Large Models Disrupt Online Education Business Model Unexpectedly

03/30 2026

03/30 2026

474

474

Leading large model companies like OpenAI and Anthropic have yet to go public, but their impact on listed companies is already palpable. Among the first to be visibly and directly affected by these large models, Chegg stands out as a representative example.

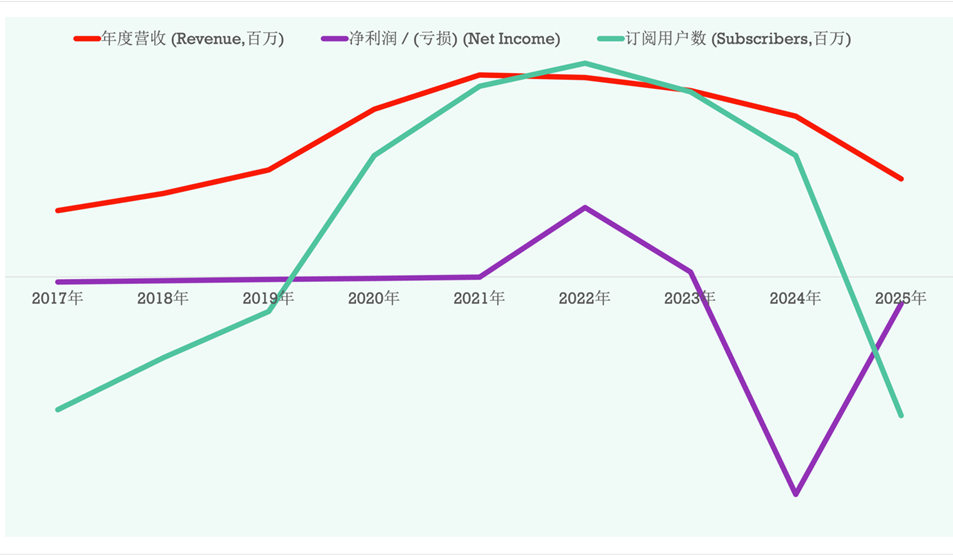

On March 23, 2026, Chegg's stock price plummeted to an all-time low of $0.57. From its peak of over $113 during the 2021 pandemic, the decline exceeded 99%. Additionally, it has lost 93% of its value from its early highs post-IPO.

This company, once considered a benchmark in online education, now boasts a market value of less than $100 million, starkly illustrating how the AI wave is consuming traditional business models.

01

Chegg's History and Business Model

Chegg's roots can be traced back to 2005, during the early days of the mobile internet. Founders Josh Carlson, Osman Rashid, and Aayush Phumbhra spotted a business opportunity on the campus of Iowa State University. Initially launched as a classified information website, they swiftly pivoted to the high-barrier niche market of textbook rentals.

Unlike the low-cost textbooks in domestic universities, textbooks for higher education in the United States are subject to publisher monopolies, frequent updates, and mandatory bundling of electronic access codes, resulting in exorbitant prices. During the 2017-2018 academic year, college students spent an average of $1,250 on textbooks and supplies, prompting many to turn to second-hand trading or rental markets.

Chegg capitalized on this pain point: starting with subscription-based textbook rentals in 2005, it exceeded $10 million in revenue by 2008. In November 2009, it secured $57 million in financing and entered an expansion phase. Subsequent growth has consistently revolved around the core of 'students—tutoring'.

In 2010-2011, it launched a digital learning platform with course selection and homework tutoring functions. In 2013, it raised another $25 million and went public on the New York Stock Exchange in November of the same year, raising $187.5 million. Post-IPO, it continued to deepen cooperation with textbook publishers to solidify its position in the tutoring market.

However, its pure digital subscription business progressed slowly, launching the educator content-sharing platform Uversity only in June 2021. This platform, however, still relied on a static question bank and lacked dynamic ecosystem operation capabilities.

From 2020 to 2023, the global pandemic drove up demand for online education, and Chegg's stock price once surged past the $100 mark, with subscription users peaking at over 8 million.

02

Chegg's Global Crisis

Beginning in 2023, the wave of generative AI swept through the market, and Chegg was among the first to be hit hard.

Its core classroom tutoring business essentially matches teachers and students for 1v1 paid Q&A, which highly overlaps with ChatGPT's conversational interaction. The latter offers comprehensive knowledge coverage, instant responses, and no fatigue, far surpassing human tutors in patience and consistency.

Even more damaging was the impact on traffic.

In February 2025, Chegg formally sued Google and its parent company Alphabet, accusing AI Overviews (AIO) of directly generating summaries in search results, intercepting user traffic that would have otherwise gone to Chegg. This led to a 49% year-on-year plunge in non-subscription traffic in January 2025.

This 'interception' effect, compounded by the proliferation of AI tools, directly triggered a cliff-like loss of subscription users. In fiscal 2025, Chegg's total revenue fell to $376.9 million, down 39% year-on-year. Revenue from its core Chegg Study (search subscription) business plummeted from about $500 million in 2024 to about $300 million.

In response to the crisis, Chegg launched its own AI tutoring platform, CheggMate, in 2023—a conversational learning assistant powered by GPT-4 and trained on its own datasets, allowing students to ask open questions and receive step-by-step answers.

However, this defensive move failed to reverse the user migration trend: students turned directly to ChatGPT, Claude, or Gemini for help.

In October 2025, the company announced a major restructuring, laying off about 45% (388 people) of its workforce. The CEO attributed the main reason to the 'dual impact of the AI new reality and Google AIO'.

Figure: Chegg experienced revenue and user turbulence from 2017 to 2025

03

Chegg's Self-Redemption

Facing irreversible user loss, Chegg chose to proactively transform: shifting from a traditional model targeting C-end students to B-end enterprise- and institution-driven SaaS services, launching the Skilling business.

This business comprises two major modules—the language learning platform Busuu, acquired in 2021, and the vocational skills training product Chegg Skills (derived from the earlier acquisition of Thinkful).

Skilling focuses on the non-standardized vocational training niche that AI has not yet fully penetrated, offering 'career entry' courses in programming, data science, UX design, and more. In 2025, it launched AI-era specialized content, such as 'prompt engineering' and 'AI-driven business analysis,' precisely targeting enterprise demand for emerging talent.

Busuu, on the other hand, positions itself as a global language training platform, emphasizing workplace spoken language and practical applications, with a 2025 target revenue of about $48 million, accounting for about 70% of Skilling's business.

From the data, Skilling contributed $68.7 million in revenue in 2025, accounting for 18.2% of the annual total. Although it declined slightly year-on-year, it achieved 11% growth in Q4, showing signs of a rebound.

The company has now split its business into two units: Skilling as the growth engine and Academic Services (traditional academic services) as the cash flow source, aiming to achieve net debt-free status with substantial cash reserves by the end of 2026. It has also significantly cut capital expenditures, focusing on expanding B2B partnerships.

04

Current and Future Pressures

However, while this transformation has a clear path, it struggles to fully compensate for the massive gap in the core business.

The Q1 2026 guidance shows total revenue expected to be $60-62 million, with Skilling contributing $17.5-18 million. The company hopes Skilling will achieve double-digit growth throughout the year, relying on the $4 billion vocational skills training market.

But the competitive landscape is already a red ocean: Coursera and Udemy have deep roots, with first-mover advantages in content breadth, certification systems, and enterprise integration. Chegg's differentiation—B2B career 'stepping stone' courses—can establish a foothold in the short term but is unlikely to form an overwhelming barrier in general training.

A deeper crisis lies in the fact that AI has driven the marginal cost of knowledge acquisition to near zero, fundamentally dismantling the 'information intermediary' logic on which Chegg relies.

Textbook rentals depend on U.S. resource monopolies and high pricing thresholds, while tutoring subscriptions rely on paid access to information gaps. In the large model era, these intermediary links are bypassed directly. CheggMate, Skilling, and even AI-specialized courses are essentially self-rescue efforts built on AI, but they also accelerate the demise of traditional businesses.

05

AI as a Stress Test for Business Models

Chegg's fate is not an isolated case but a microcosm of the collective survival struggle of first-generation EdTech companies in the AI era. Those relying on single content, information asymmetry, or intermediary fees have exposed their fragility in the face of generative AI's zero marginal cost.

Companies must confront the core question: What proportion of their services can be directly replaced by AI? How can they rebuild an irreplaceable moat on top of AI—through exclusive data, community trust, offline certification, deep enterprise integration, or genuine human value output?

Chegg is navigating the 'old sea' with Skilling but finds itself in another fiercely competitive 'red ocean.' In the current macro environment, the willingness of companies and individuals to pay for vocational skills training remains uncertain. If AI capabilities continue to leap exponentially, today's transformation may soon become the new 'textbook rental'.

AI is not just a technological revolution but a rigorous test of business logic. The adaptable survive; the lagging perish.

Chegg's case serves as a wake-up call for all companies relying on knowledge or information intermediation: In this wave, only by proactively reshaping their underlying architecture can they avoid being completely overwhelmed.

-

How Meituan is Becoming the 'Interface' for AI Integration into the Physical World

-

![]()

RoboScience Machine Science Makes ICRA Best Paper List for Two Years Running with Its 'Embodied Brain' Innovation

-

![]()

Focusing on UTG Ultra-Thin Flexible Glass! CSG Optical New Material Production Base Establishes in Xianning, Hubei

-

![]()

AI Meets Optics: Tsinghua Smart Vision Secures A+ Round Funding Led by Hillhouse Capital

-

![]()

Why are 3C Brands Flocking to Douyin Mall During 618?

-

![]()

Token Economy Falters as Economic Tokenization Faces Challenges

-

![]()

Lenovo's Monthly Surge of 109%, Foxconn Industrial Internet's Market Cap Surpasses Kweichow Moutai: A Collective Resurgence of the 'IT Old Guard'?

-

![]()

After Zhang Xue's Victory, Where is Motorcycle Intelligence Headed?