Coreweave: Strong Computing Power Sales, But Profitability Challenges Persist—Is Nvidia's 'Foot Soldier' Just Stuck in a Tough Spot?

05/09 2026

05/09 2026

553

553

AI new cloud unicorn CoreWeave released its Q1 2026 financial report after the U.S. stock market closed this morning (5/8). Overall, it was another familiar scenario of solid business and revenue growth, but profit decline worse than the lowered guidance.

This suggests the company may fall into a vicious cycle where higher revenue leads to greater losses over time, increasing concerns among investors already skeptical about the company's ability to achieve stable profitability in the medium to long term. Key details include:

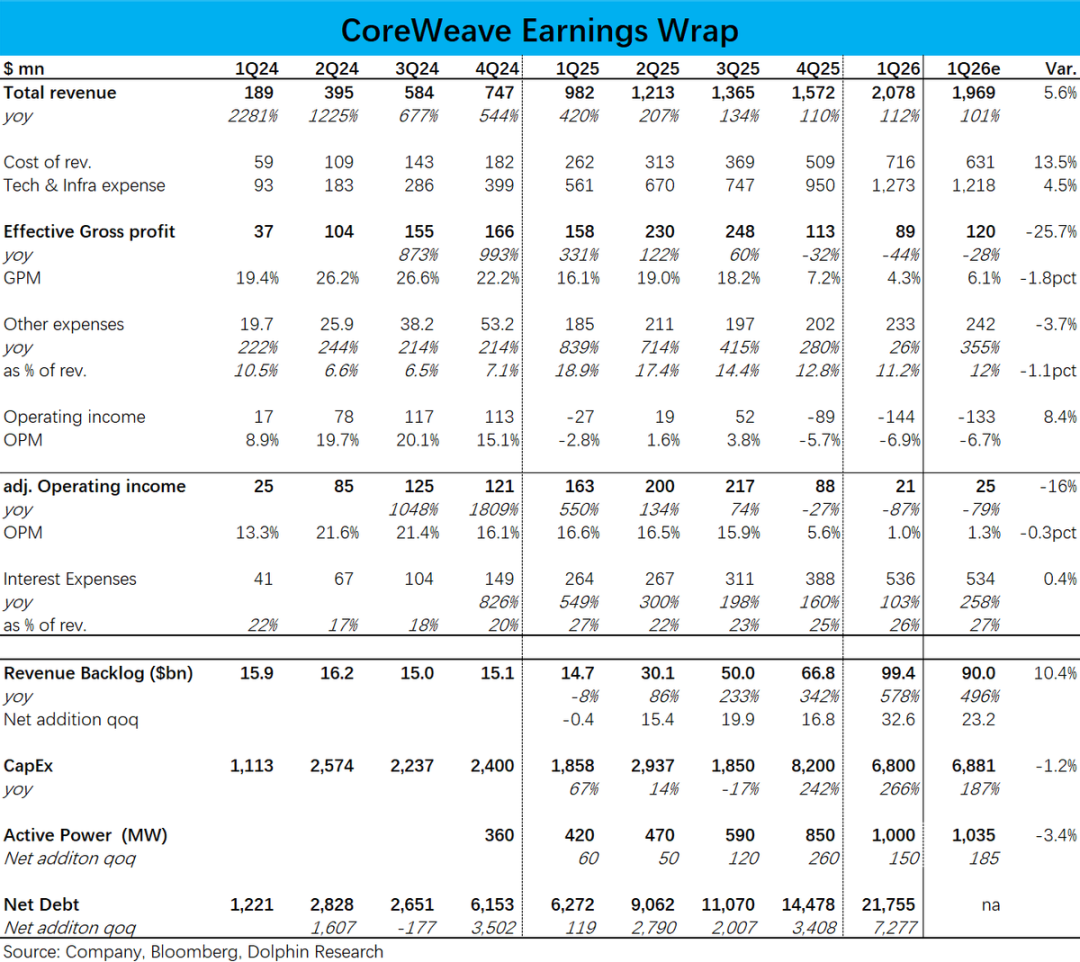

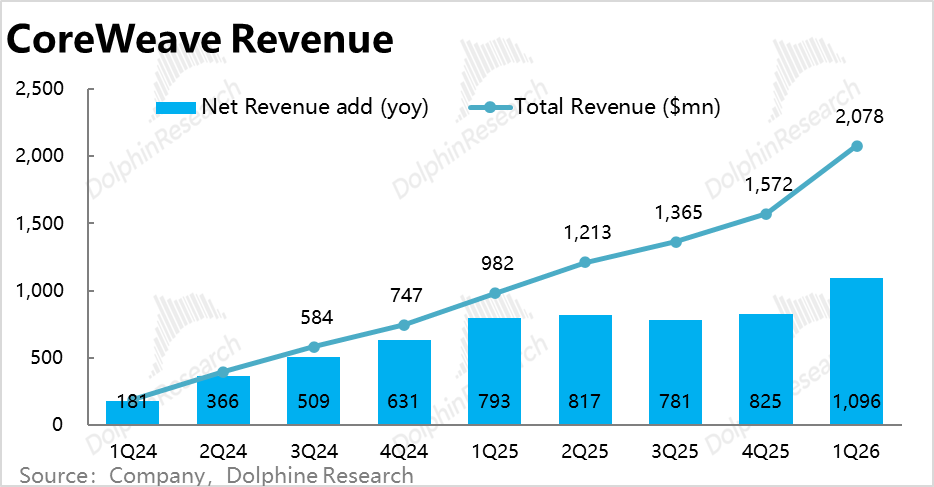

1. Record Revenue Growth: The company achieved nearly $2.08 billion in revenue, surpassing market expectations of $1.97 billion and exceeding the previous guidance range of $1.9-2.0 billion. The year-over-year net revenue increase reached nearly $1.1 billion, another all-time high.

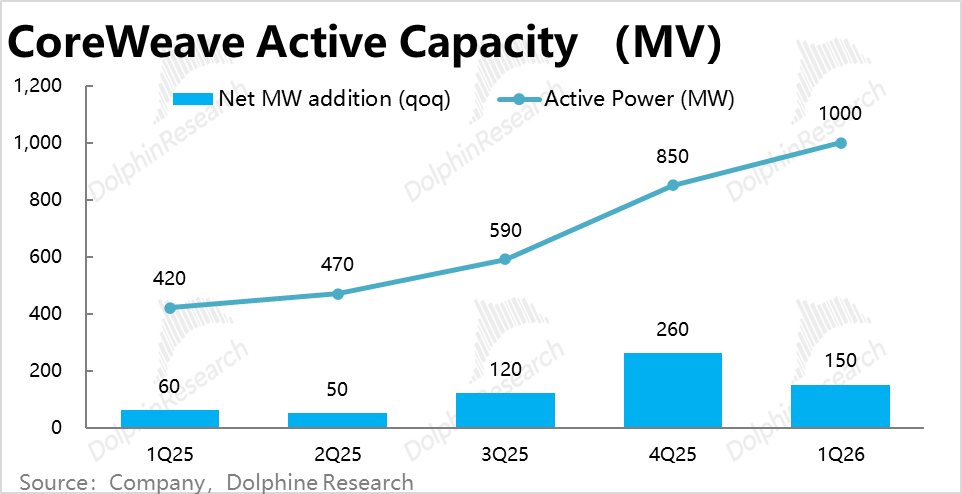

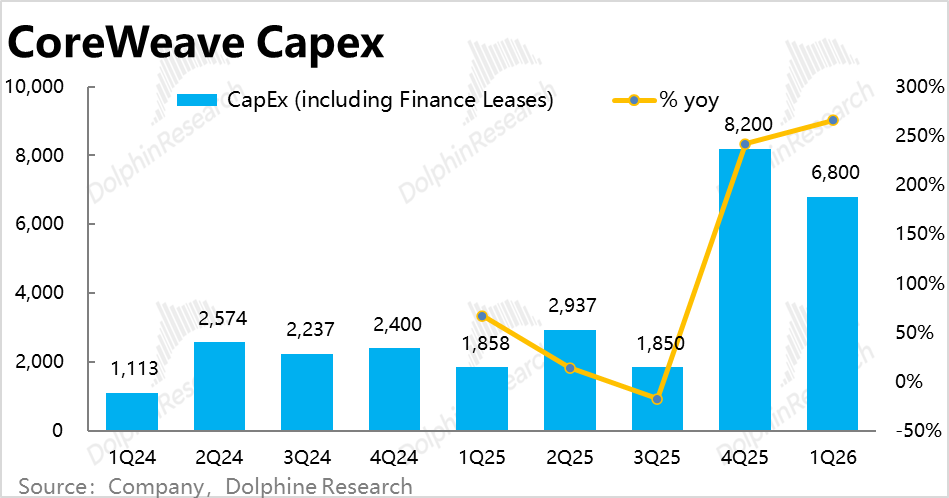

The underlying metric determining revenue, Active Power (online computing capacity), reached 1000Mw this quarter, generally in line with market expectations, with a net increase of 150Mw, though the growth rate slowed compared to the previous quarter. However, this was not surprising given that Capex guidance for this quarter was lower than Q4 last year.

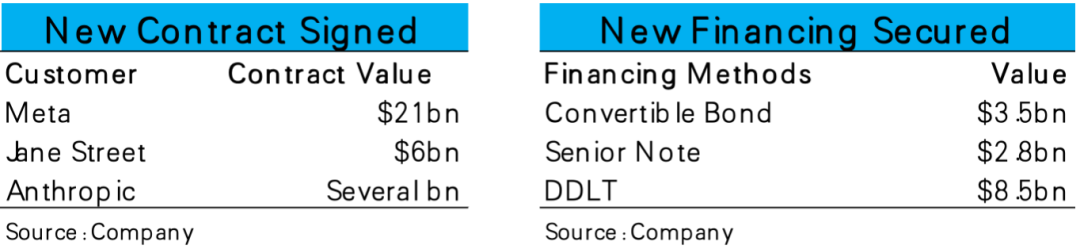

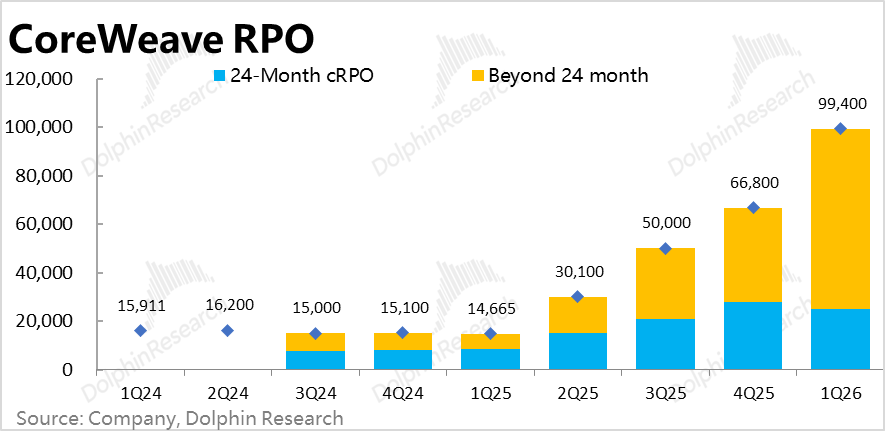

2. $30 Billion in New Orders, Continued Customer Base Optimization: The remaining performance obligation (RPO) reached $99.4 billion, a net increase of about $33 billion from the previous quarter, marking the highest single-quarter new order volume. This largely aligns with previously reported orders, including $21 billion from Meta, $6 billion from Jane Street, and approximately several billion from Anthropic.

Structurally, the RPO balance within 24 months actually declined, with all new additions exceeding 24 months, indicating that most newly signed contracts will not begin implementation until after 2027. Additionally, the company has now signed contracts with all Top 4 AI model providers, reducing its reliance on OpenAI as a single major customer.

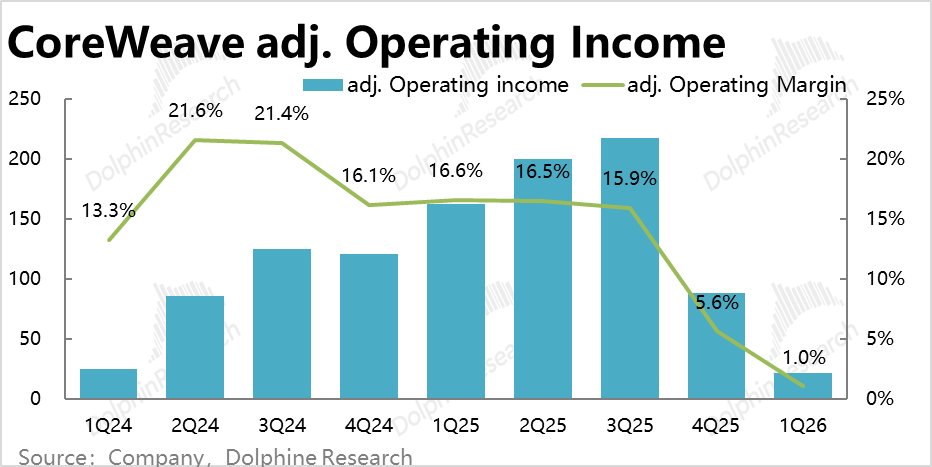

3. Significant Profit Decline: Despite accelerated revenue growth, the company's profit pressure became more evident. The adjusted operating loss for the quarter was $144 million, compared to an $89 million loss in the previous quarter, with losses widening and worse than expected.

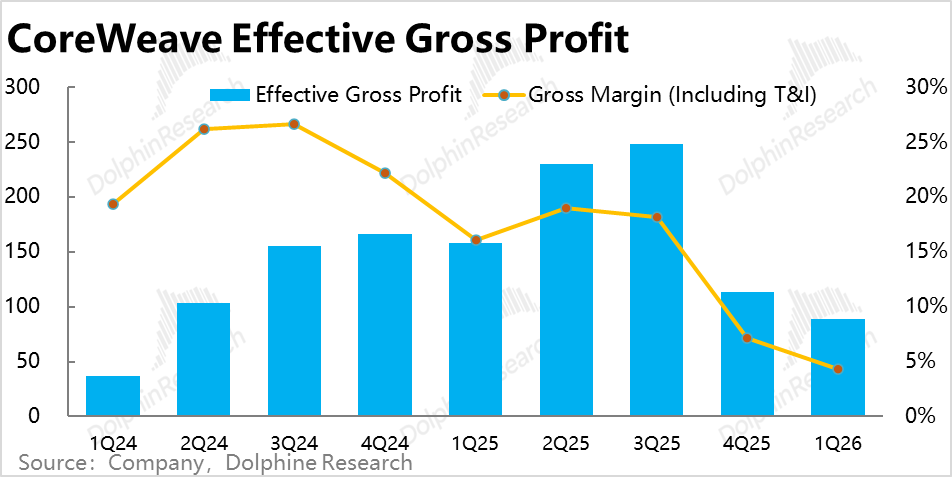

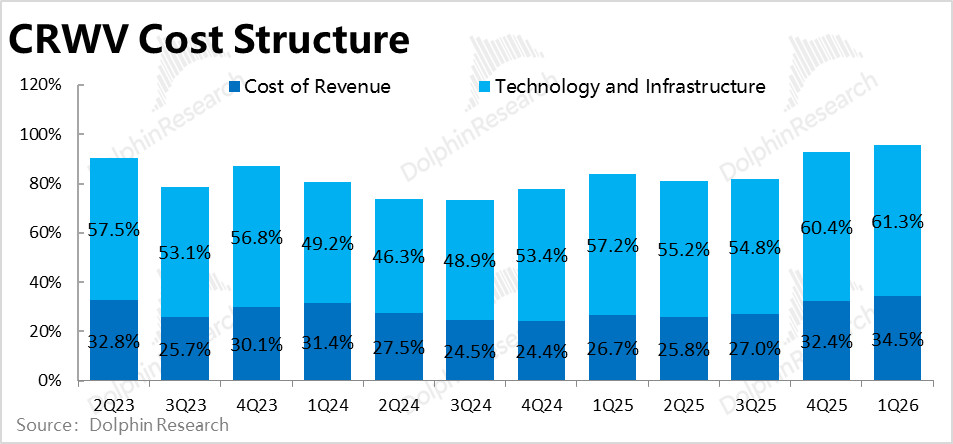

The primary drag remained gross margin, with the "true" gross margin (excluding revenue costs and Tech & Infra expenses) at 4.3%, down sharply from 7.2% last quarter and below market expectations of 6%.

As seen in the company's case, due to soaring upstream hardware prices like chips, cloud providers in the midst of large-scale computing capacity expansion face significant margin pressure, with newer cloud providers like CoreWeave experiencing even more pronounced challenges.

4. Faster Capex Growth: Corresponding to business growth, the company invested $6.8 billion in Capex this quarter, within the previous guidance range of $6-7 billion, though down from $8.2 billion last quarter.

While both Capex and newly launched computing capacity declined from the previous quarter, the trend was consistent. However, newly added computing capacity fell by 42% quarter-over-quarter, while Capex decreased by less than 20%. This indicates that the Capex required per additional MW of computing capacity is rising, possibly due to upstream hardware price increases or timing mismatches (Capex invested this quarter corresponds to computing capacity that will come online in subsequent quarters).

This also aligns with the larger-than-expected decline in gross margin this quarter.

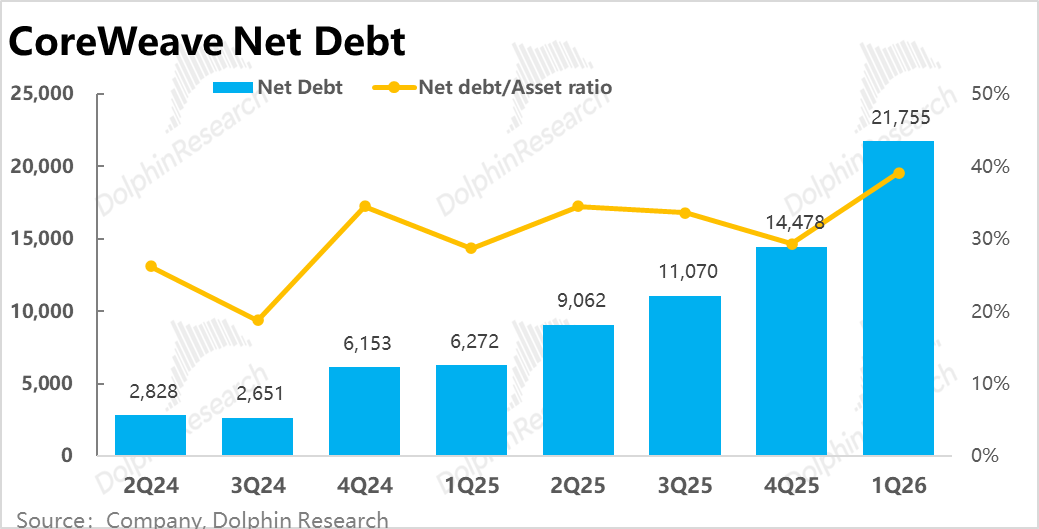

5. Continued Debt Pressure: With the rise in Capex and corresponding massive Capex demands, net debt reached nearly $21.8 billion, a quarter-over-quarter increase of nearly $7.3 billion, with the debt ratio (as a percentage of total assets) rising to 39%.

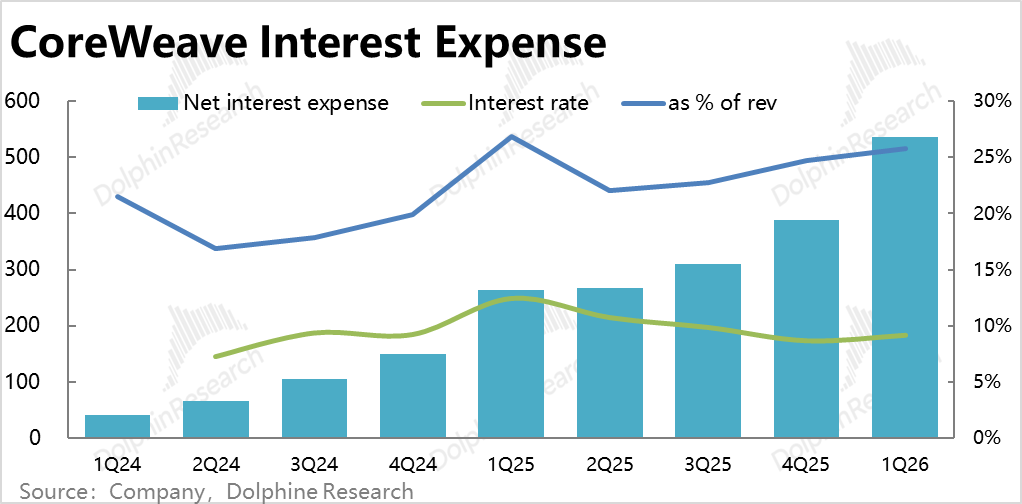

Interest expenses also increased to nearly $540 million, compared to $390 million last quarter, with the proportion of revenue rising from 25% to 26%. The current average profit margin remains around 9%-10%. The debt pressure from computing capacity investments and the resulting erosion of profits have become increasingly significant.

Dolphin Research View:

1. CoreWeave's performance this quarter, as described earlier, is a mixed bag. On the positive side, revenue growth exceeded expectations, and the company secured multiple large orders, further diversifying its customer base. On the negative side, gross margin declined more severely than expected due to business growth, and financing debt rose further to meet Capex funding needs.

However, these two situations are interconnected. In the short to medium term, the better the company's business scale grows, the greater the pressure on profits and financing. It is impossible to have the best of both worlds in the near term. Therefore, judging solely by quarterly performance, it cannot be considered poor—the company's stock price showed little change immediately after the earnings release.

The industry-relevant insights from the company's performance are: Due to upstream equipment price increases, the unit cost of building computing capacity is rising; simultaneously, due to strong demand for computing power, the revenue generated per unit of computing capacity is also increasing.

Therefore, for cloud providers, the key factors determining their core competitiveness are currently how much pricing power they have to raise prices or how much advantage they have in equipment costs. For CoreWeave, the cost increase has outpaced the price increase.

2. The bigger issue with this earnings report lies in the guidance. The primary problem is that the company expects next quarter's revenue to be approximately $2.45-2.6 billion, a limited increase from this quarter and below market expectations of $2.7-2.8 billion. Correspondingly, the company guides next quarter's Capex to be around $7-9 billion, also with a modest increase.

Based on the full-year 2026 revenue expectation of $12-13 billion, with less than $4.7 billion in revenue in the first half, single-quarter revenue in the second half needs to climb to nearly $4 billion, putting significant pressure. This raises market concerns about whether acceleration can occur in the second half to achieve the full-year target, given the lackluster computing capacity ramp-up in the first half.

Regarding profits, next quarter's adjusted operating profit is expected to be $30-90 million, implying a 2.4% profit margin, an improvement from this quarter's 1%. As the company increases utilization of existing computing capacity, profit margins will see a slight release, but the absolute value remains too low.

In terms of medium- to long-term guidance, the company's full-year 2026 expectations remain largely unchanged from last quarter, with a slight upward revision of annualized revenue by the end of 2026 from $17-19 billion to $18-19 billion. Capex budget was raised from $30-35 billion to $31-35 billion.

3. Recent Developments and Investment Logic

In summary, CoreWeave's investment logic has undoubtedly been improving recently, as reflected in the stock price rebounding 100% from the bottom after falling nearly 65% from its peak.

The core logic behind the previous stock price correction was market skepticism about the ROI of cloud providers' massive Capex—whether the substantial investments and computing capacity expansion would have sufficient demand to support them, and whether the profit margins of these AI businesses would be high enough to cover the high costs. New cloud providers like CoreWeave and Oracle faced even higher risks due to their smaller scale, weaker technical capabilities, and limited funding compared to the three major Hyperscalers.

The recent improvement in the company's logic is evident from both an industry perspective and the company's own progress. From an industry standpoint, as AI evolves from Chatbots to Agents, the entire internet (full network) computing power consumption has surged, reducing market doubts about whether there will be sufficient demand to support the newly built computing capacity.

From CoreWeave's perspective, it has made good progress in securing new large leasing orders and obtaining new funding to support Capex investments. Specifically:

a. Securing Multiple Large Orders: Since April, CoreWeave has announced several large orders, including an additional $21 billion order from Meta over 6-7 years (on top of an existing ~$14 billion contract), a ~$6 billion order from Jane Street, and a ~several billion order from Anthropic.

The significance of these developments, beyond directly boosting the company's revenue scale, is that Meta has become one of CoreWeave's largest customers, with some of the newly signed computing capacity orders to be used for Meta's AI inference.

Additionally, it signifies further diversification of the company's customer base, reducing its reliance on the OpenAI + Microsoft ecosystem (accounting for less than 40% of the company's total RPO), and establishing cooperation with all four major AI model providers.

b. Securing ~$15 Billion in Funding: Meanwhile, the company recently announced plans to raise ~$3.5 billion through convertible bond issuance, ~$2.8 billion through Senior Note issuance, and locked in a new ~$8.5 billion loan agreement. By securing a total of ~$15 billion in funding, the company's Capex funding is secured for at least the next year.

An important signal is that the interest rate on the newly locked DDLT loan is SOFR+225bps for the floating portion and 5.9% for the fixed portion, a significant decrease from the company's current average interest rate of ~10%.

Given that interest expenses currently account for nearly 30% of total revenue, the decline in debt interest rates will significantly help the company improve profit margins.

4. Overall, the company is indeed in an improvement cycle from a macro perspective, and the stock price has already reflected this. However, after significant stock price gains, issues like the computing capacity ramp-up falling short of expectations, leading to lower revenue guidance, have introduced short-term volatility in the company's logic and stock price.

Nevertheless, CoreWeave has always been a high-elasticity, high-risk speculative play, so significant fluctuations are expected. A more detailed value analysis has been published in the Changqiao App under the 「Dynamic-Depth」 section in an article with the same title.

In summary, the company has enormous long-term potential (given the massive demand for computing power, the company's revenue scale could reach tens of billions or even exceed $100 billion), but based on deliverable performance, it remains a speculative target without high certainty or a clear valuation floor.

Below is a detailed analysis:

I. Record Revenue and Order Growth

1. This quarter, CoreWeave achieved nearly $2.08 billion in revenue, a 112% year-over-year increase, surpassing market expectations of $1.97 billion and the company's previous guidance range of $1.9-2.0 billion. The net year-over-year revenue increase shows accelerating growth.

The underlying metric for revenue growth, online computing capacity (Active Power), reached 1000MW this quarter, a 150MW increase from last quarter, though the growth rate slowed compared to Q4 last year. However, this was expected considering seasonal impacts and lower Capex investment this quarter.

The implicit information is that revenue per MW of computing capacity has increased (from ~$8.7 million/MW to ~$9 million/MW), likely due to price increases from strong demand and improved utilization of newly built computing capacity.

The forward-looking metric, remaining performance obligation (RPO), reached $99.4 billion, a net increase of ~$33 billion from last quarter, marking another record high for single-quarter new orders. This largely aligns with previously reported orders, including $21 billion from Meta, $6 billion from Jane Street, and ~several billion from Anthropic.

Structurally, the RPO balance within 24 months actually declined, with all new additions exceeding 24 months, implying that most newly signed contracts will not begin implementation until after 2027.

II. The Issue of Larger Business Scale Leading to Lower Profit Margins Persists

While revenue growth has been impressive, the company's profit pressure has become more evident. The "true" gross margin (excluding disclosed revenue costs and Tech & Infra expenses) was 4.3% this quarter, down sharply from 7.2% last quarter and below market expectations of 6%.

A closer look reveals that direct data center operating costs (such as rent and energy expenses) rose more significantly this quarter, while the proportion of Tech & Infra expenses also increased but to a lesser extent.

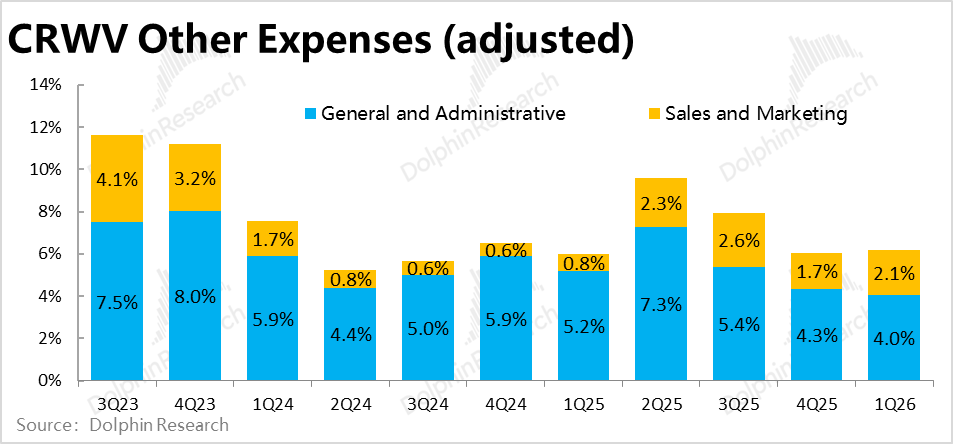

Given the company's business model of serving only a few AI giants, marketing and administrative expenses remain low, with the combined expense ratio largely unchanged from last quarter. Therefore, the decline in operating profit margin this quarter was primarily driven by the gross margin decline.

Specifically, the adjusted operating loss was $144 million, compared to an $89 million loss last quarter, with losses widening and worse than expected. The state of the company's business—the larger the scale, the higher the revenue, and the greater the losses—continues to reflect the significant margin pressure from soaring upstream hardware prices like chips and the AI business ramp-up phase.

III. Increasing Pressure on the Balance Sheet

In line with the growth of the company's business, the company invested 6.8 billion yuan in Capex this quarter, which is within the previously guided range of 6-7 billion yuan and a decrease from the 8.2 billion yuan invested in the previous quarter, consistent with the lower computing power launched this quarter compared to the previous quarter. However, Capex investment still amounted to nearly 330% of the quarterly revenue.

In response to the massive Capex demand, net debt reached nearly 21.8 billion yuan this quarter, with a quarter-on-quarter increase of nearly 7.3 billion yuan, and the debt ratio (as a percentage of total assets) rose to 39%. Consequently, interest expenses also increased to nearly 540 million yuan compared to 390 million yuan in the previous quarter, with the proportion of income rising from 25% to 26%.

It is evident that the pressure on the company's balance sheet and the erosion of profit margins by debt are becoming increasingly apparent and severe.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reprinting is only allowed with authorization.

// Disclaimer and General Disclosure Notice

This report is intended solely for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not take into account the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any person making investment decisions using or referring to the content or information mentioned in this report does so at their own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data contained in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure, but does not guarantee, the reliability, accuracy, and completeness of the relevant information and data.

The information mentioned or the views expressed in this report shall not be considered or construed as an offer to sell or a solicitation to buy securities in any jurisdiction, nor shall they constitute advice, inquiries, or recommendations regarding relevant securities or related financial instruments. The information, tools, and materials contained in this report are not intended for or intended to be distributed to jurisdictions where the distribution, publication, provision, or use of such information, tools, and materials conflicts with applicable laws or regulations, or to citizens or residents of jurisdictions where Dolphin Research and/or its subsidiaries or affiliated companies are required to comply with any registration or licensing requirements in such jurisdictions.

This report merely reflects the personal views, insights, and analytical methods of the relevant creators and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual shall (i) make, copy, reproduce, duplicate, forward, or create any form of copies or reproductions in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!