Qualcomm: Can This 'AI Shot in the Arm' Offset the Smartphone 'Achilles' Heel'?

05/09 2026

05/09 2026

620

620

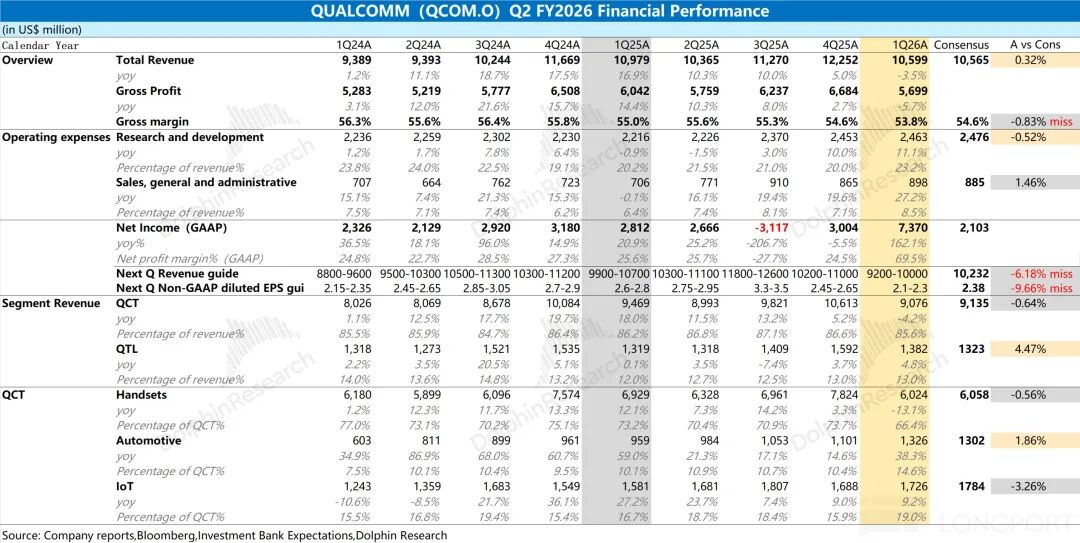

Qualcomm (QCOM.O) released its second-quarter fiscal year 2026 financial results (ending March 2026) after the market close on April 30, 2026, Beijing time. Key highlights are as follows:

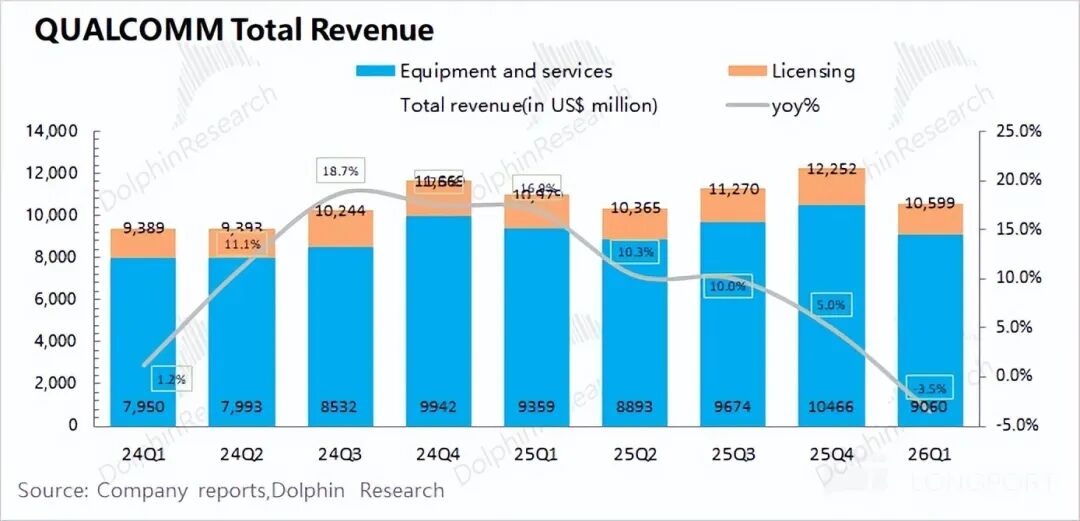

1. Core Data: Qualcomm's revenue for this quarter was $10.6 billion, down 3.5% year-over-year, in line with market expectations ($10.56 billion). The decline was primarily due to the downturn in the downstream smartphone market.

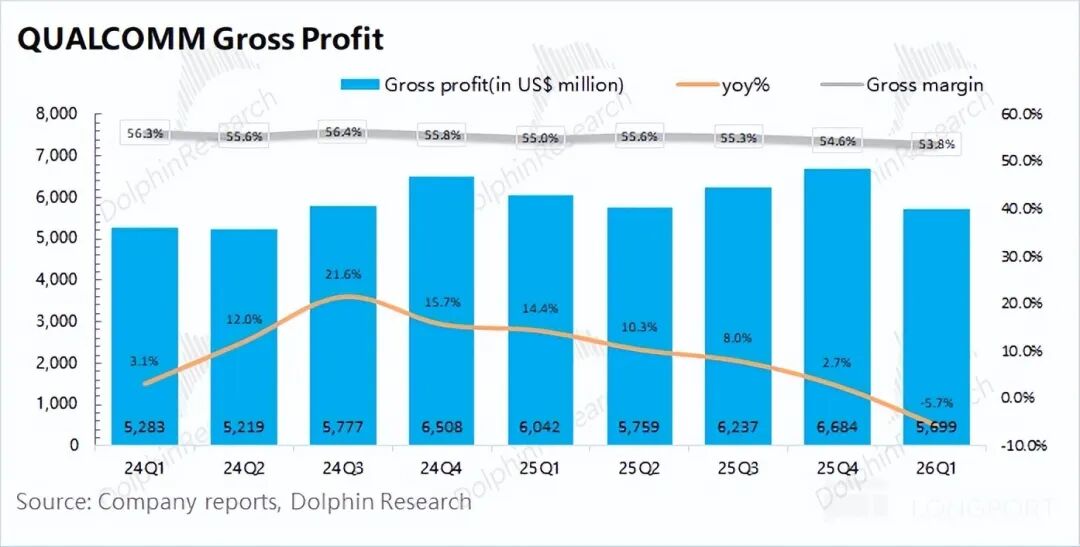

The company's gross margin for the quarter was 53.8%, down 1.2 percentage points year-over-year and below market expectations (54.6%). The memory shortage impacted the gross margin of the company's hardware business (QCT).

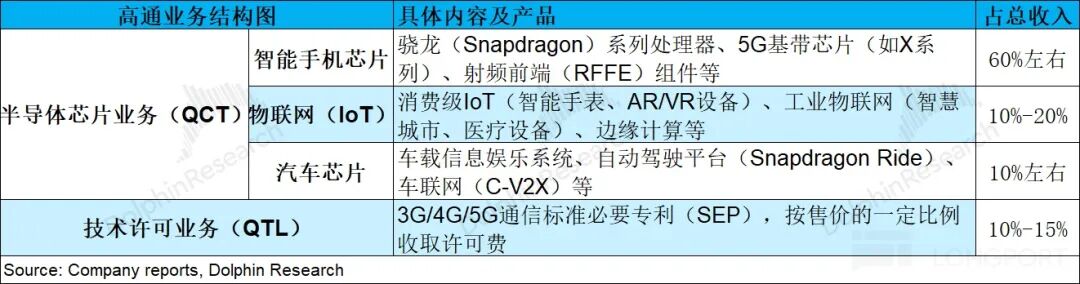

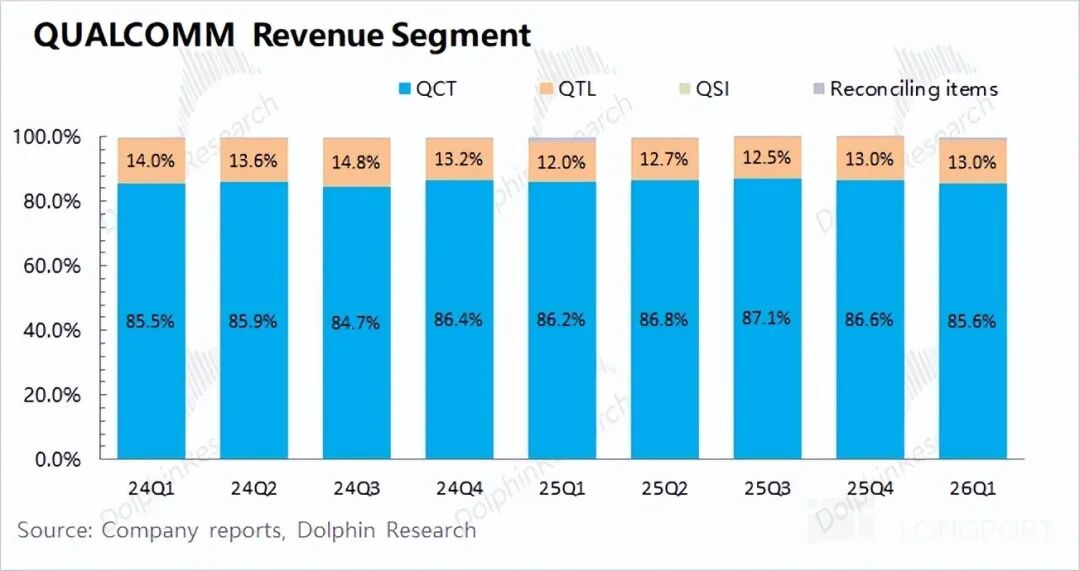

2. Business Performance: Qualcomm's (QCOM.US) business is mainly divided into semiconductor chip business (QCT) and technology licensing business (QTL), with semiconductor chips being the largest revenue source, accounting for nearly 90%.

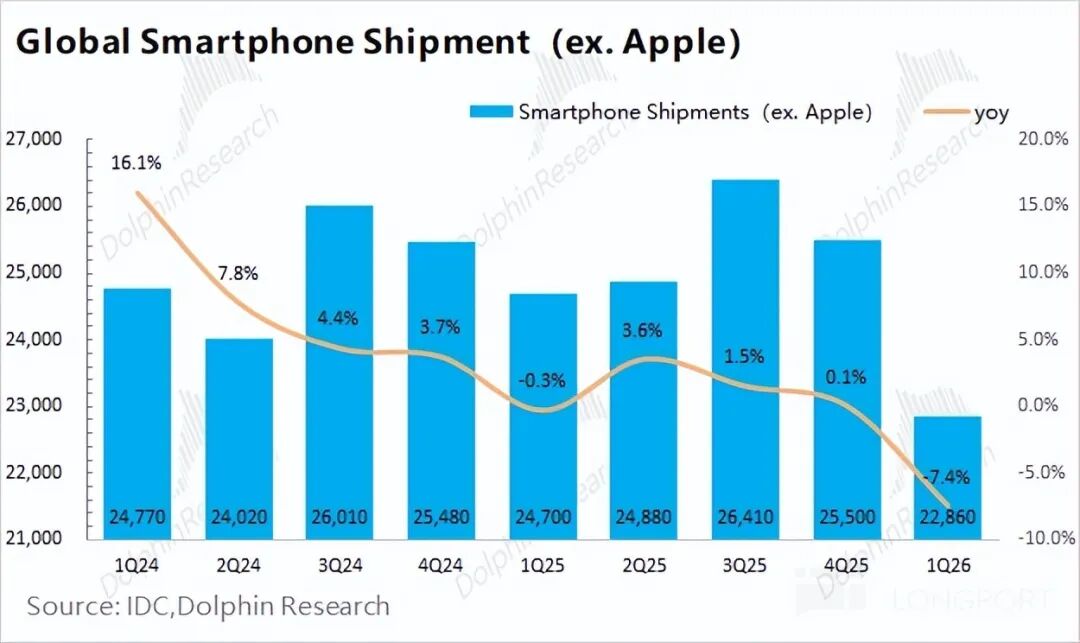

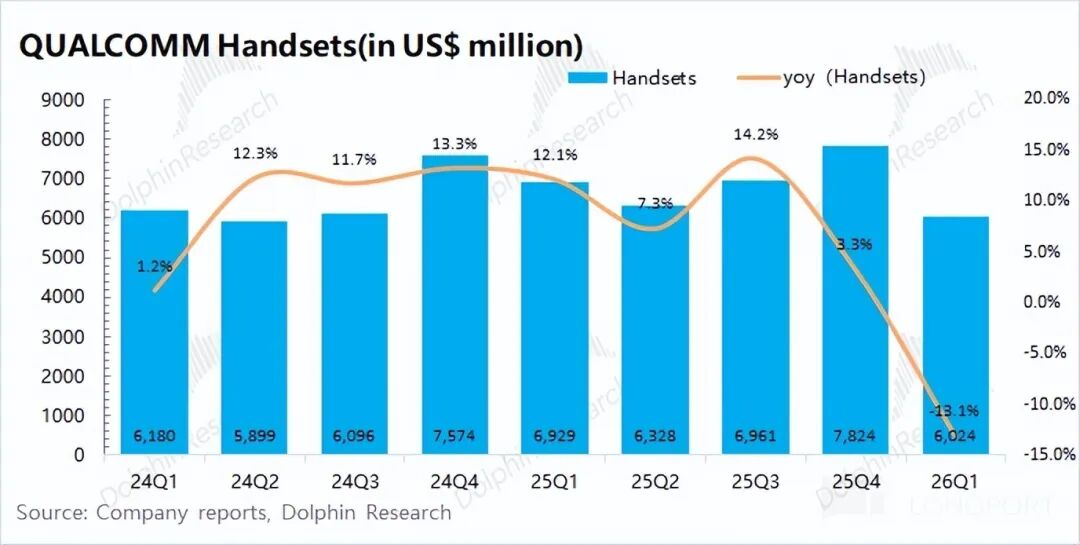

Within the semiconductor chip business: ① Smartphone revenue was $6 billion this quarter, down 13% year-over-year. The decline was influenced by two factors: industry-wide, smartphone shipments (excluding Apple) fell 7% this quarter; additionally, the company's earlier launch of flagship products shifted some demand forward.

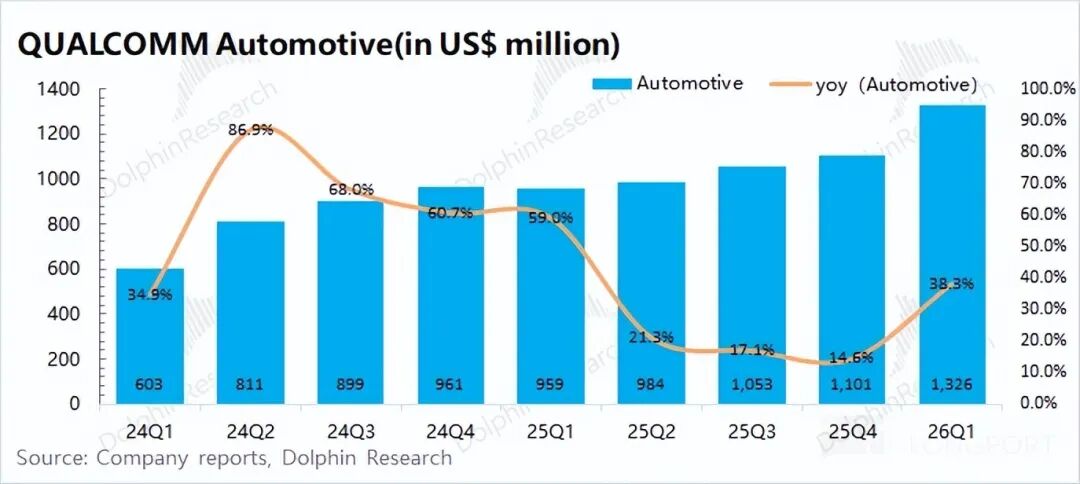

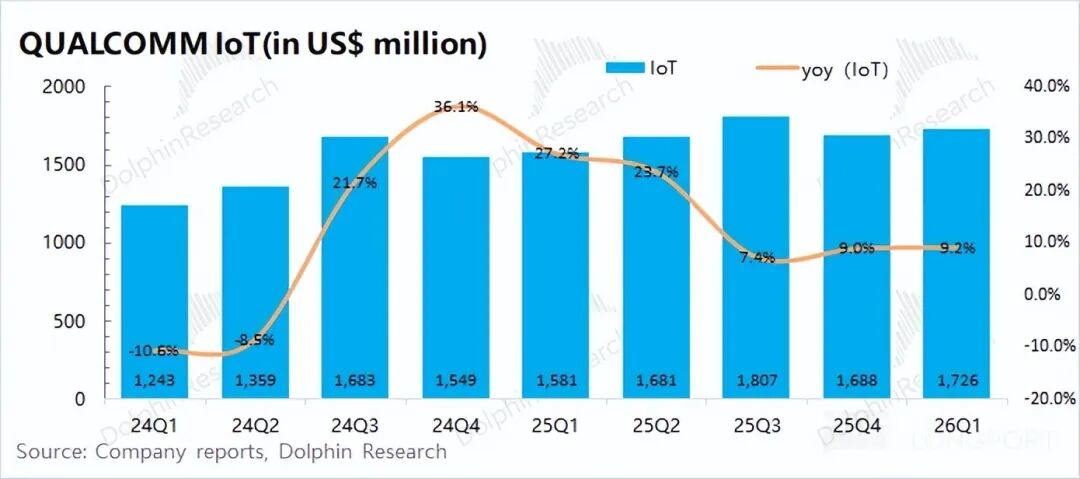

② Automotive revenue was $1.3 billion, up 38.3% year-over-year, driven by increased shipments of the Snapdragon fourth-generation digital cockpit. ③ IoT revenue was $1.7 billion, up 9% year-over-year, driven by demand for consumer and industrial products. However, IoT revenue growth slowed significantly due to tighter government subsidies and memory shortages.

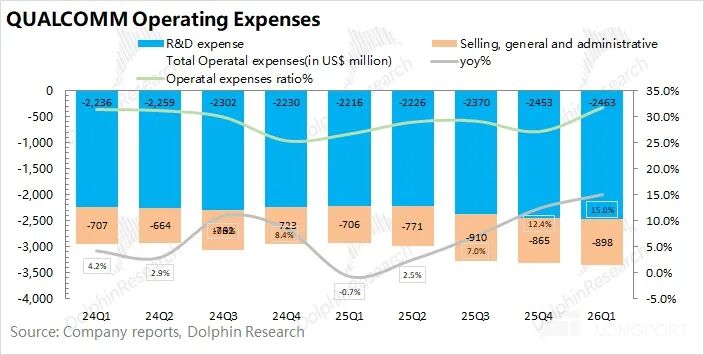

3. Operating Expenses: The company's core operating expenses increased to approximately $3.36 billion, with R&D expenses rising to $2.46 billion and sales expenses reaching $900 million for the quarter.

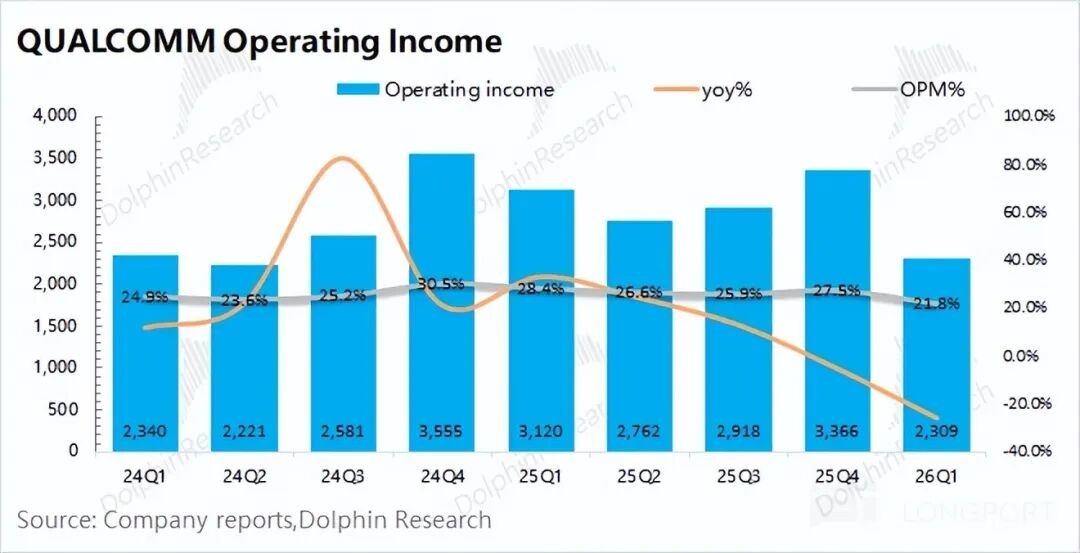

The company reported a net profit of $7.37 billion for the quarter, primarily due to the release of previously accrued deferred tax asset valuation allowances (approximately $5.7 billion). From an operational perspective, core operating profit was $2.3 billion, down 26% year-over-year.

4. Next Quarter Guidance: Qualcomm expects revenue of $9.2-10 billion for the third quarter of fiscal year 2026, below market expectations ($10.2 billion). Non-GAAP earnings per share are expected to be $2.1-2.3, also below market expectations ($2.38).

Dolphin Research's Overall View: Guidance 'Miss' Cannot Mask AI Ambitions; Valuation Logic Has Changed

Qualcomm's revenue for the quarter met market expectations, but the decline in gross margin was primarily due to the sluggish downstream smartphone market and memory shortages/price hikes, which dragged down the gross margin of its hardware business (QCT).

Beyond this quarter, the company's next-quarter guidance remains 'weak.' Revenue is expected to be $9.2-10 billion, below market expectations ($10.2 billion), with Non-GAAP EPS of $2.1-2.3, also below expectations ($2.38). This suggests continued declines in revenue and gross margin next quarter.

The largest contributor to the company's performance decline is the smartphone business. Revenue is expected to be around $4.9 billion next quarter, down over 20% year-over-year, primarily due to memory supply constraints.

Qualcomm's current performance decline was expected, and the market is primarily focused on the following aspects:

a) Traditional Segment: Core Business Under Pressure

The smartphone business is Qualcomm's largest segment, accounting for over half of its revenue. The sluggish smartphone market has put significant pressure on the company's performance. Global smartphone shipments remained at 290 million units this quarter, down 5% year-over-year.

The smartphone market consists of two major camps: Apple and Android. This quarter, Apple's smartphone shipments grew 5% year-over-year, while Android shipments (excluding Apple) fell 7%, directly impacting Qualcomm's smartphone business performance.

The pressure on smartphones and IoT in the first quarter was mainly due to the dual impact of memory shortages and tighter government subsidies. The company's guidance suggests that memory shortages will persist.

Smartphone revenue is expected to be around $4.9 billion next quarter, down approximately 22% year-over-year. Management discussed memory issues last quarter, noting that they not only 'eroded' gross margins but also escalated into 'shortages,' directly impacting smartphone shipments (memory shortages → inventory/shipment disruptions → revenue declines). This 'memory shortage cycle' will continue to pressure Qualcomm's traditional core business.

b) AI Segment: On-Device AI and Data Centers as Potential Growth Markets

Qualcomm's AI layout (AI layout , meaning 'AI strategy') will have limited short-term impact on performance but offers growth potential and a new narrative.

① Collaboration with OpenAI: On April 27, reports emerged that 'Qualcomm and OpenAI are partnering with MediaTek to develop a custom chip for AI-native devices,' boosting the company's sluggish stock.

OpenAI plans to launch an AI smartphone that breaks away from the traditional 'App model,' focusing on AI Agents. This phone will run OpenAI's models directly at the system level, potentially advancing on-device AI.

For Qualcomm, collaborating with OpenAI could reduce its reliance on the 'Android camp' and reposition the company as a 'core supplier for on-device AI.'

The news has not been officially confirmed, so attention should be paid to management's response.

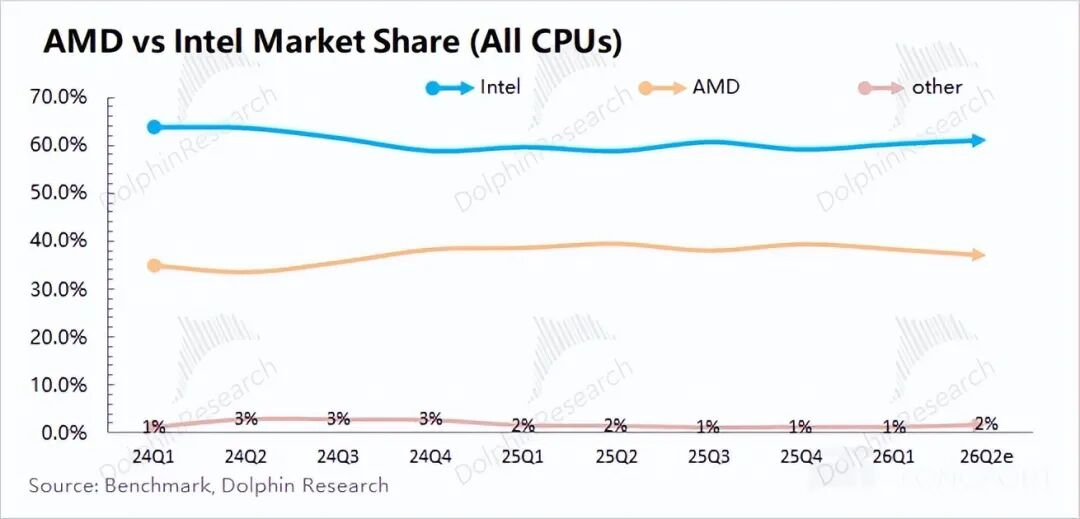

② AI PCs (vs. Intel): Qualcomm's 2026 Snapdragon X2 PC platform has entered mass production, featuring the Orion CPU and an NPU performance of 85 TOPS, making it the fastest NPU for laptops.

With the maturity of Windows on Arm architecture, Qualcomm has partnered with Microsoft, Dell, Lenovo, and others to enter the mainstream price segments. While the company has entered the PC market, its current market share remains low and poses little threat to Intel and AMD.

③ AI Data Centers: Qualcomm has announced two new AI chips—AI200 (mass production in 2026) and AI250 (mass production in 2027)—expected to contribute $5-7 billion in annual revenue starting in 2027.

Current details: 1) AI200 is a rack-level solution optimized for large language model (LLM) and multimodal inference scenarios, featuring 'high memory capacity + low total cost of ownership (TCO).' 2) AI250 adopts a near-memory computing architecture, offering 'over 10x effective memory bandwidth + lower power consumption,' focusing on memory-bandwidth-intensive inference scenarios.

The company announced post-earnings collaboration with leading supercomputing service providers for mass production, with the first shipments expected in December 2026, marking its entry into the core AI chip track ( track , meaning 'sector').

Based on Qualcomm's current market cap ($166.5 billion), its 2026 fiscal year after-tax core operating profit corresponds to approximately 21x PE (assuming revenue down 4% year-over-year, gross margin of 53.4%, and a tax rate of 13%). Historically, the company's valuation has mostly ranged between 10x and 25x PE, currently positioned slightly above the midpoint.

The company's previous lower valuation was due to its focus on traditional segments, lacking growth drivers, compounded by 'memory shortages' that pressured its traditional business. As a result, Qualcomm is eager to join the AI supply chain to boost market expectations and valuations.

For Qualcomm, traditional business pressures are well-known, including tighter government subsidies, memory shortages, and Apple's in-house modem development. The stock's decline reflects the market's full digestion of these 'sluggish' traditional business factors.

Compared to financial results, the market is more interested in AI business prospects, including AI PCs, AI data centers, and on-device AI layout (AI layout , meaning 'AI strategy'). While these businesses have limited short-term impact, new collaborations and orders generate excitement. For example, reports of on-device AI collaboration with OpenAI drove a double-digit stock price increase.

After the market broadly accepts short-term performance pressures, recent underperformance is unlikely to significantly impact the stock price. The company now primarily hopes for breakthroughs in AI-related businesses.

If Qualcomm secures large AI orders (on-device or data center-side), it will shift the company's 'narrative.' Its valuation logic will transition from a 'traditional smartphone chip company' to an 'on-device AI/data center AI chip player,' breaking historical valuation limits and unlocking greater growth potential.

Below are the details:

I. Overall Performance: Memory Shortages Continue to Pressure Traditional Business

1.1 Revenue

Qualcomm reported revenue of $10.6 billion for the second quarter of fiscal year 2026 (26Q1), down 3.5% year-over-year, in line with market expectations ($10.56 billion). QCT (semiconductor chip business) saw a significant decline, primarily due to the sluggish smartphone market and memory shortages.

1.2 Gross Profit

Qualcomm's gross profit for the second quarter of fiscal year 2026 (26Q1) was $5.7 billion, down 6% year-over-year.

The gross margin for the quarter was 53.8%, down 1.2 percentage points year-over-year and below market expectations (54.6%), primarily due to a significant decline in the gross margin of the hardware business (QCT) amid memory price hikes.

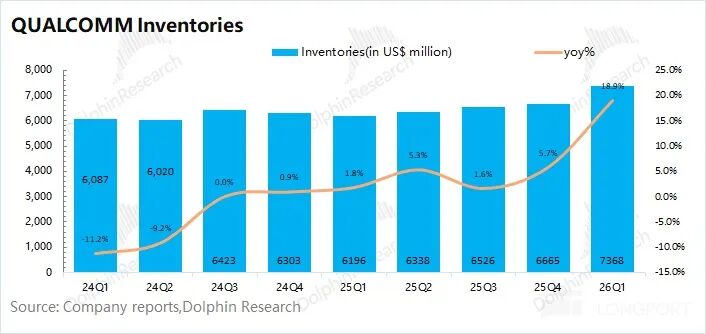

Qualcomm's inventory reached $7.37 billion in the second quarter of fiscal year 2026 (26Q1), up 19% year-over-year.

Inventory continued to rise due to cautious production plans by smartphone OEMs, as the company remains in the process of actively digesting channel inventory. Downstream clients reduced procurement and orders, with management expecting Q3 to be the 'bottom.'

1.3 Operating Expenses and Profit

Qualcomm's operating expenses for the second quarter of fiscal year 2026 (26Q1) were $3.36 billion, up 15% year-over-year.

① R&D expenses were $2.46 billion, up 11% year-over-year, remaining the company's largest investment area. ② Sales and management expenses were $900 million, up 27% year-over-year.

Given the impact of tax adjustments on profit, core operating profit is more meaningful. Qualcomm's core operating profit for the quarter was $2.3 billion, down 26% year-over-year, with a core operating margin of 21.8%. The profit decline was primarily due to lower gross margins and increased expenses.

II. Business Segmentation: Smartphones Mired in "Slump", AI Secures Major Clients

From Qualcomm's business segmentation perspective, QCT (CDMA business) remained the company's largest revenue source this quarter, accounting for 85% of total revenue, primarily comprising income from chip semiconductors. The remaining revenue mainly came from the QTL (technology licensing) business, contributing around 13%.

The QCT business is the most crucial segment of the company. A detailed breakdown is as follows:

2.1 Smartphone Business

Qualcomm's smartphone business generated $6 billion in revenue in the second quarter of fiscal year 2026 (26Q1), representing a 13% year-over-year decline, largely in line with market expectations ($6.06 billion).

Dolphin Research attributes the slowdown in the company's smartphone business growth this quarter to two primary factors: (1) The overall smartphone market performed "sluggishly" due to factors such as memory shortages and tightened government subsidies; (2) Apple's strategy of offering "more for the same price" with its new devices squeezed market share from Android brands.

Industry data reveals that smartphone shipments (excluding Apple) reached 229 million units in the first quarter of 2026, down 7% year-over-year, indicating a considerable slump in the Android smartphone market.

Compared to this quarter's performance, the company provided a revenue guidance of $4.9 billion for its smartphone business next quarter, implying a potential decline of around 22% due to ongoing memory supply constraints.

Qualcomm's smartphone business accounts for over half of the company's total revenue, making it the most significant factor influencing performance. Given the current pressures on the smartphone business, including memory shortages, tightened government subsidies, and declining market share among major clients, the company's performance is unlikely to improve significantly in the short term.

On the other hand, the overwhelming reliance on the traditional smartphone business has gradually become a burden on the company's performance and valuation. The company aims to cultivate new growth drivers while reducing the weight of its smartphone business (i.e., the Android market) and forging a "second growth curve."

2.2 Automotive Business

Qualcomm's automotive business generated $1.3 billion in revenue in the second quarter of fiscal year 2026 (26Q1), up 38% year-over-year, meeting market expectations ($1.3 billion), primarily driven by increased shipments of the fourth-generation Snapdragon Digital Chassis.

The company expects to commence commercial shipments of the fifth-generation Snapdragon Digital Chassis platform by the end of fiscal year 2026. This represents the most significant upgrade in Qualcomm's history, featuring a 3x increase in CPU throughput, a 3x boost in GPU capability, and a 12x improvement in NPU performance, supporting in-vehicle intelligent agents and L3/L4 autonomous driving processing.

The company's business model will shift from chip sales to module sales, expanding revenue potential. The company anticipates automotive business growth of around 50% year-over-year next quarter, though it will still account for only 10-20% of total revenue.

2.3 IoT Business

Qualcomm's IoT business generated $1.7 billion in revenue in the second quarter of fiscal year 2026 (26Q1), up 9% year-over-year, slightly below market expectations ($1.78 billion). Affected by tightened government subsidies and memory shortages, the IoT business's growth rate has slowed to single digits.

Qualcomm's IoT business primarily includes consumer electronics, edge networking, and industrial products. This quarter's IoT business growth was mainly driven by consumer and industrial-grade products.

Beyond conventional products, the market is also focusing on the company's AI PC and data center businesses:

(1) AI PC Business: Currently categorized under the IoT business due to its relatively small scale. Qualcomm's 2026 Snapdragon X2 PC platform has entered mass production, featuring the Orion CPU and an NPU performance of up to 85 TOPS, making it the fastest NPU for notebooks.

The company hopes AI PCs will become a new growth driver. However, its current market share in the PC segment remains low, making it difficult to compete with Intel and AMD.

(2) Data Center Business: The company previously announced its entry into the data center market. Dolphin Research believes related revenue may be included in IoT or disclosed separately.

Qualcomm announced two new AI chips—AI200 (mass production in 2026) and AI250 (mass production in 2027)—expected to contribute $5-7 billion in annual revenue starting in 2027.

Following this earnings report, management announced the company's entry into the custom chip sector, partnering with a leading hyperscale client, with initial shipments expected in the fourth quarter of 2026. This marks Qualcomm's debut as a player in the data center AI arena. The company plans to disclose more project progress and collaboration details at its Investor Day on June 24.

- END -

// Reprint Authorization

This article is an original work by Dolphin Research. Reproduction requires authorization.

// Disclaimer and General Disclosure

This report is intended for general comprehensive data purposes, designed for general reading and data reference by users of Dolphin Research and its affiliated institutions. It does not consider the specific investment objectives, product preferences, risk tolerance, financial status, or unique needs of any individual receiving this report. Investors must consult independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referencing the content or information in this report are undertaken at the investor's own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses arising from the use of the data contained herein. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, or completeness of the information and data.

The information or viewpoints mentioned in this report shall not, under any jurisdiction, be construed or deemed as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, solicitations, or endorsements of relevant securities or financial instruments. The information, tools, and data in this report are not intended for distribution to, nor are they intended to be used by, individuals or residents of jurisdictions where such distribution, publication, provision, or use contradicts applicable laws or regulations or subjects Dolphin Research and/or its subsidiaries or affiliates to registration or licensing requirements in such jurisdictions.

This report reflects only the personal viewpoints, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, with copyright reserved solely by Dolphin Research. Without prior written consent from Dolphin Research, no institution or individual may (i) reproduce, copy, duplicate, reprint, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized parties. Dolphin Research reserves all related rights.

-

![]()

Tesla Restructures Its Balance Sheet

-

![]()

Accelerating the High-Speed Interconnection Upgrade of AI Computing Clusters! JONHON Releases ELSFP External Light Source Optical Connectors

-

![]()

Breaking the overseas blockade of volumetric holographic materials, this optical enterprise secures nearly 100 million yuan in financing!

-

![]()

Why Does Jensen Huang So Openly Praise China’s AI?

-

![]()

"Wudang" Unveiled: Arm China's Next-Gen AI VPU Redefines Video Encoding

-

![]()

From Energy Conservation and Carbon Reduction to AI Decision-Making: GECON East Intelligence and Chery Group Explore a New Green and Smart Paradigm for Automobile Manufacturing

-

![]()

WAIC 2026 Observation | AI Accelerates Towards the Core of Industries, Industrial AI Enters a Critical Phase

-

![]()

Volkswagen China Fires the First Shot in Foreign-Funded 'White Box Delivery'!