Meitu: Is There No Future for Niche and Attractive SaaS in the AI Agent Era?

03/30 2026

03/30 2026

577

577

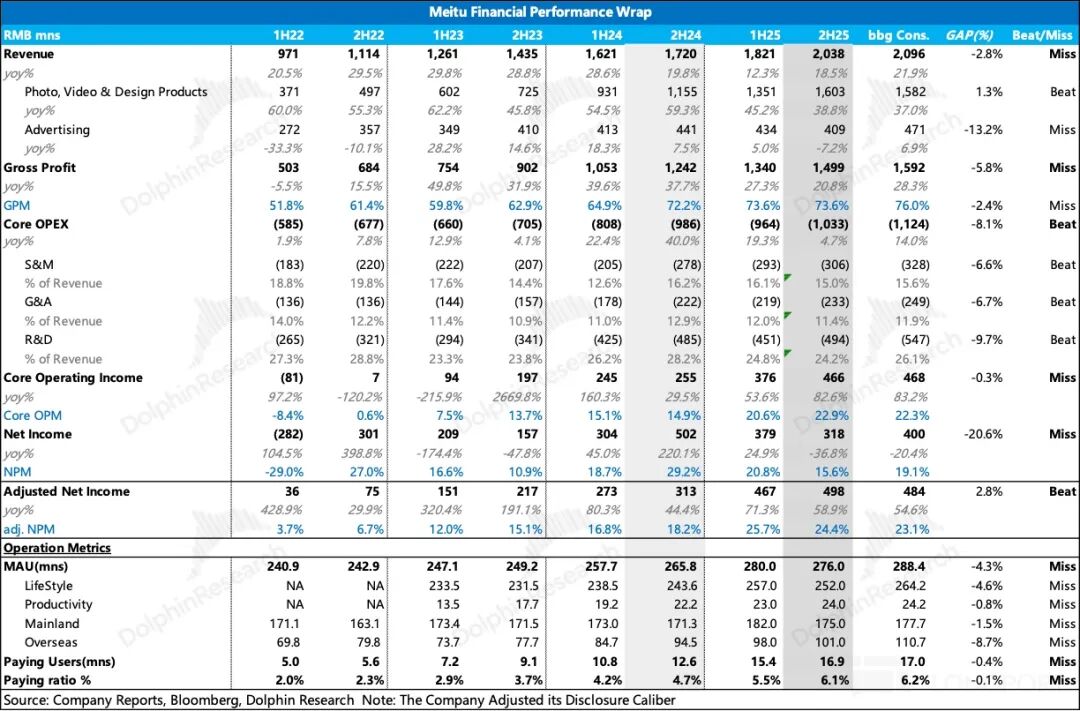

On March 27, Beijing time, after the Hong Kong market close and before the U.S. market open, Meitu released its financial report for the fiscal year 2025. The performance in the second half of 2025 was underwhelming, with revenue missing expectations and gross profit significantly lower. However, expense control exceeded expectations, keeping operating profit largely in line. Nevertheless, the user ecosystem contributing to subscription revenue was under significant pressure, leading to an overall negative impression from Dolphin Research.

During the earnings call, management addressed the claim that 'AI is replacing software,' emphasizing that models serve as infrastructure while applications deliver value. They highlighted that the two are synergistic rather than substitutes, and Meitu, as a vertical imaging application provider, would benefit from advancements in models. Management also shared their strategy for moving toward AI Agents and the prospects for B-end productivity and overseas businesses.

Key takeaways:

1. User Ecosystem:

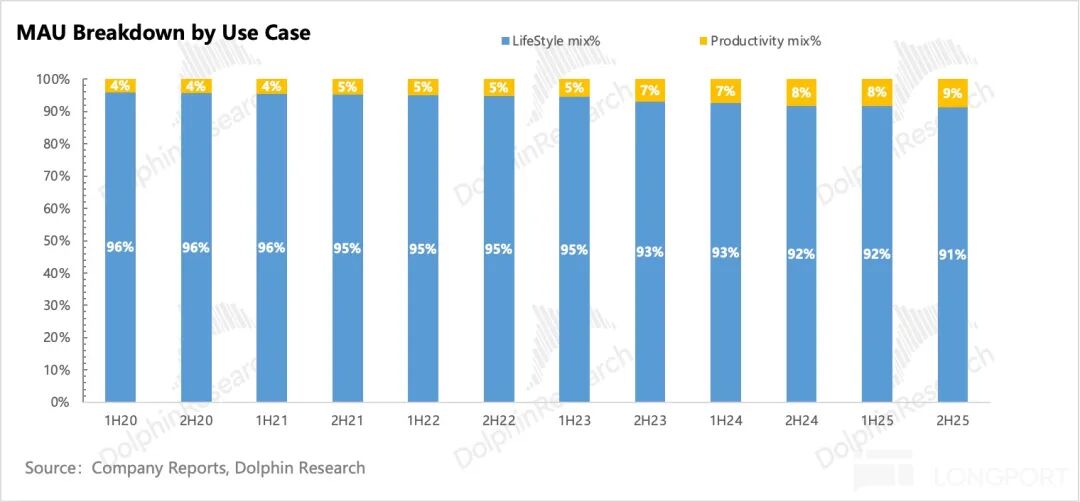

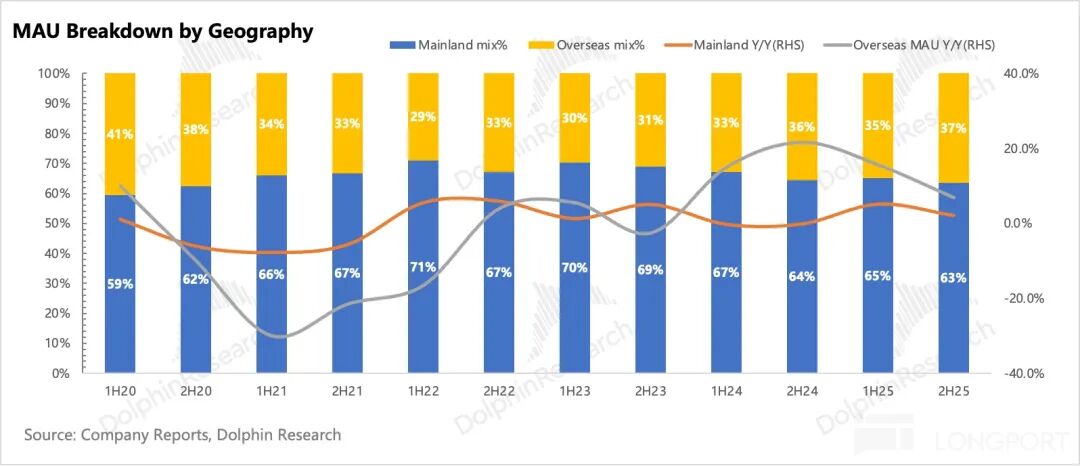

a) MAU: The call explained the decline in MAU in the second half of the year by citing the maturation of domestic lifestyle products and slowing growth. However, the MAU for productivity scenarios, which Dolphin Research is more concerned about, stood at 24 million and was not addressed. Although the B-end is still in the penetration phase in terms of user structure, growth significantly slowed from 36.83% in 2023 to 8.17% in 2025.

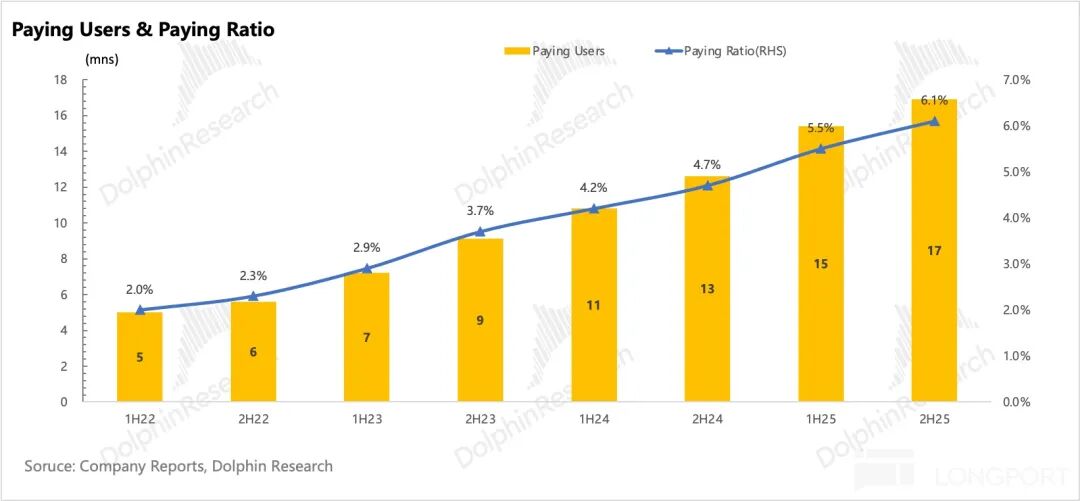

b) Subscriber Count and Penetration Rate:

- In terms of growth, subscriber numbers increased by 2.8 million in the first half of the year but only by 1.5 million in the second half. Considering the overall decline in MAU, the in-line subscription penetration rate was partly due to a shrinking denominator, suggesting lower actual conversion quality.

- Structurally, subscription penetration in lifestyle scenarios reached 5.9%, with steady growth in the second half compared to the first. In contrast, productivity scenarios saw higher annual growth in subscription penetration, but growth slowed from 2% in the first half to 1.2% in the second half.

Given the company's guidance for a breakthrough in productivity tools in the second half of 2026, there are doubts about this outlook at the current juncture.

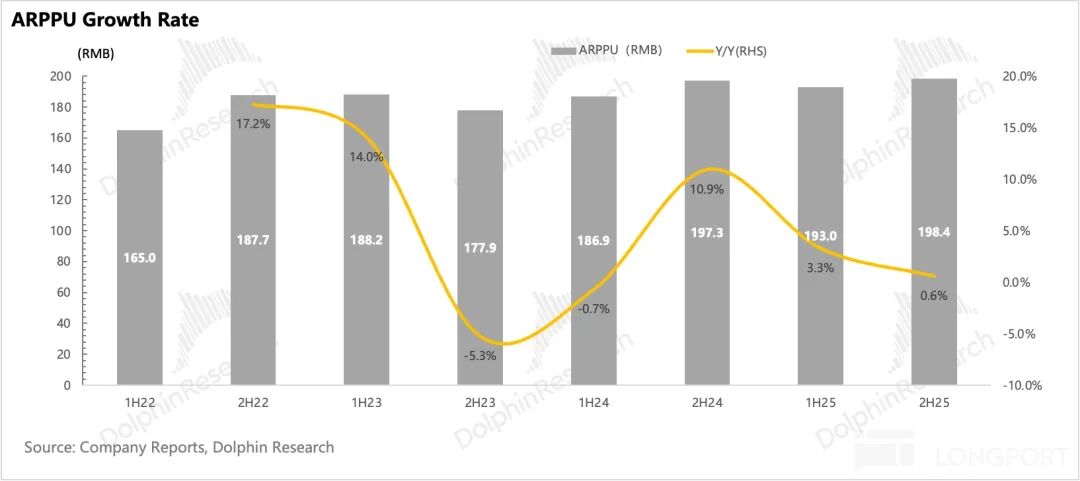

c) ARPPU: Implicit ARPPU exceeded 200 RMB, representing a 4.21% year-over-year increase, reflecting the boost from the company's globalization strategy and its shift toward B-end vertical scenarios.

2. Expense Control:

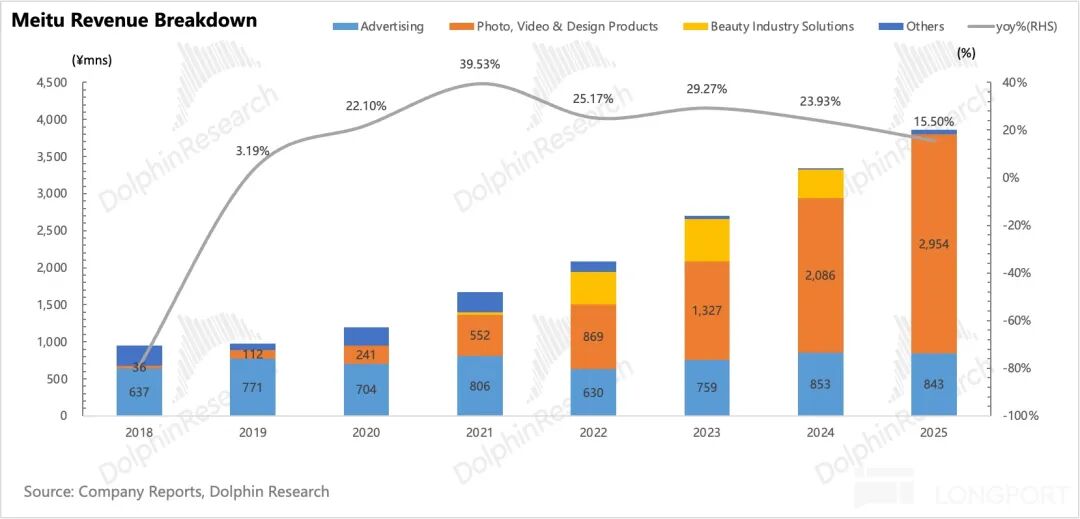

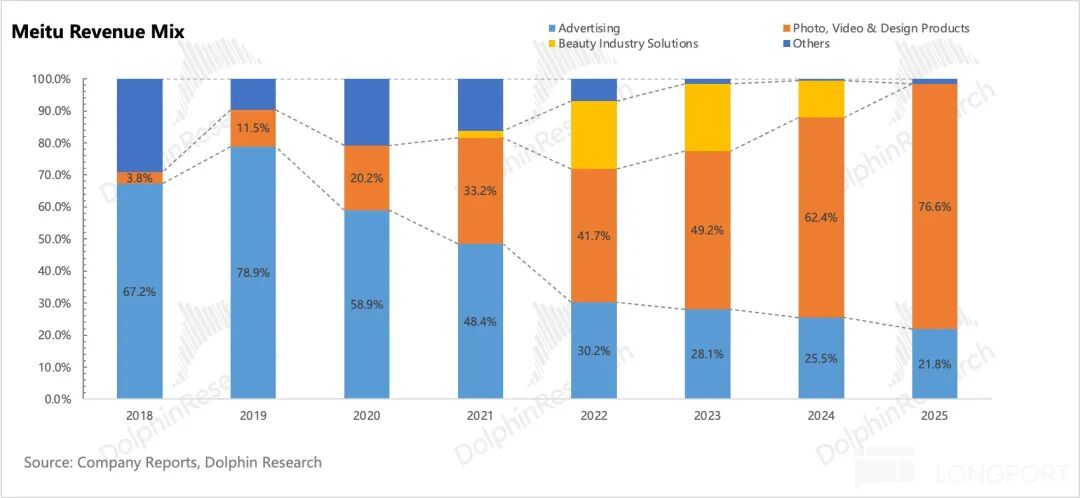

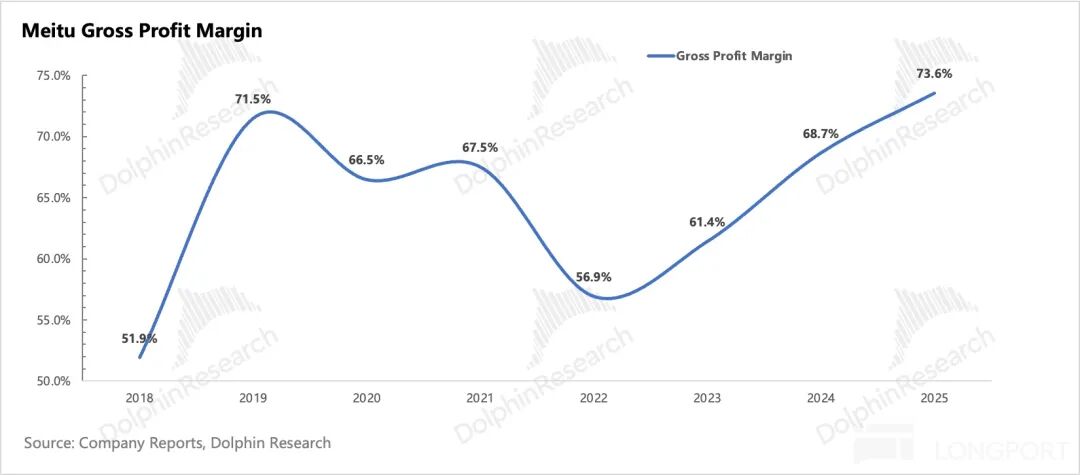

- Gross profit growth slowed to 20.8%, with gross margin remaining flat compared to the first half. The significant miss in gross profit was primarily due to two factors: a decline in the proportion of high-margin advertising revenue and the company's strategy of 'amortizing computing costs through subscription plans' (offering users access to advanced models at lower subscription prices multiple times), which significantly increased computing and API-related costs.

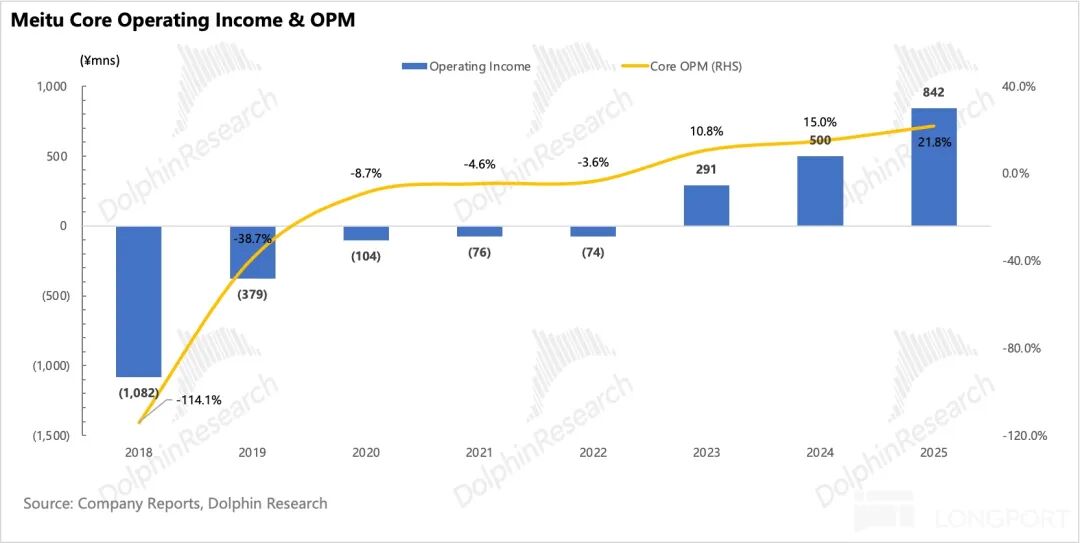

Despite the significant miss in gross profit, core operating profit reached 466 million RMB, an 82.6% year-over-year increase, largely in line with expectations. This was primarily due to Meitu's effective control of operating expenses, which exceeded expectations across the board.

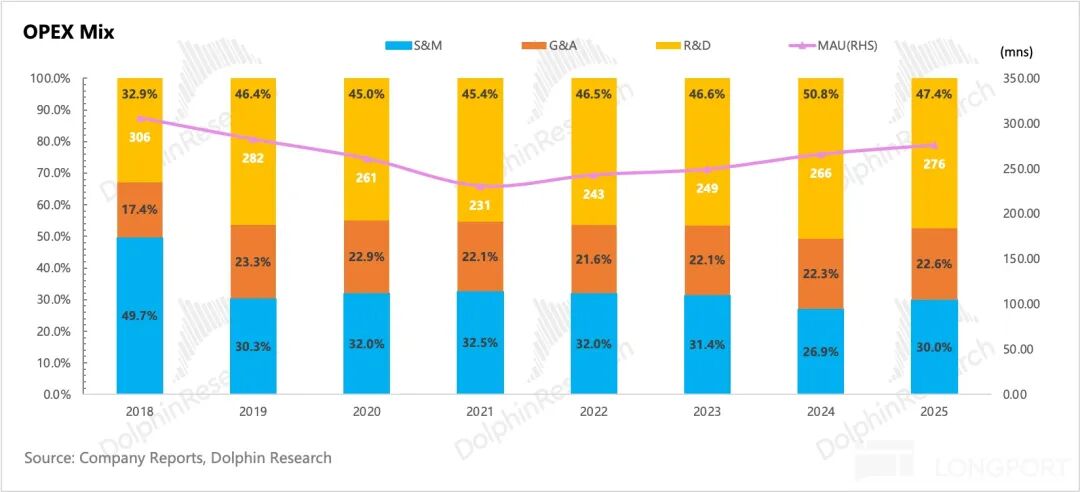

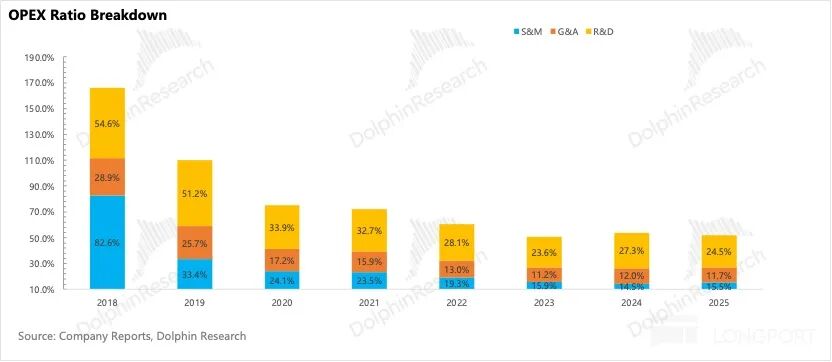

- From a sales expense perspective, Dolphin Research initially assumed that overseas expansion would require increased sales expenses. However, the proportion of sales expenses to subscription revenue remained at 16% in the second half.

- Regarding R&D spending, the company's Model Container strategy controlled expenditures related to foundational model training, resulting in a mere 3.8% increase in annual R&D spending.

Dolphin Research believes that, given the current poor performance of the user ecosystem, especially the underperformance of overseas expansion, the company may still need to increase customer acquisition through promotions. Additionally, it should be noted that the savings in R&D spending came at the expense of gross profit.

3. Cash Flow and Shareholder Returns: As of FY25, Meitu had approximately 4.4 billion RMB in net cash (cash + short-term investments - interest-bearing debt), indicating strong cash flow. Regarding shareholder returns, excluding the special dividend from the one-time revenue of liquidating cryptocurrency holdings, if the company maintains a 40% cash dividend payout ratio and includes the 300 million HKD buyback plan disclosed by management, the total shareholder returns would amount to approximately 650 million RMB. Relative to the current market capitalization of 19 billion RMB, the potential yield of 3.5% is not particularly high. Moreover, it should be noted that buybacks may not be sustainable, and excluding them, the potential return would be 2%, providing limited support.

4. Overview of Financial Data

Dolphin Research's Viewpoint

Let's first review Meitu's diverse product matrix. For an in-depth analysis, refer to: 'Meitu: Can Vertical SaaS Survive the AI Tsunami?'

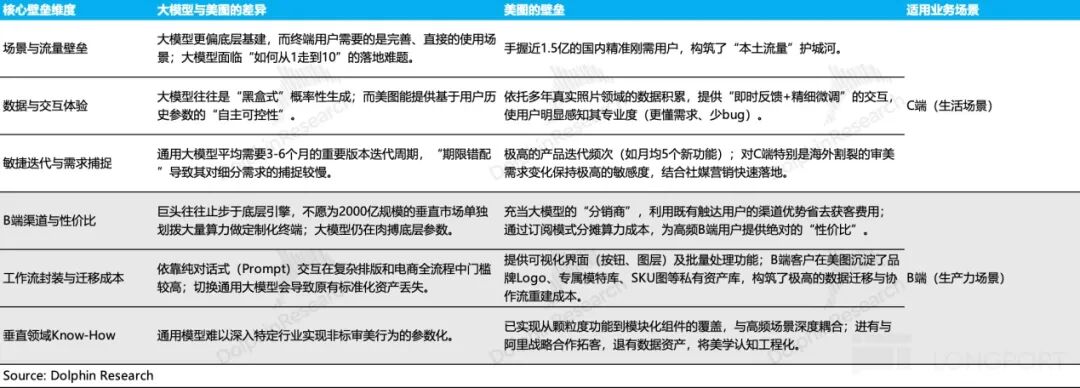

Since the release of Meitu's 1H25 financial report, its market capitalization has halved. From a market environment perspective, geopolitical risks have driven capital toward assets with high certainty. Additionally, the notion that 'AI is replacing software' has intensified as large model providers transition from Chatbots to the Agent era. Was Meitu wrongly penalized? In our initial coverage, Dolphin Research discussed Meitu's barriers against the impact of large models, with the following key points:

Although only three months have passed since our initial coverage, Dolphin Research believes that some of the company's core assumptions have been challenged due to the rapid iteration of AI interaction methods and the swift advancement of model intelligence.

A) On the C-end, Dolphin Research still believes that Meitu's foundational 'editor' functionality provides 'autonomy and controllability,' which can retain moderate and heavy users in the short term (medium to long term depending on the pace of AI development), ensuring stable user retention. Since image editing inherently relies on subjective user judgment, which is non-standardized, interactions with large models via natural language still involve hallucinations and uncertainties.

- In terms of iteration, LLM iteration speeds have significantly accelerated (e.g., MiniMax completed its iteration from M2.5 to M2.7 in just one month). Moreover, the code generation capabilities of various models continue to improve, enabling zero-code development that allows ordinary users to easily build scripts or even standalone software using large models. The trend of 'everyone can create tools' has, to some extent, weakened Meitu's advantage in functional iteration and impacted light-use scenarios. Of course, Meitu still maintains certain competitiveness by building end-to-end capabilities in deep workflows and combining aesthetic demand discovery and amplification.

- From a traffic perspective, the popularity of OpenClaw seems to indicate the next generation of Agent traffic entry points, with domestic tech giants rushing to build their own 'shrimp farms.' Users no longer need to open specific software to accomplish specific tasks, and the competition for traffic entry points has always been fierce in the domestic internet landscape.

In fact, Meitu recognized the potential of Agent interactions and launched its standalone AI Agent product, RoboNeo, in July 2025. However, as analyzed by Dolphin Research, its position as a standalone product remains unclear.

Currently, the company has integrated Agent capabilities into various product lines, which could potentially boost ARPPU from a token consumption perspective. However, this is insufficient. Based on market feedback on single-product operating data, RoboNeo still cannot serve as the entry point to connect various products.

B) The popularity of the 'lobster ecosystem' and the failure to secure traffic entry points led Meitu to recently release its official AI Skill, actively integrating into the ecosystems of tech giants and providing users with callable, combinable, and reusable standardized capability modules. We believe this expands B-end business scenarios and offers some monetization prospects, but it is unlikely to significantly alter its competitive advantage.

i) Why focus on the B-end? On one hand, the most widespread C-end use case is photo editing, which, as emphasized by Dolphin Research, relies on high-precision controllability as its core competitiveness (competitive edge). On the other hand, Skill is essentially an interface-based, modular capability that better aligns with the batch automation and productivity needs of B-end scenarios.

ii) Why is there monetization potential? Taking Meitu Design Room as an example, Dolphin Research previously highlighted 'workflow encapsulation' and 'low pricing' as key features of the product. Skill amplifies these advantages:

- Reusable workflows mean B-end users can build automation scripts based on them, further increasing migration costs when embedded into production processes. Skill, as a direct encapsulation of mature workflows, is attractive for scenarios requiring strong efficiency improvements.

- The pricing model, based on successful outcomes, significantly reduces trial-and-error costs for B-end users.

iii) Why is it difficult to change the competitive advantage? Integrating into the 'lobster ecosystem' does not enhance Meitu's competitiveness. The development threshold for Skill is low, and competitors or even individuals can create similar offerings. The core competitiveness still lies in its years of accumulated backend data assets. However, for new B-end businesses, Meitu is still in the accumulation phase.

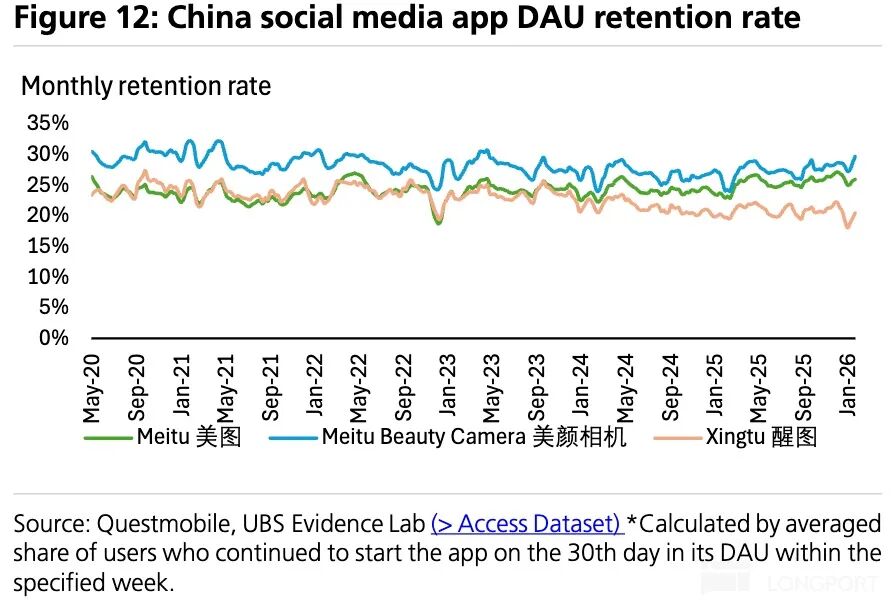

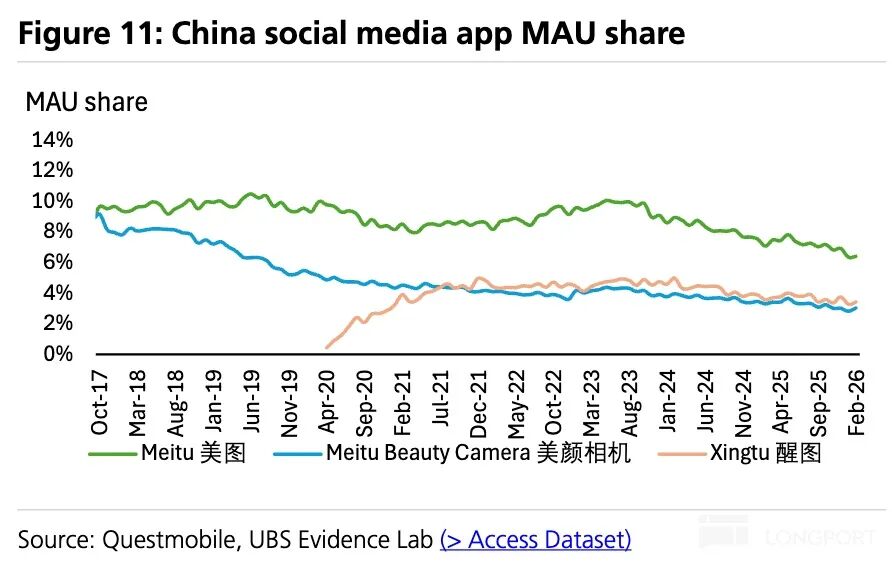

In summary, the C-end foundation has been undermined, leading to a significant drop in valuation. Fortunately, the competitive landscape remains relatively benign. The C-end business, with nearly 250 million users, remains the company's focus. According to UBS monthly tracking data, Meitu's MAU share in its product categories has remained stable, and it continues to lead the domestic photo editing market.

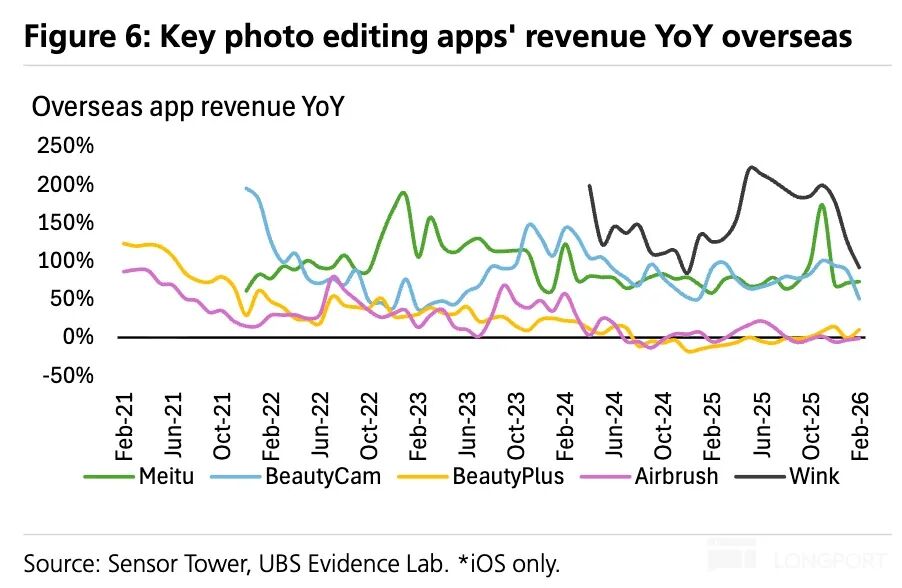

In video editing, Wink has seen explosive growth overseas, differentiating itself from ByteDance's CapCut and maintaining annual revenue growth exceeding 100%.

However, the MAU share in its track (market segment) continues to shrink, and combined with the weaker MAU data in the second half of the year, it is inevitable that large models will compete for light users. Nevertheless, the user structure has improved. Therefore, on the C-end, Dolphin Research advises against overemphasizing marginal MAU changes. Subscription penetration (implying the appeal of features to moderate and heavy users) and ARPPU growth (implying the value contributed by overseas markets) are more critical metrics.

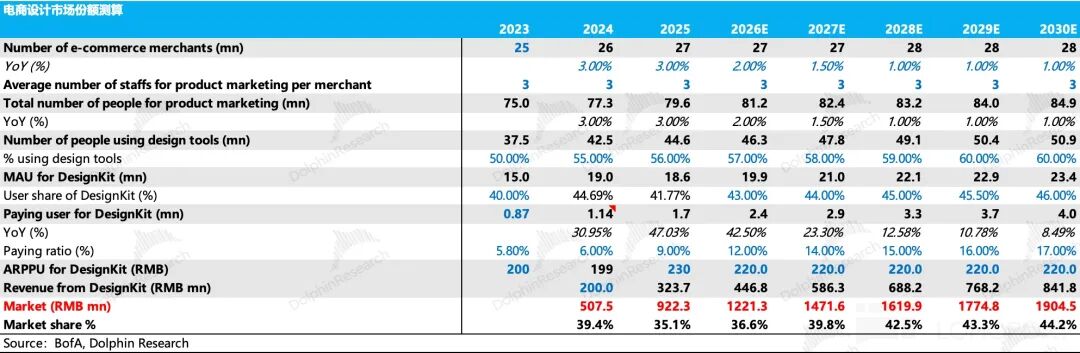

On the B-end, the financial report revealed that the company will hold an Imaging Festival in June this year to launch new productivity products. Based on Dolphin Research's calculations, the current market size for Meitu's involvement in product photography and live-streaming commentary segments is only around 2.5 billion RMB. This is a result of the company actively avoiding competition with tech giants, giving it a somewhat precarious position. Undoubtedly, the company's decision to proactively expand into vertical B-end scenarios to compete with general-purpose large models is correct. However, considering the financial data, it is challenging for capital to place high expectations on a B-end business experiencing slowing growth in both MAU and subscription penetration. The company needs to demonstrate greater resilience in its future quarterly core data disclosures.

Financial Report-Related Charts

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting is permitted only with authorization.

// Disclaimer and General Disclosure

This report is intended solely for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated entities. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or particular needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibility or loss that may arise from the use of the data contained in this report. The information and data contained in this report are based on publicly available sources and are intended for reference purposes only. Dolphin Research strives to ensure, but does not guarantee, the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or the views expressed in this report shall not, in any jurisdiction, be considered or construed as an offer to sell or a solicitation of an offer to buy securities, nor shall it constitute advice, an inquiry, or a recommendation regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for, nor are they intended to be distributed to, jurisdictions where the distribution, publication, provision, or use of such information, tools, and materials would contravene applicable laws or regulations or would result in Dolphin Research and/or its subsidiaries or affiliated companies being subject to any registration or licensing requirements in such jurisdictions, or to citizens or residents of such jurisdictions.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated entities.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) produce, copy, duplicate, reproduce, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all related rights.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?