long time, the quadruped robot (dog) market was monopolized by overseas giants like Boston Dynamics and ANYbotics. Among them, Boston Dynamics' Spot robot, with its dynamic balancing, extreme mobility, full-body coordination, and integrated perception and control technologies, can easily handle extremely complex scenarios and is hailed as the pinnacle of robotics. However, its hefty price tag of nearly RMB 1 million per unit has deterred many users.

"Cost-effectiveness" has thus become a core breakthrough path for domestic players. In the consumer-grade quadruped segment, Unitree Robotics' Go2 Air (entry-level entertainment version), launched in 2023, starts at just RMB 9,997, the first to bring robotic dog prices below RMB 10,000 and breaking overseas brand price monopolies. In November 2025, Dobot's Rover X1 further reset expectations with a starting price of RMB 7,499. For industrial-grade quadruped products, firms like Deep Robotics and Unitree Robotics have kept starting prices below RMB 100,000. These three companies now cover products ranging from RMB 10,000-level consumer entry models to RMB 100,000-level industrial models, continuously driving down industry-wide cost-effectiveness.

Meanwhile, domestic firms emphasize deep scenario penetration. Currently, quadruped robot applications have expanded from traditional research and education to commercial consumption, industrial inspections, emergency rescue, and other industry-specific uses.

In the short term, industry-grade scenarios like power grid inspections and firefighting rescue remain the primary growth drivers. In the medium to long term, the explosion of the consumer market will become the core driver of sector growth. Data from Unitree Robotics' prospectus confirms this trend, showing that from January to September 2025, commercial consumption revenue from Unitree's quadruped robots accounted for 42.30%, surpassing research and education to become the top revenue source, while industry application revenue rose to 26.12%. This "scale + scenario" approach has positioned domestic firms proactively in global competition.

In contrast, overseas quadruped robot (dog) firms, represented by Boston Dynamics, adhere to a "high-end pricing" and "technological premium" strategy, focusing on high-priced equipment sales and customized project deliveries. Their market expansion remains slow, with shipment and application scales far below those of domestic firms.

While this path maintains a premium brand image, it struggles to achieve large-scale commercialization in the short term and risks missing out on the explosive growth opportunities in the global embodied AI market. After all, in the early stages of industrialization, "usability, affordability, and cost-effectiveness" are key to market penetration.

Notably, quadruped robots (dogs) share technological synergies with humanoid robots. Their technological iteration and commercialization progress can provide valuable experience for the scaled deployment of humanoid robots. Technologies such as motion control, autonomous navigation, and core component R&D are transferable across sectors, which is the core logic behind Unitree's "quadruped-first, humanoid-later" strategy.

Driven by "technological maturity + cost reductions," domestic quadruped robots have already entered a scaled deployment phase, with core competitiveness upgrading from "usability" to "ease of use."

Of course, whether for quadruped or humanoid robots, the distinct characteristics of the competitive landscape—"domestic leadership in technology and mass production, overseas focus on technology"—essentially reflect a strategic game theory (game) between "scale dividends" and "technological premiums" in the global embodied AI market.

Jingqi Commentary

Unitree Robotics' IPO represents not just a corporate capitalization milestone but also a symbol of China's embodied AI industry transitioning from "wild growth" to "regulated development." Judging by the competitive landscape outlined in the prospectus, the global embodied AI sector has entered a "Warring States era."

Chinese firms, wielding "mass production and deployment" as their spear, leverage full industry chain advantages and scenario adaptation capabilities to seize commercialization opportunities. Overseas players, armed with "technological depth" as their shield, hold fast (hold firm to) high-end sectors, awaiting scaling breakthroughs post-technological advancement.

What is certain is that in this global embodied AI contest, the winners will be those who can both stay true to technological innovation and understand market demands. After all, the ultimate purpose of the industry has never been about "how advanced the technology is" but "how many real-world problems it can solve."

*Editor's Disclaimer: Original content is hard-earned; please respect the author. For reprints, please contact us.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?