Apple: Can It Remain 'Steadily Happy' Despite AI Absence and Rising Storage Costs?

05/09 2026

05/09 2026

635

635

Apple (AAPL.O) released its Q2 FY2026 earnings report (as of March 2026) after the market closed on the morning of May 1, 2026, Beijing time. Key points are as follows:

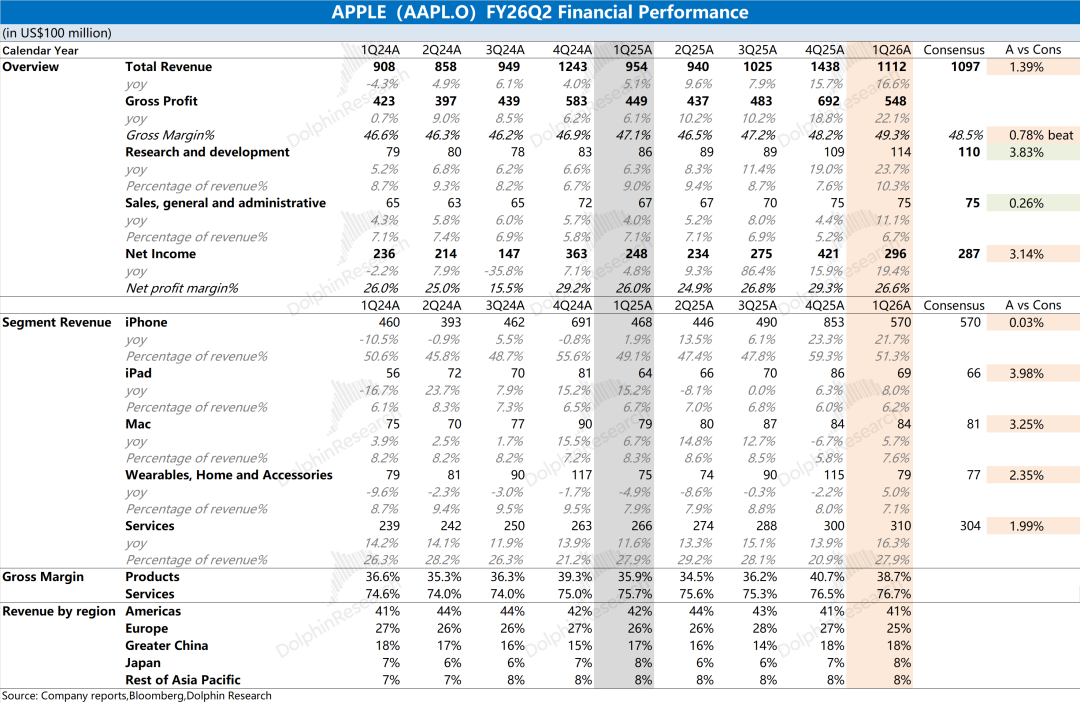

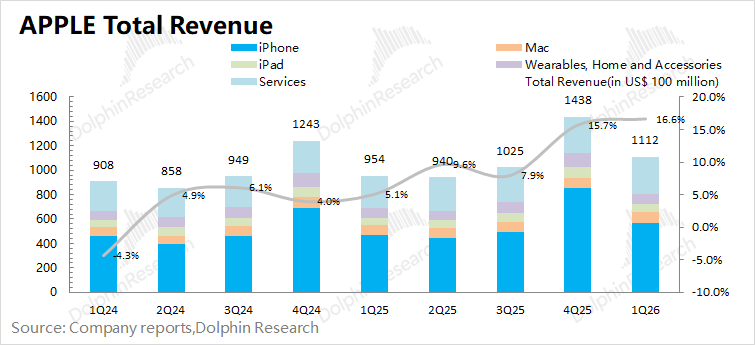

1. Overall Performance: In this quarter, Apple achieved revenue of $111.2 billion, a year-over-year increase of 16.6%, outperforming market expectations ($109.7 billion). The growth in the company's revenue this quarter was primarily driven by increases in iPhone and software services.

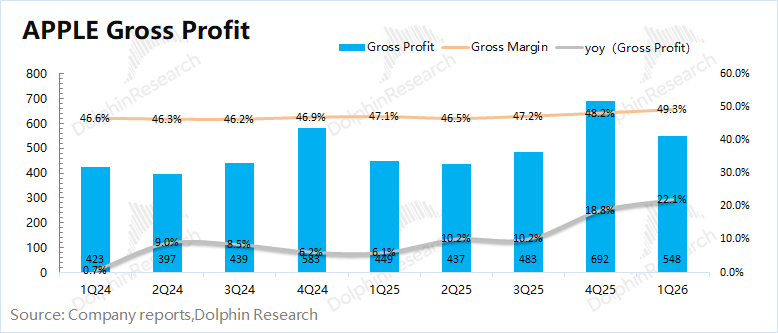

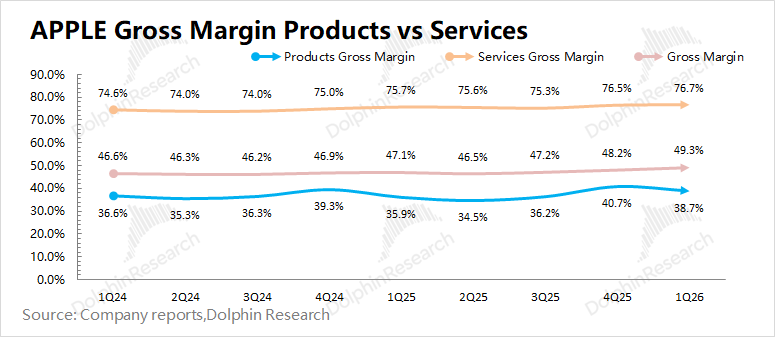

Apple's gross margin was 49.3%, up 2.2 percentage points year-over-year, exceeding market expectations (48.5%). The gross margin for software services rose to 76.7%, while the gross margin for hardware was 38.7% (up 2.8 percentage points year-over-year). The improvement in hardware gross margin this quarter was mainly influenced by increased sales of the iPhone 17 series and the depreciation of the US dollar against the Chinese yuan.

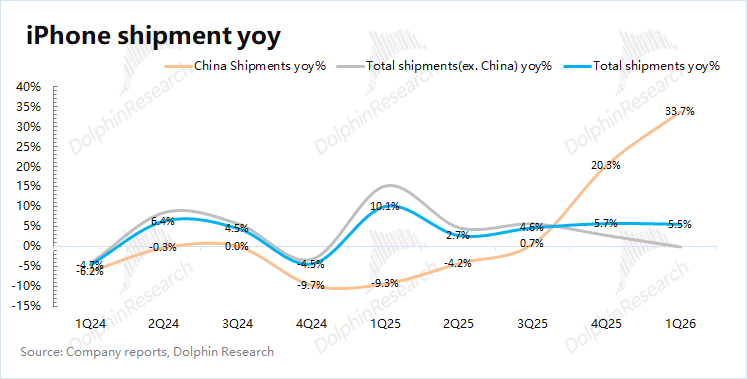

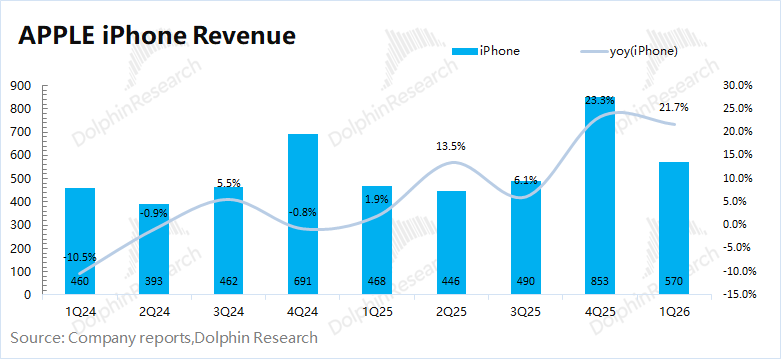

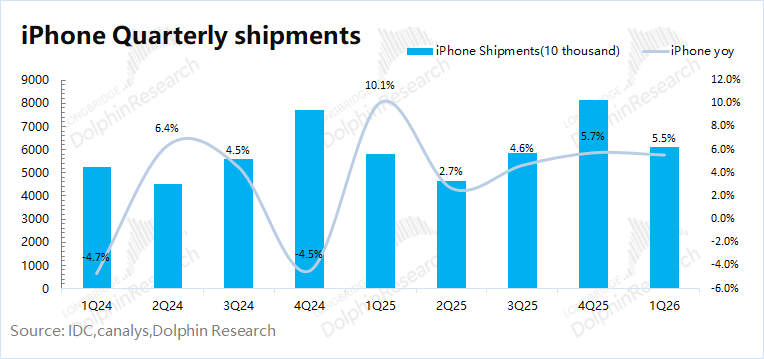

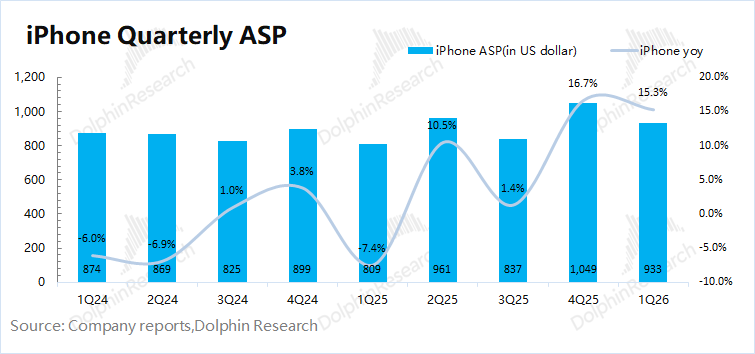

2. iPhone: The company's iPhone business generated $57 billion in revenue this quarter, a year-over-year increase of 21.7%, meeting market expectations ($57 billion). The growth in the mobile phone business this quarter was primarily driven by strong sales of the iPhone 17 series in China and the depreciation of the US dollar against the Chinese yuan. For this quarter, Dolphin Research estimates that overall iPhone shipments increased by 5.5% year-over-year, with the average selling price rising by 15.3% year-over-year.

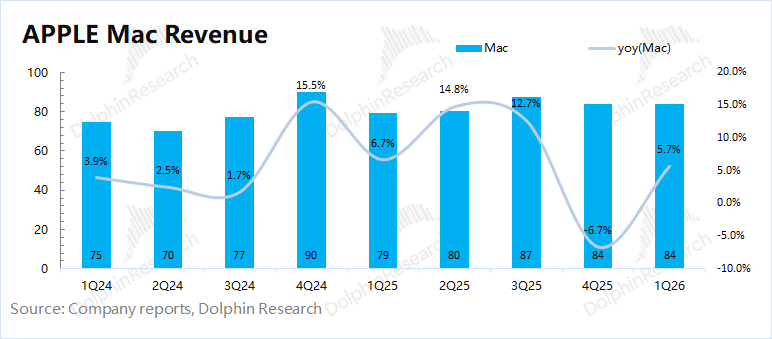

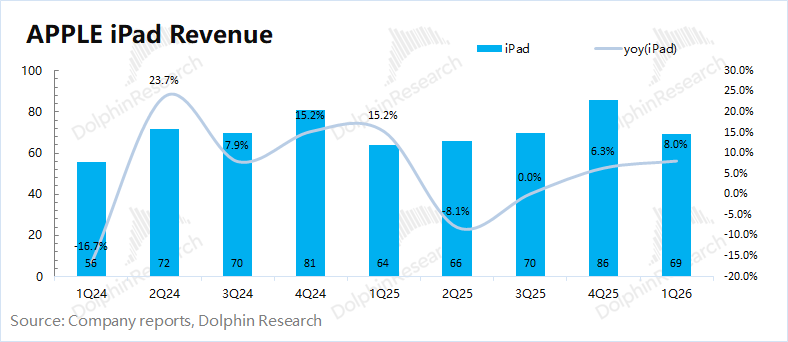

3. Other Hardware Beyond iPhone: All showed varying degrees of growth. The company's iPad business achieved an 8% year-over-year increase this quarter, mainly driven by growth in M5 Pro and A16 models. The company launched the MacBook Neo this quarter, with the starting price reduced to $599, covering a broader consumer base and driving the Mac business back to growth.

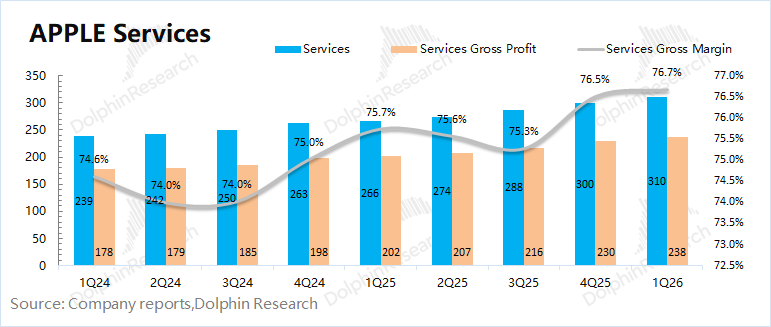

4. Software Services: The company's software services revenue reached $31 billion this quarter, outperforming market expectations ($30.4 billion) with a year-over-year increase of 16%. With a high gross margin of 76.7%, the software business contributed 28% of the company's revenue but generated 43% of its gross profit.

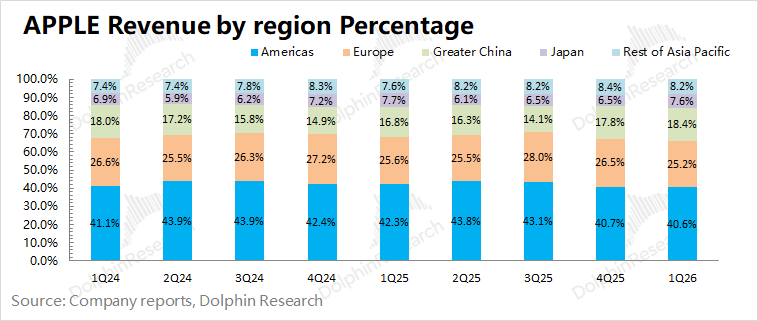

5. Regional Revenue: The Americas remained the company's primary market, accounting for over 40% of revenue and achieving a 12% year-over-year increase this quarter. Greater China was the best-performing region this quarter, with iPhone sales in mainland China increasing by 33% year-over-year (according to IDC data), as the iPhone 17 256G model also benefited from national subsidy policies.

Dolphin Research's Overall View: iPhone 17's Popularity Raises Questions About Whether the New Siri Can Address AI Shortcomings

Apple's performance this quarter was quite strong overall, with both revenue and gross margin outperforming market expectations, primarily driven by the iPhone 17 series and the depreciation of the US dollar against the Chinese yuan.

① Revenue Growth: Mainly driven by strong sales of the iPhone 17 series. iPhone business revenue increased by 22% year-over-year this quarter, with iPhone shipments in the Chinese market surging by 33% year-over-year. Although the iPhone 17 series lacked significant innovation, the model achieved notable success in the Chinese market. The iPhone 17 256G model captured market share from Android brands in China while benefiting from national subsidy policies.

② Gross Margin Improvement: Despite rising storage costs, the company's hardware gross margin increased year-over-year, mainly due to the scale effect of increased iPhone shipments and the depreciation of the US dollar against the Chinese yuan. Since Apple's products, such as the iPhone, are primarily targeted at the mid-to-high-end market, the impact of rising storage costs on the company's cost structure was relatively smaller compared to competitors, allowing Apple to better absorb this pressure.

Beyond this quarter's data, company management provided guidance for the next quarter: revenue is expected to increase by 14-17% year-over-year, corresponding to $107.1-$110 billion; the gross margin is projected to be 47.5-48.5%. The iPhone business will remain the primary driver of growth next quarter. Despite facing significant pressure from rising storage costs, the company still provided a relatively strong gross margin guidance, reflecting its excellent supply chain management capabilities.

Beyond Apple's earnings report, the market is also focused on the following aspects:

a) CEO Transition: Apple announced a leadership transition, with Tim Cook stepping down as CEO on September 1 to become Executive Chairman, succeeded by John Ternus, Senior Vice President of Hardware Engineering.

The new CEO, Ternus, has a hardware engineering background, aligning with the competitive demands of next-generation smartphones and AI devices. Cook will remain as Executive Chairman to ensure smooth global policy coordination and strategic transition.

The market generally believes that this leadership transition was a well-considered arrangement and that the personnel changes will not lead to significant shifts in Apple's strategic direction. Apple will continue to focus on the strategic balance between hardware and services, maintaining product and service growth through vertical integration and supply chain advantages. Subsequent attention can be paid to specific statements made by company management during the conference call.

b) Recovery in the Chinese Market: The company's performance recovery this quarter was primarily driven by increased iPhone sales in China. Breaking it down, iPhone shipments in the Chinese market increased by 33% year-over-year this quarter, while shipments in other markets (outside China) remained largely flat year-over-year.

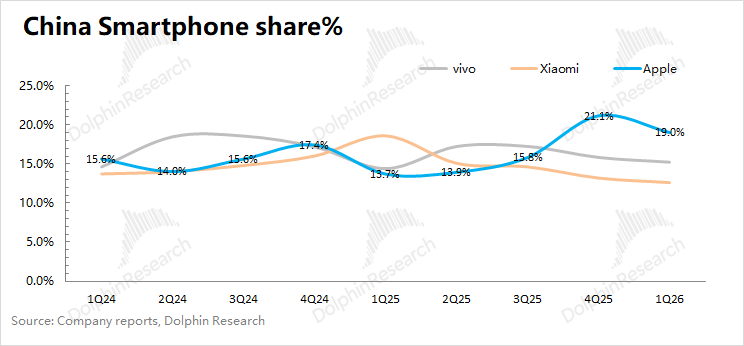

The iPhone 17 series performed well in the Chinese market, partly because the impact of rising storage costs on iPhones was relatively smaller, and partly because the iPhone 17 256G model's eligibility for national subsidies put significant competitive pressure on Android brands. iPhone's market share in China reached 19% this quarter, up 5.3 percentage points year-over-year.

c) Measures to Address Rising Storage Costs: ① Signing long-term memory procurement agreements to lock in costs. Leveraging scale advantages to secure favorable memory contract prices + building inventory in advance as a buffer; ② While developing in-house modems, reducing costs for other non-memory components; ③ Optimizing product mix or implementing appropriate price increases to raise the company's average selling price. Considering the gross margin guidance provided for the next quarter, the company still has the ability to mitigate the impact of rising storage costs through supply chain management.

Driven by the strong growth of the iPhone 17 series, Apple's short-term performance is quite impressive. Regarding the impact of rising storage costs, the market can see that the company can dilute or absorb cost pressures through long-term agreements, supply chain management, and product mix adjustments.

However, recent 'outstanding' performance does not eliminate market doubts about the sustainability of the company's high growth, keeping its valuation within traditional ranges. Given the ongoing advancements in AI and large models, the market is more eager for Apple to achieve innovation breakthroughs in AI or the new Siri, which represent key growth prospects in the medium to long term.

Apple boasts a vast hardware user base, providing the company with a relatively ample 'buffer period.' However, if the company fails to achieve breakthroughs in AI, it may face competition from other players. Recently, there have been reports that OpenAI plans to launch an AI smartphone that breaks away from the traditional 'App model.'

Overall, Apple's short-term performance is impressive, primarily reflecting strong sales of the iPhone 17 and the company's excellent supply chain management capabilities, maintaining a relatively clear 'moat' advantage.

Behind this 'stable' performance, the market is more eager for the company to innovate and break through, enabling it to surpass traditional valuation ranges. The recent management change is also a sign of the company's pursuit of change, and attention can be paid to management's outlook and strategic plans for the future.

Here is a detailed analysis:

I. Apple's Core Business Remains 'Very Strong'!

1.1 Revenue:

In the second quarter of fiscal year 2026 (1Q26), Apple achieved revenue of $111.2 billion, a year-over-year increase of 16.6%, outperforming market expectations ($109.7 billion). All of the company's businesses saw varying degrees of growth this quarter, particularly benefiting from accelerated growth in the iPhone business.

From the perspectives of hardware and software:

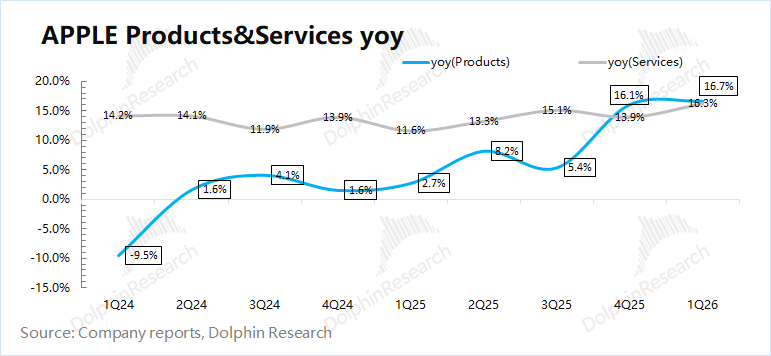

① The company's hardware business grew by 16.7% this quarter. The acceleration in hardware business growth was primarily driven by the iPhone business. With strong sales of the iPhone 17 series, the iPhone business maintained growth of over 20% for two consecutive quarters.

② The company's software business grew by 16.3% this quarter, maintaining double-digit growth. The resolution of the Google lawsuit earlier reduced risks for the company's software business. As AI applications integrate more models, the company's software business is expected to sustain growth momentum even with single-digit growth in the App Store.

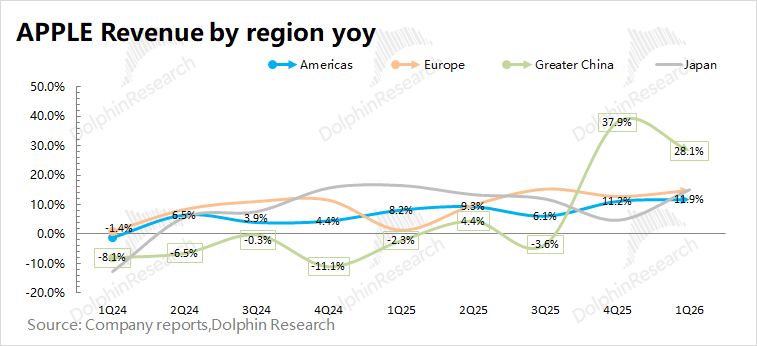

From a regional perspective: Revenue increased year-over-year in all regions. The Americas, Europe, and Greater China are the company's three primary revenue sources. Specifically, the Americas accounted for over 40% of revenue, with 12% growth this quarter; Europe maintained growth of 14.7% this quarter.

Greater China was the best-performing region this quarter, with growth reaching 28%. This was because the iPhone 17 256G model also qualified for national subsidy policies, directly driving a 33% year-over-year increase in iPhone sales in mainland China this quarter.

1.2 Gross Margin:

In the second quarter of fiscal year 2026 (1Q26), Apple's gross margin was 49.3%, up 2.2 percentage points year-over-year, outperforming market expectations (48.5%). The improvement in the company's gross margin was primarily driven by increases in both hardware and software gross margins.

Breaking down gross margins by hardware and software: Apple's software gross margin continued to rise to 76.7% this quarter; hardware gross margin increased year-over-year to 38.7%, mainly benefiting from the scale effect of strong sales of the iPhone 17 series, reduced tariff costs, and the depreciation of the US dollar against the Chinese yuan.

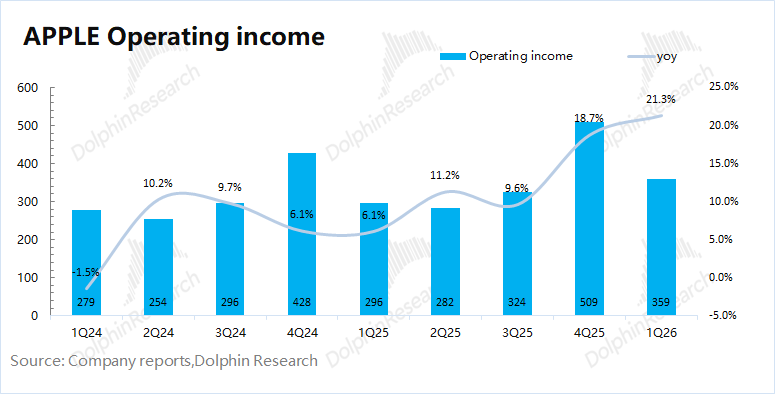

1.3 Operating Profit:

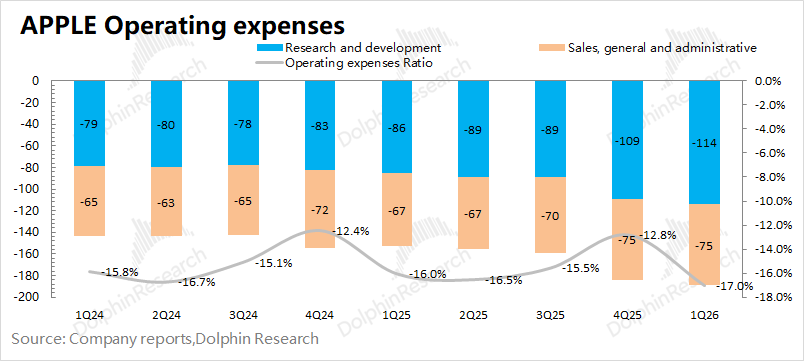

In the second quarter of fiscal year 2026 (1Q26), Apple's operating profit was $35.9 billion, a year-over-year increase of 21%. The growth in the company's operating profit this quarter was driven by both revenue growth and gross margin improvement.

The company's operating expense ratio was 17% this quarter, up 1 percentage point year-over-year. This was mainly due to increased investment in research and development for both products and services, with R&D expenses rising by 23% year-over-year this quarter.

In terms of capital expenditures, compared to the hundreds of billions in quarterly investments by tech giants, Apple's quarterly capital expenditures were just $1.97 billion, a significant year-over-year decline of 36%. Despite increased AI investments by other major companies, Apple has maintained relatively low capital expenditures.

However, Apple is not neglecting AI; rather, because the company does not engage in external data center operations and develops its own chips, its AI-related R&D investments are reflected in R&D expenses for in-house chip development rather than capital expenditures for purchasing chips from external suppliers. The company's R&D expenses are indeed increasing, but the scale remains small compared to the chip purchases of cloud service providers.

II. iPhone: Strong Sales in China Drive Growth Against the Trend

In the second quarter of fiscal year 2026 (1Q26), iPhone business revenue was $57 billion, a year-over-year increase of 21.7%, meeting market expectations ($57 billion). The year-over-year growth in the company's iPhone business this quarter was primarily driven by strong sales of the iPhone 17 series in China and the depreciation of the US dollar against the Chinese yuan.

From the perspective of the relationship between volume and price, Dolphin Research will analyze the main sources of growth in the iPhone business this quarter:

1) iPhone Shipments: According to IDC data, the global smartphone market declined by 5% year-over-year in the first quarter of 2026. Apple's global shipments increased by approximately 5.5% year-over-year this quarter, outperforming the overall market.

The growth in the company's shipments this quarter was primarily driven by sales of the iPhone 17 series in the Chinese mainland market. With the iPhone 17 256G eligible for national subsidies, sales in the Chinese mainland region increased by 33% year-over-year this quarter (while the overall Chinese market declined by 3.6% year-over-year), making it the best-performing market.

2) Average Selling Price (ASP) of iPhones: Based on iPhone business revenue and shipment volume, the ASP for iPhones this quarter was approximately $933, a 15% year-over-year increase. Influenced by the iPhone 17 series and the depreciation of the U.S. dollar against the Chinese yuan, both revenue and product selling prices in China benefited from favorable exchange rate movements.

III. Other Hardware Beyond iPhones: Return to Growth

3.1 Mac Business

In the second quarter of fiscal year 2026 (1Q26), Mac business revenue reached $8.4 billion, up 5.7% year-over-year, outperforming market expectations ($8.1 billion).

According to IDC, global PC market shipments increased by 3.8% year-over-year this quarter, while Apple's PC shipments grew by 12.7% year-over-year, outperforming the overall market. Combining company and industry data, Dolphin Research estimates that the ASP for Macs this quarter was $1,355, a 6% year-over-year decline.

This quarter, the company released products such as the MacBook Neo (with a starting price reduced to $599 to attract a broader user base), the M5 MacBook Air, and the M5 Pro/M5 Max MacBook Pro. The market response to the MacBook Neo, in particular, has been quite positive.

3.2 iPad Business

In the second quarter of fiscal year 2026 (1Q26), iPad business revenue reached $6.9 billion, up 8% year-over-year, outperforming consensus expectations ($6.65 billion), primarily driven by growth in the M5 Pro and A16 models.

More than half of the iPads sold this quarter were to new users, with double-digit growth achieved in emerging markets (India, Mexico, Thailand, etc.).

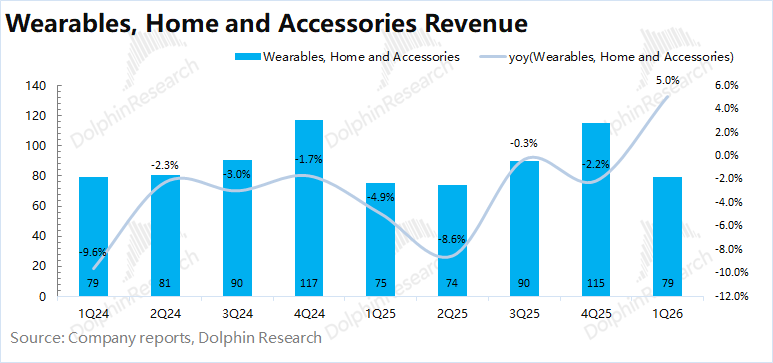

3.3 Wearables and Other Hardware

In the second quarter of fiscal year 2026 (1Q26), revenue from wearables and other hardware reached $7.9 billion, up 5% year-over-year, slightly outperforming market expectations ($7.7 billion), with growth primarily driven by the wearables and accessories businesses.

IV. Software Services: Solid "Ecosystem Moat," Anticipation for New Siri

In the second quarter of fiscal year 2026 (1Q26), software services revenue reached $31 billion, up 16% year-over-year, outperforming consensus expectations ($30.4 billion). Even with the U.S. App Store allowing external links, Apple's software services revenue maintained double-digit growth, reflecting the strength of Apple's software ecosystem.

Gross margin for software services was 76.7% this quarter, continuing to improve. With its high gross margin, the software business contributed 28% of the company's revenue but generated 43% of its gross profit this quarter.

This quarter, the company's software services business reached record highs in both developed and emerging markets, while also setting revenue records in areas such as advertising, music, payments, and cloud services. The Apple App Store introduced new advertising slots in search results and will launch ads in Apple Maps in the U.S. and Canada this summer (focusing on local businesses).

Apple Intelligence now integrates dozens of capabilities, including visual intelligence and real-time translation. Regarding the market's focus on the new Siri, the company clearly stated that it will be launched this year.

Apple believes that AI is not a standalone feature but rather a capability based on chip and on-device AI processing, emphasizing privacy first. Given the company's current R&D growth rate, which is significantly faster than its overall growth rate, AI investment represents an additional incremental portion.

The resolution of the previous Google lawsuit has released risks for Apple's software business. Considering Apple's ability to control its ecosystem, even if single-digit growth in the App Store becomes the norm, it will not affect the overall double-digit growth performance of the services business.

After purchasing the "Gemini" service, Apple has deepened its cooperation with Google in software. Google Gemini will provide Apple with trillion-parameter models and technical support, while underlying computation will still rely entirely on on-device computing and Apple's private cloud.

If the new Siri launched this year delivers "impressive" performance, it will not only empower Apple's AI capabilities but also bring more growth opportunities.

- END -

// Reposting and White-Labeling

This article is an original piece by Dolphin Research. Reposting requires authorization.

// Disclaimer and General Disclosure

This report is for general comprehensive data purposes only, intended for users of Dolphin Research and its affiliated institutions for general reading and data reference. It does not consider the specific investment objectives, investment product preferences, risk tolerance, financial situation, or special needs of any individual receiving this report. Investors must consult with independent professional advisors before making investment decisions based on this report. Any investment decisions made using or referring to the content or information in this report are at the investor's own risk. Dolphin Research shall not be liable for any direct or indirect responsibilities or losses that may arise from the use of the data contained in this report. The information and data in this report are based on publicly available sources and are for reference purposes only. Dolphin Research strives to ensure but does not guarantee the reliability, accuracy, and completeness of the information and data.

The information or opinions mentioned in this report shall not, under any jurisdiction, be regarded or treated as an offer to sell securities or an invitation to buy or sell securities, nor shall they constitute recommendations, inquiries, or endorsements of relevant securities or related financial instruments. The information, tools, and data in this report are not intended for or proposed for distribution to jurisdictions where distribution, publication, provision, or use of such information, tools, and data conflicts with applicable laws or regulations, or to citizens or residents of jurisdictions where Dolphin Research and/or its subsidiaries or affiliated companies are required to comply with any registration or licensing requirements in that jurisdiction.

This report merely reflects the personal views, insights, and analytical methods of the relevant contributors and does not represent the stance of Dolphin Research and/or its affiliated institutions.

This report is produced by Dolphin Research, and the copyright is solely owned by Dolphin Research. Without the prior written consent of Dolphin Research, no institution or individual may (i) reproduce, copy, duplicate, reprint, forward, or create any form of copies or replicas in any manner, and/or (ii) directly or indirectly redistribute or transfer them to other unauthorized persons. Dolphin Research reserves all relevant rights.

-

![]()

Zhipu's Trillion-Dollar Valuation: A New Chapter for China's AI

-

![]()

Is Laifen, a 'Dyson Alternative' on the Rise, Now Ensnared by the 'Alternative Curse'?

-

![]()

Beyond Patents: Insta360 and DJI Compete in Retail

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving

-

![]()

Insta360 vs DJI: A Fiercely Contested Duel Despite Lopsided Market Clout

-

![]()

Sino-US Autonomous Driving Divergence: Overseas Authoritative Index Reveals True Track Gaps

-

![]()

Insta360 Goes All In Against DJI

-

Changan Automobile Encounters Triple Challenges: Declining New Energy Vehicle Adoption, Sharp Profit Drops, and All-Time Low Stock Price