Samsung’s Home Appliance Business: A Seemingly Inevitable Decline

05/11 2026

05/11 2026

401

401

Author | Fang Qiao Editor | Wang Gefa

Selling off inventory and then withdrawing—this appears to be Samsung’s final move in the Chinese market.

Samsung Electronics announced on its official website that it would cease selling all home appliance products in mainland China, encompassing a full range of categories such as TVs, monitors, air conditioners, refrigerators, and washing machines. This marks the end of Samsung’s 34-year presence in China’s home appliance market.

Once the news broke, the market’s reaction was rather counterintuitive. Samsung’s stock price surged instead of plummeting, jumping by over 14% in a single day and pushing its market capitalization past the $1 trillion mark. On JD.com, Samsung TV transaction volume soared by over 200% year-on-year, while offline stores were flooded with calls as many consumers rushed to purchase what they perceived as the ‘last batch.’

Behind this withdrawal lies a company’s strategic retreat following a complete shift in profit focus, as well as the final chapter in two decades of evolution within China’s home appliance industry.

In fact, signs of this exit had surfaced early. Three weeks prior to the official announcement, the president of Samsung’s Visual Display Business Division publicly stated in Seoul that the Chinese market faced numerous challenges and that a comprehensive business assessment was underway. After the Chinese New Year this year, Samsung largely halted restocking products in mainland China, leading to shortages of some popular TV models in multiple regions. A store employee revealed that only about 30,000 units of Samsung home appliances remained in inventory across China.

However, this was not a sudden collapse; rather, it was a long, gradual decline.

Around 2013, Samsung TV still commanded nearly a 20% share of China’s high-end large-screen TV market, with shipments reaching 2.55 million units in 2014, making it the top foreign brand. Yet, its market share dwindled year by year. Data from Aowei Cloud shows that by 2025, its online sales share had dropped to 0.67%, while its offline share stood at just 3.09%. The decline was even more pronounced for refrigerators and washing machines, with market shares hovering around 0.4%.

Over a decade, TV shipments plummeted from 2.55 million units to about 300,000 units, a nearly 90% drop. Statistics from Runto Technology reveal that in 2025, the combined TV shipments of four major foreign brands—Samsung, Sony, Philips, and Sharp—in China fell below 1 million units.

With such a sharp decline in market share, profits naturally could not hold up. Throughout 2025, Samsung’s division responsible for TV and home appliance businesses reported its first-ever loss, amounting to approximately RMB 926 million. Samsung itself stated in a notice to distributors that losses were the primary reason for the exit.

Interestingly, even at this stage, Samsung TVs were not exactly slow-moving in stores. Some distributors noted that Samsung TVs, priced RMB 2,000 to 3,000 higher than domestic brands, offered slightly wider profit margins. ‘Selling one or two Samsung TVs during good times could match the revenue from selling ten domestic brand TVs,’ one distributor said. What truly caused the continuous shrinkage of market share was a shift in overall consumer preferences.

According to a 2025 report by Accenture, the proportion of consumers prioritizing domestic brands in the home appliance sector rose from 33% in 2021 to 69% in 2025. It was not that Samsung suddenly encountered problems at a specific point; rather, the entire ecosystem for foreign home appliance brands was gradually thinning out.

Samsung’s lag in China’s home appliance market can be attributed to a specific misstep: it misjudged display technology trends.

In the late 2010s, Samsung judged that liquid crystal display (LCD) technology had reached its limits and began scaling back panel manufacturing, shifting its focus to OLED and Micro LED technologies. Meanwhile, domestic brands staged a comeback in the Mini LED segment. Data from Aowei Cloud shows that in 2024, China’s Mini LED TV sales reached 5.56 million units, accounting for 18% of the color TV market. By 2025, global shipments of this category hit 12.9 million units, up 67% year-on-year, with TCL, Hisense, and Xiaomi collectively capturing 62% of the global market share.

Samsung, however, was entirely absent from the mainstream price range of RMB 5,000, with comparable products still priced above RMB 15,000. Industry association observations suggest that Samsung lost its LCD supply chain layout, while Hisense and TCL both operate their own panel factories, giving them far superior cost control capabilities from panel to finished product.

Beyond pricing, responsiveness also proved to be a hurdle. Domestic brands could adjust features based on user feedback on a weekly or monthly basis, adding functions like Douyin (TikTok) screen casting and local streaming media compatibility. These changes, while seemingly minor, were key factors for many consumers when upgrading devices.

Samsung’s product decision-making authority rested with its Korean headquarters, often requiring a full quarterly approval process from feedback to implementation. By the time products reached consumers, competitors had already released multiple updates.

Yet, on the same day Samsung announced its exit from China’s home appliance market, it released a financial report that surprised the outside world. In the first quarter of 2026, the company reported consolidated revenue of KRW 133.9 trillion, up about 69% year-on-year; operating profit reached KRW 57.2 trillion, up about 754% year-on-year, with single-quarter profit exceeding the total for all of 2025. This performance was driven by its semiconductor business, with the DS division contributing about 93.8% of the group’s operating profit for the quarter.

Samsung’s position in the memory chip market determines its role in the current AI boom. According to TrendForce and Omdia data, in the fourth quarter of 2025, Samsung held about a 36.6% share of the global DRAM market and about a 28% share of the NAND flash memory market, both ranking first in the industry.

AI’s driving demand for memory chips continues to accelerate. TrendForce estimated in February this year that DRAM contract prices would rise by 90% to 95% in the first quarter of 2026. As the largest supplier, Samsung’s pricing power is evident.

While home appliances are incurring losses, memory chips are generating huge profits. The contrast makes the logic behind exiting China’s home appliance market clear: this is not a defeat but a resource reallocation after stopping losses. Capital market reactions confirmed this judgment, with Samsung’s stock price surging and its market capitalization breaking the $1 trillion mark on the day of the exit announcement.

The broader context is that Samsung’s departure is merely a phased outcome. In recent years, Sony transferred a 51% stake in its TV business to TCL, Toshiba sold its white goods business to Midea, and LG handed over channel operations to local agents.

The contraction of Japanese and Korean foreign home appliance brands in China is no longer an isolated case. Chinese brands have completed a two-decade journey from catching up to leading, with eight domestic manufacturers—including Hisense, TCL, and Xiaomi—capturing a combined 94.1% share of China’s TV market in 2025. Once this market landscape is established, there is virtually no realistic possibility for foreign brands to stage a comeback through head-on competition.

Disclaimer: The content of this article is for reference only. The information or opinions expressed herein do not constitute any investment advice. Readers are advised to make investment decisions cautiously.

-END-

-

![]()

Understanding 'Computing Power Inflation' in One Article: Why Is AI Getting Cheaper for You, Yet Computing Power Companies More Profitable?

-

![]()

The World is Re-evaluating China's Chips

-

![]()

Chongqing Releases 'Detailed Rules for the Administration of Expressway Testing of Intelligent Connected Vehicles (Trial)': Permitting L3+ Vehicles on Expressways: The 'Practical Examination' for Auto

-

![]()

Samsung’s Home Appliance Business: A Seemingly Inevitable Decline

-

![]()

Zhipu’s GLM-5V-Turbo ‘Crosses the Rubicon’: The Dawn of a Domestic Multimodal Agent War

-

![]()

Doubao Introduces Charges: Fewer and Fewer Purely Free Large Models

-

![]()

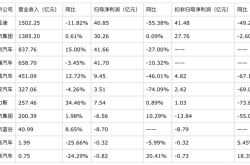

Q1 Financial Reports Released: Cumulative Profits of Ten Automakers Lag Behind CATL

-

![]()

Can Doubao's Paid Subscription Model Succeed?