Alibaba’s Instant Retail Funds Should Be Redirected to AI Initiatives

03/24 2026

03/24 2026

466

466

No one doubts Alibaba’s capacity to compete on multiple fronts. However, the resources consumed by instant retail are, in effect, constricting the potential of its AI strategy. Facing competitors like ByteDance and pivotal opportunities in AI, it would be more strategic to consolidate resources and outpace rivals in this unprecedented opportunity rather than continuing to heavily invest in instant retail.

After Alibaba released its earnings report, discussions quickly emerged about reassessing its value.

Nonetheless, Alibaba’s Hong Kong-listed stock dropped 6.3% following the earnings announcement, with the stock price declining 14% year-to-date.

This is clearly not indicative of a value reshaping, particularly when considering large AI companies like MiniMax and Zhipu. The market is not convinced by the logic behind Alibaba’s value reassessment.

The core issue lies in skepticism about Alibaba’s continued focus on instant retail. At a time when AI demands comprehensive efforts, Taobao Flash Sale should not continue to drain Alibaba’s resources.

Part.

01

Instant Retail: Struggling Against Market Trends for Share

Instant retail is indeed a strong suit for Alibaba, but the cost-effectiveness of fighting against market trends for share is questionable.

In the fourth quarter (Alibaba’s third fiscal quarter), Alibaba’s instant retail revenue soared by 56% to 20.8 billion yuan. This segment is indeed the most dynamic within Alibaba’s e-commerce and even its entire business.

According to Alibaba’s plan, instant retail follows a high-frequency driving low-frequency business model, aiming to boost overall e-commerce through food delivery.

However, from the fourth quarter’s perspective, this model has not yet borne fruit. Alibaba’s Chinese e-commerce business generated 131.6 billion yuan, up just 1% year-on-year. Its growth rate is nearly identical to JD.com’s, which saw a 1.53% revenue increase in the fourth quarter. Jiang Fan mentioned during the earnings call that factors such as weak macroeconomic consumption, a mild winter, and a late Chinese New Year posed significant challenges to growth in December.

This statement objectively indicates that the macro environment’s impact on Alibaba far outweighs the incremental growth brought by instant retail.

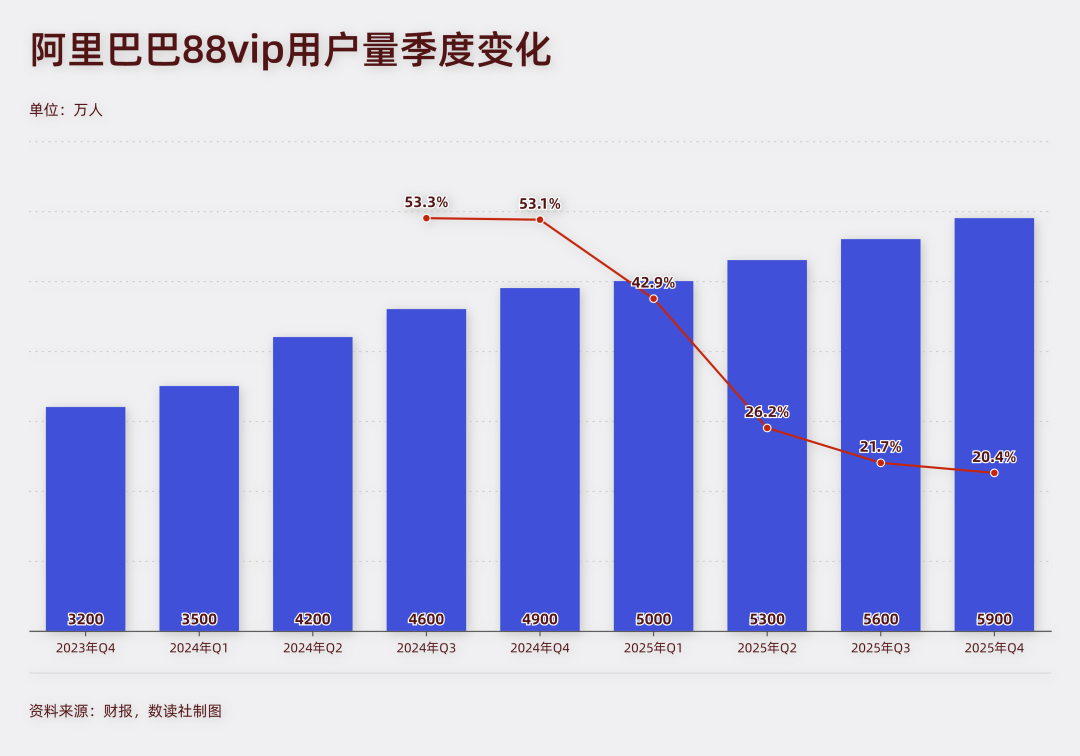

In 2025, Alibaba made significant moves with Ele.me and tentatively included Hema in the benefits for 88VIP members, yet the results remain unimpressive. In the fourth quarter, the number of 88VIP members reached 59 million, up about 20.4% year-on-year. Both the increment and growth rate are no longer comparable to the past.

In fact, the domestic e-commerce market is saturated, making large-scale growth difficult. The instant retail sector, after fierce competition, only accounts for 13% of Alibaba’s entire Chinese e-commerce group, up from 8.8% year-on-year, a mere 4.2 percentage point increase.

To achieve this 4.2 percentage point increase, Alibaba has paid a hefty price.

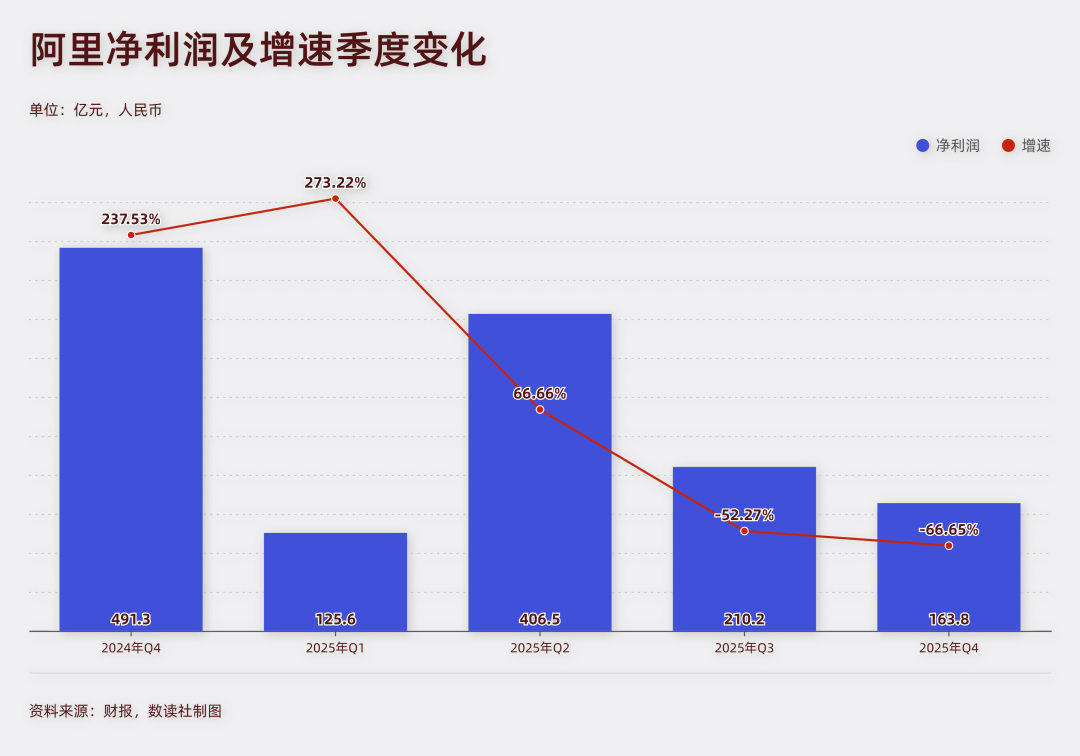

The adjusted EBITA for the domestic e-commerce department was 34.6 billion yuan, a significant year-on-year decline of 43%, with instant retail being the primary reason. Net profit was 15.6 billion yuan, a substantial year-on-year decrease of 66%. Under non-GAAP accounting, it also fell by 67%, again with instant retail being the top reason.

Net cash from operating activities was 36 billion yuan, a 49% year-on-year decline. Free cash flow was 11.3 billion yuan, a significant 71% year-on-year drop. The primary reason for the sharp decline in free cash flow is the investment in instant retail.

In essence, Alibaba is investing heavily—under the pressure of a two-thirds decline in net profit and a 70% loss in cash flow—into the vast ocean of instant retail, in exchange for 56% growth.

What if there was no such investment? In the fourth quarter of 2024, the local services group, including Ele.me and Gaode, still achieved 12% growth. In the two quarters before the heavy spending, both local services and instant retail saw double-digit growth. At least from the current results, Alibaba’s investment in instant retail resembles using a sledgehammer to crack a nut, with a very low return on investment.

Perhaps during the market expansion phase, Alibaba did not rush to charge merchants fees. As long as it captures a sufficient market share in the long run, a chemical reaction might occur, and this revenue has a good chance of further increasing.

With heavy investments, Alibaba has indeed seized a significant share from Meituan. According to Analysys data, in the fourth quarter, Taobao’s instant transaction volume accounted for a 45.2% market share, surpassing Meituan by 0.2 percentage points, ranking first. Even according to JPMorgan’s data, Taobao Flash Sale’s share is as high as 42%, approaching Meituan’s 50%. In 2024, Meituan Food Delivery accounted for 65% of the market, while Ele.me accounted for 33%. Alibaba is on the verge of victory in this battle.

However, platform-based economies are hardly a lucrative business worth boasting about.

On the one hand, large-scale money-burning does not align with current market trends. On March 23, three Beijing departments summoned 12 platform companies, announcing the first batch of issues related to “involutionary” competition, with JD.com, Taobao Flash Sale, and Meituan among them. This method of subsidized money-burning is under strict regulation, making Alibaba’s frenetic investment in instant retail increasingly less valuable.

On the other hand, even if Alibaba secures the top spot in instant retail, it is not an unbreakable market. Meituan’s example has proven that even with a two-thirds market share, it can still lose market share due to competitor subsidies. Consumers do not develop excessive loyalty to platforms, and the lowest price still wins.

Instead of struggling against market trends for share, it would be better to accelerate deployment in favorable conditions.

Part.

02

AI: Desperately in Need of Nourishment

Compared to instant retail, cloud intelligence business is Alibaba’s true future.

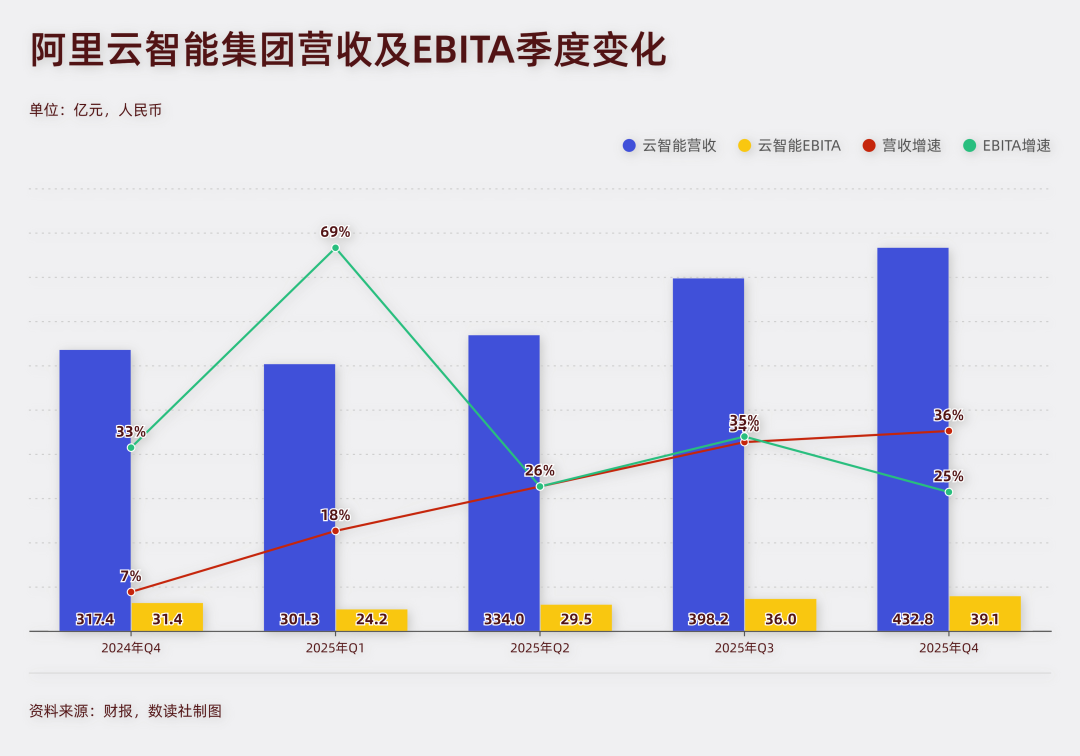

In the fourth quarter, Alibaba’s cloud intelligence business generated 43.3 billion yuan in revenue, a significant 36% year-on-year increase, with growth second only to instant retail. The profit return on this business is also substantial. Adjusted EBITA was 3.9 billion yuan, a significant 25% year-on-year increase. In the earnings report, regarding the decline in net profit, Alibaba mentioned that the growth of its cloud business improved operating performance, partially offsetting the profit decline caused by investments in instant retail.

Cloud intelligence business is Alibaba’s critical safety net, especially when overseas business grew by only 4% this quarter. Cloud intelligence business plays a crucial role in terms of growth and profit contribution.

Alibaba mentioned in its earnings report that the growth of this business is primarily driven by increased revenue from public cloud services. According to IDC, Alibaba Cloud has topped China’s overall financial cloud market for six consecutive years and has also ranked first in the hybrid cloud PaaS and services market.

However, besides traditional strengths, the power of AI cannot be ignored. After all, before the fourth quarter of 2024, the cloud intelligence business had seen single-digit growth for multiple consecutive quarters. Alibaba revealed that AI-related product revenue has achieved triple-digit year-on-year growth for ten consecutive quarters.

A low base is certainly key to triple-digit growth, but it does demonstrate the growth momentum of Alibaba’s AI business.

Alibaba has established a full-stack AI layout, with chips and cloud computing as the AI infrastructure layer; and an AI model and application layer consisting of Token Hub, large models, MaaS business, and “to B + to C” applications. Together, they form a complete capability from AI infrastructure to applications.

Breaking it down, in terms of “to B + to C” applications, “QianWen” has over 300 million monthly active users. QuestMobile data shows that its DAU rose to 73.52 million on February 7 and is now integrated with Alibaba’s “full suite,” initially taking on the form of an Agent. The enterprise-level Agent platform “Wukong” has been released and embedded in the DingTalk ecosystem.

In terms of chips, T-Head’s self-developed GPU chips have achieved mass production, with a cumulative delivery of 470,000 units as of February 2026.

Regarding the Token main thread, Alibaba has established a dedicated business group, with Wu Yongming personally at the helm, integrating Tongyi Lab, MaaS platform, QianWen, Wukong, and AI innovation businesses, all centered around the production, distribution, and application of “Tokens.”

Alibaba has high expectations for its cloud and AI businesses, setting a goal of doubling growth: over the next five years, cloud and AI-related commercial revenue will rise from the current 146.6 billion yuan to 100 billion US dollars. This implies an annual compound growth rate of 36.24%, a highly challenging target.

If Alibaba truly focuses on its AI business, it would likely be pursued by the market, especially since Alibaba is one of the few companies pursuing a full-stack AI layout.

However, the capital market does not view Alibaba as a true AI company, assigning it a trailing PE of only 23 times. Compared to AI chain companies like Cambrian, Moore Threads, and MiniMax, it follows a different logic.

Under such circumstances, if Alibaba strengthens its AI label, it might boost confidence and change its valuation logic. However, Alibaba’s attitude toward instant retail remains very clear—at all costs.

At the investor exchange meeting on January 8 this year, Alibaba stated that it would continue to increase resource investment in 2026, with the primary task being market share growth, aiming to achieve an absolute first place in the instant retail market. Alibaba said it would not pursue short-term profitability in the next two years, instead continuing to subsidize merchants and users, expanding covered cities and delivery efficiency, with order volume and market share as the core performance indicators.

Such a statement seems full of determination, but continuing to intensify investment in instant retail will only increase market divergence over Alibaba and may even cause Alibaba to miss the current critical stage of AI.

Part.

03

Competition: Fierce Rivals on All Sides

At this critical stage of AI layout, Alibaba is not in a leading position, and its competitors’ strategic determination and organizational management efficiency are no weaker than Alibaba’s.

Earlier this year, three giants launched a red envelope war, and Alibaba briefly topped the Apple App Store’s free chart with subsidies. However, over a month later, Alibaba and its subsidiary Ant Afu dropped to 8th and 10th place in downloads, below Doubao and Yuanbao.

The application layer requires sufficient marketing support, and the R&D layer also needs saturated preparation.

In the fourth quarter, Alibaba’s capital expenditures were 29 billion yuan, with total capital expenditures for 2025 reaching 123.8 billion yuan. This scale is indeed very large.

However, competitors are not far behind. According to the Financial Times, ByteDance’s capital expenditures for 2025 are approximately 150 billion yuan, with an expected increase to 160 billion yuan in 2026. Moreover, the company’s AI chip budget will reach 85 billion yuan, with a test order for 20,000 H200 chips already placed.

Currently, ByteDance has formed a clear layout of four major product lines: among them, the AI inference chip “SeedChip” plans to obtain its first batch of samples by the end of March 2026 and aims to produce at least 100,000 units this year, eventually increasing production capacity to 350,000 units.

In the AI field, the competition between ByteDance and Alibaba has just begun. Compared to Meituan in the instant retail sector, ByteDance is clearly a more formidable opponent, and AI is the area where Alibaba needs to provide more support.

ByteDance and other competitors have a very clear path, making AI their core strategy and aligning everything with AI. Besides AI, ByteDance is hardly seen allocating resources to other sectors.

Besides the pressure from ByteDance on the comprehensive end, the impact from Baidu, Moore Threads, and Cambrian on the chip end, and the competition from Zhipu and MiniMax in the Token field all mean that Alibaba cannot afford to be complacent.

No one doubts Alibaba’s ability to compete on multiple fronts. However, the resources currently consumed by instant retail and its impact are, in effect, constricting the potential of its AI strategy. As of December 31, 2025, Alibaba’s net cash decreased from 366.4 billion yuan at the beginning of the year to 297.4 billion yuan, a reduction of about 69 billion yuan.

Investments in the AI era have already prompted many giants to initiate layoffs. In March, Meta is planning its largest-ever layoff, aiming to cut about 20% of its global workforce, or approximately 16,000 employees, primarily due to rising AI costs. By analogy, even with nearly 370 billion yuan in cash reserves, Alibaba cannot afford to be complacent in winning this competition.

Instead of pouring heavy investments into instant retail, which has seen little fluctuation, it would be more strategic to consolidate greater resources and secure a leading position in the next decade’s layout.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?