Foreign Home Appliance Brands' Mass Exit: Chinese Brands Still Face Uphill Battle

05/09 2026

05/09 2026

386

386

The retreat of foreign brands does not equate to a total victory for Chinese home appliances. Amidst these industry shifts, foreign brands are recalibrating their strategies in China, while Chinese home appliances are also navigating a fierce "survival-of-the-fittest" phase.

Cover image source: Unsplash

Another global home appliance behemoth has decided to leave the Chinese market.

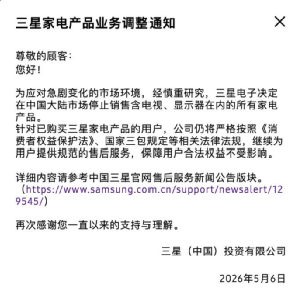

Recently, Samsung Electronics announced: "In response to rapidly evolving market conditions and after careful consideration, Samsung Electronics has decided to cease sales of all home appliance products, including televisions and monitors, in the Chinese mainland market."

This means that, with the exception of Samsung mobile phones, Samsung's home appliance division will completely withdraw from the Chinese market. However, Samsung is not alone. In recent years, foreign home appliance brands have quietly initiated their departure.

In April of this year, U.S. water heater giant A.O. Smith initiated a process to evaluate the sale of its Chinese business. By the end of last year, Sony had transferred its home entertainment business, including televisions, to TCL Holdings. Panasonic handed over its TV business in Europe and North America to Skyworth...

Suddenly, the market was filled with exclamations of "foreign home appliances are retreating; domestic brands must rise." While the ascent of Chinese home appliances is undeniable, interpreting the withdrawal of foreign brands as a "rout" may be more concerning than the departure itself.

Foreign home appliance brands are merely exiting the Chinese market, but competition in the home appliance sector has not ended. Instead, it has intensified globally, evolving from a single-market rivalry to a comprehensive contest involving global supply chains, brand influence, and overall corporate strength.

The long journey for Chinese home appliances has just begun.

1

Foreign Home Appliance Brands' Mass Exit

The exodus of foreign home appliance brands began to show signs over a decade ago.

Around 2010, Philips transferred its monitor and TV business in the Chinese mainland to TPV Technology. In 2016, Foxconn completed its acquisition of Sharp, marking the first time a major Japanese home appliance company came under foreign control.

Subsequently, foreign home appliance giants began divesting or scaling back their operations in China: Haier acquired Sanyo's white goods business, Toshiba TV was acquired by Hisense, Whirlpool China was acquired by Galanz, and LG granted Saif Group full-channel new retail operational rights for its home appliance category...

Now, Samsung's complete exit from the Chinese market was also foreshadowed. In March of this year, Samsung's absence from AWE 2026 sparked rumors that the company was planning to shift its home appliance business from a self-operated model to an agency-based one.

Amidst widespread sentiments of "the end of an era," the departure of foreign brands has long been a predestined footnote to the transformation of China's home appliance market.

In the 1990s, foreign brands were synonymous with "premium brands," representing not just taste in the living room but also an unshakable confidence in quality. Consumers nearly unconditionally trusted foreign brands' technology and products.

However, with the rise of Chinese home appliances, the era of "foreign brands dominating" has become a thing of the past.

On one hand, Chinese home appliances began to catch up rapidly. Brands like Haier, Midea, Hisense, and TCL gradually broke foreign brands' monopolies by addressing technological shortcomings and leveraging cost-effectiveness.

By 2025, Haier, Midea, and Gree collectively accounted for approximately 70% of China's major home appliance market. According to Euromonitor International, Chinese home appliance brands' overseas market share surged from 2.9% in 2015 to 10.9%, proving that Chinese home appliances are no longer just "invisible" players relying on OEM models to go global.

On the other hand, foreign brands began to slow down.

According to AVC data, as of April this year, Samsung's offline market share in China for color TVs, refrigerators, and washing machines stood at 3.54%, 0.41%, and 0.37%, respectively, ranking 5th, 14th, and 15th, effectively fading from the mainstream.

Sony TV, once dominant in the color TV market with its Trinitron technology, has now been relegated to "Others." By 2025, Sony's TV market share in China had fallen below 2%.

The successive retreats of Japanese and Korean home appliance brands from the Chinese market reflect the shifting tides between Chinese and foreign brands. However, beyond stronger competition, foreign brands' inability to adapt to the Chinese market has also widened the gap.

A senior color TV industry insider noted that Samsung's centralized management model struggles to adapt to China's rapidly changing consumer market. In contrast, Chinese brands better understand local consumer needs and embrace market and channel changes more swiftly.

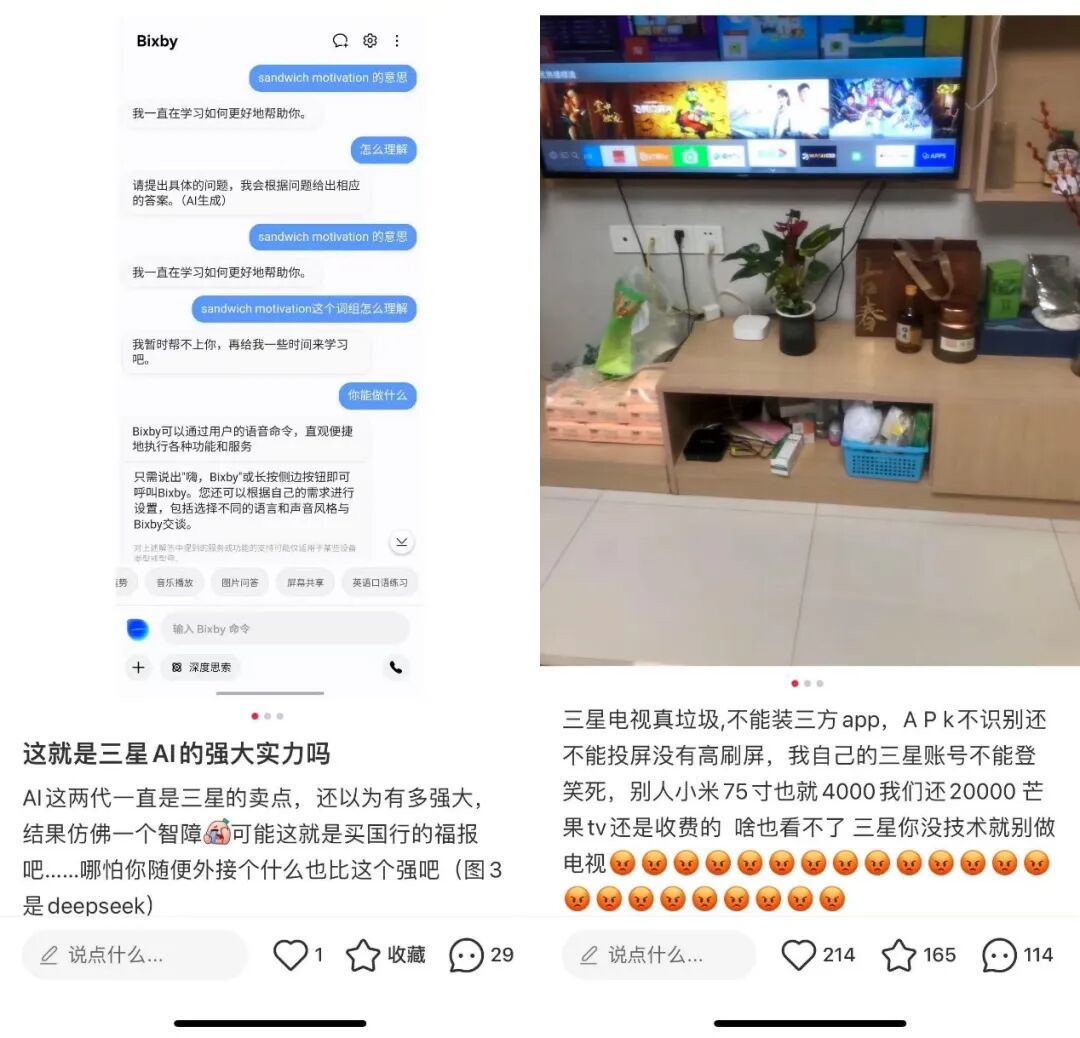

For example, in recent years, many home appliance brands have ventured into whole-home smart solutions. Brands like Midea and Xiaomi have shifted their competitive focus from hardware specifications to software and smart ecosystem development, with AI integration already on the agenda.

However, Samsung home appliances still rely on their proprietary ecosystem. For instance, many consumers complain that Samsung TVs cannot download third-party apps and often experience lag or disconnections during mobile screen mirroring. Additionally, while Samsung has clearly bet on AI, its component advantages have not translated into competitive terminal products.

Besides lagging software capabilities, their original hardware advantages are also disappearing. In the past, foreign TV brands like Sony and Samsung held core display panel technologies and production capacity, giving them pricing power over premium products.

Today, panel giants like BOE and TCL CSOT have deeply invested in high-end OLED and Mini LED technologies. TCL launched mass-market Mini LED products as early as 2021, while Samsung only began large-scale promotion in 2022.

With declining product competitiveness and inability to compete on price, exiting the Chinese market seems the best choice for foreign home appliance brands.

2

The "Business Logic" Behind It

For foreign home appliance brands, exiting the Chinese market is not necessarily a bad choice but rather one that respects market dynamics.

In their eyes, the logic of winning has changed—they aim not just for profitable business but for more lucrative, effortless, and high-margin opportunities.

Looking at the performance of Japanese and Korean home appliance giants like Sony and Samsung, while their Chinese market presence has dwindled, their overall situations have not deteriorated—in fact, they are thriving.

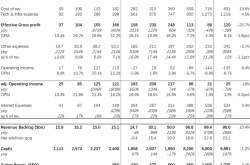

Samsung established its semiconductor division as early as the 1980s, renaming it Samsung Electronics. In Q1 2026, the company achieved record-high sales (approximately RMB 606.4 billion) and operating profit (approximately RMB 261 billion).

According to securities firm estimates, Samsung's Device Solutions (DS) division, responsible for chip business, reported operating profit far exceeding KRW 50 trillion (approximately RMB 232.5 billion). Driven by the global memory chip shortage, the storage business contributed nearly 90% of Samsung's operating profit, while the home appliance business remained unprofitable.

Similarly, Sony has long focused on entertainment. In FY2024, Sony's film, music, and gaming businesses accounted for over 60% of group revenue, up from around 40% in 2016.

According to Q3 FY2025 results, the company's sales reached JPY 3,713.7 billion, up 1% YoY, while operating profit surged 22% YoY to JPY 515 billion, driven by high-margin businesses like image sensors and gaming services.

Notably, Sony's image sensors not only dominate the DSLR camera market but also supply most global high-end smartphones, silently contributing revenue.

However, beyond these businesses, foreign home appliance brands still face fierce competition in China's home appliance market. In recent years, weak consumer demand has trapped the domestic home appliance market in an inventory competition trap, with price wars becoming the norm.

According to AVC data, in Q1 2025, air conditioner prices dropped over 10%, with RMB 1,000 units becoming common. In the refrigerator market, sub-RMB 2,200 low-end models saw the most significant growth.

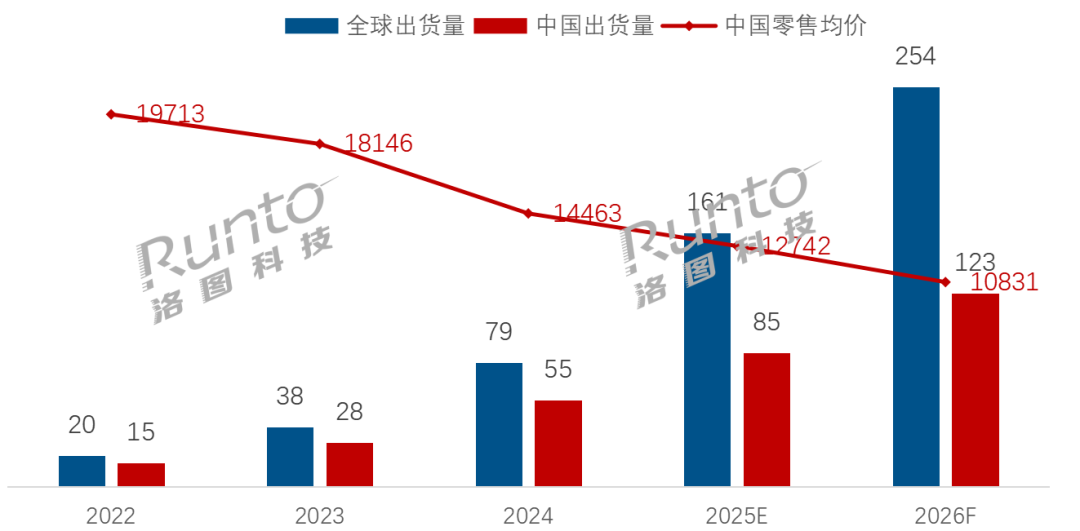

TV prices have also "collapsed." According to LoCTech data, the average retail price of 100-inch TVs fell from RMB 19,713 in 2022 to RMB 12,941 in H1 2025 and is expected to approach RMB 10,000 in 2026.

For foreign home appliance giants, the home appliance business is no longer a "golden goose," with gross margins hovering around single digits and even incurring losses.

In comparison, Samsung's memory chip business is expected to achieve gross margins of 60-70%. In FY2024, Sony's music business reported an operating profit margin of 19.4%. The choice is clear.

Capital markets are also voting with their feet. On the same day Samsung announced its exit from the Chinese market, Samsung Electronics' market cap surpassed USD 1 trillion, making it the second Asian company (after TSMC) to join the trillion-dollar club.

This gives foreign home appliance giants the confidence to leave, as they have already concentrated resources on more promising sectors. Shedding the home appliance business allows them to travel lighter and focus on core competitive advantages.

3

Far from a Total Victory

From this perspective, the withdrawal of foreign home appliance brands has two sides.

First, we must acknowledge the achievements of Chinese home appliances. Today, Chinese home appliances have gone global, leading in production scale, supply chain integrity, and cost control.

China manufactures approximately 80% of global air conditioners, 70% of refrigerators, and over 50% of washing machines, boasting a complete independent supply chain from compressors and motors to chips and panels. Core components like compressors and motors also dominate 90% of the global market.

Global home appliances rely on "Made in China," allowing Chinese companies to move faster by standing on the shoulders of giants.

However, not all home appliance brands have seized the era's opportunities: Former color TV leader Konka faces delisting risks due to negative net assets; air conditioner maker Chigo has initiated bankruptcy proceedings; once-dominant TV giant Changhong has incurred hundreds of billions in losses...

Thus, the withdrawal of foreign brands is far from a total victory for Chinese home appliances. Amidst these industry shifts, foreign brands are recalibrating their strategies in China, while Chinese home appliances are also navigating a fierce "survival-of-the-fittest" phase.

Even industry-leading Chinese brands are far from relaxing.

Today, the global home appliance market faces dual pressures of weak consumption and rising costs. In this context, competition has shifted from "how to grow" to "how to survive."

This is the "hidden pain" of Chinese home appliances—while they have secured a global foothold and broken free from reliance on OEM models, their brand appeal in the premium market remains weak.

To address this, Chinese home appliances must escape price-based competition and stockpile more ammunition to transcend the "manufacturing logic" of the industry and explore new, high-potential narratives.

Midea's Vice President Wang Jianguo revealed that the company will invest at least RMB 50 billion over the next three years in cutting-edge fields like AI large models, new energy, robotics, and embodied AI.

Haier, Gree, and Skyworth are actively entering the new energy sector. Skyworth plans to spin off its subsidiary Skyworth Solar for listing on the HKEX, while Haier's Haier New Energy has initiated IPO preparations.

TCL continues to double down on semiconductors, planning to acquire a 45% stake in Guangzhou Huaxing Semiconductor. Gree Chairwoman Dong Mingzhu also stated that Gree has achieved independent R&D, design, and manufacturing across the entire chip supply chain.

Over the past decade, Chinese home appliances have transitioned from technological followers to autonomous controllers and then to technological leaders, ushering in a "Chinese era" for global home appliance manufacturing.

However, breaking the decades-old brand barriers erected by home appliance giants is no easy feat.

The AI era presents new opportunities. China boasts the world's strongest home appliance supply chain and most advanced AI hardware and software application ecosystem, enabling home appliances to move beyond standalone hardware competition. Through self-development or partnerships, they can transition toward a comprehensive "human-vehicle-home" ecosystem—a moat that other home appliance giants struggle to replicate.

To know others is wisdom; to know oneself is enlightenment. Only by viewing the withdrawal of foreign home appliance brands from China objectively can Chinese home appliances better understand their position and direction.

The strength of Chinese manufacturing lies not in whom it defeats but in whom it ultimately becomes.

-

![]()

Sales Review of Top Five Independent Automakers in April 2026: BYD Leads, Chery Closely Pursues

-

![]()

2026 Beijing Auto Show: A Spectacular Showcase of 9-Series Flagship Vehicles

-

![]()

Triple Gamble: Is Insta360 Eyeing the Next 10 Billion Yuan Market?

-

![]()

Foreign Home Appliance Brands' Mass Exit: Chinese Brands Still Face Uphill Battle

-

![]()

Coreweave: Computing Power Sales Soar, But Profits Falter—Is Nvidia's 'Foot Soldier' Fighting for Survival?

-

![]()

Coreweave: Strong Computing Power Sales, But Profitability Challenges Persist—Is Nvidia's 'Foot Soldier' Just Stuck in a Tough Spot?

-

![]()

The Rationale Behind the Financing Rush Among Major Model Firms: Dark Side of the Moon and StepFun Spearheading the Charge

-

![]()

DeepWay Makes Another Attempt at HKEX Listing: Annual Revenue Hits 4 Billion, Operating Cash Flow Turns Positive, Has the 'Tesla of Heavy Trucks' Overcome Its Toughest Challenge?