Who are the key players in the WiFi6 chip market, both visible and behind the scenes?

05/09 2026

05/09 2026

488

488

Seven years have passed since WiFi6 officially began certification in 2019. Despite three years of hype around WiFi7, the 6GHz frequency band has yet to be fully deployed globally. In the wireless arena, WiFi6 has quietly sustained revenue and profitability for many chip manufacturers.

01

WiFi6: Still the Market Mainstream

The success of WiFi6 (802.11ax) stems from its precise alignment with essential needs, balancing performance and cost. It achieves a theoretical peak rate of 9.6Gbps, supports OFDMA and 8-stream MU-MIMO technologies, ensuring smooth transmission and low latency (10–30ms) for multiple connected devices. With TWT technology, it reduces terminal power consumption. Its compatibility with the full 2.4GHz and 5GHz bands enhances wall penetration and interference resistance. Affordable routers priced around $15 can meet gigabit broadband and 4K streaming demands, making it the mainstream (mainstream) choice for households and SMEs.

WiFi7 (802.11be), however, offers significant theoretical improvements, with a peak rate of 46.1Gbps, support for 320MHz ultra-wide channels and 4096-QAM modulation, MLO multi-link aggregation for cross-band parallel transmission, latency as low as 1–5ms, and a 16×16 MU-MIMO design for high-density access stability. Yet, these advantages remain largely theoretical for now.

Currently, WiFi7 faces three core challenges to widespread adoption. First, spectrum limitations: the 6GHz band is primarily allocated to mobile communications in China, restricting its civilian use and preventing WiFi7 from fully leveraging its performance advantages. Second, the terminal ecosystem lags, with less than 10% of smartphones and computers supporting WiFi7, and scarce compatible smart home devices, resulting in a subpar overall experience. Third, high costs persist, with WiFi7 chips and modules currently priced at 2–3 times those of WiFi6, and routers remaining expensive, further dampening upgrade enthusiasm among general users.

Market data shows that the WiFi6 and WiFi6E chipset market was valued at approximately $39.03 billion in 2024 and is projected to grow to $107.4 billion by 2033. This growth is driven by increasing demand for high-bandwidth applications like 4K/8K video streaming, online gaming, and cloud computing.

The emergence of WiFi7 is expected to further accelerate market expansion, enhancing performance and reducing latency. However, WiFi6 is likely to remain dominant for the next 2–3 years. WiFi7 will only achieve large-scale adoption once conditions such as civilian access to the 6GHz band, a mature terminal ecosystem, and price reductions are met.

02

Strategic Divergence Among the Three Chip Giants

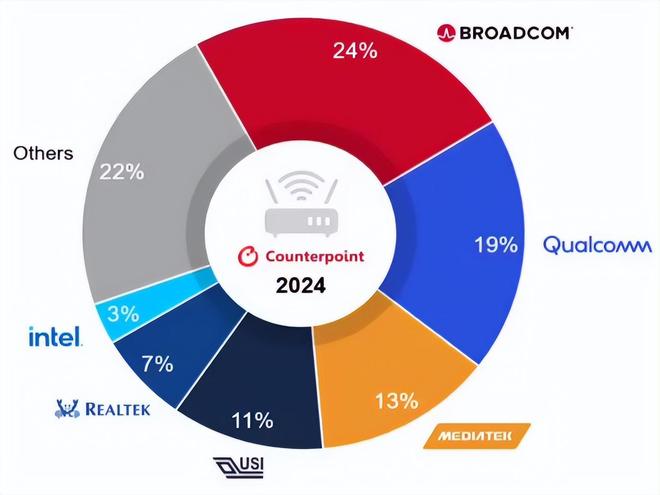

According to Counterpoint market data, in 2024, Broadcom led the Wi-Fi6, 6E, and Wi-Fi7 markets with a 24% share, followed by Qualcomm (19%) and MediaTek (13%). The three have chosen vastly different paths.

Broadcom's strength lies in its "fully autonomous and controllable" hard power: it independently develops and produces almost all key components, from RF front-end and baseband processing to switch chips and SoC cores. Focusing on the high-end market, its major client is Apple. Beyond iPhones, Broadcom chips are widely used in most high-end wireless routers and enterprise-grade APs globally, earning a reputation for stable performance as the "flagship standard."

If Broadcom is a hardcore player focusing on core chips, Qualcomm is an ecosystem builder specializing in integrated solutions. Its Wi-Fi platforms are never single chips but complete solutions integrating AI processing, Mesh networking, and carrier-grade management, emphasizing "out-of-the-box experience upgrades." On mobile devices, chips like FastConnect 6900/7800 are deeply coupled with Snapdragon platforms, offering peak rates up to 4.8Gbps and optimizing system-level power consumption and intelligent connectivity through features like 4K QAM and 160MHz channel bandwidth. On the network side, platforms like Networking Pro 1200 support up to 12 spatial streams and 1,500 concurrent users, with flexible tri-band configurations.

MediaTek has risen rapidly through precise positioning. In its Filogic series, the mainstream Filogic 830 adopts a 12nm advanced process, integrating a 4×4 WiFi6 baseband and RF, achieving a maximum rate of 6Gbps, and introducing a unique 3T3R RF architecture and built-in front-end module. This highly integrated design not only reduces system power consumption but also significantly cuts peripheral component counts and material costs, enabling terminal manufacturers to quickly launch affordable, high-performance WiFi6 routers. As a result, MediaTek has rapidly grown in the consumer router and smart home markets, with its share climbing to around 13%, becoming a key driver of WiFi6 adoption in the mass market.

03

The Overlooked Player Tiers: Intel, Realtek, HiSilicon, UNISOC

Although Intel has exited the mobile SoC market, its WiFi chips remain dominant in the notebook sector, particularly due to their integrated connectivity with Intel Core platforms, a preferred choice for many PC manufacturers. Realtek, meanwhile, quietly dominates the sub-$15 router market and IoT devices with massive shipment volumes.

However, the real variables lie in mainland China.

The technical difficulty and application scenarios of Wi-Fi chips create a natural hierarchical structure. From bottom to top, there are IoT-end chips, data transmission STA-end chips, and AP-end chips.

In the IoT Wi-Fi MCU sector, domestic manufacturers have established certain advantages, with typical players including Espressif and BK Integrate. Espressif's main product is the ESP32-C series. In April 2021, it released the ESP32-C6, its first SoC supporting Wi-Fi6. In May 2022, it launched the ESP32-C5, the world's first RISC-V architecture 2.4/5GHz Wi-Fi6 dual-band dual-mode SoC. Both Wi-Fi6 products integrate self-developed low-power Bluetooth technology and have achieved mass production.

STA-end chips refer to Wi-Fi chips used in terminal devices such as smartphones, tablets, laptops, TVs, and set-top boxes. Compared to IoT-end chips, this field demands significantly higher RF performance, data throughput, and power management, posing greater technical challenges.

Domestic manufacturers continue to make strides in this track (sector), with representative companies including Wuqi, Amlogic, and HiSilicon.

In 2022, Wuqi introduced China's first 1x1 dual-band concurrent Wi-Fi6 chip, WQ9101; in 2023, it launched the 2x2 dual-band high-performance Wi-Fi6 STA chip, WQ9201, integrating Wi-Fi6 RF and baseband performance on a single chip. Its performance rivals international first-tier manufacturers, filling multiple technical gaps in China's high-end Wi-Fi6 chip sector and leading internationally in certain metrics, such as 30%–40% lower Wi-Fi6 PA power consumption compared to current industry levels. Public information shows that Wuqi's WQ9201 STA has been shipped in bulk for applications like set-top boxes, cloud computers, and enterprise routers.

Amlogic's W-series chips are self-developed high-speed data transmission Wi-Fi Bluetooth dual-mode integrated chips, already in mass production. Its official website lists Wi-Fi6 product models including W265P1, W265S1, and W265U1 (2T2R, 22nm) in Wi-Fi6+BLE5.4 combinations, primarily targeting markets like smart set-top boxes and smart TVs.

AP chips are the core components of routers and gateways, acting as the "central brain" of Wi-Fi networks. Their R&D difficulty is the highest, and their strategic significance is immense, making them a critical area where domestic chipmakers urgently need breakthroughs.

Technical barriers in this field concentrate on three points: first, integrating the most complex Wi-Fi protocol stacks, multi-user scheduling algorithms, and RF front-end designs; second, requiring long-accumulated top-tier IP, RF analog design capabilities, and system-level integration experience; third, the iterative pressure from new-generation technologies—Wi-Fi6 upgrades modulation from 256-QAM to 1024-QAM, significantly increasing single-spatial-stream data throughput and imposing stringent requirements on RF front-end and baseband processing; while Wi-Fi7's key technologies like 320MHz channels, 4096-QAM modulation, and multi-link operation (MLO) further raise the bar. Currently, domestic chips still lag behind international leaders in 6GHz band RF performance, EVM metrics, and latency control.

Despite these challenges, a few domestic enterprises are accelerating their efforts, such as HiSilicon, Wuqi, and Sichip Communication.

04

The Future of WiFi Chips: AI Chipification and Chip AIization

The battleground for WiFi chips is no longer just about "speed competition."

From "mere connectivity conduits" to "edge intelligence nodes," the deep integration of AI and WiFi is reshaping the entire industry logic.

First is "AI chipification": hard-integrating NPU, DSP, and other AI acceleration units into WiFi baseband and RF sides, directly hardwareizing algorithms like channel analysis, interference suppression, and traffic scheduling to achieve real-time, low-power localized intelligent processing, completely freeing dependency on cloud computing power. Second is "chip AIization": deeply binding WiFi protocol stacks with AI algorithms to enable adaptive RF optimization and intelligent band selection through machine learning, focusing competitiveness on user-perceivable metrics like latency, concurrent experience, and energy efficiency.

The underlying logic is simple: the AIoT boom has spurred demand for "connectivity + edge computing," the lightweighting of large models has made on-device intelligence feasible, and cost reductions driven by process advancements are creating a triple resonance that accelerates the penetration of AI WiFi chips.

Recent market enthusiasm has been ignited by new product launches from leading manufacturers, each addressing industry pain points directly:

Broadcom took the lead, unveiling the world's first Wi-Fi8 chip ecosystem in October 2025, featuring built-in hardware AI acceleration engines for full-scenario coverage. The new Wi-Fi8 solution series includes: BCM6718 for residential and operator access applications, BCM43840 and BCM43820 for enterprise access applications, and BCM43109 for edge wireless clients like smartphones, laptops, tablets, and automobiles. At CES 2026, it added new products to strengthen low-latency advantages for home AI applications.

Mark Gonikberg, Senior Vice President and General Manager of Broadcom's Wireless Communications and Connectivity Division, stated: "Wi-Fi8 represents a fundamental shift in wireless networks. The AI era demands faster, smarter, and more reliable networks. Broadcom's Wi-Fi8 products deliver high-performance, low-latency, and predictable connectivity for edge AI. We will also drive Wi-Fi8 adoption across the industry through flexible licensing models, accelerating edge AI development."

Qualcomm followed closely, releasing its AI-native Wi-Fi8 full product line in March 2026. This comprehensive portfolio includes the Qualcomm FastConnect 8800 mobile connectivity system and five new Qualcomm Atheros networking platforms. Each product is designed to deliver the connectivity and computing performance needed for next-generation products, meeting real-world AI demands with groundbreaking architectures and unparalleled intelligence.

Gautam Sheoran, Senior Vice President and General Manager of Connectivity, Broadband, and Networking at Qualcomm Technologies, said: "As AI-driven demands evolve, network traffic patterns are fundamentally changing, requiring us to rethink core architectures. Qualcomm Technologies is redefining this architecture to make AI ubiquitous. Next-generation networks and devices need not only AI-native designs but also new high-performance, intelligent connectivity. Our Wi-Fi8 products offer a complete solution: faster speeds, higher reliability, longer range, and powerful AI capabilities."

Qualcomm Technologies' Wi-Fi8 product portfolio has received positive feedback from the industry.

Currently, all solutions in Qualcomm Technologies' Wi-Fi8 portfolio are being sampled to customers, with commercial terminals expected to launch in the second half of 2026.

Ultimately, the outbreak (boom) of AI WiFi chips is not merely a functional superposition (addition) but a fundamental transformation of industry logic. 2026 marks the first year of its large-scale commercialization. With technological generational shifts, ecosystem synergies, and accelerated localization, the high-growth cycle of this multi-billion-dollar track (sector) has begun. Manufacturers with AI hard integration capabilities and the ability to provide multi-protocol fusion and scenario-based solutions will undoubtedly become the biggest winners in this trend.

-

![]()

Piercing Through Industry Chaos: The Curtain Rises on Compliance for Autonomous Driving

-

![]()

Insta360 vs DJI: A Fiercely Contested Duel Despite Lopsided Market Clout

-

![]()

Insta360 Goes All In Against DJI

-

Changan Automobile Encounters Triple Challenges: Declining New Energy Vehicle Adoption, Sharp Profit Drops, and All-Time Low Stock Price

-

PTFE's 'AI Moment': Transforming from the 'Plastic King' to the Pinnacle Material for Computing Infrastructure

-

![]()

When Apple Starts to Pay the AI Tax

-

![]()

Robot Traffic Outpaces Human Traffic: With AI Needing Neither Rest nor Spending Power, Who Will Purchase Ad Spaces?

-

![]()

A Dark Horse Emerges in the AI Vision Track: A 50-Year-Old Veteran Creates "AI Eyes" and Launches the "First Physical AI Stock"