Li Xiang Lets Go of His Obsession, Li Auto Slows Down Its Pace

03/24 2026

03/24 2026

632

632

By Luo Xia

Edited by Zhang Xiao

In the first half of 2021, Li Auto reached the milestone of a secondary listing in Hong Kong, finally shedding the financial constraints of its earlier years and beginning to increase investment in planning BEV models.

At that time, Li Auto had not yet achieved the later high points, but the blockbuster effect of the Li ONE and the company's operational efficiency advantages were accelerating.

In 2021, Li Auto delivered approximately 90,000 units of the Li ONE model alone, equivalent to the sales of NIO's three models and XPeng's two models. The gross margin for the same period was 21.3%, with an adjusted net profit of RMB 780 million under non-U.S. GAAP.

This boosted founder Li Xiang's confidence and ambition, leading to the strategic goal of selling 1.6 million vehicles by 2025. He mentioned this ambitious target on multiple public occasions thereafter.

At that time, the "1.6 million vehicles" target was more of a Attitude change (posture shift) for Li Auto, transitioning from a focus on efficiency to further scaling up.

However, reality poured cold water on Li Auto, as the "growth myth" became unsustainable. In 2025, Li Auto delivered 406,000 vehicles, a year-on-year decline of 18.8%.

Correspondingly, revenue reached RMB 112.3 billion, a decrease of 22.3%; net profit plummeted from RMB 8 billion to RMB 1.1 billion, an 86% drop. The company also slipped back into operational losses, with an annual operating profit of -RMB 520 million, achieving paper profitability only through RMB 1.92 billion in interest income.

Behind these figures, the two long-standing defensive lines that Li Auto had hold fast (adhered to) were simultaneously under pressure.

On one hand, the gross margin fell below the healthy benchmark of 20% defined by Li Auto itself. On the other hand, the advantage of extended-range products was broken, while new BEV models could not yet support cash flow. This once-unique new energy vehicle (NEV) company now stands at a critical crossroads of transformation.

From an industry perspective, by 2025, the penetration rate of China's NEV market had historically surpassed 50%, and the industry had fully shifted from incremental expansion to stock game (stock competition). The original pattern (landscape) of "NIO, XPeng, and Li Auto" was rapidly disrupted by new players such as HiMo, Xiaomi, and Leapmotor.

From a corporate perspective, Li Auto in its transitional phase is be caught in (mired in) complex challenges arising from the shift between old and new growth drivers, with challenges coming from both external and internal factors, as well as from products and organizational construction.

Li Auto has already accelerated its transformation. 2025 was the most pressure-filled year for Li Auto, but it was also the year of the most rapid transformation, ranging from organizational restructuring on the R&D side to management changes on the channel side, all aiming to lay a solid foundation for long-term competition. Li Auto's sales target for 2026 is no longer aggressive, set at "only" 20%.

This more conservative growth target compared to the past is not necessarily a bad thing for Li Auto. Slowing down the pace might allow the company to Power storage rebound (gather strength for a rebound).

01

Gross Margin Erosion: A More Serious Issue Than Sales Collapse

Li Auto was the first Chinese new energy vehicle startup to achieve annual revenue of RMB 100 billion and the first to achieve annual profitability. Its profitability was built on two pillars: scalable sales expansion and an industry-leading gross margin.

In 2023 and 2024, Li Auto sold 376,030 and 500,505 vehicles, respectively.

Since Li Auto positioned itself in the mid-to-high-end extended-range SUV market, with mainstream product prices ranging from RMB 250,000 to RMB 400,000, this pricing strategy brought it a gross margin exceeding 20% and sustained profitability.

However, in 2025, Li Auto's sales reached 406,343 units, roughly 94,000 fewer than the previous year. This decline was reflected in revenue, with annual revenue falling by 22.25% year-on-year and net profit dropping by 86%. The magnitude of the revenue and net profit declines was not on the same scale, indicating that Li Auto's problems extended beyond just a sales slump.

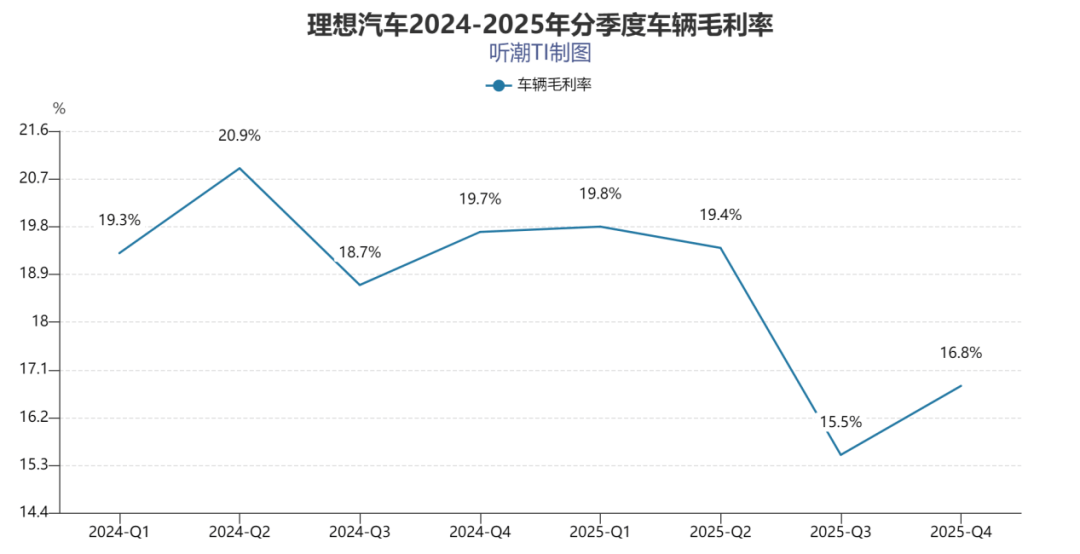

From a financial perspective, Li Auto's vehicle gross margin showed a continuous decline in 2025, falling from 19.8% in the first quarter to 16.8% in the fourth quarter, with the lowest point reaching 15.5% in the third quarter.

The direct trigger for the declining gross margin was the change in product mix.

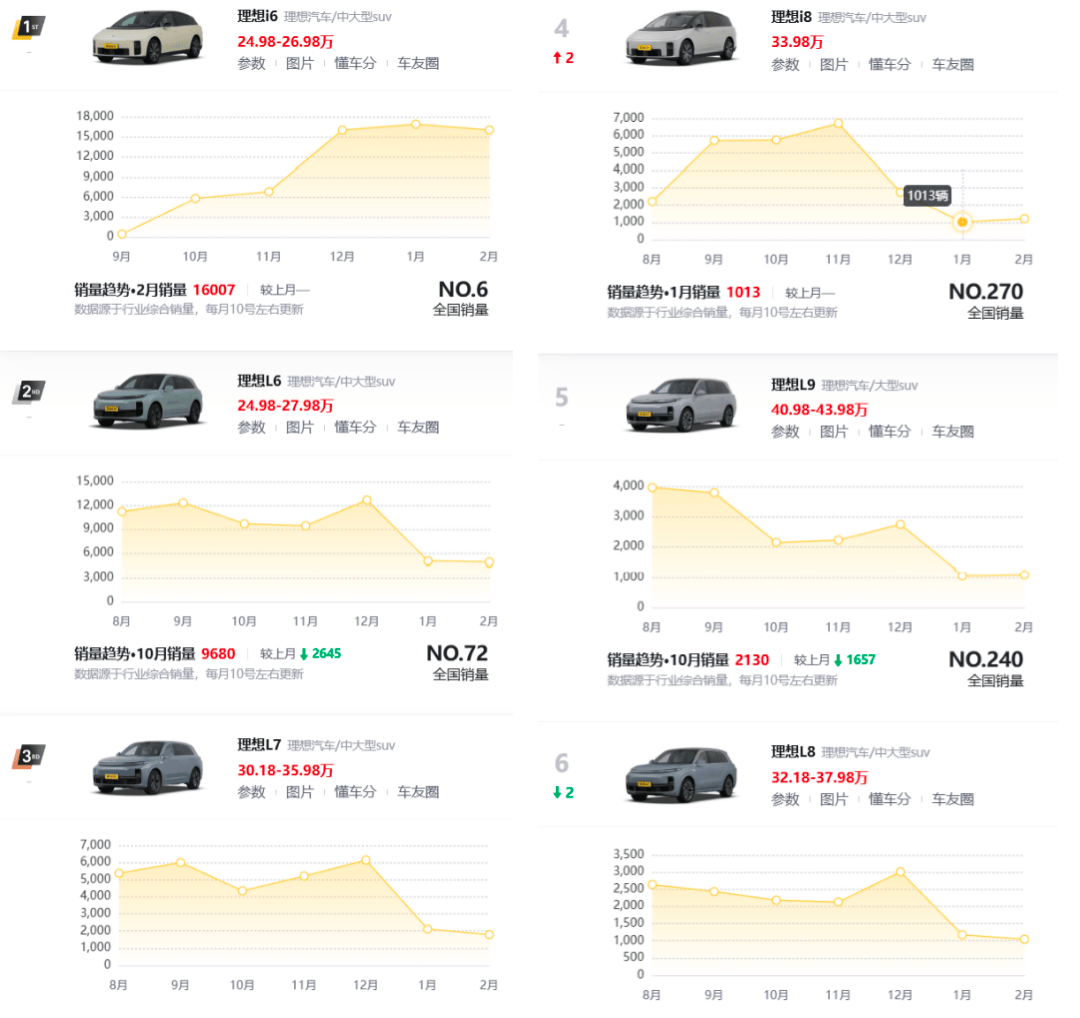

The Li i6, launched on September 25, 2025, is Li Auto's lowest-priced BEV model. It received over 20,000 firm orders on its launch day and accounted for 60% of Li Auto's monthly sales by February 2026.

With a unified price of just RMB 249,800 for all i6 variants, combined with promotional offers during the initial sales period, the terminal price even fell below that of the comparable extended-range model L6. This directly caused Li Auto's average revenue per vehicle in the fourth quarter to drop to RMB 249,600, the lowest since 2022.

Figure/Li i6 promotional page

Figure/Li i6 promotional page

In other words, in recent months, Li Auto's best-selling model has been its lowest-priced one. However, the i6 was launched at the end of the third quarter of 2025, which cannot fully explain the entire year's gross margin decline.

In addition to the change in product mix, the provision for expected costs related to the recall of the Li MEGA in the third quarter of 2025 also dragged down the gross margin.

Another factor, not explicitly mentioned in the financial report, was the intensifying industry price war, which further exacerbated the downward pressure on gross margins.

Throughout 2025, competition in the NEV market became increasingly fierce, with price adjustments becoming the norm. Li Auto was forced to join the fray, repeatedly offering price cuts and promotions for its L-series extended-range models. Currently, while i6 deliveries have reached a new high, the model is still operating at a loss per unit. According to management, it is expected to achieve monthly profitability only by the second quarter of 2026.

Thus, the gross margin falling below the benchmark line means that the foundation of profitability has been shaken. For Li Auto, which has long relied on high gross margins to support R&D and transformation, when the low-priced i6 becomes the sales mainstay and high-priced models struggle to grow, relying on price cuts to maintain stability, the erosion of gross margin becomes a structural issue rather than a short-term fluctuation.

02

BEVs Bring Surprises, Extended-Range Models Expose Greater Risks

The performance of the i6 exceeded market expectations but also exposed the fragility of Li Auto's product matrix.

The i6 is equipped with an 800V high-voltage platform, a self-developed 5C battery, a range of up to 720km, and supports ultra-fast charging. It also continues Li Auto's advantages in smart cockpits and family-oriented features. In 2025, Li Auto delivered 81,300 BEV units, with the i6 accounting for 78,000 units, or 96% of BEV sales.

In contrast, data from Dongchedi's sales rankings show that in the past six months, sales of Li Auto's L-series models have generally trended downward.

Li Auto once led the new energy vehicle market with its extended-range technology, cleverly avoiding the range and charging anxieties of early BEVs and building a strong position with its L-series extended-range models. The L-series, launched as early as 2022, surpassed 1 million cumulative sales in just 31 months. Meanwhile, many automakers followed suit with products featuring "refrigerators, TVs, and sofas," launching more extended-range models to compete for market share.

From a sales perspective, L-series sales have shown a clear downward trend since the second half of 2025, and this trend continued into the first quarter of 2026. Sales data from January-February 2026 show that monthly sales of the L6 hovered below 6,000 units, the L7 around 2,000 units, and the L8 and L9 at just over 1,000 units each.

Sales trends of Li Auto's full product lineup in the past six months, Figure/Dongchedi

Sales trends of Li Auto's full product lineup in the past six months, Figure/Dongchedi

Comparing these monthly sales figures with those from previous months, the decline is almost at the 50% level. It should be noted that the L-series once achieved monthly sales of 50,000 units, but now it is down to around 10,000 units.

Li Auto's sales guidance for the first quarter of 2026 is 85,000 to 90,000 units, a year-on-year decline of 3%-9%. Given the current monthly sales of the i6 at 15,000-20,000 units, this means the first quarter will likely still be "carried" by the i6, which will account for over 50% of total sales, while pressure on the L-series will persist.

The i6's pricing strategy clearly prioritizes market share, and this "volume-at-the-expense-of-margin" approach, while quickly opening up the BEV market, has also locked in a lower gross margin space. With the competitiveness of the original "cash cow" L-series continuing to decline, Li Auto faces significant challenges.

Li Auto is not unaware of this issue and is attempting to revitalize its extended-range business through product iterations.

According to the financial report, the next-generation L9 will be launched next quarter, equipped with a self-developed M100 chip and a wire-controlled chassis, while also introducing a facelift for the smaller L6 model. The company hopes to regain market share through technological upgrades and configuration optimizations.

The success of the i6 has proven Li Auto's potential in the BEV field, but it also means the company must now fight on two fronts—stabilizing the extended-range base while driving the BEV business toward profitability. Against the backdrop of a growing BEV trend and continuous competitive pressure, whether these upgrades can reverse the decline of extended-range models remains to be seen in the market.

03

Transformation and Growing Pains: Li Auto Awaits Its "Spring"

In 2025, Li Auto entered its most critical transformation phase since its inception.

Starting in the second half of the year, the company abandoned its professional manager system and returned to a founder-led entrepreneurial model. Over the course of a year, more than 10 executives and core leaders left, with nearly the entire Huawei-affiliated management team exiting.

The drastic organizational adjustments essentially represent a recalibration of Li Auto's development path. Li Xiang stated bluntly during an earnings call that organizational upgrades typically take 12 to 24 months to yield results. This means that the performance fluctuations, internal friction, and growth slowdown experienced by Li Auto in 2025 are inevitable growing pains of the transformation process.

These growing pains did not appear suddenly.

In 2024, due to the MEGA's underperformance, Li Auto conducted a large-scale workforce optimization involving over 5,000 people. Adjustments were also made at the channel level, with market reports suggesting the closure of 100 stores. The company clarified during an earnings call that this was a normal culling of inefficient stores.

Objectively speaking, during the rapid expansion of the past few years, issues such as unreasonable store locations, declining foot traffic, and low operational efficiency did exist and were exposed as competition intensified.

The simultaneous adjustments in organization, channels, and strategy are most clearly reflected in Li Auto's relatively pragmatic sales target and cautious R&D investment for 2026.

Against the backdrop of dense ( dense ) new vehicle launches in the mid-to-high-end market above RMB 200,000 and limited overall incremental growth, Li Auto set its annual sales target at over 20% year-on-year growth, corresponding to approximately 500,000 units. Compared to the more aggressive targets of some peers, Li Auto's approach is clearly more cautious and aligns with the current mindset of "stabilizing operations before pursuing growth."

Financially, Li Auto remains prudent. As of the end of 2025, the company held RMB 101.2 billion in cash reserves, a relatively high level in the industry, providing a safety buffer for the transformation.

For 2026, R&D expenses are expected to reach RMB 11.3 billion, with nearly half earmarked for AI and intelligence-related fields. The company is bearing high investment pressure while awaiting the gradual implementation of technologies.

After the industry entered stock competition, the product advantages Li Auto once relied on are being caught up, while new technological barriers are still being built. The ramp-up of BEV models, supply chain fluctuations, rising raw material prices, and internal organizational adjustments have all contributed to this round of growing pains.

However, these growing pains are also pushing Li Auto to address issues left over from its rapid expansion.

The i6 has overcome the most difficult production ramp-up phase, with supply chain bottlenecks largely resolved and monthly delivery capacity stabilizing at 20,000 units. Backorders will be gradually fulfilled over the next month or two. The stable growth of the i6 also signifies that Li Auto's brand strength has officially extended from extended-range to BEV markets, laying the foundation for a second growth curve.

In the second quarter of 2026, the all-new L9 will be officially launched, equipped with a self-developed M100 chip, a wire-controlled chassis, and an 800V active suspension, featuring comprehensive upgrades in perception, computing power, and vehicle control. It is seen as a key model for Li Auto's transition from "product definition leadership" to "technological leadership."

Internal operational efficiency is also undergoing synchronous reforms. In March 2026, Li Auto introduced a store partnership mechanism, delegating operational and profit-sharing rights to individual stores in hopes of addressing issues of over-expansion and inefficiency at the root level, with the goal of seeing improved sales performance by the third quarter.

Facing external pressures such as rising battery and chip costs, Li Auto primarily mitigates cost pressures internally through long-term agreements with suppliers to lock in prices, platform-based R&D, self-developed cost reductions, and more robust ( robust ) new product pricing, striving to restore gross margins to healthy levels. In 2026, all Li Auto models will adopt a dual-brand battery solution from CATL and Li Auto, with Li Auto leading design and quality control to further stabilize the supply chain and consistency of the user experience.

For Li Auto, the growing pains of 2025 are more like the cost of proactive adjustments. The company has slowed the pace of scale expansion to address shortcomings in organization, efficiency, and technology, rebuilding long-term competitiveness as the industry transitions from rapid growth to a shakeout phase.

In the rapidly evolving NEV market, there are no eternal defensive lines for companies—only continuous iteration. Li Auto's current proactive "squat" seems more like preparation for a steadier and more sustainable leap in the next phase.

-

![]()

The Unstoppable Rise of 'Optical Progress and Copper Decline': Sunny Optical’s Strategic Vision for the Next Decade

-

![]()

AI + Going Global in the Second Half: No Intermission for Robot Vacuum Cleaners

-

![]()

The Suffering Endured in E-commerce, Walmart Doesn't Want to Repeat in AI

-

![]()

What Does the Doubling of New Energy Vehicle Exports Mean?

-

![]()

Ghosn: 'Only I Can Save Nissan'

-

![]()

Volkswagen Lays Off 100,000 Employees, The Elephant Sits Down

-

![]()

Expanding Production Capacity! Yutong Optics Acquires Approximately 1.5 Hectares of Industrial Land in Chang'an, Dongguan

-

![]()

Why Is Nokia Making a Comeback in the AI Era?