China Breaches the Southeast Asian Defense Line of Japanese Automobiles

04/17 2026

04/17 2026

412

412

Introduction

This trend of one brand rising while another declines is particularly pronounced in the new energy sector.

Thailand serves as a pivotal automobile manufacturing hub and export base in Southeast Asia. Leveraging its highly developed industrial ecosystem and comprehensive parts support capabilities, its automobile production has consistently led the region, earning it the moniker of the “Detroit of the East”.

The Bangkok International Auto Show stands as the largest and most influential auto event in Southeast Asia, boasting significant commercial value. It is widely regarded as a barometer for the Southeast Asian automotive market.

Over recent years, the Bangkok International Auto Show has upheld a distinctive industry practice: on the exhibition's closing day, the organizer releases a comprehensive record of on-site bookings for each participating brand, utilizing real sales data to provide an intuitive snapshot of the latest market trends.

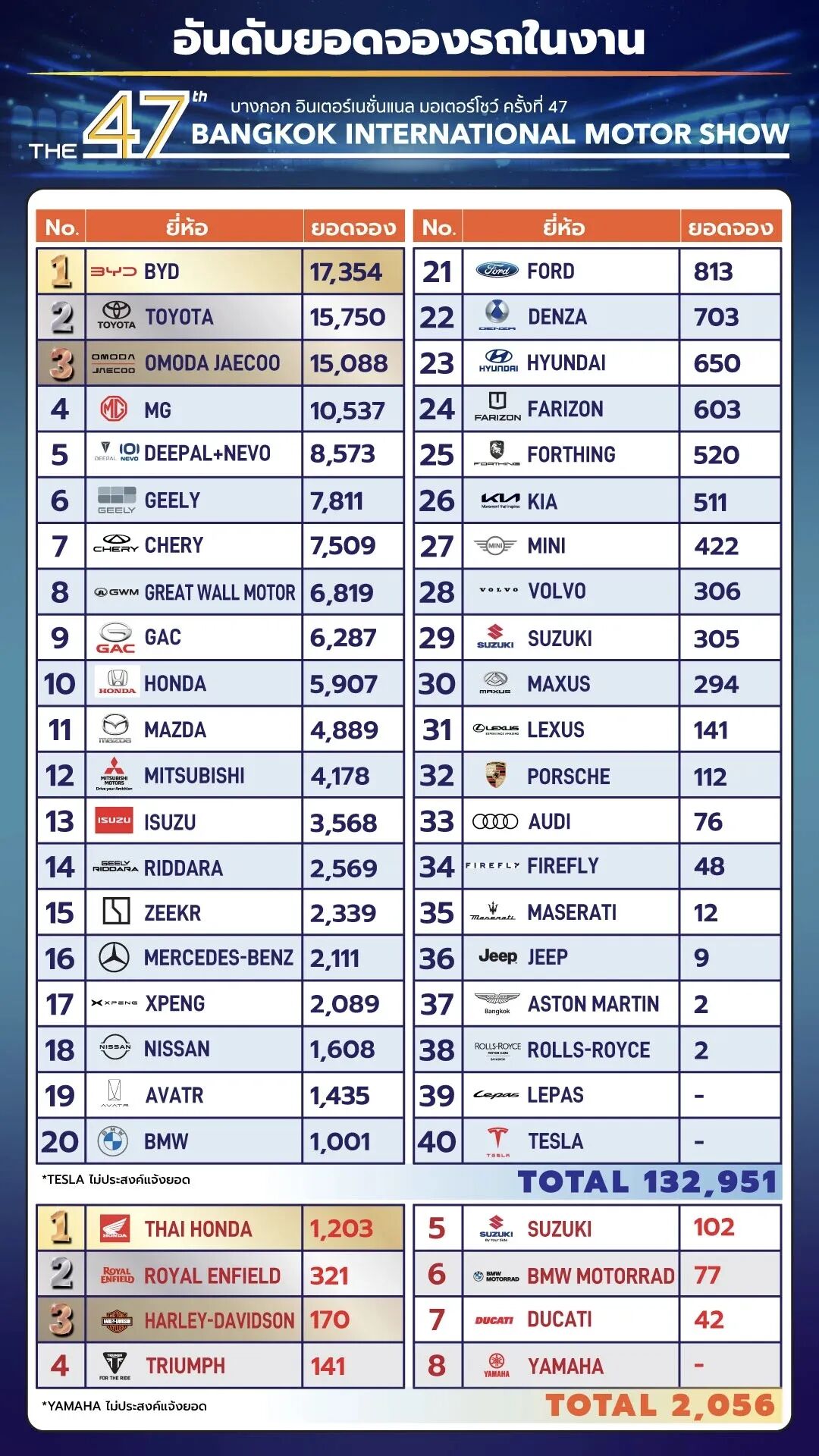

According to foreign media reports, at the recently concluded 47th Bangkok International Auto Show, the total bookings for the Chinese contingent surpassed those of Japanese brands for the first time.

Based on the organizer's statistics, BYD led the booking list at this auto show with 17,000 bookings (excluding Denza), surpassing Toyota's 15,700. Chery's OMODA & JAECOO secured the third position with 15,000 bookings.

Among the top ten automotive brands in terms of bookings, Chinese brands occupied seven spots, with MG, Changan Automobile, Geely Automobile, Great Wall Motors, and GAC Group all making the cut. Honda, as the second Japanese automotive brand to feature in the top ten, ranked tenth in overall orders at this auto show.

01 Chinese Brands Make a Splash in Thailand

The rapid progress of the Chinese contingent and the growing fatigue of Japanese brands were evident at the Bangkok International Auto Show. This event not only showcased the rise of Chinese automobiles in the local market but also vividly reflected the shifting landscape of the entire Southeast Asian automotive market.

The Southeast Asian automotive market has reached a turning point.

The era of Japanese dominance, which has spanned over half a century, is gradually drawing to a close. Japanese automotive giants, which once commanded nearly 90% of the market share in Thailand and constructed an impenetrable barrier, are now facing unprecedented market pressure and share loss in the face of the collective and rapid advance of Chinese brands.

According to data from the Automotive Industry Division of the Federation of Thai Industries (FIT), among the top ten automakers in terms of sales in the Thai market in 2025, Toyota still held the top spot with 230,000 units sold, followed by Honda and Isuzu Motors with 73,000 units each. However, Chinese brands secured five positions, demonstrating robust market growth momentum.

Among them, BYD ranked fourth with nearly 40,000 units sold; MG's annual sales exceeded 27,000 units, ranking fifth; Great Wall Motors, Changan Automobile, and GAC ranked eighth to tenth with 18,000, 14,000, and 13,000 units sold, respectively.

As early as 2019, Japanese brands commanded an overall market share of 87% in the Thai automotive market, with 89.6% in the passenger vehicle segment and as high as 85.3% in the commercial vehicle segment. This marked the peak period for Japanese cars in the Thai market, when only a handful of Chinese automakers, such as MG, were selling locally, accounting for a mere 2.8% of the market share.

In just six years, the market landscape has begun to reverse, with the monopoly advantage of Japanese cars continuously eroding and Chinese brands achieving exponential growth.

In 2025, Chinese automobile sales in Thailand exceeded 100,000 units for the first time, reaching 134,000 units, a year-on-year increase of 81%. The market share increased by nearly 10 percentage points from 2024 to 22%, second only to Japanese cars at 68%. It is worth noting that this is also the first time the market share of Japanese cars in Thailand has fallen below 70%.

This trend of one brand rising while another declines is particularly evident in the new energy sector.

In 2025, sales of pure electric models in Thailand reached approximately 120,000 units, a year-on-year increase of about 80%, with Chinese brand electric vehicles accounting for more than 80% of the market share. Looking ahead, this market landscape will further solidify, and the growth momentum will become even more pronounced.

According to data released by the Automotive Industry Division of the Federation of Thai Industries (FIT), total automobile sales in Thailand last year reached 621,000 units, an 8.5% increase compared to 2024. The core driving force behind this market growth is the rapid expansion of the new energy vehicle segment.

Data indicates that cumulative sales of new energy models in Thailand reached 276,700 units in 2025, accounting for 45% of total sales. It is particularly noteworthy that pure electric vehicles are gradually establishing market dominance, with their sales share continuing to expand and becoming a key driver of the overall increase in future new vehicle sales.

02 China Challenges the “Fortress” of Japanese Cars

Japanese cars have been deeply entrenched in the Southeast Asian market for seven decades.

After the 1950s, Japanese automakers gradually entered the Southeast Asian market. Later, influenced by the Plaza Accord on the yen, Japanese automakers massively accelerated localized production in the 1980s, establishing a highly mature industrial chain in Southeast Asian countries.

Consequently, Japanese cars have “set up camp” in Southeast Asia about 30 years earlier than their European, American, and Chinese counterparts.

For an extended period, benefiting from the characteristics of low investment and high returns in the Southeast Asian market, Japanese cars have regarded this market as a veritable profit engine and cash cow, as well as one of the important “fortresses” for the Japanese automotive manufacturing industry to stabilize its global industrial chain.

Now, this “fortress” is being challenged by Chinese automobiles.

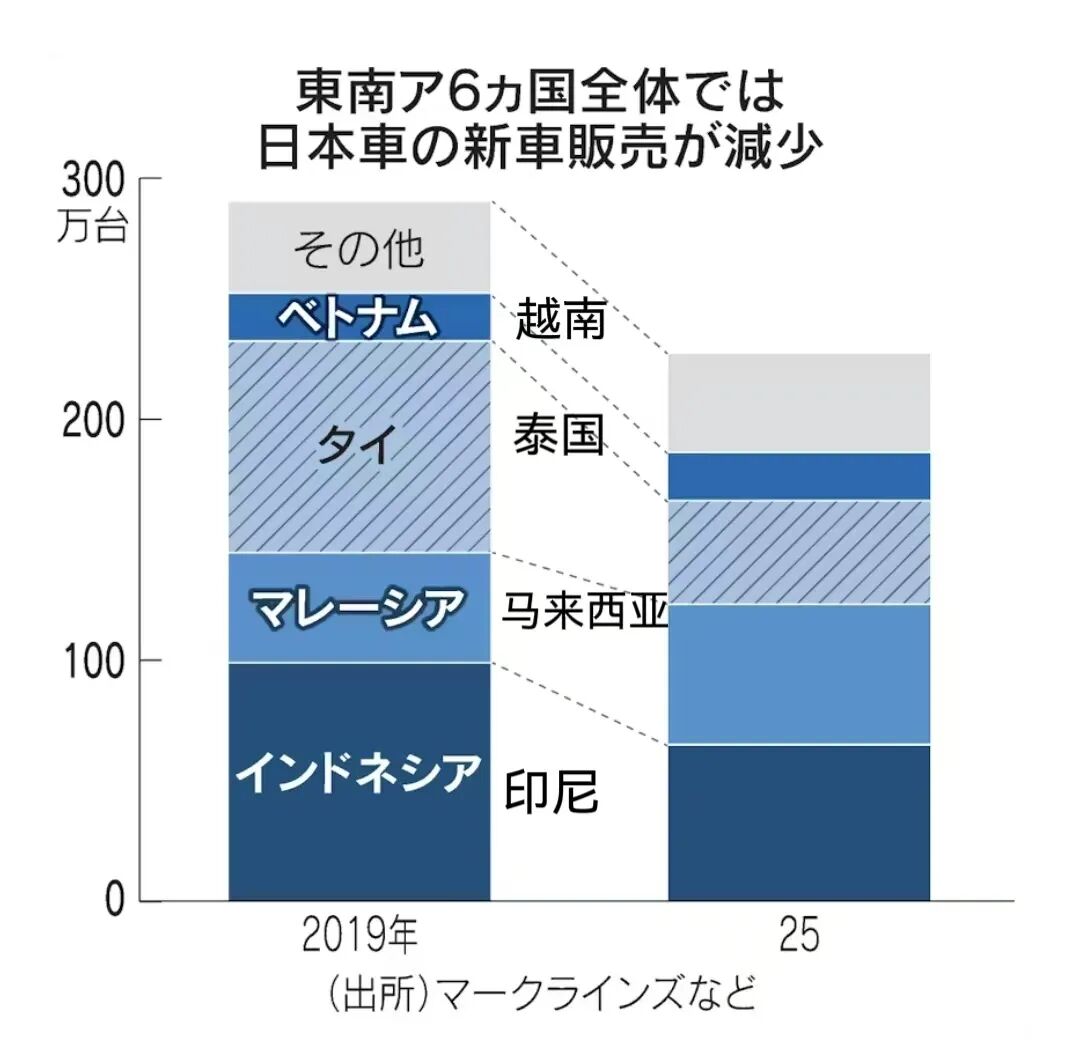

Nikkei Asia reviewed the market share of Chinese and Japanese automakers in new vehicle sales in six Southeast Asian countries in 2025, revealing that sales of Japanese cars have all declined from the previous year's levels. Over the past year, Japanese cars sold a cumulative 2.27 million units in the six Southeast Asian countries, a decrease of 22% compared to the peak in 2019.

Among them, the market share in Indonesia fell by more than 8 percentage points year-on-year to 81%; the Thai market fell by 9 percentage points to 68%; the Vietnamese market fell by 6 percentage points to 33%; the Malaysian and Philippine markets also saw declines of 3-4 percentage points, respectively, and Singapore also fell by 6 percentage points.

Indonesia has long been the largest automotive market in Southeast Asia (slightly surpassed by Malaysia in 2025) and the industrial and profit core of the region, becoming a “new battlefield” for Chinese automobiles to expand globally in recent years.

According to Nikkei Asia statistics, in just 2025, the market share of Chinese automobiles in Indonesia more than doubled year-on-year to 14%. It is worth mentioning that nearly half of the sales were contributed by BYD.

The watershed moment arrived around 2023.

In that year, the policy window in Southeast Asia fully opened, becoming the most critical external condition for Chinese automobiles to “land” in the Southeast Asian market.

Starting in 2022, the Thai government introduced the EV3.0 incentive policy for new energy vehicles, stimulating the market with a series of measures, and the policy had an immediate impact; at the end of 2023, Thailand introduced EV3.5, which mainly included provisions for purchase subsidies and reductions in consumption tax, road tax, and import tax.

In 2023, Malaysia announced an investment of 95 billion ringgit in the development of advanced manufacturing, with a focus on new energy vehicle research and development. Additionally, the government also introduced a series of tax relief measures, such as reductions in road tax for new energy vehicles.

From sporadic overseas expansion to systemic rooting, in just three years, Chinese automakers have completed a key leap in Southeast Asia from product exports to industrial rooting—complete vehicles, batteries, core components, and charging networks have been implemented in coordination, building their own new energy industrial ecosystem barriers with efficient cost control and highly competitive pricing strategies.

The market landscape once dominated by Japanese brands for an extended period is quietly being rewritten, and a more open, diverse, and dynamic new era of the Southeast Asian automotive industry is unfolding with the deep participation of Chinese Smart Manufacturing (intelligent manufacturing).

Editor in Charge: Du Yuxin Editor: He Zengrong

THE END

-

![]()

Jitian Xingzhou: A Pioneer in Optical Payloads Secures Hundreds of Millions in Series B Funding!

-

![]()

Orders Secured Through to the Second Half of the Year! The Rationale Behind the 'Surge' in Demand for This Company’s Optical-Grade Base Films

-

![]()

Beyond Patents: The Retail Rivalry of Insta360 and DJI Unfolds

-

![]()

180 Billion Market Cap Vanished! How Did Seres Fall So Far?

-

![]()

Blockbuster! Domestic storage takes the global double crown for the first time, from an AI company

-

![]()

China Spearheads Formulation! World's Pioneering Global Technical Regulation for Automated Driving Systems Greenlit and Unveiled

-

![]()

Farewell to Pulsed Support Policies: Three Major Auto Policy Directions from Multiple Departments Take Effect on the Same Day

-

![]()

Embercore AI’s Accelerated Funding: The Robot Industry’s Shift Toward ‘Learning Systems’