Performance Plunge: Splurging 1.8 Million Yuan on a South Korean Company with No Revenue to 'Save Face'? Leading Robot Stock Leaves 70,000 Investors Stunned

04/17 2026

04/17 2026

652

652

Source: Shenlan Finance

When the bubble of performance bursts, all the "speculative hype" becomes worthless.

Last night, Zhongda Lide—a once-high-flying stock in the robot reducer sector—poured cold water on the market.

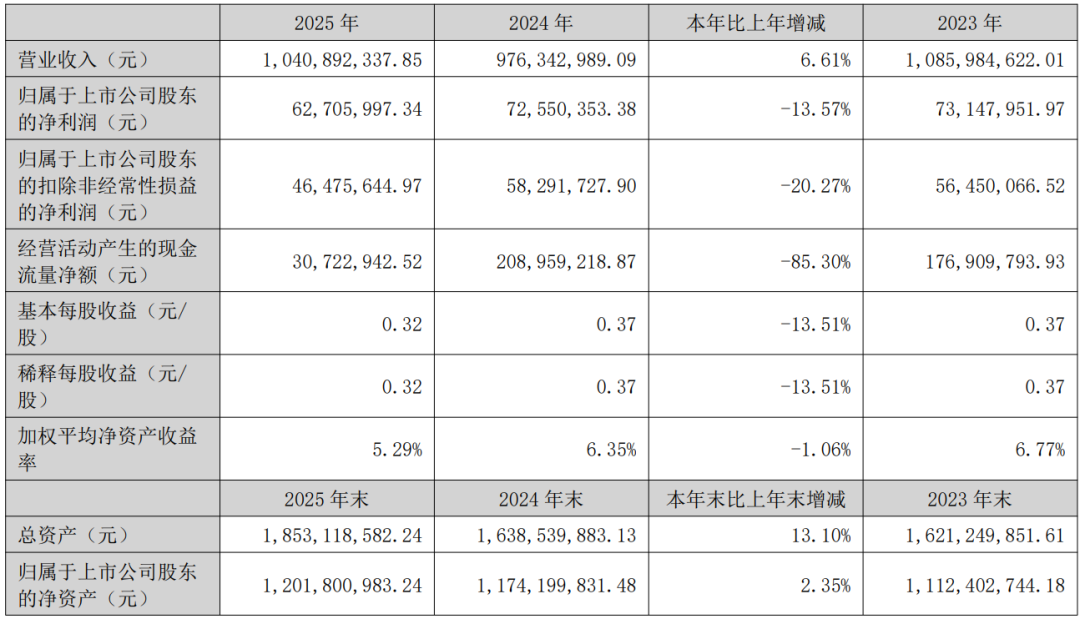

The 2025 annual report showed a full-year revenue of 1.041 billion yuan, a modest 6.61% increase year-on-year (YoY). Net profit attributable to shareholders fell by 13.57% to 62.706 million yuan. Net profit excluding non-recurring items plummeted by 20.27% to a mere 46.4756 million yuan.

This marks the second consecutive year of declining net profit for Zhongda Lide.

The past two years coincided with the peak of hype surrounding humanoid robots. Zhongda Lide, whose stock once soared fivefold, has now delivered a disappointing performance report. Faced with stark financial data, the bubble blown by "speculative hype" has burst.

What puzzles the 72,200 shareholders even more is that amid this performance collapse, the company plans to spend 1.8 million yuan to acquire a newly established South Korean firm with zero revenue and zero profit.

1

A 'Reducer Star' on the Rise: Stock Soars Amid Hype

Zhongda Lide has never been short of compelling narratives in the humanoid robot space.

Based in Ningbo and founded in 1998, the company is one of the few in China to master the core technologies for three precision reducers: RV, harmonic, and planetary.

What are reducers? They serve as the "joints" of robots, accounting for roughly 30% of the total machine costs, and represent one of the biggest bottlenecks to the mass production of humanoid robots.

The logic of "speculative hype" is straightforward: humanoid robots are poised for explosive growth, demand for reducers will surge, and Zhongda Lide—a leader in domestic substitution—will soar.

Its client list is impressive. Terminal customers listed in its annual report include Zhiyuan Robotics and Fourier Intelligence, both domestic leaders in humanoid robots, along with industrial players like Novolift, Hangcha Group, and Sany International.

In the narratives of "speculative hype," Zhongda Lide’s clients allegedly span the entire humanoid robot ecosystem, from Unitree Technology, Ubtech, Zhiyuan, and XPENG to Tesla.

For instance, one narrative claims that Zhongda Lide is the core supplier of planetary reducers for Unitree, accounting for 63% of its procurement volume, with locked-in orders worth 3.2 billion yuan in 2025.

Coupled with brokerage reports repeatedly emphasizing the "accelerated industrialization of humanoid robots," capital rushed in.

Over the past two years, Zhongda Lide’s stock price surged over fivefold from its low, fully pricing in market expectations.

2

More Absurd Than Missing Targets: Spending Millions on a Shell Company?

The results? The annual report laid bare the truth.

Full-year net profit shifted from slight growth in Q3 to a decline, with Q4 net profit attributable to shareholders at just 5.5 million yuan, down 64.8% YoY.

Net profit excluding non-recurring items was even bleaker. Government subsidies—a non-recurring gain—reached 20.3691 million yuan, accounting for 32.48% of net profit. The core business’s profitability decline far exceeded the surface-level data.

One telling detail: Institutions like Everbright Securities and Hualong Securities had forecast full-year net profit of 90 million yuan or higher, expecting over 24% YoY growth. The actual figure was just 63 million yuan—nearly 30 million yuan short.

Digging into the financials, several figures stand out.

Expenses eroded profits across the board. Revenue rose only 6.61%, yet selling expenses surged 19.41% to 48.2585 million yuan; administrative expenses jumped 22.73% to 81.0532 million yuan. R&D spending, meanwhile, slightly declined from 63.8495 million yuan to 62.9565 million yuan.

Inventory ballooned from 256 million yuan at year-end to 317 million yuan, with inventory write-downs reaching 15.188 million yuan—up over 60% YoY. In short, produced goods aren’t selling or fetching good prices.

Accounts receivable hit 125 million yuan, up 23.76% YoY, with bad debt provisions rising.

Net cash from operating activities plummeted 85% to 30.72 million yuan. Thin accounting profits were matched by even thinner cash inflows.

The most audacious move came on the night of the annual report release.

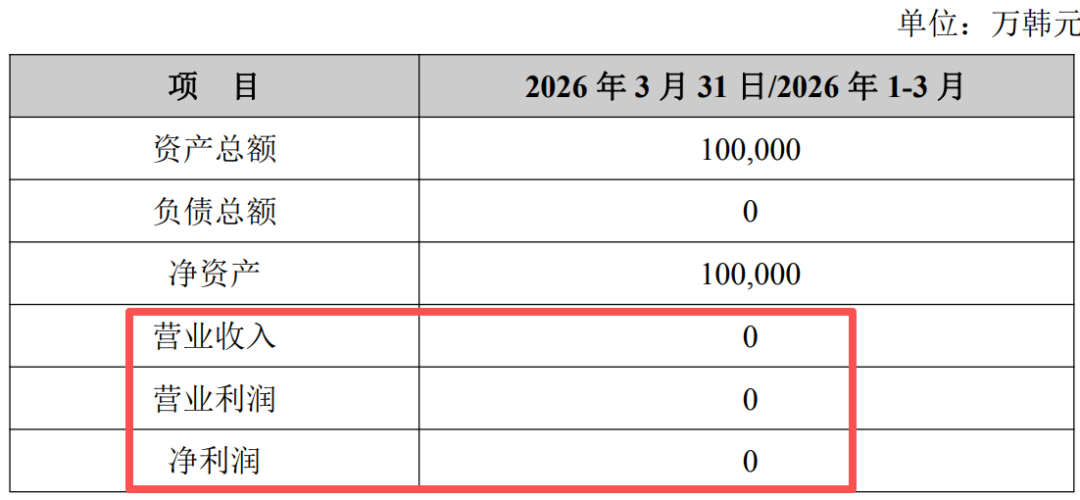

On April 15, before announcing its performance, the company preemptively announced plans to acquire a 39% stake in a South Korean firm named 'PM Co., Ltd.' for 390 million won. The headline figure sounds imposing, but in yuan—about 1.8 million yuan.

Shareholders’ comments cut to the chase: 'Releasing this acquisition before earnings—trying to offset a performance bomb with a 1-million-yuan deal? Dream on.'

A closer look reveals the proposed acquisition: a South Korean firm with zero revenue and zero profit, established recently on February 11, 2026. Essentially, spending 1.8 million yuan to buy a zero-revenue startup for 'show.'

Zhongda Lide’s overseas expansion is real—its Thai subsidiary did contribute 114,000 yuan in revenue in 2025. Total overseas revenue reached 93 million yuan, with plans to open subsidiaries in Germany and Vietnam. But timing this overseas acquisition smoke screen so obviously raises questions.

3

Not Alone: Hype Without Profit

Zhongda Lide’s missed targets aren’t isolated. The entire robotics supply chain, from downstream to upstream, is experiencing the awkward gap between "sky-high expectations" and "harsh reality."

Downstream, Unitree Technology led global shipments of pure humanoid robots in 2025 with just over 5,500 units. Ubtech remained unprofitable, selling only 1,079 full-sized embodied AI humanoid robots. Its major automotive orders involved annual deliveries in the hundreds.

Upstream, Sanhua Intelligent Controls, a thermal management leader, saw negligible revenue from robotics in 2025. Zhongma Transmission, a gear and transmission maker, posted its first annual loss of 5.8 million yuan.

Lead Harmonic Drive, a harmonic reducer leader, saw Q1-Q3 2025 net profit attributable to shareholders rise nearly 60%—one of the few upward revisions. Yet its gross margin fell from 39.53% to 36.60% YoY, reflecting an industry still in the investment phase, mired in price wars, low margins, and poor returns—far from mass profitability.

Goldman Sachs released a deep dive on humanoid robots in early 2026, noting their true AI capabilities remain unproven. It forecasts global shipments of 51,000 units in 2026 and 76,000 in 2027—a multiple jump from 15,000–20,000 in 2025, but far below market expectations of 500,000 units.

Goldman believes global shipments may only reach 502,000 units by 2032. True commercial scale won’t arrive until 2027–2030. The current phase hasn’t even completed the transition from "0 to 1."

Unitree’s robots flipping on Spring Festival Gala stages look cool—but that’s for research and performance. Tesla’s Optimus, which Elon Musk has hyped for "mass production next year" for years, keeps delaying. Ubtech’s industrial humanoid robots, despite orders from BYD and NIO, ship in the hundreds annually—hardly a robust supply chain.

Without real downstream orders, who will buy midstream reducers, motors, and drivers?

This is the fundamental logic behind Zhongda Lide’s consecutive missed targets. The market trades on 2030 expectations, but the company delivers 2025 results—a full production cycle apart.

4

Conclusion

Zhongda Lide isn’t without a future. Humanoid robots are a long-term, high-potential sector—no one doubts that. As a core component, reducers offer vast domestic substitution potential and technical barriers.

The issue is that stock prices have already priced in years of future narratives. When performance repeatedly disproves expectations, valuation corrections are inevitable. Hence the stock’s continuous decline since Q4 2025.

For investors, two things must be distinguished: the industry’s long-term trend and the stock’s short-term rhythm. The former is real; the latter may be a trap.

Until real mass production orders arrive, all surges may prove to be paper wealth.

Shenlan Finance’s new media cluster, rooted in the Shenlan Finance Journalist Community for 15 years, is a leading domestic financial new media platform. Its accounts focus on China’s most valuable companies, cutting-edge industries, and emerging regional economies, providing value-driven content for investors, corporate executives, and the middle class. Welcome to follow.

-

![]()

Wang Huiwen, Former Meituan Executive, Achieves 20-Fold ROI, Supports 24 AI Startups

-

![]()

Another AI Computing Power Unicorn Launches IPO! Founded by a Changjiang Scholar

-

![]()

OFILM Holdings Secures Zhongke Daojing, Marking a Significant Leap in the Optical Communication Industry!

-

What Will Be the Next Key Battleground for Large Models After AI Coding?

-

![]()

Leapmotor's Sales Soar, Yet Hidden Concerns Loom

-

![]()

China’s Action Camera Market Soars: 3.12 Million Units Sold in Six Months, DJI Secures 74% Dominance

-

![]()

Zhang Yiming: Strategic Retreat as a Path Forward

-

![]()

Exploring Charging for Some Features of QianWen App: Can It Follow the Path of Doubao?