The 'Hidden Costs' and 'Explicit Anxieties' in Robot Financial Reports

04/13 2026

04/13 2026

628

628

What domestic robots lack most right now is not money

In 2026, the capital market's enthusiasm for humanoid robots remains high.

Since March, there has been a continuous stream of investment and financing news in the embodied intelligence industry. Yinhé General announced the completion of a new round of financing totaling 2.5 billion yuan, while Songyan Power completed a Series B financing of nearly 1 billion yuan. Data from IT Juzi shows that as of March 20, 2026, there have been 207 financing events in China's robot sector this year, with 133 involving humanoid robots, and a total of 115 companies securing funds.

The primary market continues to bet heavily with real money, keeping the track (sàidào: sector) hot, yet on the other side of the ocean, a different scene unfolds.

Silicon Valley star startup K-Scale Labs suddenly disbanded its team and open-sourced all its technology on the eve of mass production, with only $400,000 left in its accounts; Rethink Robotics, a pioneer in collaborative robots, went bankrupt for the second time in August 2025 after its initial collapse in 2018; social robot manufacturer Aldebaran shut down in February 2025; children's companion robot Embodied closed; and iRobot, the pioneer of robotic vacuum cleaners, filed for bankruptcy protection in December 2025... These once-shining names all fell just before 'dawn.'

This contrasting situation of 'heat and cold' forces the market to ask: How far have robots actually come? Against this backdrop, a group of robot companies, including UBTECH, Dobot, Geek+, and Unitree, have successively disclosed their 'report cards' for the past year. From these financial reports, we might find some answers.

01

Revenue is up across the board, but few are profitable

Looking at the financial reports, the most intuitive (zhíguān: intuitive ) (intuitive) signal is that everyone is selling more.

In 2025, UBTECH's revenue reached 2.001 billion yuan, a year-on-year increase of 53.3%; Geek+'s revenue was 3.171 billion yuan, up 31.6%; Woan Robot, which went public on the Hong Kong Stock Exchange late last year, reported revenue of 900 million yuan, a 47.7% increase; Dobot, the 'first collaborative robot stock,' had revenue of 492 million yuan; and Unitree's revenue was 1.708 billion yuan, a massive 335% year-on-year increase.

The entire industry is undergoing a collective transition from 'prototypes' to 'commodities.' Humanoid robots, warehousing robots, household robots, and collaborative robots each have their own logic for scaling up, but beneath the consensus on growth, structural concerns persist in the industry.

First, while revenue is rising, profits are not.

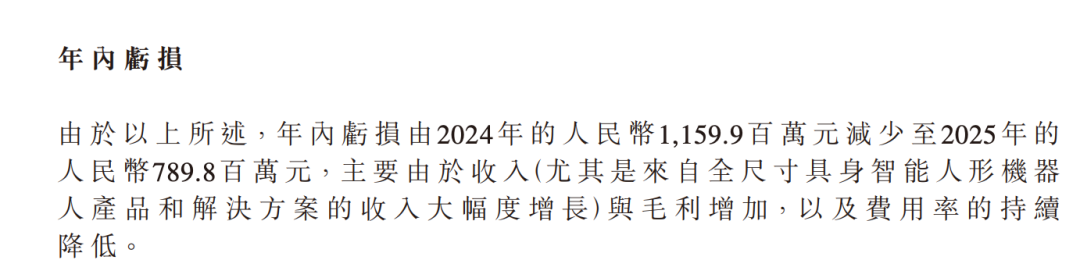

Financial report data shows that UBTECH incurred a loss of 790 million yuan, narrowing by 370 million yuan from the previous year but still far from breaking even; Dobot reported a net loss of 84.04 million yuan, narrowing by 11.316 million yuan year-on-year; Huayan Robot reported a loss of 15.6 million yuan in the first nine months of 2025; and Yunji Technology fared even worse, with total revenue of just 550 million yuan from 2022 to 2024 but losses reaching 800 million yuan.

Except for Unitree and Geek+, the vast majority of publicly traded robot companies remain stuck in the quagmire of 'increasing revenue without increasing profits.' Even Geek+, which achieved profitability, did so for the first time on an adjusted basis and is highly dependent on high-margin overseas markets; Unitree's profitability is built on a special structure where research and educational customers account for over 70% of its business.

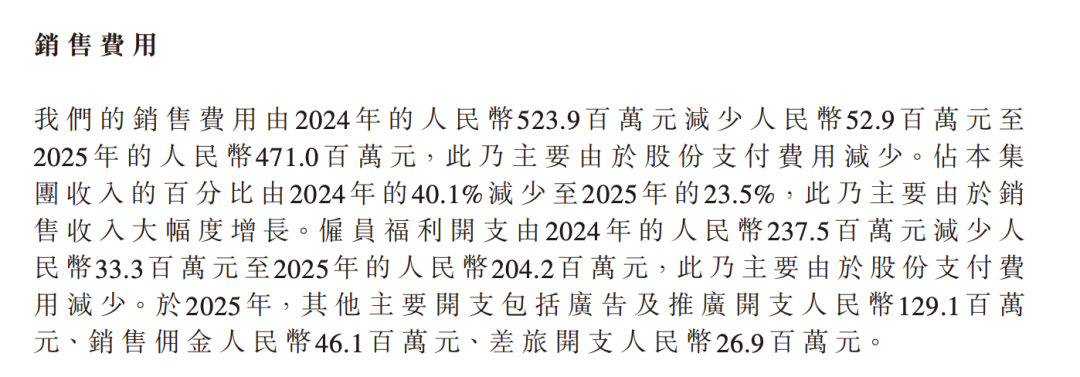

Second, losses are narrowing, but 'bleeding' has not stopped.

'Three expenses' (selling, general, and administrative expenses) remain high across the board. For example, UBTECH's combined selling, general, and research and development expenses in 2025 totaled 2.561 billion yuan, higher than its revenue; Dobot's selling and distribution expenses increased by 32.1% year-on-year to 182 million yuan; and Woan Robot's selling expenses surged by 81.3% year-on-year to 312 million yuan.

Although Unitree Technology achieved per-capita revenue of 3.55 million yuan with a team of just 480 people, this was the result of an 'extremely simple product line + deeply integrated supply chain + highly refined team + highly dispersed customer base' and is not universally applicable in the industry. Most companies are still in the extensive stage of 'revenue growth driven by input,' and the inflection point for economies of scale has not yet arrived.

Third, pressure on cash collection is mounting.

Take UBTECH, an early player in embodied intelligence, as an example. While increased sales of humanoid robots have driven revenue growth, accounts receivable have also soared. In 2025, its accounts receivable reached 1.842 billion yuan, a 40% year-on-year increase, with accounts receivable/revenue exceeding 92% and bad debt provisions reaching 539 million yuan, a 29% provision ratio.

For most robot companies, customer structure determines cash flow quality. Manufacturers with governments and large manufacturing enterprises as their main customers may have impressive book revenue, but cash flow tightness persists. Once accounts receivable aging worsens, bad debt provisions will eat into profits.

These three underlying concerns all point to a core contradiction: the robot industry is moving from 'able to demonstrate' to 'able to work,' but a vast technological and commercial gap remains between 'able to work' and 'able to make money.'

02

From the 'cerebellum' to the 'brain'

Over the past two years, the technological narrative in the robot industry has mainly revolved around 'locomotor capabilities.'

In 2024, Unitree Technology achieved the world's first full-sized electrically driven humanoid robot backflip in place, and in 2025, its humanoid robot exceeded a running speed of 5 meters per second, setting a new world record; UBTECH's Walker S series completed complex operations such as handling, sorting, and quality inspection in factories...

These breakthroughs led the outside world to believe that the 'body' issues of robots had largely been solved, but the R&D investment structure revealed in robot financial reports hides undeniable 'anxiety.'

Unitree Technology raised 4.2 billion yuan in its IPO, with nearly half of it (2.022 billion yuan) explicitly earmarked for embodied large model R&D; UBTECH invested over 500 million yuan in R&D in 2025, with 270 million yuan allocated to full-sized embodied intelligent humanoid robots. The company predicts that its R&D budget will further increase to 700 million yuan in 2026, focusing on embodied large models, world models, and product iteration.

Meanwhile, Dobot's R&D expenses increased by nearly 60% year-on-year, with most of the new investment going to embodied intelligence, amounting to 45.1 million yuan, accounting for 39.3% of total R&D investment; Geek+, despite being profitable, established an embodied intelligence subsidiary in July 2025 to strategically layout (bùjú: layout) the embodied intelligence sector and broaden its technological boundaries...

Clearly, R&D resources across the industry are shifting from the 'cerebellum layer' to the 'brain layer.' Behind this shift is the gradual convergence of hardware gaps among companies, where 'running faster and jumping higher' no longer suffices as a differentiated barrier.

In March 2025, Goldman Sachs released a field research report on Unitree Technology, with a core judgment pointing to a structural imbalance in the company's technological architecture: 'Unitree's robots are strong in gait control technology, not in the brain.'

The report noted that Unitree's perception layer adopts a multi-sensor fusion solution combining 3D LiDAR, depth cameras, and wide-angle cameras, while the decision-making layer's UnifoLM large model integrates reinforcement learning with simulation training; the execution layer achieves millisecond-level joint response based on model predictive control. However, these three layers have not yet achieved true end-to-end fusion. Semantic understanding at the perception output level is shallow, the decision-making layer's generalization ability for open-domain tasks is weak, and the execution layer's precision in following high-level intentions is limited.

This is not a problem unique to Unitree but a technological commonality across the industry. Hardware has reached global top-tier standards, yet robots still cannot independently understand tasks, plan paths, or handle unexpected situations.

Thus, the shift in technological focus from the 'cerebellum' to the 'brain' may signify a changing dimension of competition. In the past, the focus was on supply chain integration capabilities and motion control algorithms; in the future, it will be on generalization abilities from virtual simulation to the real world.

This arms race has far higher barriers than hardware-level competition, requiring not only sustained financial investment but also overcoming the bottleneck of 'high-quality physical interaction data,' a resource even scarcer than funding.

03

How far is the 'GPT moment' for embodied intelligence?

Data, especially high-quality data, has always been the most critical constraint variable in the evolution of embodied intelligence.

The breakthroughs in language large models over the past few years were fundamentally possible due to the vast amounts of publicly available text data on the internet, but embodied intelligence faces a completely different data dilemma.

It requires interaction data from the physical world, such as visual sequences, force feedback, tactile signals, and corresponding motion instructions generated when robots perform tasks in reality. Collecting such data can only be done in real or high-fidelity simulated environments, making it extremely costly and difficult to generalize.

Liu Peichao, founder of Dobot, once stated: 'The valuable data accumulated in the industry last year did not exceed 30,000 hours. There may be hundreds of thousands of hours of data that are not very valuable, useful only for pre-training and difficult to generalize and improve (robot operation) accuracy.'

As the importance of high-quality data grows, 'where does the data come from' ceases to be a technical question and becomes a strategic one. Facing this common dilemma, companies have provided starkly different answers based on their own strengths.

Unitree's strategy is to 'feed data with hardware.' With 5,500 humanoid robots deployed in global labs and universities, buyers use these platforms to run their own algorithms and conduct research, objectively accumulating diverse scenario data for Unitree.

UBTECH's strategy is to 'exchange data for scenarios.' The Walker S series is directly deployed in the production lines of BYD, Audi FAW, and Foxconn, using billion-scale high-quality data from real industrial scenarios to train its self-developed Thinker large model.

Dobot's strategy, on the other hand, is to 'build data reflow (huíliú: reflow ) (reflux) through scale.' By shipping hundreds of thousands of robotic arms annually, it constructs a data reflux system that continuously feeds operational data from different factories and workstations back into model iteration.

The speed and cost of acquiring high-quality physical interaction data directly determine the evolutionary pace of embodied intelligence large models. This means that competition over the next two to three years will essentially be a battle for data assets. Whoever can first establish a closed loop of large-scale, diverse, and high-quality real interaction data will gain the upper hand in the evolution of embodied large models.

Conversely, companies with insufficient data acquisition capabilities may gradually fall behind in the 'brain' competition, even if they have achieved excellence at the hardware level.

In summary, through these financial reports, revenue growth confirms the acceleration of commercialization, narrowing losses signal early signs of economies of scale, high accounts receivable highlight the immaturity of business models, and the collective shift in R&D investment structures indicates that the industry has recognized where the true bottlenecks lie.

The next two to three years will be a major test of each company's data strategies and technological roadmaps. Only those that have completed layout (bùjú: layout ) (layouts) at both the 'brain' and data ends will qualify to compete in the next phase.

* Image sourced from the internet. Please contact for removal if infringement occurs.

-

![]()

Is Design the Root of the Problem? The Lexus ES Dilemma: Despite New and Old Models Coexisting Post-Redesign, Sales Plummet by 40%

-

![]()

Are Japanese Automakers Now Taking Cues from China? A Perspective on Japan's Reversal in Learning

-

![]()

In the First Half of the Year, Car Companies’ Profit Margin Plummets to 3.8%! CPCA: Automakers Must Speed Up Battery Production Amid Upstream Pressures | MINGJING Pro

-

![]()

Tesla’s Q2 Revenue Rises, Yet Profitability Slips; Energy Storage Margins Take a Dive

-

Chinese Automakers Strike Gold Overseas: Prices Double?

-

![]()

Joint Ventures, Once Dismissed, Are Now Making a Comeback

-

![]()

Automotive Market News: Retail Penetration Rate of New Energy Vehicles Reaches 62.8%

-

![]()

Once a Sales Leader Among New Car Manufacturers, Now Selling Equipment at Bargain Prices