Triple Gamble: Is Insta360 Eyeing the Next 10 Billion Yuan Market?

05/09 2026

05/09 2026

331

331

Revenue Surges, Profits Halve: Founder Urges Investors to Stay Calm

On April 28, Insta360 Innovation (hereinafter referred to as Insta360) unveiled its full-year 2025 and Q1 2026 financial results, showcasing a highly robust performance.

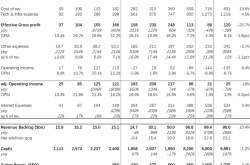

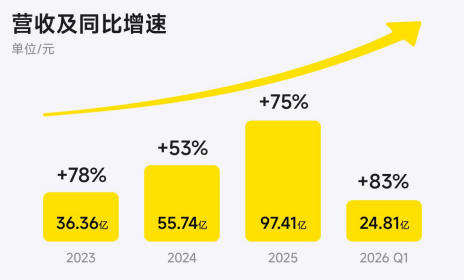

The financial reports indicate that Insta360 is in a phase of rapid expansion. In 2025, the company's revenue soared to 9.741 billion yuan, marking a 74.76% year-on-year increase. In Q1 2026, revenue further climbed to 2.481 billion yuan, up by 83.11%. Over the past three years, Insta360's revenue has nearly tripled, reflecting a compound annual growth rate exceeding 63%. This growth rate is on par with the hardware achievements seen in today's thriving AI sector.

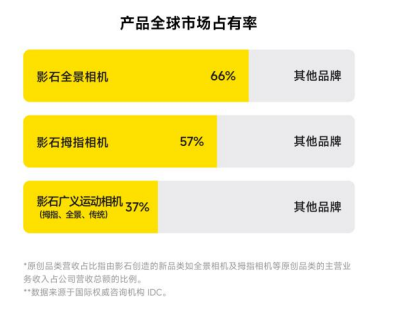

Despite the revenue surge, Insta360 has not relented in its market dominance. According to IDC data, Insta360 commands a 66% share of the global 360-degree camera market, 57% of the portable thumb camera segment, and 37% of the broader action camera category. Regardless of how the market is defined, Insta360 stands as a dominant "oligopoly player" in its respective niches.

Focusing on profitability, Insta360 has prioritized revenue growth over immediate profits. Financial data reveals that Insta360's net profit attributable to shareholders was 929 million yuan in 2025, down 6.62% year-on-year. In Q1 2026, net profit further declined to 85 million yuan, a 52% year-on-year drop.

Addressing the profit contraction, Insta360 founder and chairman Liu Jingkang stated in a shareholder letter: "High-intensity strategic investments to support long-term development have led to a short-term decline in profit metrics." In simpler terms, Insta360 has set its sights on larger goals and is intentionally prioritizing "strategic non-profitability." Liu repeatedly mentioned the concept of a "photography robot" and outlined three new product categories—gimbal cameras, microphones, and drones—expected to launch within the next year, transitioning from investment to revenue generation.

For investors, Insta360's expansion as a publicly traded company cannot rely on mere speculation. What exactly is Insta360 planning to expand into, and how robust is the "safety cushion" in its financial statements?

Regardless, Insta360 is betting big on its vision for the future.

Cash Flow, Inventory, R&D Investment: Insta360's Triple Gamble

Before delving into the pressures Insta360 faces, let's quickly review the company's fundamentals.

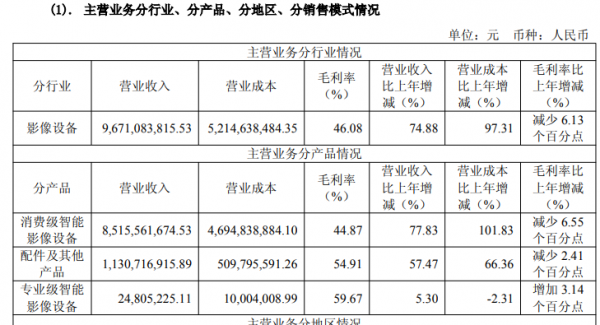

Insta360's business is divided into consumer-grade smart imaging devices, accessories and other products, and professional-grade smart imaging equipment. Consumer-grade devices primarily include portable cameras like 360-degree and action cameras, while professional-grade equipment refers to VR-specific 360-degree cameras and AI video conferencing all-in-one machines.

The consumer-grade business is the company's core revenue driver, accounting for 88% of total revenue (as per the annual report). In terms of profitability, the company's overall gross margin stands at 46.08%, an exceptionally strong level in the consumer electronics sector, even surpassing Apple's smartphone margins (~40%).

At the product level, Insta360's primary customers are overseas, with international revenue more than double domestic revenue. In terms of sales channels, Insta360 maintains a balanced online-to-offline ratio of roughly 4:5. This equal split indicates strong consumer awareness of the brand and products, reducing the need for heavy offline investments to reach customers.

Based on this information, Insta360 can be considered a highly competitive consumer-grade imaging hardware manufacturer. The company's sole risk lies in its relatively singular revenue stream.

"Today, over 60% of Insta360's revenue comes from original niche categories we pioneered 7–8 years ago," Liu Jingkang emphasized in his shareholder letter. Clearly, Insta360 is aware of this risk.

To explore new frontiers, Liu explained Insta360's next objectives and investments: "Beyond our existing business (360-degree cameras, thumb cameras, action cameras, etc.), we are strategically investing in R&D for two drone models (including the Yingling panoramic drone), gimbal cameras, wireless lavalier microphones, and three other new categories. We also developed three custom chips. Our strategic investments in these areas totaled 762 million yuan in 2025 and 262 million yuan in Q1 2026—approximately 80% and 300% of our net profit attributable to shareholders for the same periods, respectively." This explains the significant profit decline in Q1 2026.

But are the consequences of Insta360's investments merely short-term profit pressures? Perhaps not entirely. Insta360 has made three highly "aggressive bets" in its financial statements.

First, in terms of cash flow, Insta360 is effectively trading balance sheet strength for accelerated expansion.

On paper, Insta360 is not short of cash. By the end of 2025, the company held 4.9 billion yuan in cash (monetary funds + trading financial assets - short-term liabilities), bolstered by last year's IPO proceeds. Its full-year net cash flow from operating activities was 1.386 billion yuan, up 18% year-on-year—a strong performance. However, breaking it down, while Q1 2026 revenue grew 83%, net profit attributable to shareholders plummeted to 85 million yuan due to 262 million yuan in strategic new product investments.

In essence, the company invested three times its profit into R&D. In other words, Insta360's core business revenue generation is now slower than its strategic spending.

How will core business revenue sustain growth? Insta360 is betting on sustained high-speed revenue expansion.

Financial statements show that Insta360 is leveraging upstream and downstream partners as a "reservoir" for its revenue data. By the end of 2025, inventory stood at 2.9 billion yuan, up 192% year-on-year; contract liabilities (prepayments) reached 342 million yuan, up 289%; and accounts payable totaled 3.092 billion yuan, up 174%.

The simultaneous growth of these three figures indicates that Insta360 is placing larger orders with suppliers (converted into inventory, raw materials, and contract manufacturing) while extending payment terms, and collecting more prepayments from downstream customers. The difference can be used to fund R&D and channel expansion (offline stores grew from 36 to nearly 300).

While such practices are common in the consumer electronics sector and reflect increased bargaining power across the supply chain, they require the company's long-term vision to materialize as planned. New and existing product lines must convert into actual revenue; otherwise, the loop cannot close.

How can new and existing product lines ensure revenue conversion? Insta360 has "maxed out" R&D.

In Q1 2026, R&D spending reached 465 million yuan, while net profit was just 85 million yuan. This means the company invests over 5 yuan in R&D for every 1 yuan of profit.

Such "output-agnostic" R&D investment is more common in early-stage internet and AI companies, where software has no fixed material costs, and R&D expenses can be significantly "diluted" once revenue scales. However, as a consumer hardware company, Insta360's products inherently have fixed material costs.

Overall, Insta360's financial statements reflect confidence in sustained high-speed revenue growth, both from existing and new innovative businesses.

Fortunately, according to IDC data, Insta360's core products are in a rapid growth phase. In 2025, shipments of Insta360's 360-degree cameras surged nearly 60% year-on-year, capturing over 65% of the market. In the "thumb camera" segment (detachable action cameras per IDC), it maintained a lead with over 50% market share. The upcoming higher-spec Go Ultra model, expected later this year, is poised to deliver an even better shooting experience than the Go 3S.

Regarding new products, Liu Jingkang provided an implicit timeline in his shareholder letter: "Gimbal cameras, wireless lavalier microphones, and drones are expected to transition from investment to revenue generation within 2026." In other words, Insta360 aims to see revenue contributions from these new categories within 12 months.

Perhaps to reassure shareholders, Insta360 announced an unexpected dividend plan in its annual report: 2.35 yuan per 10 shares. This is rare among Chinese tech growth companies, which typically opt for "zero dividends, full retention." While the absolute amount is modest, the message is clear—the company's foundations are solid, and investors can rest assured.

Nevertheless, Insta360 has just three quarters left to deliver on this promise.

Introducing the "Photography Robot" Concept: Insta360 Fully Embraces AI

Perhaps Liu Jingkang's aggressiveness is justified.

Looking back at Insta360's competition with GoPro, its victories were never driven by "cost-effective substitution" but by scenario innovation.

As Liu recalled in his shareholder letter: In 2017, when GoPro's sales began to decline, Insta360 addressed native pain points of action cameras—difficult framing, shaky footage, and selfie sticks in shots—through panoramic technology, pioneering a "shoot first, frame later" experience. In 2019, the thumb camera GO series solved wearability and bulkiness issues. In 2023, the Ace series expanded action cameras from "sports shooting" to Vlogging and street photography.

While both companies miniaturized professional cameras and integrated stabilization, waterproofing, and image algorithms into shooting devices, Insta360 derived over 60% of its revenue from original niche categories, capturing 66% of the global 360-degree camera market by addressing video creators' needs from shooting to content creation.

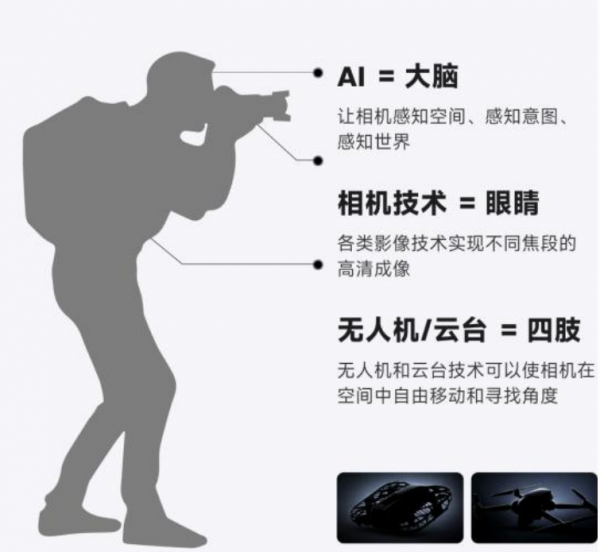

Historically, AI in shooting scenarios primarily optimized image quality, stabilization, and beautification. Now, Insta360 envisions AI handling shooting, framing, content generation, and automatic editing—acting as a "photography robot." "In drones, gimbal cameras, and lavalier microphones—seemingly mature categories—we see significant unmet customer needs and technological innovation opportunities globally," Liu said, highlighting Insta360's chosen direction.

Building on AI-driven photography transformation, Insta360 has extensively integrated AI capabilities into its product lineup. For example, the flagship Ace Pro 2 action camera features dual AI chips to enhance low-light performance. The AI-powered Flow series smartphone stabilizer enables dynamic tracking through AI subject recognition. The standout feature, however, is AI editing: "We began developing automatic editing technology six years ago, with client export rates now nearing 50% annually," Liu said.

For new product lines, the Insta360 Wave wireless lavalier microphone competes with AI voice recorders, featuring on-device AI acoustic algorithms for intelligent noise reduction, meeting summary generation, and AI Q&A. The Link series AI gimbal camera (a network camera with a gimbal) enables intelligent subject tracking, gesture control, and automatic top-down shooting. Such AI capabilities are primarily found in gimbals and gimbal cameras but lack direct office or conferencing counterparts in the market.

In the drone segment, Insta360 aims to deliver a "flying god's-eye view." Take the December 2025 launch of the Yingling Antigravity A1 drone: its significance lies not in the drone itself but in integrating 360-degree panoramic imaging, immersive flight perspectives, motion-sensing controls, and 8K panoramic video capture, all tied into Insta360's mature automatic editing workflow. While AI-edited and panoramic flight shooting products exist, Insta360's key advantage is the freedom to reconstruct 360° footage from any angle—a capability mostly absent in market alternatives.

In essence, Insta360's new products represent an "arrangement and combination" of existing AI capabilities in shooting devices, repurposing accumulated expertise in imaging algorithms, AI recognition, and automatic editing into new hardware forms. Compared to global leaders in AI large models or embodied AI, Insta360's AI capabilities may not stand out, but it is fully committed to embracing AI.

At the organizational level, Insta360 has fully integrated AI into workflows. According to its annual report, AI agents are now deployed across R&D, marketing, supply chain, and customer service. In Q1 2026, approximately 43% of the company's application code was generated by AI. For the full year of 2025, over 50% of online customer service was handled by AI. Perhaps AI can help offset some expansion costs. Additionally, in the booming field of "physical AI," Insta360 has begun providing panoramic data collection services for robotics companies to train embodied AI models, positioning panoramic cameras as the "visual infrastructure" for embodied AI.

Epilogue

Insta360's aggressive expansion is a necessary step for a "small but beautiful" company to ascend to "major league" status.

To some extent, Insta360's ambitions mirror those of AI-native device creators in the AI large model era, such as AI voice recorders, AI cameras, and AI toys. However, Insta360 is leveraging a triple gamble to replicate its success in pioneering 360-degree cameras into new smart hardware categories like drones, gimbals, and microphones.

Perhaps this expansion will propel Insta360's revenue from 9.7 billion yuan to the next 10 billion yuan milestone. Regardless, the success of this high-stakes gamble will be determined within 2026.

-

![]()

Sales Review of Top Five Independent Automakers in April 2026: BYD Leads, Chery Closely Pursues

-

![]()

2026 Beijing Auto Show: A Spectacular Showcase of 9-Series Flagship Vehicles

-

![]()

Triple Gamble: Is Insta360 Eyeing the Next 10 Billion Yuan Market?

-

![]()

Foreign Home Appliance Brands' Mass Exit: Chinese Brands Still Face Uphill Battle

-

![]()

Coreweave: Computing Power Sales Soar, But Profits Falter—Is Nvidia's 'Foot Soldier' Fighting for Survival?

-

![]()

Coreweave: Strong Computing Power Sales, But Profitability Challenges Persist—Is Nvidia's 'Foot Soldier' Just Stuck in a Tough Spot?

-

![]()

The Rationale Behind the Financing Rush Among Major Model Firms: Dark Side of the Moon and StepFun Spearheading the Charge

-

![]()

DeepWay Makes Another Attempt at HKEX Listing: Annual Revenue Hits 4 Billion, Operating Cash Flow Turns Positive, Has the 'Tesla of Heavy Trucks' Overcome Its Toughest Challenge?